ARE - Alexandria Real Estate: A Fast-Growing And Fairly Valued REIT

2023-11-02 20:15:42 ET

Summary

- Alexandria Real Estate Equities specializes in developing Class A/A+ properties for the life science, agtech, and advanced technology industries.

- Despite the challenges faced by office REITs, it has shown strong performance and provides a safe dividend yield.

- Unfortunately, there is no discount to NAV to offer a margin of safety here, though the stock price is historically low and represents fair value.

Alexandria Real Estate Equities, Inc. ( ARE ), founded in 1994 and headquartered in Pasadena, CA, is an office REIT that develops Class A/A+ properties intended for leasing to corporations involved in the life science, agricultural technology, and advanced technology industries.

There is an impressive growth story to be told here and this is one of the most conservatively financed REITs out there with great liquidity to weather any storm. Further, the dividend is very safe based on both the historical distributions and the payout ratio. However, I look for REITs that the market offers at a NAV discount. This is not the case here, so I am rating the stock as a HOLD. But let's take things from the beginning.

Portfolio

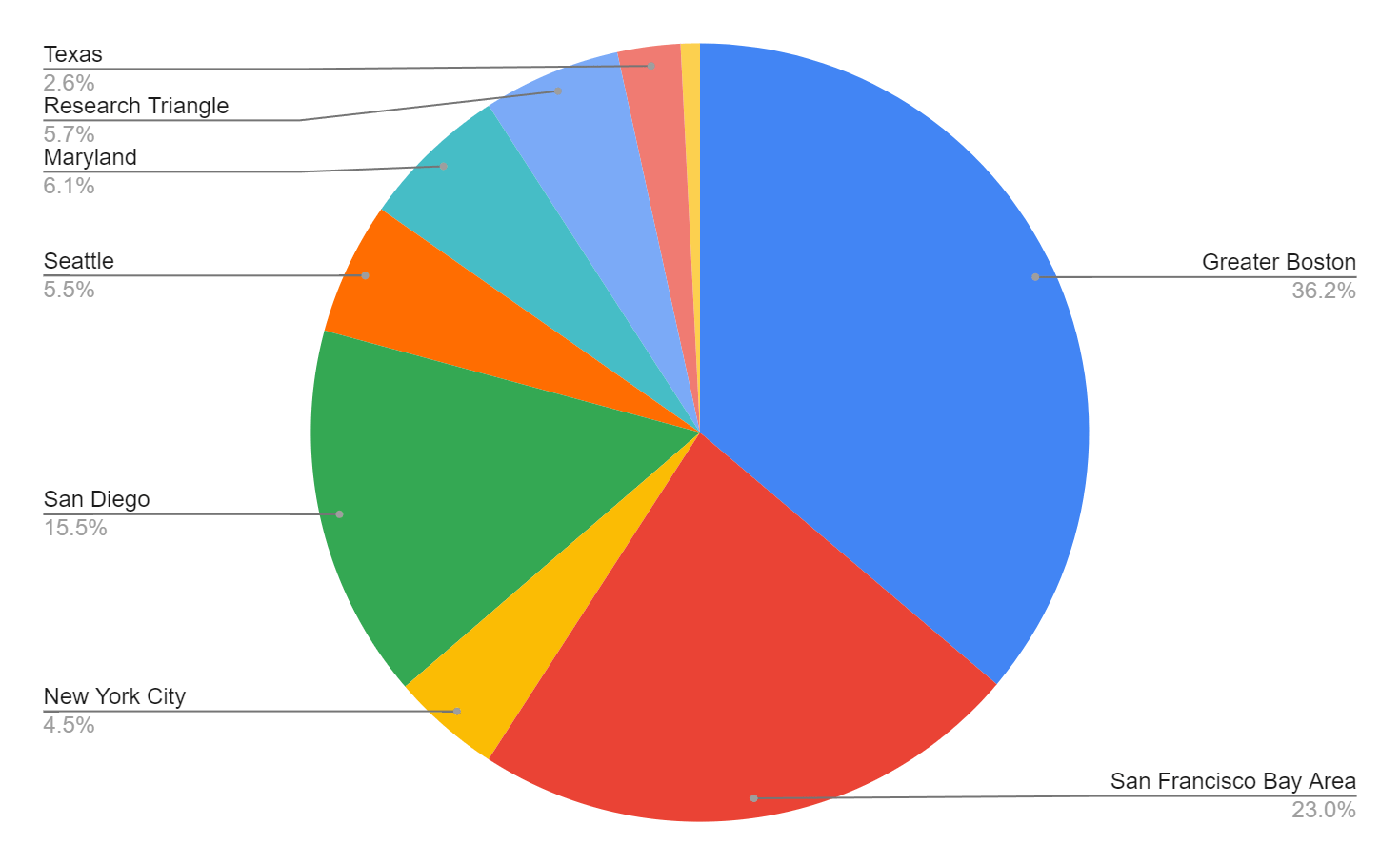

Alexandria Real Estate has properties in Greater Boston, San Francisco Bay Area, San Diego, Maryland, Research Triangle, Seattle, New York City, Texas, and Canada, all together amounting to about 75 million sqft.

As of the end of the third quarter, it was reported that 49% of the REIT's annual rental revenue came from Investment-grade or publicly traded large-cap tenants. Its biggest tenants include Eli Lilly, Moderna, Alphabet, Harvard University, Uber, AstraZeneca, Pfizer, and the U.S. Government.

To be fair, Alexandria is concentrated in the Greater Boston and San Francisco Bay areas as well as San Diego based on its rental revenue:

{kind=link}

However, both its resilient tenant base and its focus on industries that some office landlords try to focus on as a hedge make its portfolio very attractive to own.

Performance

When it comes to its occupancy, it decreased to 93.9% for the 3rd quarter from 95.3% for the same period in 2022. But it is still higher than what we often see with office REITs these days.

Though vacancy expansion is something that may be scaring many investors away from office REITs these days, the tenants that Alexandria targets are very reassuring of the long-term potential. An equally degree of confidence can be offered by the REIT's historical operating performance:

The confidence these trends inspire is enhanced by more recent results. Rental revenue in the third quarter annualized for instance reflects a 29.38% increase from the average of the annual figures in the last three years.

In the chart above, you can see the almost 100% growth marked by operating earnings since 2019. A more important figure to watch out for, however, is same-property cash net operating income, which excludes income from relatively new leases and adds back non-cash expenses. Growth is also observed here as same-property cash NOI in Q3 annualized represents a 34.16% increase from the past 3-year average.

Last, Q3 AFFO annualized is 35.18% higher than the average annual AFFO of the last 3 fiscal years; a very impressive growth that partly contributes to the safety of the current dividend. But we'll talk about that in a minute.

Leverage

What I most appreciate about Alexandria Real Estate after its performance is the way it handles debt. Its Debt/Assets ratio is currently ~29%; it almost seems there was a conscious effort by management to bring leverage so low over the past decade. Consequently, Debt to EBITDA is at a very attractive 5.4 multiple.

Similarly impressive is its interest coverage growth over the years, today at 8.1x. Coupled with the upward trend of operating income, such coverage could be supported by the REIT's relatively low cost of debt; its debt currently consists of secured notes amounting to about $110 million and unsecured senior notes of approximately $11 billion, which carry a 3.7% weighted-average interest rate.

Its maturity schedule also looks good. The next balloon payment is ~$600 million and comes due in 2025. In 2026, the amount that matures is a bit higher at ~$760 million and ~$350 million matures in 2027.

Dividend & Valuation

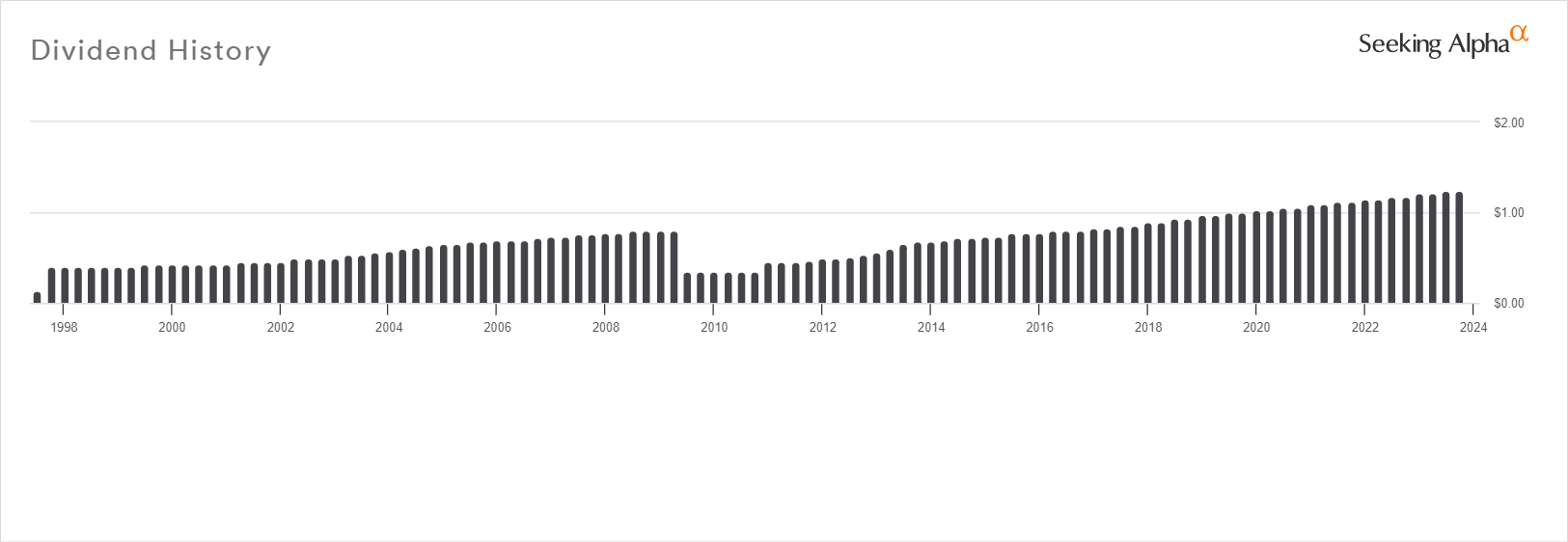

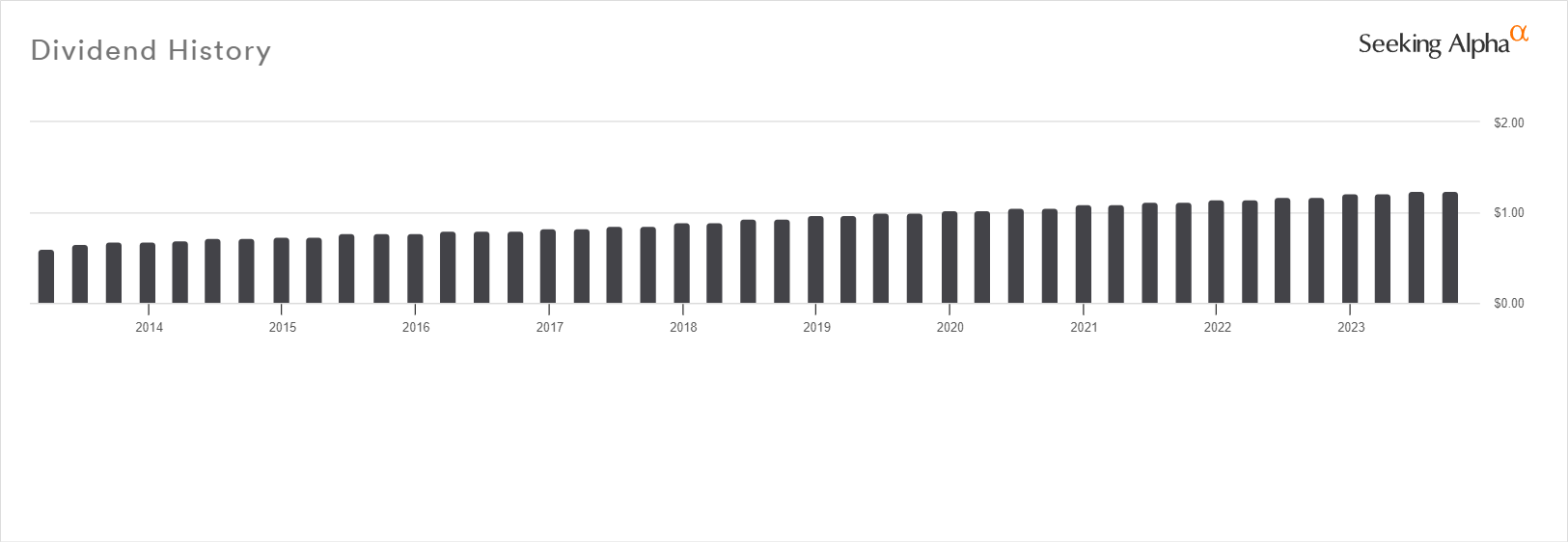

Alexandria pays a quarterly dividend of $1.24 which results in a 5% forward yield. I believe this to be safe for several reasons.

First, the REIT has been pretty consistent in paying a dividend for 25 years:

{kind=link}

Second, it has been increasing it for 12 years in a row:

{kind=link}

Last, its payout ratio is at 34.61%, which leaves plenty of room for further dividend growth as well as expansion.

Now, it's true that the yield doesn't represent a great value these days. That's further expressed by Alexandria's FFO multiple, which is low enough for my taste, but it is high on a relative basis:

However, I wouldn't go as far as to say that ARE is overvalued just because of this. The competitors listed above simply don't enjoy the portfolio and tenant base that Alexandria does. For this reason, I see ARE as fairly valued right now which is at least weird in my opinion as the management of the REIT's assets deserves a premium; I think we have the fearmongering regarding office space to thank for that.

The 5.49% implied cap rate that ARE is trading at pretty much agrees with the rate I would use to value its assets (around 6%), so it confirms the stock as fairly valued.

Risks

The problem with "fairly valued" is the lack of a margin of safety which always discourages me from investing in a company. So, the most obvious risk is related to this.

Another risk is the currently high Federal Funds rate which has been inversely correlated with the downward pressure of many REIT stocks' prices since the Fed started its hike cycle in 2022:

Even if there are no further hikes on the table, until we see some cuts stock prices may remain depressed. This naturally leads to an opportunity risk too.

For what is worth, some opportunity cost has been already realized by anyone who may have held ARE in the last decade as SPY didn't lag far behind. The alpha that ARE has provided isn't much to drool over. You could buy SPY and sacrifice a little of the performance for far a much higher safety of principal.

Verdict

Therefore, I assign a HOLD rating for ARE right now, subject to change if it falls anywhere near $60 per share, which would represent about a 30% discount to NAV based on a 6% cap rate.

To be clear, the price at which the market currently offers ARE could be one we will not see for a very long time. I believe that there is a mispricing in place. However, no mispricing will motivate me to buy unless it offers a margin of safety. It's entirely personal and you may not assess risk the same way I do, leading you to believe that this is a rare opportunity. The HOLD rating is within the context of my own risk tolerance.

What's your view? Do you own ARE or intend to? Also, let me know if this article was helpful (or not). I appreciate the feedback. Thank you for reading!

For further details see:

Alexandria Real Estate: A Fast-Growing And Fairly Valued REIT