ARE - Alexandria Real Estate's Fundamentals Keep Debunking The Doomsayers

2023-11-02 14:52:13 ET

Summary

- Alexandria Real Estate Equities, Inc. is a dominant player in the life science REIT sector, owning research labs in top bioscience hubs in the U.S.

- Despite strong fundamental growth, Alexandria's stock price has fallen by 50% since 2021.

- The stock is trading at low multiples and is undervalued, with potential for substantial growth in the future.

Alexandria Real Estate Equities, Inc. ( ARE ) is a life science real estate investment trust, or REIT, owning a dominant share of research labs in the top bioscience hubs of the United States.

It is a strange feeling being simultaneously right and wrong on Alexandria. I think I got the fundamentals right, but from a stock price standpoint, ARE has been one of my worst calls, down about 50% since I wrote about it in late 2021 .

The idea at the time was that ARE had strong growth ahead with the ability to raise rents materially and also grow NOI from developments coming online. This has largely played out as expected. FFO/share grew from $7.76 per share in 2021 to $8.97 per share in 2023.

{kind=link}

That is 15.5% bottom line growth in the last 2 years. ARE is expected to grow FFO/share another 19% by 2026.

The part I got wrong is that I thought this fundamental success would be matched with favorable stock price appreciation. Generally speaking, when a company becomes more valuable via higher earnings and asset appreciation, the stock price tends to move with it.

Yet somehow, with ARE, the stock price has fallen in half during its growth spurt.

As it stands today, ARE trades at the following multiples

- 10.2X forward FFO (funds from operations).

- 12.8X forward AFFO (adjusted FFO).

- 61% of net asset value ((NAV)).

These are extremely low multiples for a large cap, investment-grade REIT with a strong growth trajectory. I think it is worth substantially more than market price, making it opportunistic.

The negative price movement seems to have been brought forth by a series of doomsday predictions.

ARE Doomsday predictions

- Office space is going to be vacated.

- ARE is going to have to induce tenancy through either lower rent or excessive TI.

- Rising interest rate environment could invalidate low cap rate lab real estate.

- Lab construction boom threatens ARE's submarkets.

Each of these ideas was well publicized, leaving investors with a constant feeling that something was about to destroy ARE. Every piece of good news was interpreted as irrelevant in the face of pending disaster and every piece of bad news was interpreted as the tip of the iceberg about to sink the Titanic.

Debunking doomsday prediction #1: Office space going to be vacated

Research labs are inherently mixed facilities with some combination of wet labs/research stations and more typical office space. This is for functional reasons. A scientist might collect the data in the lab portion and then analyze the data at a computer which would be in the more traditional office setting.

So while it is true that a significant portion of ARE's square footage is office and that office is fundamentally struggling right now, ARE's office space is joined at the hip with lab space. It is part of what makes the labs functional. The tenants want this mix of space as these buildings were specifically designed to maximize the research capabilities of the tenants.

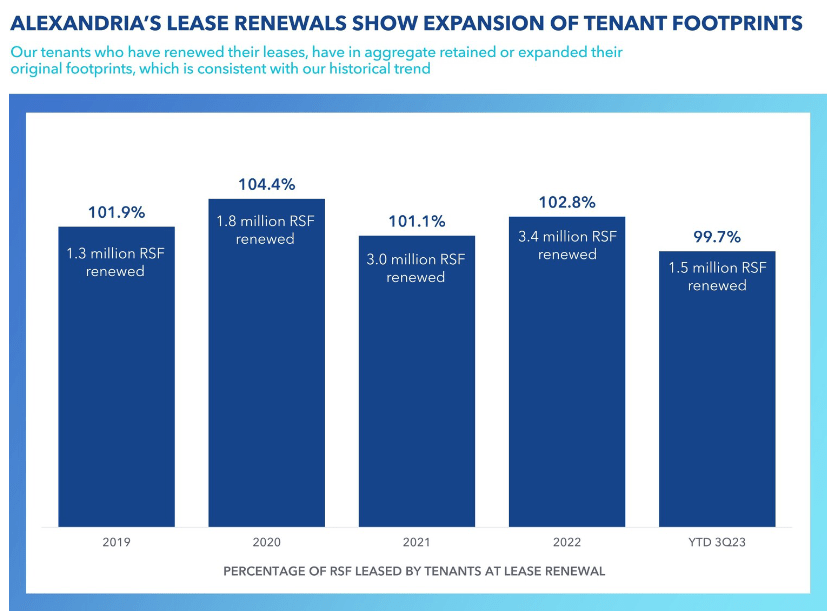

The idea that tenants actively want the space shows up in the numbers. ARE's lease renewals often come with the tenants increasing the square footage they lease.

{kind=link}

This is the opposite of what one would see in office where tenants are either vacating or shrinking their footprint. As a side note, I suspect office leasing will bounce back at some point in the future, but for now it remains rough.

In addition to renewals coming in strong, ARE is leasing up existing vacancies as evinced by leasing volume exceeding lease expiries.

- 867,582 square feet leased in Q3 2023 .

- 622,654 square feet of leases expired.

ARE is increasing occupancy in what is approximately the trough of the office market. Not only that, but they are increasing occupancy under favorable terms which brings us to doomsday prediction #2.

Debunking doomsday prediction #2: ARE is going to have to induce tenancy through either high TI or reduced rental rates

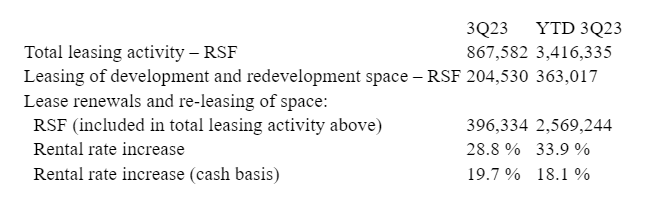

Shown below is ARE's leasing activity for Q3 and year to date 2023:

{kind=link}

Rental rates on new leases were 28.8% higher on a GAAP basis and 19.7% higher on a cash basis than expiring leases. This strong leasing resulted in ARE increasing its 2023 guidance by 2 cents at the midpoint to $8.97-$8.99

There is always some expense involved in leasing real estate. Tenants want a fresh building that is going to be functional for their purposes and move-in ready. This expense is accounted for as tenant improvement cost otherwise known as TI.

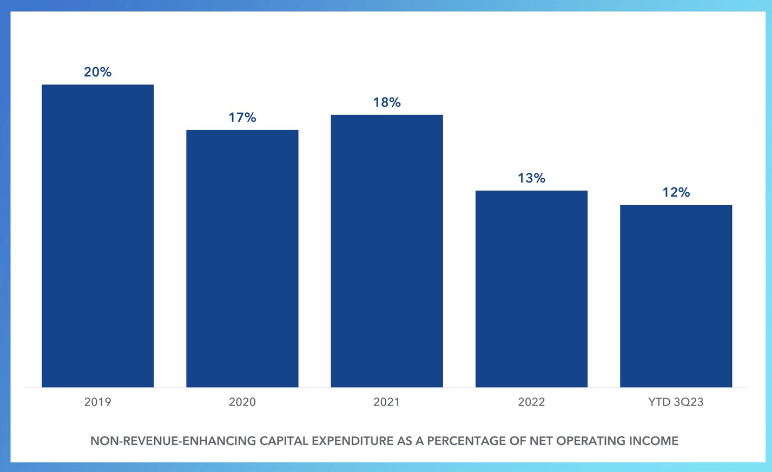

Industrial real estate is highly regarded for its very low TI while office has high TI. Lab space is somewhere in between. I am by no means suggesting that ARE is a low capex company. In 2023 capex was 12% of NOI.

{kind=link}

However, this 12% is normal. In fact, it is significantly lower than it has been historically which suggests that this capex is not a sign of inducing tenancy. It is also an expense that is already factored into AFFO.

Rental rates increased materially, and TI is below normal. ARE is objectively not inducing tenancy by giving tenants favorable terms.

Debunking doomsday prediction #3: Rising interest rates invalidating low cap rate labs

High quality research labs such as those in AREs portfolio have consistently transacted at very low cap rates in the 4s and 5s. Even today they are still transacting there.

The doomsayers have put forth the idea that 4% to 5% cap rate real estate would be underwater if interest rates were in the 5s which they now are for a significant portion of the yield curve. On the surface, this idea makes quite a bit of sense. The interest expense one pays on the mortgage could be higher than the NOI. There are, however, 2 things wrong with this idea.

- NOI is less than stabilized NOI.

- ARE has locked in cost of capital.

The reason sophisticated buyers are paying billions of dollars to buy life science properties at cap rates in the 4s and 5s is because they anticipate NOI growth. A stagnant income stream does not transact at a 4%-5% cap rate in today's environment. These properties are only transacting there because in place rents are substantially below market rate rents.

Depending on the vintage of the existing leases, market rents are 15%-40% above current rents so the buyer of these properties is anticipating being able to roll rent up to market rates whenever the lease expires.

Thus, it is only nominally a low cap rate. The stabilized cap rate is probably closer to 6% or even 7%. The spread over cost of capital is still there.

For weaker players, there is some concern on timing. If interest expense is high now but the higher rent only comes a few years down the road, it would be a cashflow concern. This is not a problem for ARE because of the way it has structured its balance sheet.

Here is some data from ARE's supplemental:

{kind=link}

ARE is 99% fixed rate debt with no maturities until 2025. The weighted average remaining term on its debt is 13.1 years and its weighted average cost is 3.7%.

Its cost of debt is largely flat for the foreseeable future. It will be able to raise its rents to market rates well before it has to pay market interest rates on its debt.

ARE is supremely well-positioned for rising interest rates.

Doomsday prediction #4: lab construction boom threatens ARE's submarkets

You may notice that unlike the other headers there is no "debunking" in the sentence above. Unlike the other misguided notions this one is firmly grounded in reality. It is factually true that there is a large amount of competing supply under construction in ARE's submarkets.

- Cambridge has 2.8 million rentable square feet ((RSF)) under construction.

- South San Francisco has 3 million RSF under construction.

- Sorrento has 1.4 million RSF under construction.

San Francisco seems to be the epicenter of oversupply as it not only has excessive construction, but it is being delivered into weak demand.

ARE's CEO Peter Moglia discussed the San Francisco supply on the Q3 2023 conference call :

"In San Francisco Bay, unleased competitive supply remaining to be delivered in the second quarter of '23 is estimated to be 5% of market inventory, which is a reduction of 1.6% over last quarter due mainly from deliveries. In 2024, the unleased competitive supply will increase market inventory by 8%, a 0.8% reduction, unfortunately, not driven by leasing, but due to a downward revision of estimated square footage to be delivered during the year. In 2025, the unleased competitive supply will increase market inventory by only 1.2%, which is a good indication that developers in this market are beginning to act rationally."

That is certainly too much supply, but there are 2 beacons of hope within this data.

- Some of the planned construction has been canceled.

- A cessation in construction starts indicates supply will be far more moderate in 2025 and beyond.

Given the supply pipeline it behooves us to examine the extent to which it could impact ARE.

In-place leases are not going to be as affected because they are already locked in and even upon lease expiry there are significant switching costs. The primary impact of the new supply is going to be on ARE's developments. They are having to compete with other developments for tenants.

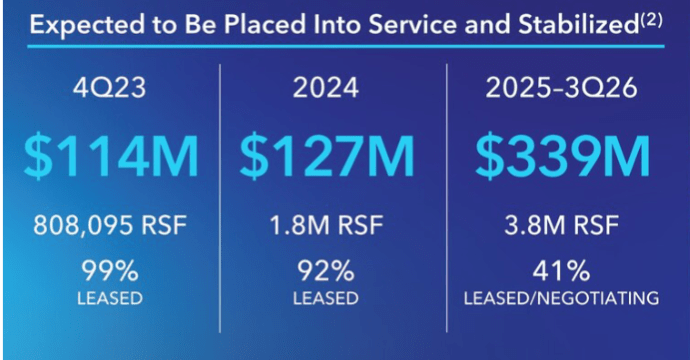

This is potentially a significant headwind because ARE has a large pipeline of developments in progress consisting of over 6.4 million rental square feet that is expected to be delivered from 4Q23 through 3Q26.

ARE estimates this will be $580 million of incremental annual NOI.

{kind=link}

Some of these are Joint Ventures, so the NOI at ARE's share is closer to $491 million.

ARE has 137.7 million shares outstanding, so that represents an incremental $2.82 per share of NOI. Note that this will not be 100% margin as these developments are not 100% funded at this point, but I anticipate significant AFFO/share accretion.

That accretion, however, is dependent on these developments leasing up successfully. In that regard, ARE has 2 advantages over the competing new supply:

- Property quality/location.

- Existing relationships with major biotech tenants.

Much of the competing supply is more of an empty shell that could be outfitted for biotech or regular office depending on what tenants they can drum up. In contrast, ARE's developments are purpose built for life science to be maximally functional for the targeted tenants.

The majority of ARE's leasing comes from existing tenants either expanding or wanting additional locations. These relationships fuel lease-up of the developments.

Once again, we don't need to rely on just the logic of why ARE should fare better in leasing. The data shows that they are leasing much better than the competition.

- Remaining 2023 deliveries are 99% pre-leased

- 2024 deliveries are 92% pre-leased

- 2025 and beyond deliveries are already 41% pre-leased.

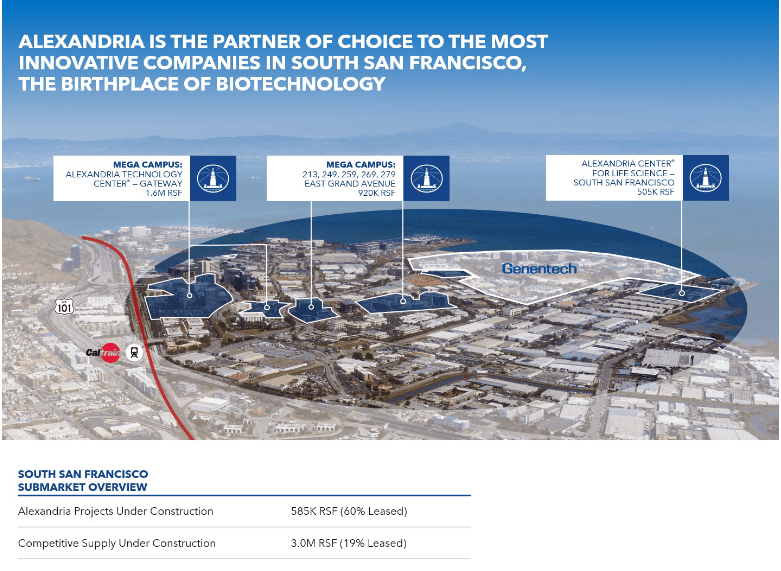

Even in San Francisco, which is the most challenged market, ARE is finding some leasing success.

{kind=link}

Its developments are 60% pre-leased while competing new supply is only 19% leased.

So far, it appears ARE is handling the new supply quite well but it is a risk factor that should be monitored. In particular, I will be watching for the pace of new groundbreakings continuing to slow.

The buy thesis

ARE is trading at prices that indicate substantial damage. In my opinion, the data shows that they have performed well and are positioned to continue growing. There are of course risk factors but that is always going to be the case for any company.

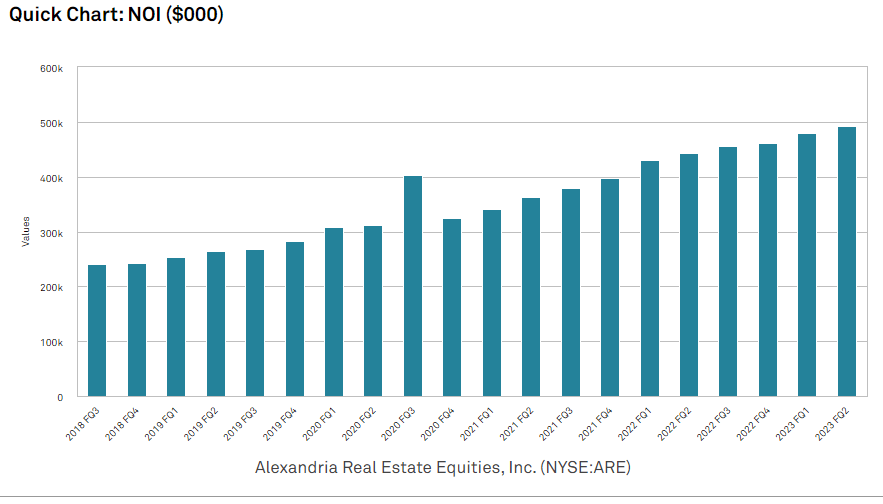

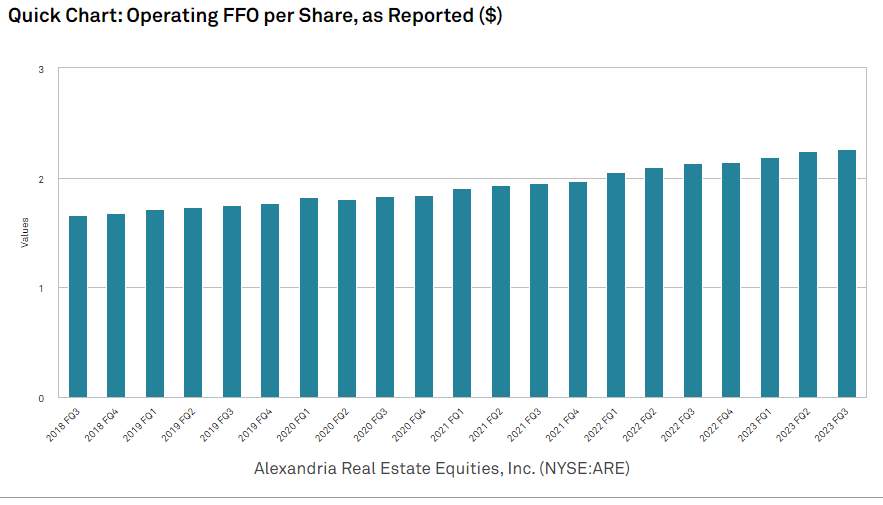

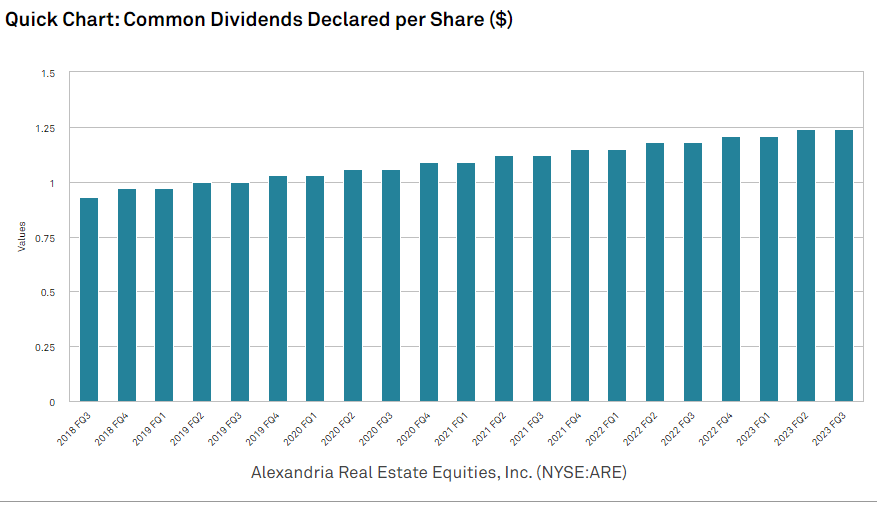

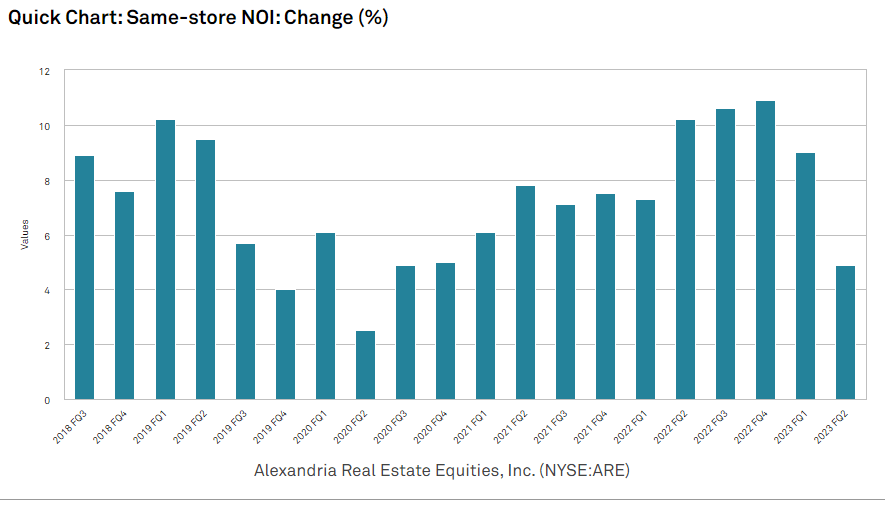

ARE's multiple is far too cheap for its growth rate and I think it will expand materially as continued success quells fears. Following are charts of NOI, FFO/share, dividends and same store NOI growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Those do not look like the data points of a company that has traded down 50%. Either there is some major problem lurking that I am not seeing, or Alexandria Real Estate Equities, Inc. stock is opportunistically cheap.

For further details see:

Alexandria Real Estate's Fundamentals Keep Debunking The Doomsayers