ARE - Alexandria Real Estate: Last Call?

2023-12-10 07:00:00 ET

Summary

- Alexandria Real Estate Equities stock offers a compelling upside despite its current high valuation.

- The company has strong fundamentals, including liquidity, low debt, high occupancy rates, and diversified assets.

- Alexandria is a dominant landlord in the life science industry, which has a high level of spending and demand for specialized real estate.

This article was co-produced with Wolf Report.

We recently wrote an article where we posited that it might be a good "last chance" to get into VICI ( VICI ) at a low valuation.

Since we're seeing the same sort of possibilities with Alexandria Real Estate Equities ( ARE ), we've made sure to seize the day and increase with double digi t exposure.

We're going to show you why the company offers a fairly compelling upside, despite being above $110/share now.

Despite short-term pressures in the office sector, Alexandria's long-term thesis remains strong, with the potential for significant appreciation over a 5-10 year period.

The company has strong fundamentals - liquidity, low debt, high occupancy rates, and diversified assets - making it an attractive investment opportunity.

In this article, we'll digest the 3Q23 results and see what sort of realistic upside we could expect to materialize in the next few years.

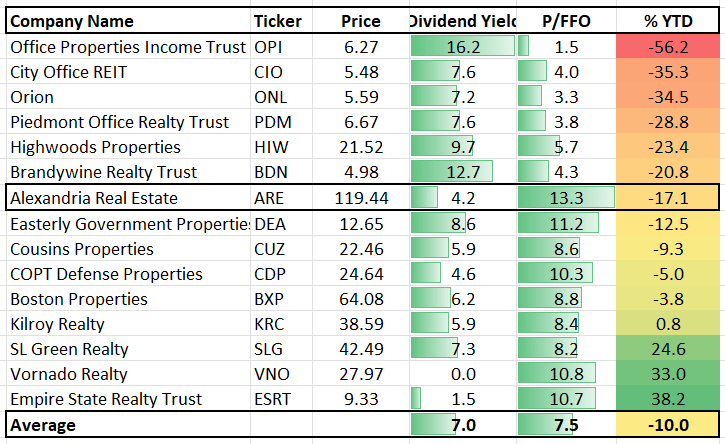

Quality with a very good upside

We're bullish with these office REITs:

All of which are BBB-rated or above and offer significant yields and reversal upsides. Our positions in all three of these companies have seen stellar returns in the short term, and we expect significant returns in the long term as well, despite the fears about refinancing next year.

Throwing out the baby with the bathwater seems to be a far-too-common notion in today's stock market, and as a value-oriented investor, this is something we greatly avoid.

Alexandria, despite its lower yield than the aforementioned Office REITs, is a great investment here, because it is qualitatively very different than other Office REITs - including top-tier players like BXP, HIW, and KRC.

The focus on laboratories and real estate properties with a high barrier-to-entry has proven, over a historical period, to be capable of outperforming even companies like Berkshire Hathaway ( BRK.B ) (BRK.A).

While the recent small downturn in share price has taken the edge off of its 1,311% RoR since its 1997 IPO, the company's returns are still very attractive.

Out of the REITs currently available on the market, only Welltower ( WELL ) has achieved better RoR than Alexandria.

ARE IR

Unlike Welltower, we believe ARE to be in a significantly more attractive segment, the life science industry, where the $450B worth of annual R&D investments indicate a very high level of spending.

Funding since 2018 has come to $2.1T in that timeframe alone, and Alexandria provides space to the companies in this segment.

Recent trends, both in 3Q23 and in 1H23, confirm the continued interest in ARE's properties despite an otherwise somewhat strained market.

The company placed into service in 3Q23 almost $40M of annual net operating income based on 450k RSF, which was 100% leased.

The same leasing grade/occupancy could be seen for the space put into operation in 1H23 for the company.

And going forward, this is what the leasing grades and occupancies are expected to look like.

ARE IR

Show me another REIT that manages a 92-99% occupancy in "technically" the office REIT space on a forward basis. We believe you'll have difficulties finding any sort of similar company here.

That's also part of the reason why we expanded the position so significantly when the company dropped to double digits.

ARE has become the dominant landlord for these types of properties and is strategically targeting specific geographies.

ARE IR

Some updated fundamentals for you to consider as well.

The company has nearly $6B of available liquidity, which pretty much enables ARE to pursue whatever projects, within its framework, it deems attractive.

This adds to the fact that ARE has no debt maturing prior to 2025 , and what debt it does have is 99% fixed at 3.7%, with 13.1 years on average remaining.

The company sports a 5.1x net debt and pref to adjusted EBITDA, with a BBB+ from S&P Global and Baa1 from Moody's.

We do not believe it is hyperbole to say that this company is one of the best fundamentally managed office REITs out there.

We believe all of our investments are qualitative, but it's no coincidence that my commercial portfolio has a position in ARE that is more than 6x that of other Office REITs.

This should show you just what sort of risk/reward expectations we have here, and how little we care for dividend yield next to quality.

The company has managed a 32.2% growth in quarterly FFO since early 2019, which is very impressive when you start to consider the environment in which they were able to do so.

And on the fundamental side, looking at portfolio specifics, you have a client base of 800+ industry-leading tenants.

ARE IR

Again, we do not believe this to be hyperbole - we're careful with such wording.

You can see above the degree of rent collection and the diversification. The demand for the company's space is telling of the underlying trends. We may not be particularly interested in investing in Biotech or pharma overall - but we're very interested in investing in the owners of these properties, because we know these companies most often cannot use "fungible boxes" for their operations.

They need incredibly specialized real estate, and this is what ARE offers.

The ongoing lease renewals even in this macro is once again telling, with 1.5M RSF renewed at a 99.7% percentage of RSF leased by tenants at lease renewal.

Businesses are staying with ARE. This company also has a near-negligible exposure to the work-from-home trend. The work done by the employees often cannot be done anywhere else due to the nature of the space and laboratories.

We're very comfortable with our investment in ARE and its prospects going forward - let me show you why, and why 3Q23 has clarified this further.

Alexandria Valuation - A lot to like here

It's always about what we're paying and what we're getting.

In this case, we can conclude that the current P/FFO for Alexandria comes to a 13.2x P/FFO, which compares to the 10-year average of 20.71x, nearly twice its current level (Source: FactSet Data).

It's not as great as when we were trading at double digits not long ago, but if you didn't buy, and we know some of you did not, then this could mark the last chance you have to get into ARE at an attractive multiple.

FAST Graphs

Why would you want to get into ARE, you might wonder.

Let's begin with forecast accuracy.

It's perfect.

By perfect we mean that both on a 10% and 20% 10-year margin of error, the company has never missed an estimate.

Not once.

That means that these estimates where the company is expected to grow at 5% or thereabouts, you can pretty much take those to the bank, as we see it.

Furthermore, it really doesn't matter what sort of multiple you forecast for ARE.

Oh, you could forecast a 9x P/FFO and get a negative 14% RoR until 2025E, but the likelihood of this company going to single-digit FFO multiples for the long term is very unlikely.

At anything around 10x or above, you're not losing money on this investment under current forecasts with that 100% forecast accuracy rating.

At 15x P/FFO, you're getting 16% annualized RoR, even after the recent bout of valuation increase. That's market-beating, and that's only to a 15x P/FFO, which is more than 5x below where the company has been historically trading.

At normalized P/FFO, using the 20-year P/FFO of 17.7x to make it even more conservative, you could expect an annualized RoR of 25%.

FAST Graphs

To compare, our own upside is over 30% annually.

That's because we bought it cheaper.

But this is still a very good upside for those of you getting "in" now.

ARE offers the best of many worlds.

It's an Office REIT without being your typical office.

It has a decent yield, but the biggest upside here is safety and the likelihood of future outperformance when valuation normalizes.

And remember, that 25% per year, that's based on the 20-year normalized P/FFO.

If we go to the 5-year, you're still at over 30% per year - but we do not believe the company to warrant such a valuation or multiple given the last few years of extreme macro.

We believe a correction is in order, but we do believe that correction will end above 15-17x P/FFO, not below that level - the company is "too good" for that.

ARE has continued to grow, and the company's portfolio and fundamentals are better today than they were 5 years ago.

We would have never bought the company at its premium - but below 14x P/FFO, this company becomes not only interesting, it becomes compelling.

At below 12x P/FFO, it becomes a "must buy", and even at today's level, we argue that it's one of the foremost office sector buys in the REIT space you could realistically consider.

There are many attractive opportunities in REIT-dom, but this remains the best one we see in office.

{kind=link}

Thesis

- Alexandria Real Estate is a class-leading REIT in the office sector, though we would argue it is far better than your average office REIT, including some of the "best" ones we invest in, such as BXP, HIW, and KRC.

- This company is undervalued very rarely - so when it is, this warrants immediate highlighting - which is exactly what we're doing here.

- We give ARE a "BUY" with a $165/share PT, which comes to a very conservative 19.5x P/FFO on a forward basis.

Remember, we're all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, we harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, we buy more as time allows.

4. We reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are our criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of our criteria, making it relatively clear why we view it as a "BUY" here.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Alexandria Real Estate: Last Call?