ALC - Alcon: The Steady Force Of 'Boring'

2023-06-27 18:49:46 ET

Summary

- Alcon is expected to outpace market growth and gain market share in the surgical and vision care sectors, with growth driven by factors such as the increasing global aging population and rise in myopia.

- Along with Costco, Aon, and Marsh & McLennan, Alcon is another "boring" investment in my portfolio.

- Alcon's focus on R&D, product innovation, and accelerated free cash flow generation contribute to a positive outlook, earning a "Buy" rating.

To My Dear Readers:

To my readers, I have some "boring" companies in my portfolio, including Alcon ( ALC ), Costco ( COST ), Aon ( AON ), and Marsh & McLennan ( MMC ). These companies consistently generate 4-6% organic sales growth, regardless of the macroeconomic conditions. Additionally, they benefit from margin expansion through tuck-in acquisitions or new store openings, resulting in double-digit earnings growth over the course of the business cycle. Based on my investment experience, investing in these stocks can provide tremendous downside protection during market sell-offs.

Alcon is the market leader in most of its cataract surgical device and vision care markets. Since its spinoff from Novartis in 2019, I have been a shareholder of Alcon. Following the spin-off, Alcon has made significant investments in R&D, as well as new products, while also transforming its legacy IT systems. As a result, their capital expenditure has already reached its peak, and I anticipate a growth acceleration in their free cash flow in the coming years.

According to Alcon's estimates, the market is expected to grow at a mid-single-digit rate. However, I believe that Alcon has the potential to outpace market growth by gaining market share in both the surgical and vision care sectors. The global penetration of advanced technology intraocular lenses remains relatively low, presenting ample opportunities for Alcon's growth.

{kind=link}

Growth Catalysts

Growing cataract procedures : Historically, global cataract procedures have grown at a rate of 5% annually. This growth is primarily driven by factors such as the increasing global aging population and the rise in myopia due to the extensive use of electronic devices. Alcon projects that approximately 50% of the global population will have myopia by 2050. Furthermore, it is worth noting that 90% of visual impairments can be prevented or cured, with cataract procedures and contact lenses playing a significant role in addressing vision impairments.

US ATIOL Penetration Growth : Alcon's recent survey data suggests that the penetration of advanced technology intraocular lenses (ATIOL) in the US could potentially reach as high as 35%. Currently, the penetration rate stands in the high teens, indicating substantial room for growth in the US ATIOL market. In Q3 2019, Alcon held a market share of 28%, but with the introduction of new products and advancements, their market share surpassed 31% by the end of 2022.

Daily disposable contact lens : The daily disposable contact lens market constitutes approximately 60% of the total contact lens market and is experiencing faster growth compared to reusable contact lenses. The convenience factor associated with daily disposables is a significant driver for consumers. Before the spin-off, Alcon had no investment in the daily disposable business, resulting in a loss of market share to Cooper ( COO ). However, since the separation, Alcon has invested in research and development, launching products such as Precision 1, Total 30, and Total 1 Toric. As a result, Alcon has gained around 250 basis points of market share in the global daily toric contact lens market. Currently, Alcon holds approximately 29% of the global market share in the disposable contact lens segment, which is the fastest-growing segment in the contact lens market.

Pricing Growth : Alcon has demonstrated its ability to pass on cost inflation to its customers. In Q1 '23, they witnessed sales growth driven by pricing, particularly in consumables, contact lenses, and ocular health products. Price increases accounted for approximately one-third of their top-line growth during that period. On the surgical side, Alcon had limited pricing flexibility before the onset of the Covid-19 pandemic, as most of their long-term contracts lacked price escalation clauses. However, they have since begun incorporating pricing clauses into these contracts. Additionally, approximately one-third of their consumables were sold on a stand-alone basis without contracts, providing Alcon with the ability to adjust pricing accordingly.

Peaked Capex spending : Following the spinoff from Novartis in 2019, Alcon initiated the upgrading of its legacy IT systems, such as ERP systems. Consequently, their capital expenditure spending exceeded normal levels. In 2019, they spent only $676 million on capex, but this figure surged to $1.18 billion in 2021 before peaking. Since then, their capex spending has begun to decline. Despite several one-time payments expected in 2023, including transformation and a legal settlement, Alcon anticipates significantly improved free cash flow compared to 2022. Reduced capex spending will contribute to higher free cash flow in the future, with Alcon projecting $2.2 billion in free cash flow by 2027, implying a 35% compound annual growth rate from the 2022 level.

Near-term Headwinds

Overall, I perceive Alcon as a rather "stable" company, and I believe their organic sales growth rate is slightly higher than the market growth rate of 5%. This means that I do not anticipate any significant earnings surprises from Alcon on a quarterly basis. However, with some tuck-in M&A deals, I expect them to deliver sales growth in the mid-to-high single digits and double-digit free cash flow growth, according to my forecast.

Slowdown in Vision Care business : Historically, the vision care industry has grown at a rate of around 5%. Due to current macro uncertainties, Alcon considers it prudent to assume that the market will grow slightly below its historical rate in the second half of 2023. However, I believe Alcon has the potential to continue gaining market share and increasing penetration in the ATIOL market, allowing them to grow faster than the overall market. Additionally, I view the demand for contact lenses as relatively resilient to macroeconomic conditions.

Reimbursement Policy Change in Korea : There was a reimbursement policy change for surgical implants in Korea last year, resulting in higher out-of-pocket expenses for many Korean patients. This policy change has caused some fluctuations in year-over-year comparisons. However, it's important to note that Korea represents a small market for Alcon, accounting for a low-single-digit percentage of their total revenue. Alcon's largest foreign markets outside the US are Japan and China.

Outlook & Valuation

Alcon's financial targets of reaching $12 billion in sales, achieving a mid-20s core operating margin, and generating $2.2 billion in free cash flow by 2027 appear reasonable and attainable. The projected 35% compound annual growth rate for free cash flow from 2022 to 2027 suggests a strong growth trajectory. This growth is expected to be driven by various factors, including sales growth, margin expansion, stabilization of capital investments and inventory levels, as well as the successful completion of transformational and new business integration initiatives. Considering these factors, I agree that Alcon's financial targets are realistic and within reach.

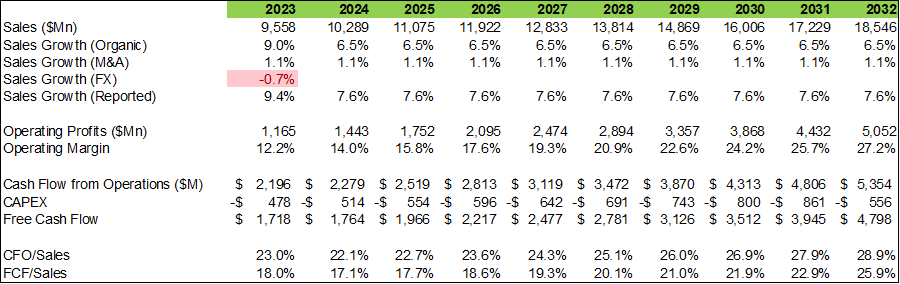

In my two-stage DCF model, I assume 6.5% of organic sales growth, 1.1% of M&A growth, 10% of WACC, 20% of tax rate, and 4% of terminal growth rate.

In the model, the operating margin is estimated to reach 27.2% in 2032, and cash flow conversion to reach 25.9% in 2032.

Alcon DCF Model, Author's Calculation

{kind=link}

With these assumptions, the present values of FCFF over the next 10 years and terminal value are $11.7 billion and $34 billion, respectively. Adjusting the debt and cash, the fair value of Alcon's stock is $91 in the model.

Alcon DCF Model, Author's Calculation

Conclusion

In summary, Alcon operates in a stable growth industry and their focus on R&D and product innovation positions them for higher sales growth than the overall market. With their peak capital expenditure phase in the past, Alcon is expected to accelerate their free cash flow generation. While considered a "boring" company, these factors contribute to a positive outlook. Considering the fair value, I assign Alcon a "Buy" rating.

For further details see:

Alcon: The Steady Force Of 'Boring'