ALEX - Alexander & Baldwin: Maintaining Its Moat On The Hawaiian Islands

2023-06-19 07:48:42 ET

Summary

- Shares in Alexander & Baldwin (“A&B”) remain in a narrow trading range. But they are outperforming much of their peer set.

- Market dominance in the Hawaiian Islands continues to provide a protective moat to their core business.

- A&B can rise higher from current trading levels. But ongoing efforts to dispose of a discontinued unit creates near-term uncertainties.

- Though I view shares favorably, I find it best to wait until the disposition is ultimately completed before engaging in any new or further positioning on the stock.

Alexander & Baldwin ( ALEX ) (“A&B”) is treading water and living the island life.

ALEX stock is little changed since a prior update , flat YTD, and up about 5% over the past year.

YCharts - Recent Price History Of ALEX

While this could be frustrating for some investors, it’s comparably better than many of their retail-based peers. Names such as Acadia Realty Trust ( AKR ), Federal Realty Investment Trust ( FRT ), and Regency Centers ( REG ), for example, were all negative on a YTD basis through the week ended June 16, 2023. The results are more mixed over the past year, with REG up 7%. AKR, on the other hand, is down nearly 10% and FRT is up about 2.25%.

A&B has the potential to rise higher from current trading levels. But I believe it is being held back by the uncertainty surrounding the ongoing efforts to sell Grace Pacific and their Maui Quarries (“Grace”). The company also lost an industrial tenant during Q1, which created a drag on their leased rates. And they have near-term maturities on their secured debt in 2024. Until these three open areas are resolved, I view it best to “hold” shares.

The Grace Disposition

Prior to December 31, 2022, A&B operated and reported on three segments, one of which was Materials & Construction (“M&C”). As part of a recent simplification of their business, A&B discontinued this segment. The results of operations are now separately reported below the line.

At present, the unit is being marketed. More specific details are unknown. But I view it as likely that any deal will get done this year. In February, A&B announced a leadership transition . As part of this, current CEO, Christopher Benjamin, is set to formally retire on June 30, 2023, but will serve through the end of the year in a consultant capacity to the new incoming CEO, Lance Parker.

Given the changeover, I can’t envision the new CEO being bogged down by legacy operations. A fresher start makes more sense. When questioned on their Q1 release, Benjamin said that he does expect A&B to be out of Grace by the end of the year but did emphasize that it wouldn’t be at “whatever it takes.” In other words, the unit isn’t expected to be sold at prices less than what it’s believed to be worth.

Using Proceeds For Debt Repayment

Where they ultimately will recycle the proceeds is viewed to be a key determinant of the stock’s outlook. From a liquidity standpoint , the company has about +$470M in dry powder. That’s about equivalent to their total debt outstanding. I, therefore, believe A&B is on strong financial footing. A modest leverage ratio of about 5x (excluding their land operations in M&C) further reinforces this.

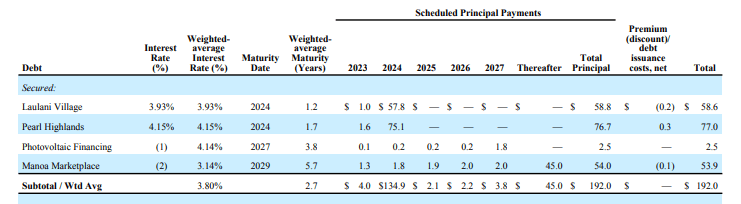

The proceeds will add to their existing liquidity position. A&B will then have options. They have two larger secured maturities coming due in 2024. Would they direct the proceeds to the debt paydown? At the end of 2022, A&B entered into swap agreements, which enabled them to lock in a blended interest rate of just under 5%. It’s unlikely, then, for the proceeds to be recycled here.

Q1FY23 Investor Supplement - Debt Maturity Schedule

{kind=link}

Using Proceeds To Grow Industrial Portfolio

They could expand their portfolio through acquisitions. Recently, they acquired an industrial asset at a 5.6% cap rate via a sale-leaseback transaction to a local bottling and storage operator. The terms of the lease include a 3% annual escalator over a term of 10 years.

The acquisition will add to their industrial portfolio, which already represents about 17% of their portfolio net operating income (“NOI”). Looking ahead, I can see this share increasing to a fifth of total operations. The growing exposure is important, as the market size is estimated to be around 60 MSF. Currently they own just 1.3 MSF or 2% of that share.

Average rents in the Hawaiian industrial market also run higher than the national average. Currently it’s about $15.70/psf. That’s about 60% above what their industrial counterparts command. The second highest title is held by Rexford Industrial ( REXR ), which operates in the infill Southern California market. And their rates are still over a dollar less, at $14.35/psf.

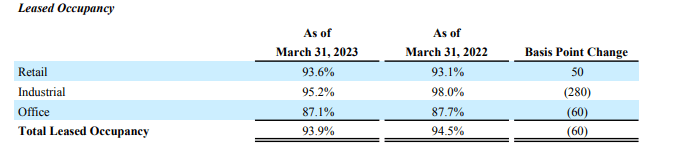

A&B’s higher rates, however, can create tenant strain, especially if the market begins to turn. In Q1, A&B lost one tenant through natural expiration. Given the demand for space, it’s surprising the tenant didn’t renew. Perhaps the higher rate factored into the decision making. The loss resulted in a 60 basis points (“bps”) takeaway from the overall portfolio leased rate, which stood at 93.9% at the end of Q1.

Q1FY23 Investor Supplement - Summary Of Leased Occupancy At Period End

{kind=link}

The industrial vacancy rate is currently 0.81% in the Hawaiian market. That’s well below the national average. I, therefore, don’t expect A&B to have issues backfilling the space. But Parker did state that a few specialized improvements would need to be made to accommodate the changeover in tenancy. Proceeds from the eventual sale of Grace could be directed at the leasing efforts. I wouldn’t, however, view that as accretive unless A&B was able to capture a significant mark-up on the new lease. Based on the last call, it appears investors would have more insight into that on the Q2 release.

Using Proceeds To Grow Retail Portfolio

A&B could also employ resources to their core business, which entails their retail/grocery component. This brings in about 65% of their annual NOI. Currently, they have one development, which appears to be progressing as expected and is expected to be completed in Q3.

Aside from this project, A&B doesn’t have an active pipeline. But they do see additional value-add opportunities and do expect to announce more projects in the future. The offloading of Grace will enable them to focus their efforts on any new initiatives.

There is also upside potential in acquiring additional grocery or drugstore anchored properties. Currently, they own 2.2 MSF of an estimated 10 MSF market. Increasing their share here could create a favorable runway for growth.

In Q1, they realized blended spreads of 6% on their retail leases and generated overall same-store NOI growth of 2.2%. Additional market share gains in combination with pending commencements can drive this figure higher in future periods.

Is ALEX Stock A Buy, Sell, Or Hold?

Looking ahead, A&B maintained their previously stated full-year guidance. This sees core FFO at a midpoint of $1.11/share, with same-store NOI growth between 2% and 4% or between 5% and 6.5% when excluding the impact of prior year reserve reversals.

At current trading prices, A&B fetches a multiple of 16.8x forward FFO. While this represents a premium to peers, I believe it’s supported by their wide-moat in the Hawaiian market, as well their high share of NOI derived from industrial assets. In addition, the company also derives 15% of their business from ground leases, which provides a protective barrier to their reoccurring revenues.

The eventual sale of Grace is expected to benefit A&B. In Q1, the unit turned in a +$4.2M loss due to a slow start to the year due to weather and project commencement delays. By recycling out of this segment, A&B’s operating results will be less exposed to variability, such as that experienced in their paving business.

On their Q1 discussion, current CEO, Chris Benjamin, noted that they’re actively engaged with a bidder on the unit. This provides some degree of confidence regarding interest. But I still would find it more prudent to wait until the deal is completed before new or further initiation on A&B. This will provide investors with time to assess the impact of the deal. Was it sold at favorable prices? Or was it a more desperation-type sell? Investors could also get a sense of where the proceeds will be recycled into. New acquisitions? Debt paydown? Internal developments?

Until these uncertainties are clarified, investors may find it best to soak up the island vibe from the mainland.

For further details see:

Alexander & Baldwin: Maintaining Its Moat On The Hawaiian Islands