ALFVY - Alfa Laval: 'Hold' Is The Right Choice For The Time Being

2023-08-09 02:30:59 ET

Summary

- Alfa Laval has delivered triple-digit returns and excellent margins, but the company is believed to be overvalued now.

- The company's 2Q23 report showed positive results, with strong growth in the energy and marine divisions.

- I've been selling my position in Alfa Laval and rotating into other undervalued stocks due to the company's high valuation.

Dear readers/followers,

My investment in Alfa Laval ( ALFVF ) was actually a significant one at its prime. I had over 3% of my portfolio invested in this superb company, and this investment has returned triple digits, with excellent margins, since I purchased it. I underestimated both how high the company would climb and the speed at which it would do so, and my articles for some time have reflected this premiumized situation we're seeing for the shares.

I still believe the company is expensive. In fact, not long after my article, the company broke 390 SEK/share again, and that's when I did multiple rounds of taking profits.

In this article, I'm going to detail to you my manner of profit-taking, and my future stance for the company. As of now, my Alfa Laval position is down to less than 0.5% of my total portfolio, and I do not expect massive outperformance on a future basis at this price.

Let's take a look at the trends here.

Alfa Laval - Plenty to like, delivering value, but too expensive here

First off, this is what Alfa Laval has returned if you followed my "BUY" rating back in the COVID-19 times or thereabout.

Seeking Alpha ALFVF RoR (Seeking Alpha)

At my time of selling, the company had delivered well in excess of 120% RoR in a relatively short timeframe. It's a great company. Any time this business is cheap is a time when it should be looked at and potentially invested in. If someone were to ask me what company to first pick in Sweden, Alfa Laval would always be in the top 5 of that list.

I also seem to be the lone cover on SA in this company. The company delivered its 2Q23 report, and this report was a positive one, yet another reason for the company to continue to perform well, which it has. The company significantly grew its top line, by which I mean over 20% intake of orders, net sales, and overall adjusted EBITDA, the last of which grew by 21% and which was the lowest number. 17% of the net sales growth increase of 34% was in fact organic growth.

The energy division grew by far the most out of all of the divisions. The segment saw continued strong intake with YoY growth of 20.4% in ordered and 35% in sales. Most of this growth came from the expected investment growth in energy efficiencies and similar markets. This is something we clearly expected. When I started covering the company, I viewed and presented it as a major beneficiary of these trends, and with gas/refineries currently recovering, there's a lot to like here.

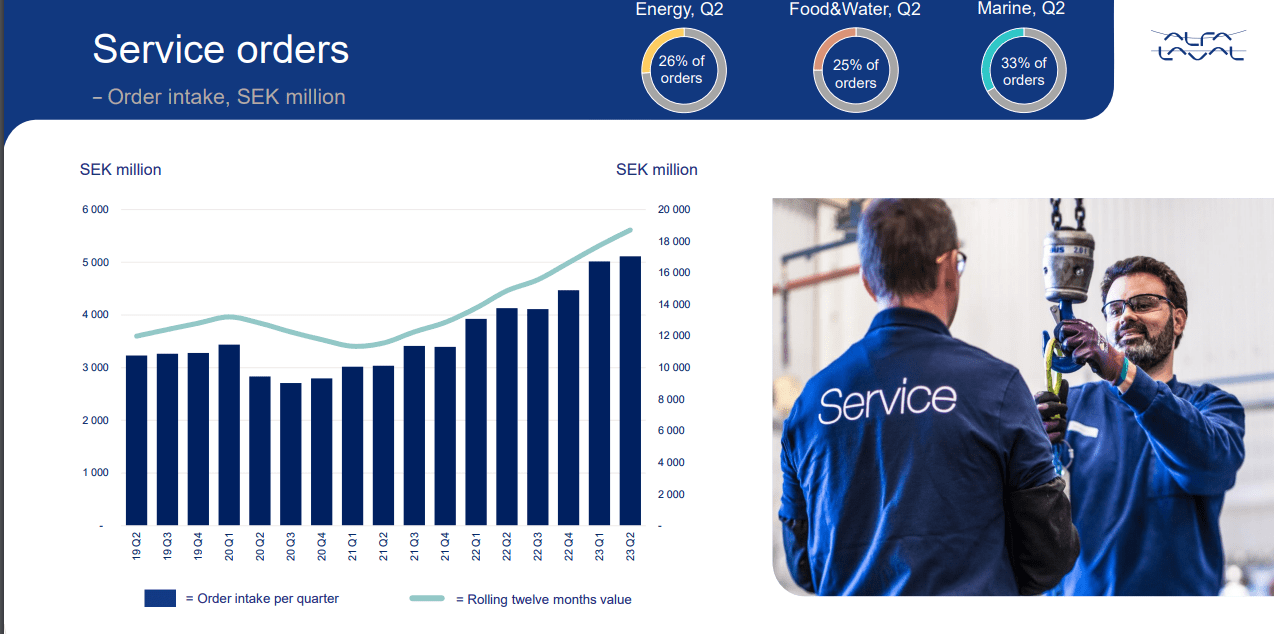

Also, record-high service order intakes during the quarter, driving extremely impressive sales and EBITDA growth.

Alfa Laval IR (Alfa Laval IR)

But other segments showed strong trends as well. The company showed strong top-line growth also in Marine, with good demand for pumping systems and sustainable solutions. Again, service volumes were delivered as well, and the only problem was a margin impact from a legacy order backlog, operational imbalances, and a low overall factory load.

The company has already started initiatives to address these issues and expects to have them under control with improvements in the next fiscal quarter already. The company's Boiler & Ballast Water Treatment businesses are also being addressed here.

Food & Water?

Plenty of positives. Good demand, with larger projects, supply chain challenges are unwinding nicely, with continued improvements for the service segment. Operating margins were somewhat down YoY due to the mix - large projects tend to have lower margins than say, service, and as a result, the company had lower margins.

However, on the whole of it, the company is a very attractive business with a good sales mix and a very attractive split. Just take a look at the service order mix.

{kind=link}

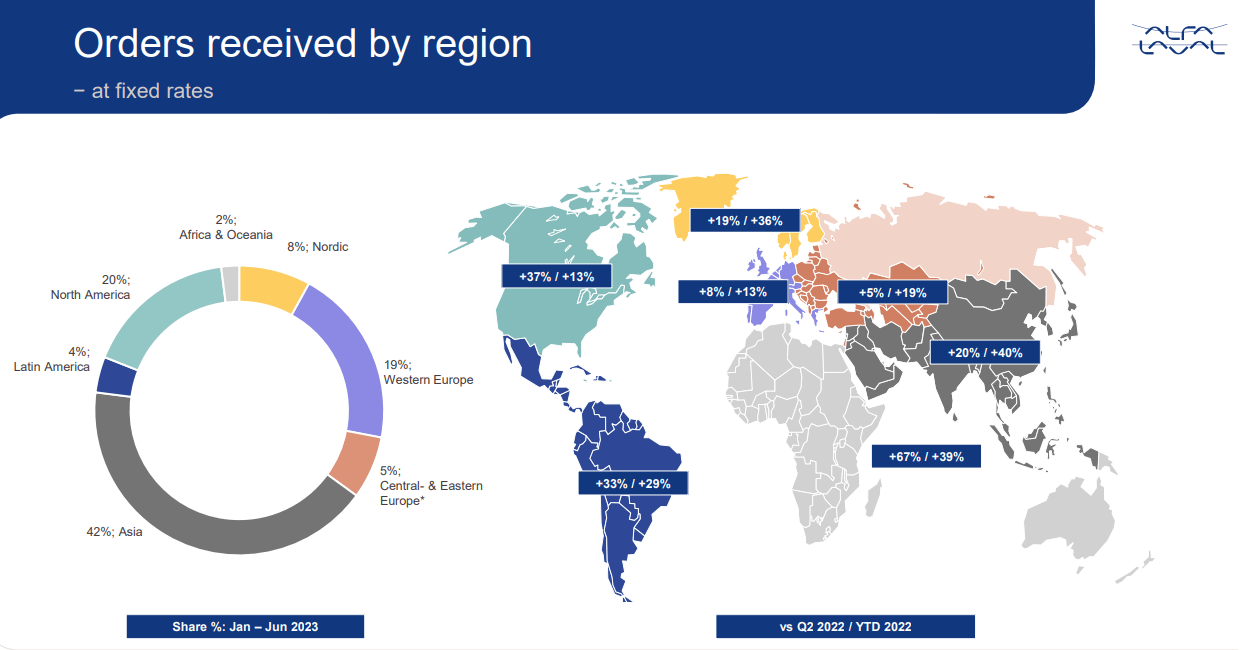

Also, geographically speaking, the mix is very attractive, though could be better if Asia wasn't such a large represented portion here.

{kind=link}

With sales and orders up organically, improving supply chains, and a slowly normalizing market, there could be a case for investing in Alfa Laval - if the company wasn't at such a massive overvaluation. The company has a very attractive overall backlog of over 45B SEK, over 20B of which is for delivery in 2023 with another 25B in 2024 or later. That marks a nearly 50% YoY increase and a 2Q23 book-to-bill of 1.16x.

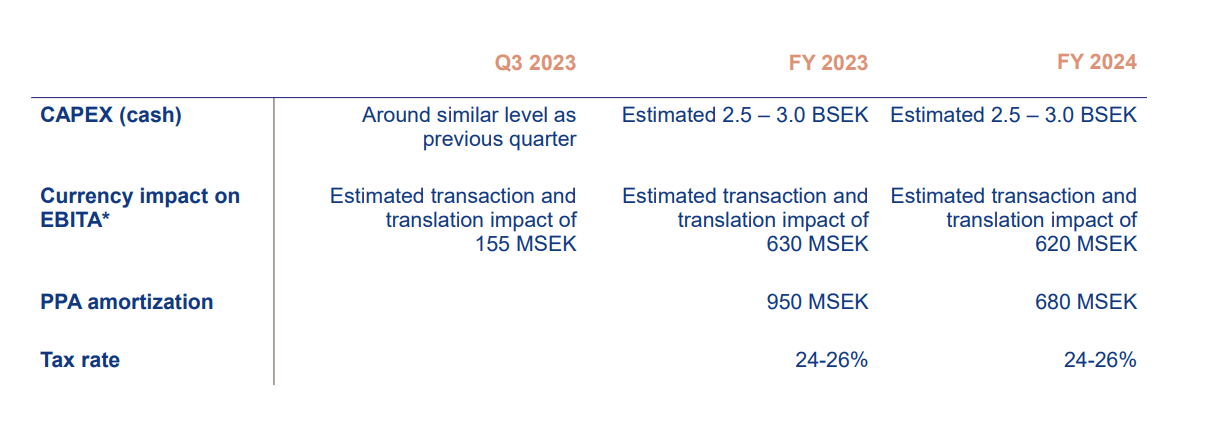

The company has also given us updated 2023 guidance.

{kind=link}

I expect that Alfa Laval will remain a competitive business despite both slightly slowing economic activity and challenged end markets overall. The top markets remain USA and China, with the Nordic markets as a third.

However, the problem isn't business performance, as I've mentioned prior.

Unlike many contributors on SA, I don't have an issue sticking to my guns when it comes not only to "BUY" ing, but to selling as well or rotating for profit. I'm very firm in my conviction that every company has a designated value where it'd behoove you to sell, not to keep buying or even holding, and investing in something else.

For Alfa Laval, my target for this action has been around the 360-380 SEK mark for a long time - so when the company hit that level, that's when I started rotating the business and investing in other things. But when I sell, I don't just sell everything I have. Usually, I do it through a mix of a few ways because we're talking about a quality business.

For around 25-30% of my position, I write long or medium-dated covered calls, if I can enhance my yield by about 3-5% on an annualized basis. If I can, then this is something I consider good enough to maybe stretch that upside a bit more.

Usually, I'll sell about 20-40% fairly quickly though, realizing my profits in the company. With Alfa Laval, it was hard, because this is a market leader at a very high-performance level - and I know how rare it is to find this company at even anything close to an undervaluation.

So when selling, I knew I wouldn't be able to easily or quickly buy it back at a cheap price. And indeed, that has been the case.

Alfa Laval has above-average gross, operating, and net margins for its sector. It has among class-leading RoE, and a very conservative 1.7x debt/EBITDA ratio.

It's an extremely balanced sales mix with an industrial COGS of below 67%, which is excellent considering how COGS-heavy this business actually is.

{kind=link}

Despite troubles, the company hasn't had many issues retaining an ROIC/WACC profitability. The one drawback it did, which I believe it did much too impulsively, was to cut the dividend during COVID-19 - and I did mark it down for this. But overall, the whole operation is at a very high overall level with great future potential.

The only issue is, we can't really pay anything for that - and that's where the company fails one of the more fundamental of my tests - hence why I'm down to 30% of my original holding.

Alfa Laval - Now overvalued, or fully valued even for a high 2025E result.

The company's dividend yield is now down to a 1.57% level, which is lower than it's been for a very long time. Alfa Laval is BBB+ rated with a continued low debt/cap, but there's very little excuse even for this valuation with this in consideration.

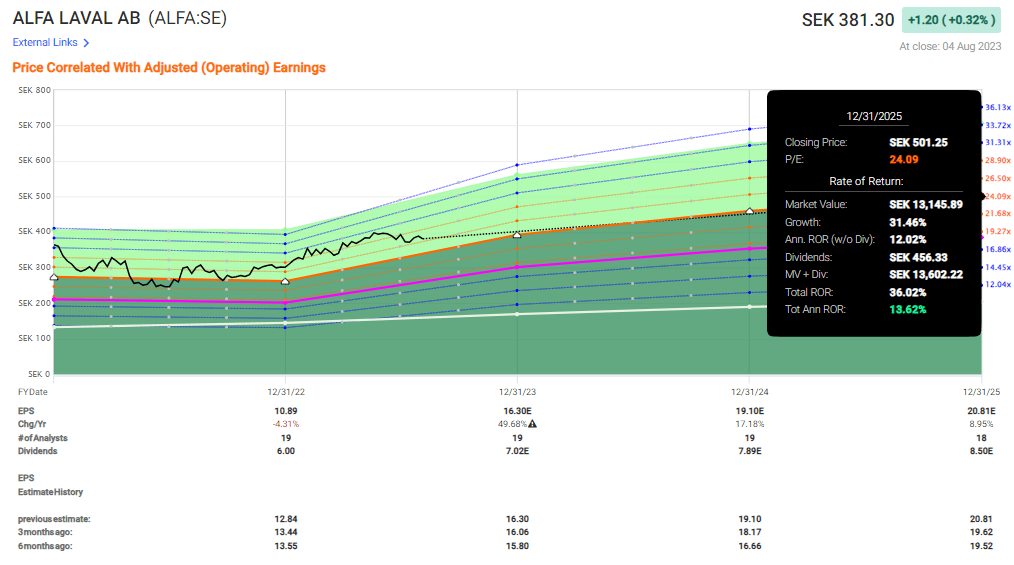

Even considering this industrial at over 24x P/E, the 5-year potential upside is now below a 15% annualized RoR level. Not only is that low contextually, but it's also low across the sector.

{kind=link}

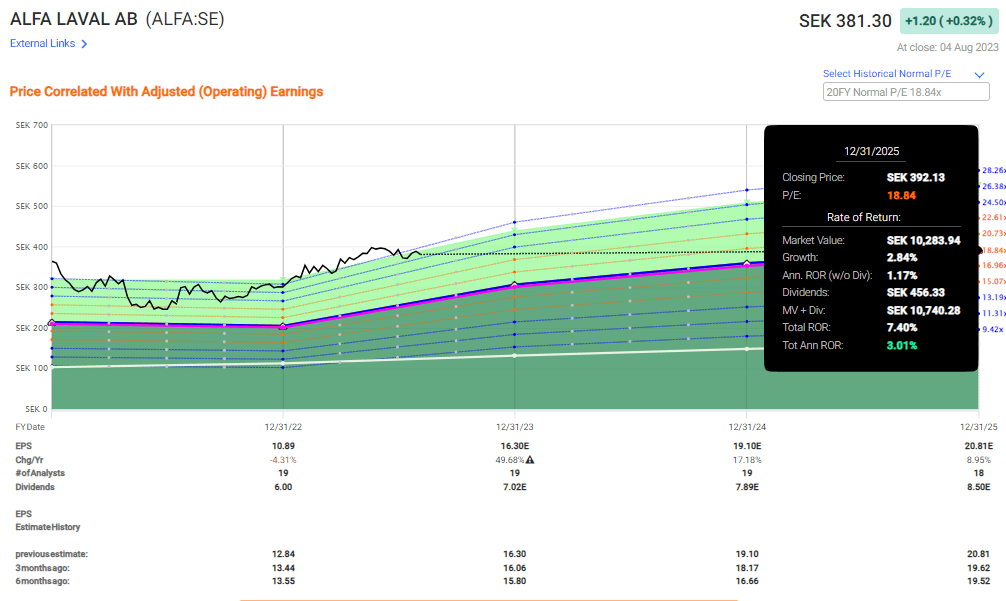

Plenty of industrial companies trade well below 15x P/E and have a substantially higher yield as well as a substantially higher overall upside. My own target is to normalize Alfa Laval to its 20-year average, which comes to about an 18-19x P/E. This is much more in line with a fair overall valuation for this sort of growth and business quality, while also taking into consideration the potential for volatility due to the cyclicality of key sectors.

That upside looks like this.

{kind=link}

Or perhaps I should say "lack of upside".

Still, we shouldn't claim that Alfa Laval is unsafe. That's not the impression I want to give. Diversification is solid. Insofar as major customers go, Alfa Laval does not have any single customer that represents more than 10% of net sales. The largest customer for the company's products is Tetra Pak, which represents only 5% of overall net sales. (Source: Alfa Laval Annual Report)

So, plenty of safety on that front. This is also reflected in the company's share price target - though surprisingly they do have a relatively conservative PT for the company. 18 analysts follow the company with PTs ranging from 267 to 490 SEK, a massive delta in the context here. Only 3 analysts out of those 18 are actually at "BUY", with a massive 16 either at "HOLD" or "SELL".

I add my voice to this chorus with my current method. It could be said that my covered calls are in fact the wrong way to go because it does mean I have to hold my 30% remainder at a premium until at least December of 2023, when these options expire. However, I believe that the company may see some unrealistic (at least at its core) valuation spike driving it up to around 410. If it doesn't, well I've already sold 70% of my stake at a 110%+ profit, making this the last in a long line of solid profit-makers in my portfolio since COVID-19.

For now, this is my thesis on Alfa Laval, and I would caution you very seriously to go too deeply into this investment.

Thesis

- The company is a fundamentally appealing industrial out of Sweden that, to my mind, is a must-own in a conservative dividend stock. Current valuations continue to dictate "HOLD" however, as the premium is reaching absurd levels of near-tech investments.

- My rotation has been based on both writing medium-dated covered calls, adding 3-5% to my annualized yield, and straight selling of the common equity.

- The valuation has made the yield less than 2%, and the upside is around 6-7% even with the dividend growth included, and that's assuming we don't get a cyclical downturn.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

At the current valuation, the stock lacks meaningful upside to justify a good valuation. For this, I give the company a rating of "HOLD".

For further details see:

Alfa Laval: 'Hold' Is The Right Choice For The Time Being