ALC - Alcon: Rich Premium For Low Growth

2023-05-15 08:24:01 ET

Summary

- Alcon has experienced consistent revenue growth in recent years, the stability of both the company and the industry doesn't warrant a compelling investment case at its current valuation multiples.

- The eye care industry is a worldwide market that may not experience any catalysts, but consistent growth year after year.

- While I appreciate the company's stability, I am not convinced that the current premium is fair to pay. Nevertheless, I think a hold rating is fair for now.

Investment Thesis

Despite experiencing a significant increase in share price from its March lows, Alcon Inc. ( ALC ) still has the potential to provide attractive returns to investors. The company has established itself as a leader in the eye care industry, operating in a market that is expected to grow at a 5% CAGR between 2022 and 2027. ALC is well-positioned to capture this growth and generate similar numbers as they have done in the past, with a 5.5% CAGR in net sales from 2019 to 2022.

However, the current forward P/E ratio of over 30 makes it challenging to justify a strong buy recommendation. Therefore, I believe that a hold rating is appropriate until we see a reduction in valuation, which could create a series of long-term opportunities for investors.

The Market Forecast

While the eye care market may not be experiencing explosive growth like some other industries, it is expected to maintain a steady 5% compound annual growth rate until 2027, as reported by the company itself. Alcon, with its strong position and various brands, should be able to achieve top line growth that matches or exceeds the industry CAGR. An EPS growth higher than 5% could very well be possible if the company starts to buy back shares with the large amount of FCF they have.

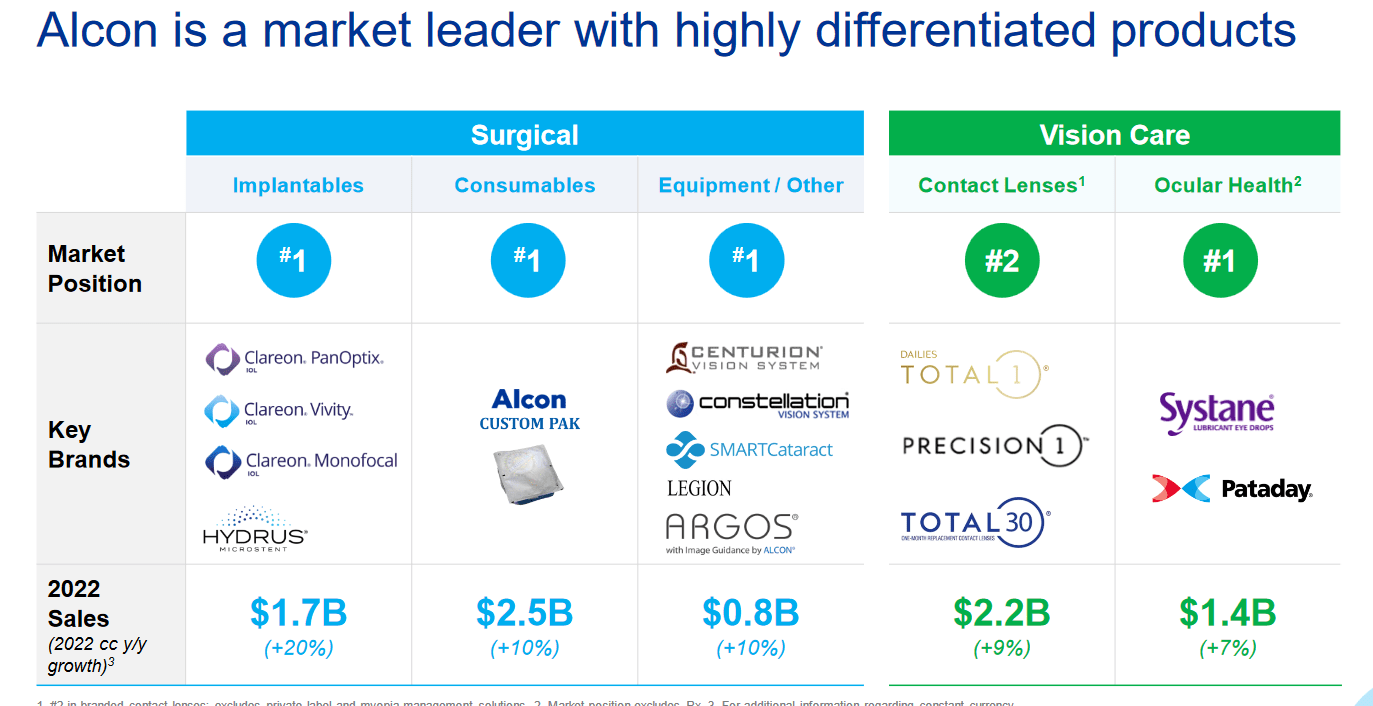

Market Position (Investor Presentation)

{kind=link}

Alcon holds a major position in all markets except for contact lenses, but they dominate the markets with the highest estimated CAGRs. The company aims to increase its free cash flows to $2.2 billion by 2027, a significant improvement from the just under $900 million levered cash flows they had in 2022. While Alcon's reputation for share buybacks has been poor in the past, as the outstanding shares have been increasing YoY, driven also by stock based compensations, amounting to $140 million in 2022. A transition into generating significant amounts of free cash flows by 2027 should make it easier to create long-term value for shareholders through buybacks and dividends.

One of the reasons for the continued need for eye care is the increase in eye disorders worldwide, and more people are able to afford the necessary care. Contact lenses, for example, are not a one-time purchase , and there is no indication of a slowdown in the market growth. Companies such as Alcon will be able to pass on costs to consumers due to the essential nature of the products they provide.

Decent Fundamentals

Since 2016, Alcon has been able to deliver consistent revenue growth with the exception of 2020, a challenging year for many companies. The company's leading position in the eye care industry, backed by a diverse set of brands, has been instrumental in achieving this growth. ALC's net margin of 3.84% in 2022 is both sustainable and leaves room for improvement. The company's optimistic outlook on free cash flows also suggests an ability to increase margins.

Cash Flow Statement (Earnings Report)

{kind=link}

One concern is the decreasing cash position from 2021 to 2022, dropping nearly $600 million to $980 million despite generating almost $900 million in free cash flows and diluting shares. This raises questions about whether the company is considering buying back a significant number of shares. In my opinion, this could be a viable strategy that would create value for long-term shareholders. A plan like this shouldn't be hindered by the long-term debts of $4.5 billion, because if the company achieves their projected FCF by 2027, they would be generating almost half their long-term debt as FCF. At a net debt/EBITDA of 2.19, Alcon's debt levels appear manageable.

Rich Valuation Seems Unsupported

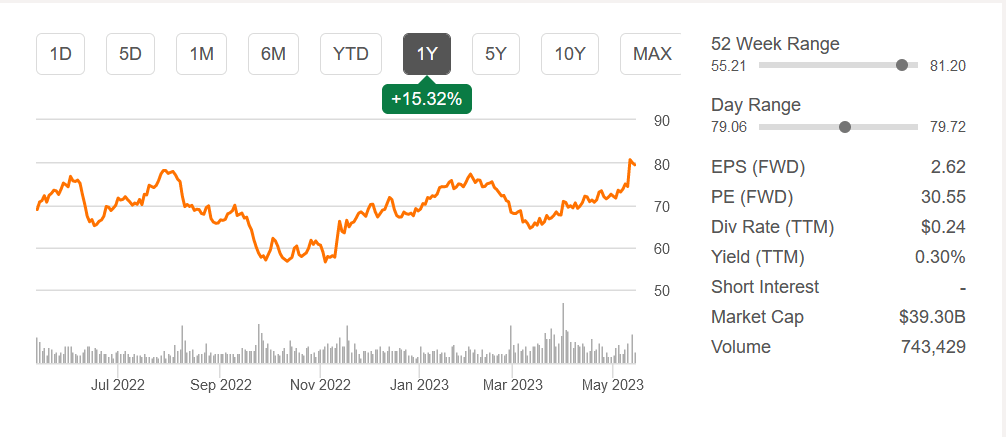

Regarding the company's valuation, I previously mentioned that I don't believe the current price justifies a strong buy case. Although the forward P/E is decreasing, it is still quite high at 30x earnings, which is a significant premium to pay for a company that is not part of a rapidly growing industry. However, the stability of the company has likely contributed to this high valuation. The p/FCF ratio for the TTM sits at 31, but the company aims to more than double its cash flows by 2027, which would bring the price-to-cash-flow ratio down to around 16. While this is not a high price to pay necessarily, it is still a ways off.

In my opinion, the company's stability has played a significant role in driving up the share price. However, paying a high premium for a quality company is not always necessary. A pullback in the share price is not out of the question, and a price-to-earnings ratio of around 18-19x earnings seems like a better deal. For comparison, a smaller company like National Vision Holdings ( EYE ) has a forward P/E of 37 and a much lower net margin of 2.1%. Additionally, EYE has negative cash flows, and earnings forecasts are uncertain. Breaking into the market is challenging, and I believe that established companies like ALC have the capital to maintain their position and limit competition in the industry.

Company Risks

One potential risk of investing in ALC is the company's history of share dilution, which may not seem significant at less than 0.5% per year but can dampen growth prospects. As an established company, ALC should allocate capital in a way that satisfies investors. Additionally, the high premium price makes the stock vulnerable to a significant pullback if market conditions change. Trading at a forward P/E of 30x, ALC lacks sufficient support to justify its valuation, and any missed targets or negative developments could exacerbate this issue. Despite ALC's optimistic outlook on cash flows and growth potential, there are economic and inflationary pressures that may impede progress in 2023. Therefore, it may be prudent to wait for a pullback before investing in ALC, ideally at around 18-19x earnings.

Conclusion

Alcon Inc. is a well-established company with a dominant market position in several segments of the eye care industry. However, the growth rate of the industry is not very high, and while ALC may be able to match it, the high premium currently required to invest in the company is a concern for me.

{kind=link}

A forward P/E of around 30x, with expected double-digit growth, is not reasonable in my opinion. Nonetheless, the company's stability and long history of steady growth lead me to believe that a hold rating is appropriate at this time.

For further details see:

Alcon: Rich Premium For Low Growth