ALC - Alcon: Lackluster Growth Given Its Valuation

2023-07-26 04:33:52 ET

Summary

- Alcon stock is currently trading at over 30x earnings, which is considered high for a company not expected to deliver EPS above 20 - 25% in the next few years.

- Despite the high trading multiple, Alcon has a strong business model and is a leader in the eye care industry, with recent positive developments in its product line and services.

- Alcon's share price is currently inflated due to hopes of significant free cash flow being diverted to shareholders, but I suggest this optimism may be misplaced and recommend a hold rating for the company.

Investment Outline

It seems that there are just some companies that keep on trading on high multiples and you never seem to get a pullback where you can add. In the long run, it might not matter that much to buy at higher premiums but I can't bring myself to see Alcon Inc. ( ALC ) as anything other than a hold right now. Paying over 30x earnings is quite high for a company that isn't necessarily expected to deliver EPS above 20 - 25% in the next few years, then I could understand it.

But ALC keeps trading at a higher multiple and the 5-year average p/e is 37. That isn't too much the multiple it's at now brings less risk. I find there to still be a risk that a pullback might unproportionally drag down the share price of ALC more in comparison to other major companies in the sector like Johnson & Johnson ( JNJ ) for example. This brings me to my rating for ALC right now, a hold but eagerly awaiting a pullback where a position potentially could be started.

Recent Developments

As ALC operates as a leader in the eye care space they are constantly developing new technologies to advance its product line and services. On the 6 of May , they announced some very positive news about a recent study they had performed. The study showcased that Clareon and Eyhance monofocal IOLs provide a similar range of vision which both includes distance and intermediate visual acuity. Positive developments such as these are what have guided ALC into being in the dominant position it has in the eye care industry.

{kind=link}

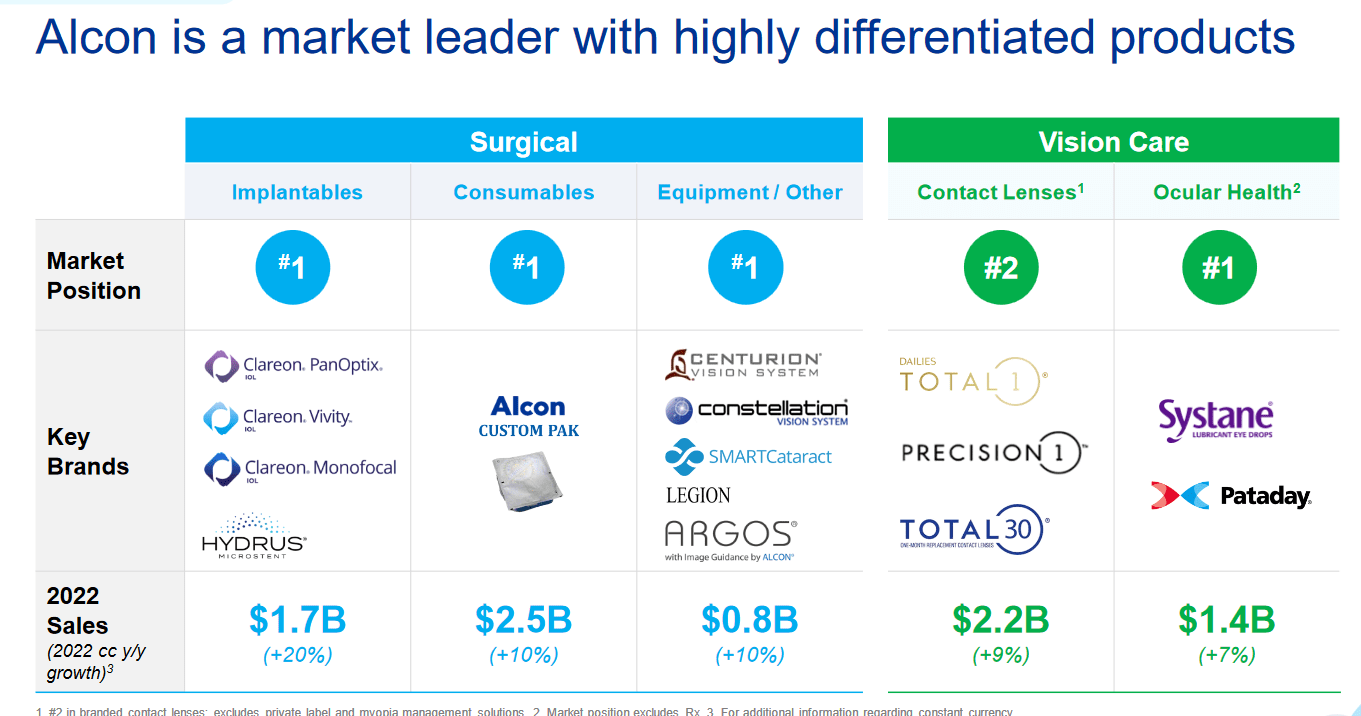

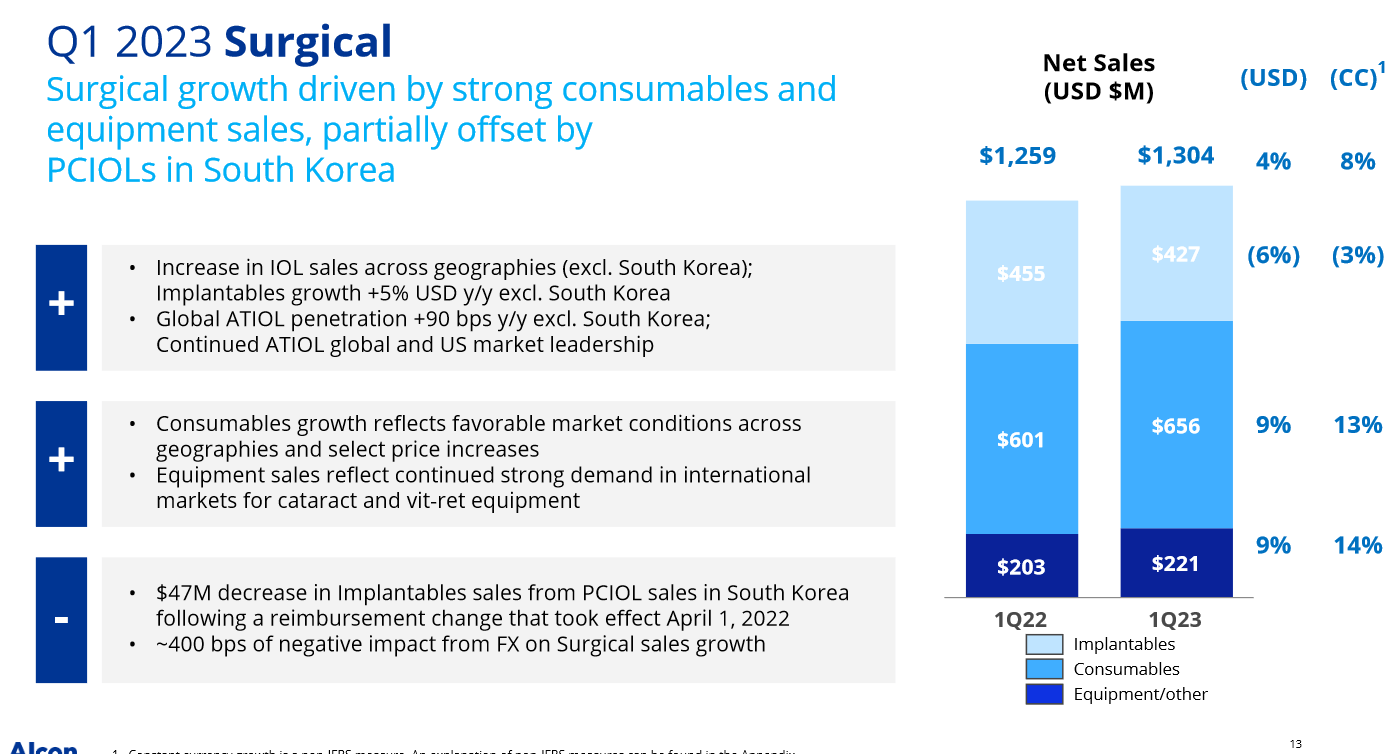

We are not that far off from the next earnings report from ALC, on August 17 the date has been set for the release of the Q2 results . I expect to see continued QoQ growth throughout the company and its segments. Looking at the results from Q1 of 2023 for some guidance the revenue mix consisted of Surgical making up the majority of revenues at $1.3 billion or 56%. Some of the growth drivers for the surgical segment came from increased sales in many key geographical markets. In South Korea though there was a $47 million loss as there was a change in reimbursements for PCIOL. This shouldn't however weigh on the results for Q2 and recovery should be visible.

{kind=link}

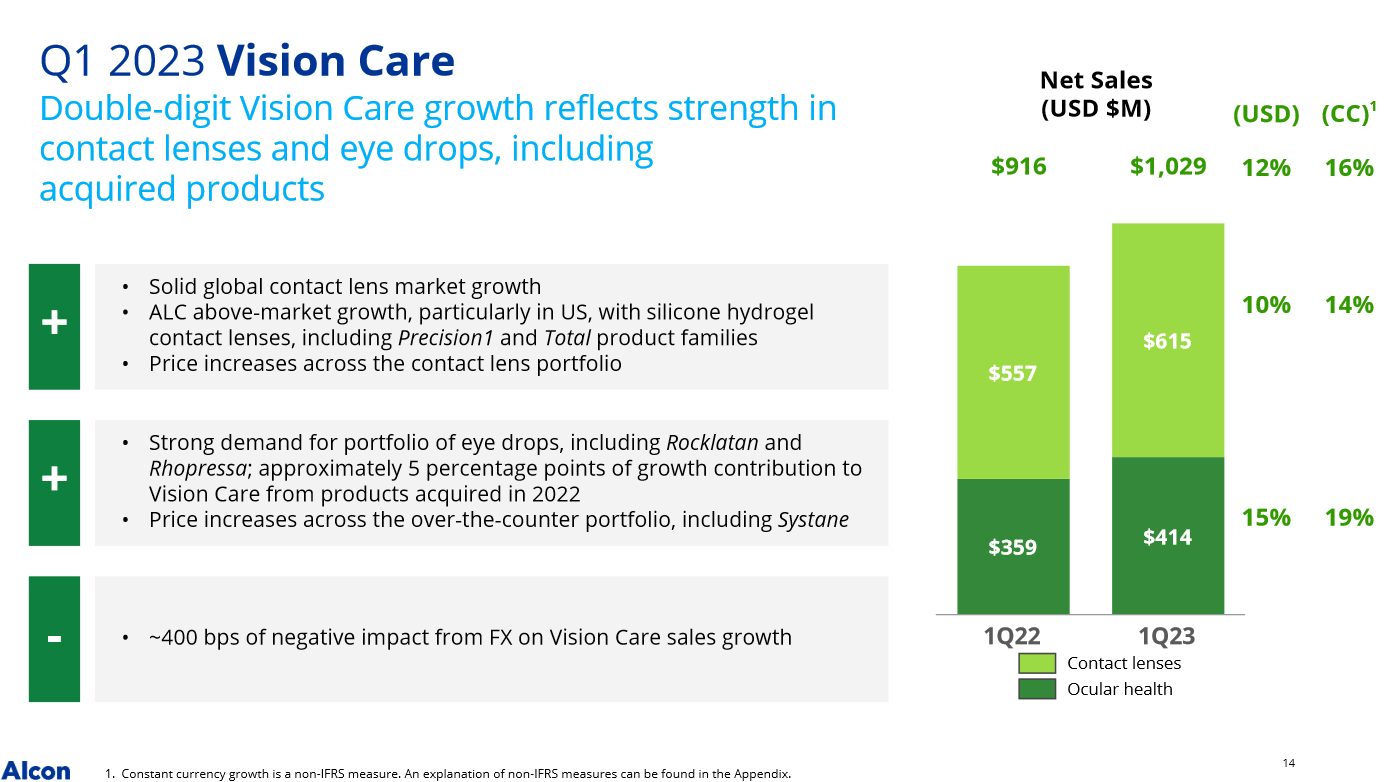

The rise of equipment and consumables for the surgical segment I think is a significant tailwind for the coming quarters. Consumables are quickly becoming a larger portion of the revenues here and positive study news like the above here it establishes ALC in the eyes of the consumer as a continued obvious choice.

Margins

Margin Profile (Seeking Alpha)

The margins for ALC are a highlight in my opinion. It is right now above many of its historical margins, despite a higher interest rate environment and inflation still being persistent and hurting operating expenses. It seems that ALC has been able to offset this somewhat though.

{kind=link}

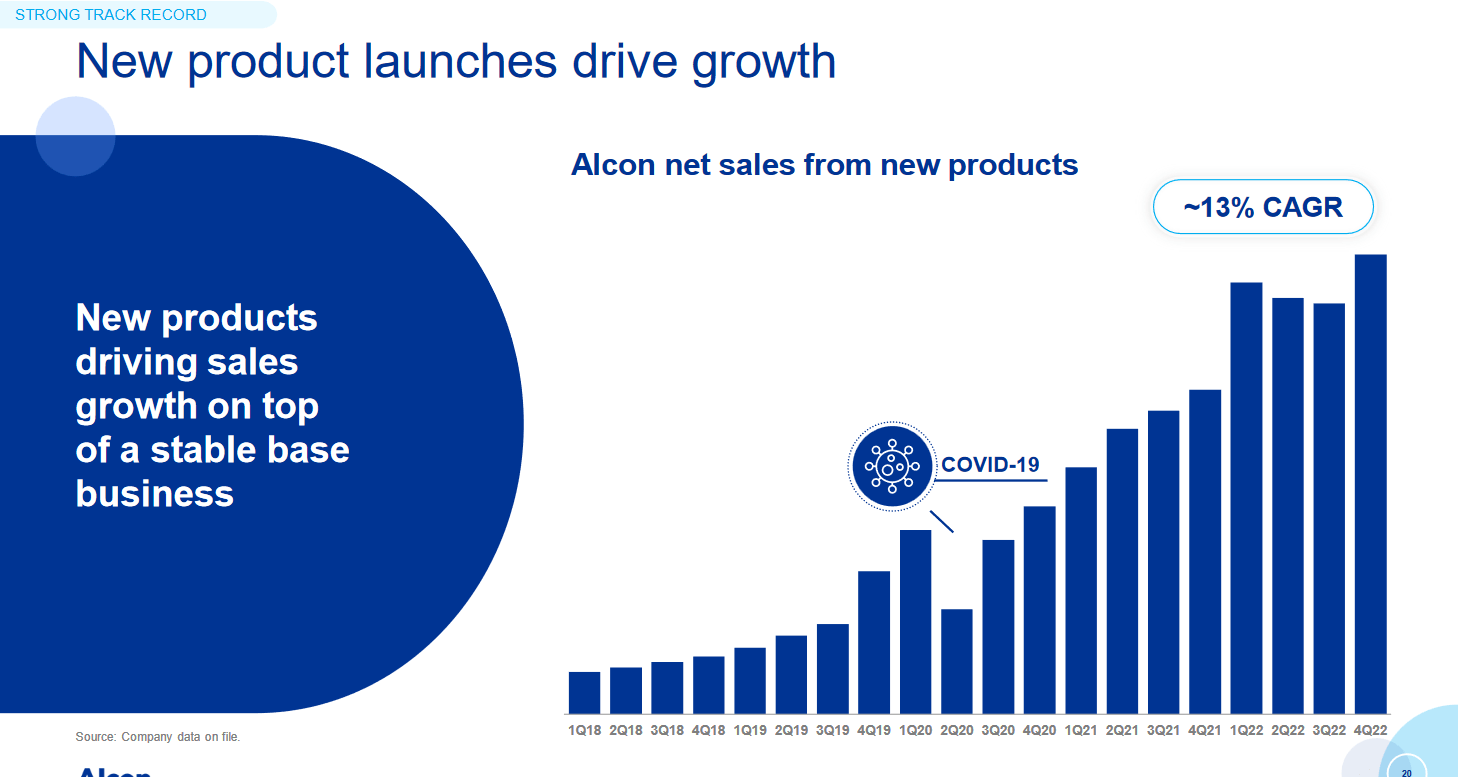

New products have been a significant reason why ALC has been able to grow the way it has. The CAGR of net income for the last 5 years sits at 5.53% right now which displays the impact that a continuously growing product line has on growth. This is setting ALC up very well to achieve its target of $2.2 billion in FCF by 2027. From 2022 that would be a very significant t increase, around 175%. This is where I can why ALC is trading so high right now. The hopes of a significant amount of these FCF diverted to shareholders are driving up the share price. If the sales for 2027 of $12 billion come true and they reach $2.2 billion in FCF that would be a margin of 18%. That seems quite high honestly, seeing as the TTM is under 10%. This brings me to have a slightly higher discount rate in the DCF model below here.

Valuation

DCF Model (Author)

Even though the hopes are high that ALC will be able to reach $2.2 billion in FCF by 2027, it doesn't mean that buying now would be getting it at a discount. As the DCF model above here concludes the intrinsic value currently is at $8.47 per share. ALC is trading around 10x that amount. I included a $2.2 billion in FCF by 2027 but I find it appropriate to also have a slightly higher discount rate at 1.1. The share price is trading high and the significant improvement in FCF from 2022 results seems optimistic. I also include the debt in the model as with a growing position currently at $4.5 billion there will need to be a large amount used for this rather than paying a higher dividend or buying back shares. That ultimately leaves less for the shareholders, which should mean a lower premium for the share price, but as we have seen the market has other ideas.

Risks

In the past, the vision care industry has maintained a steady growth rate of approximately 5%. However, considering the current macro uncertainties, Alcon is being cautious and expects the market growth to be slightly below its historical rate in the latter half of 2023. This conservative approach reflects the company's prudence amidst the ever-changing economic landscape.

{kind=link}

Nonetheless, I remain optimistic about Alcon's prospects as they possess the potential to not only sustain but also expand their market share. Their focus on the ATIOL (Advanced Technology Intraocular Lens) market provides them with a competitive advantage, enabling them to outpace the overall market growth. As advancements in vision care technologies continue to evolve, Alcon's commitment to innovation positions them for continued success in meeting customers' needs and driving further growth.

Investor Takeaway

ALC is like we have discovered to be one of those companies that just keep on trading at a very high multiple no matter what happens in the market. The reliability of the business model is a big appeal but is it worth paying the 30x earnings premium for, to me no unfortunately not. I think there are better options out there that might yield better returns over the long term.

I want to make it clear though that I recognize the incredible business model that ALC has set up and their dominant position lends them ability to continue growing its dividend and buying back shares. A hold rating seems the most reasonable seeing as ALC will likely continue to report YoY growth, but not at the rate which would make me view them as a buy.

For further details see:

Alcon: Lackluster Growth Given Its Valuation