ASTL - Algoma Steel Group: A Hold Until Shipments Are Back On Track

2023-05-24 04:36:12 ET

Summary

- Algoma Steel Group has seen a worrying decline in revenues, fueled by both lower shipments and lower steel prices.

- The outlook for the industry remains positive as reshoring and still strong manufacturing demand in the US should help fuel growth.

- Shares are being diluted, and until the company shows they can get back to the 2022 levels of shipments, I will have them as a hold.

Investment Summary

Algoma Steel Group Inc. ( ASTL ) is a Canadian steel producer specializing in the manufacturing and supplying of high-quality steel products. With a strong emphasis on quality and precision, Algoma Steel serves various automotive, construction, energy, and manufacturing industries.

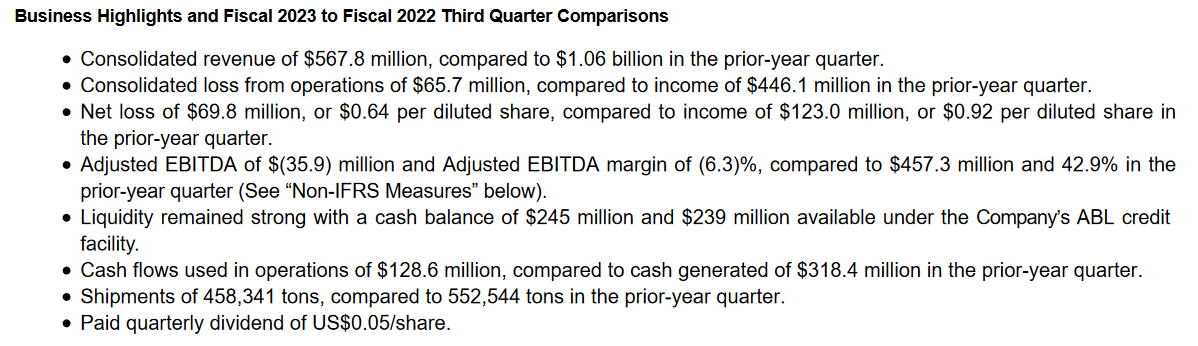

Despite the perhaps momentum steel is seeing this hasn't translated into growing revenues for the company, in fact, quite the opposite. The revenues were $1.06 billion in the third quarter of 2022, to just under $600 million in the last earnings report . A noticeable drop that the management blamed on lower production and shipments. Drops like this cause concerns and that is perhaps a large reason for the disappointing stock chart we are seeing with ASTL. But it can't all be blamed on the shipments, the hot rolled coil steel prices are not as favorable as a year ago but are seeing a rebound at least. The company still operates a decent balance sheet and the reshoring to the US should help boost demand. Given that said, I am optimistic about the outlook for ASTL and will keep a hold rating until I see a more clear uptrend in revenues again and productions are back on track.

Reshoring Is Adding Momentum To US Steel

One major factor driving growth for the company is the trend of deglobalization. Many companies are shifting their production away from China and exploring alternative manufacturing locations like India or Vietnam. Additionally, there is a growing trend of companies relocating back to the US to mitigate global supply chain disruptions experienced during the pandemic. By establishing a more streamlined and efficient business model, companies aim to enhance resilience during challenging times. This shift also fosters increased domestic demand, thanks to the advantages of close proximity-the US government's incentives to boost domestic manufacturing spending further support this trend.

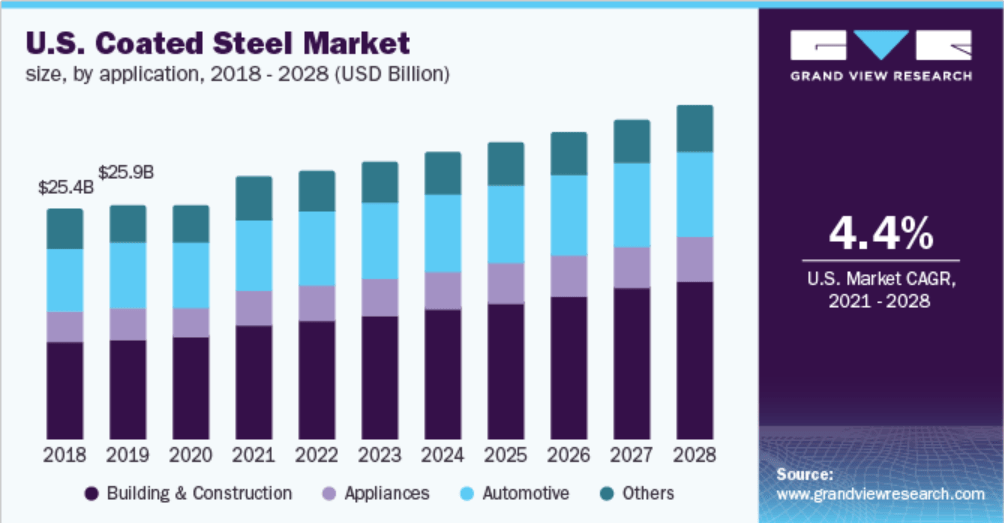

Steel Market Outlook (grandviewresearch)

{kind=link}

In the case of ASTL, steel production in the country has displayed steady growth throughout 2022, with a notable 5% increase in December compared to November. This paired with the optimistic sentiment around steel in the US should help become a tailwind for the company and hopefully a return to business as normal for the last part of 2023 as the company recovers production and shipments. The US Coated Steel market highlighted above I think also showcases the strength of the market. The US seems to also be at the start of another infrastructure boom which would only help to increase demand for ASTL and its products.

Looking at what the company themselves are projecting , they see the coming fourth quarter resulting in shipments between 555,000 - 565,000 tons of total steel shipments. This would be an increase of about 21% compared to the last result, which would put the company well on track to get back to previous revenue levels.

Quarterly Result

ASTL continues to operate in a challenging market are has had its shipments down noticeably over the last 12 months as a result of it. The CEO Michael Garcia said the following in the last report , "I have been disappointed by the level of production and shipments in the last two quarters". I think the coming quarters will be crucial to look at the results and whether the company is able to successfully execute and get back on track.

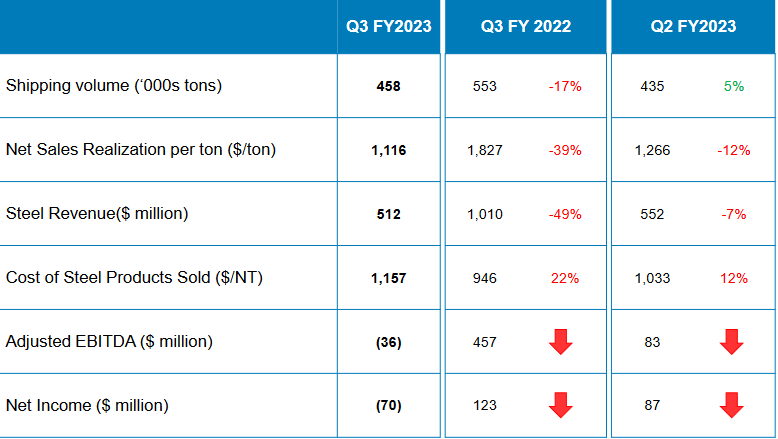

Earnings Highlights (Earnings Report)

{kind=link}

The loss in shipments of course also impacted the revenues, which dropped over $400 million to $567 million for the quarter. This is also caused by the steel prices taking a major hit too, down 35.7% YoY.

Company Results (Investor Presentation)

{kind=link}

Fortunately, the company hasn't started having negative cash flows as a result of this loss in revenues. But cash flows used in operations was $128 million compared to $318 million in the prior-year quarter, as highlighted in the last report . But this has meant the company continues diluting shares, which of course hurts an investor. Outstanding shares going from 71 million in 2021 to over 150 million in the last report is significant and a factor for the lower multiple the company is getting in my opinion. The company does have positive cash flows and negative net debt which makes me wonder why they ever would need this capital. It hurts investors and doesn't seem like a very solid long-term plant to rely on. The coming few reports will be key to seeing this number develop and getting an idea of the actual rate investors are getting diluted.

Risks

Looking at the risks associated with the company, the major one outside would be a slowdown in US manufacturing and infrastructure spending. Some might say this is already happening at a small rate so it will be key to look out for. Shipments have slowed for ASTL so another hit like that would be a major setback and would most likely result in a lower share price to adjust for the loss in revenues.

Steel Market (IHS Markit)

As seen in the last report also, unfavorable steel prices will have a major impact on the revenues for the company. They are in an industry where they have to follow the rest of the market and set the prices accordingly. They don't necessarily have a moat saying their product is superior to someone else, which makes for volatile reports as we have seen. Fortunately, the future does seem quite positive and steel prices are expected to rebound somewhat.

Valuation & Wrap Up

Looking at the valuation of ASTL they are trading a fair bit under the sector average forward multiple, which sits at 13, and ASTL at 7. But as I mentioned before, the recent uncertainty in the production levels for the company is a likely culprit to this lower multiple. In my opinion, if the company is able to successfully get back to shipment levels seen in 2022 there is a case to be made there is much more upside than downside here.

{kind=link}

This uncertainty makes me prone to not justify a buy case just yet. Besides that, the dilution of shares is concerning too, and until there is a noticeable slowdown in that or a stop I will keep a hold rating for ASTL. There's no lack of companies in the steel industry, and sometimes it's better to go with the more well-established ones, like Steel Dynamics Inc. ( STLD ) for example. A company trading at a low multiple too and a sustainable dividend yield in my opinion. Apart from that the company is also buying back shares at a good yearly rate. To conclude, there are improvements needed with ASTL before I will rate them a buy. For the moment they will have a hold rating and I will keep a close eye on the coming quarter's shipment results to get an idea of how the comeback for the company is going.

For further details see:

Algoma Steel Group: A Hold Until Shipments Are Back On Track