DIDIY - Alibaba: All You Need To Know

Summary

- China is in the middle of a pivotal change for its international capital markets through the stock market connection mechanism.

- The relatively low implied volatility for Chinese companies listed in the US indicates that most risks are already factored into BABA's stock.

- The odds of a delisting scenario have been improved in favor of BABA.

- Theoretically, a PCAOB inspection can still find some reporting irregularities, but such a scenario of finding material misstatements is remote.

- There is light at the end of the tunnel, and we are getting closer to a new pivotal phase for the international markets, where Alibaba could come out stronger than ever.

Introduction & Progress Review

In an earlier analysis, we explored how past events and actions of Mr. Son and Mr. Ma have made CCP revengeful. Below, I summarize a quick throwback to the most important updates from previous articles, and subsequently, we explore how things evolved for Alibaba Group Holding Limited ( BABA ). Unless you want to refresh your memory, you can skip this section.

In December 2021 , in this article, I placed particular emphasis on why the NVIDIA-ARM Deal initiated by Mr. Son should be terminated, quoting:

If the ARM deal goes through, NVIDIA would gain an unfair competitive advantage and lead to US Hegemony and dominance over the semiconductor sphere.

A few months later, true to my forecasts NVIDIA – ARM deal was finally terminated, as was expected. Many might wonder what this has to do with BABA; I urged you to go back and connect the dots first. In addition, we have also analyzed why the CCP is still going after the outspoken billionaire Mr. Ma, especially after the false ownership disclosures for ANT Group:

Not only that, Mr. Ma had falsely disclosed a 10% ownership in ANT, and when the Chinese regulators eventually found out that he was effectively exercising control with more than 50% ownership through a complex arrangement of related entities, this has made China furious seeking revenge for the misconduct.

Not surprisingly, the recent announcement that Mr. Ma is giving up control of Ant Group will restore the company's IPO efforts. Still, we shouldn't expect it anytime soon until the restructuring is over and Mr. Ma is out.

Then, early in 2022, I urged the importance for BABA investors to prioritize understanding its politics rather than its fundamentals, as the political landscape is what ultimately drives its share price in the short run. Undoubtedly, BABA's fundamentals are solid, so investors should not waste time obsessing over the company's low valuation and great fundamentals, leading to confirmation biases. Instead, they can 'protect' the downside by understanding how the CCP and state capitalism work and how the Party implements policies and pursues common prosperity goals. A snapshot from the analysis in March 2022:

As a result, BABA stock is expected to trade sideways in the medium term, and Mr. Son could unload more shares gradually, setting downward pressure. As a result, the meaningful reduction of SoftBank's shareholding in BABA is expected to please the CCP, as it is quite evident that Mr. Son's actions are against CCP's plans, and they prefer to see him exit his positions in Chinese equities.

Nearly six months later, Mr. Son cut BABA's stake from 23.7% to 14.6% through 'forward sales' contracts. Softbank has sold more than half of its Alibaba stake. Eventually, the stake now falls below the threshold for maintaining its board seat, having less influence on the conglomerate's decisions.

All the above indicate (but do not confirm) that the CCP was going after the two moguls that managed to concentrate too much power in their hands, and their actions went out of control. Thus, monitoring the movements and compliance would allow investors to form reasonable expectations of the regulatory crackdown's direction and, therefore, the destiny of BABA.

Investment Thesis

It's been almost two years since the regulatory crackdown started. Today's analysis reviews the most critical updates, the current regulatory framework, and what Alibaba investors should expect.

I remain very bullish on Alibaba shares on the Hong Kong Exchange (9988), making it the largest position in my highly concentrated portfolio. This is an investment I plan to own for the next decade, and I am not concerned with short-term fluctuations. But, understandably, BABA/9988 is not for all, and investors should always put their money where their mouth is and invest within their circle of confidence.

Stock Exchange: Hong Kong vs. China

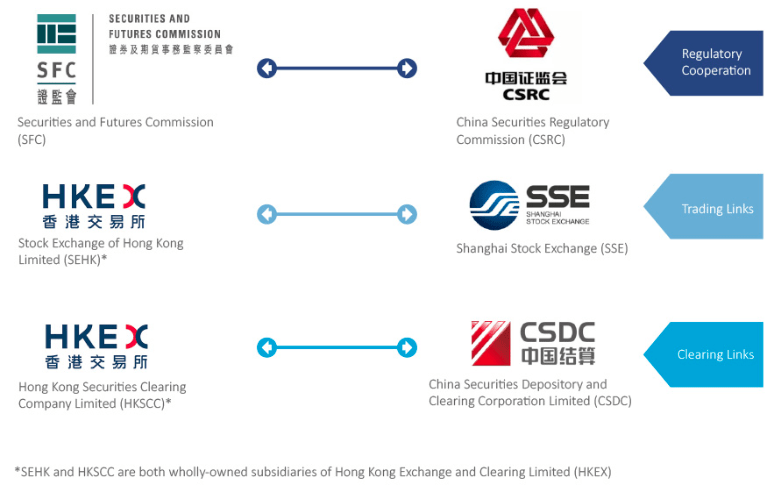

The relationship between Mainland China and Hong Kong is somewhat complex and getting even more complicated regarding politics and economics. As broadly known, Hong Kong has limited autonomy as the People's Republic of China controls it. The Hong Kong Exchange (HKEX) is the preferred destination for Chinese companies that need to raise capital due to the less restrictive and looser financial requirements. In addition, the non-existent capital controls compared to Mainland China are another crucial point for global expansion.

Before launching " Shanghai-Hong Kong Stock Connect " in 2014, retail investors had no access to Chinese stocks. Alibaba is now seeking a primary listing on HKEX, which would allow mainland Chinese investors to access stocks in HKEX. So far, that was not possible since Alibaba's primary listing is on NYSE. This is one of the most critical developments between mainland China and international markets, which aims to facilitate cross-border stock and bond investments.

{kind=link}

Framework (english.sse.com.cn/access/stockconnect/introduction/)

New Pool Of Investors - Liquidity Boost From China & Other Asian Markets

As a result, this stock market connection mechanism between Shanghai, Shenzhen, and Hong Kong will bring massive capital flows from Mainland China for 9988. Some have perceived the recent announcement of dual listing by Alibaba in the market as a desperate move for delisting fears. In fact, it is a diversification move as under the new rules with a primary listing in HKEX, mainland Chinese investors will be able to access it.

As per the company, the trading volumes in Hong Kong have risen since 2019, and the listing will help broaden the company’s investor base in Asia. Undoubtedly, the Chinese government's desire to revive the country's status as an international financial center, which dwindled during the strict lockdown measures of the pandemic years, is in line with support for Hong Kong's stock market and a primary listing closer to Beijing.

However, a transfer like this also gives Chinese businesses the risk of being kicked out of the US. Another important fact is that the mainland China majority includes retail investors rather than institutional as in HKEX, making it more volatile to rumors and news.

Alibaba Can Maintain Its Valuation

Alibaba could become eligible for trading by mainland China-based investors in early 2023 via the Stock Connect program, assuming the company successfully converts to a primary listing in Hong Kong this December. The market interest and implied surge in trading volumes in the internet giant may prompt bourses in the mainland to expedite Alibaba's inclusion in the program.

For example, Zai Lab shares were included as an eligible Stock Connect stock within a month after the firm converted its secondary listing to a primary one in Hong Kong in June. In addition, an increased likelihood of a strong rebound in Alibaba's revenue and profit growth for fiscal 2024 ending March may drive stronger trading from China via the Stock Connect next year. These moves are expected to meaningfully improve the stock's liquidity and support the company's valuation prospects.

Losing NYSE Will Partly Hurt Valuation

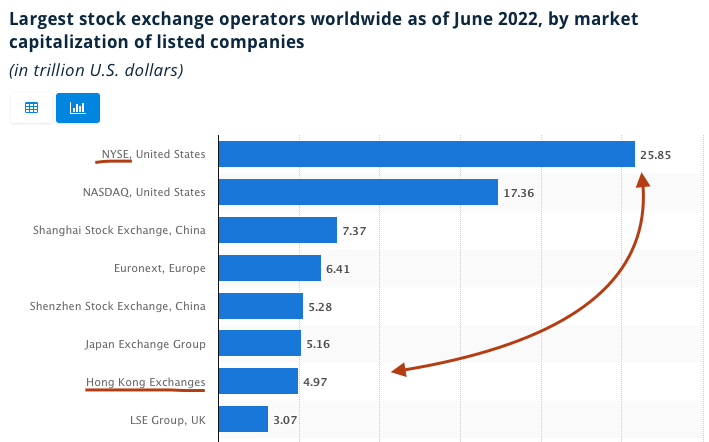

If BABA goes through delisting from NYSE, then HKEX would be the sole and primary listing. As of year-end of 2021, HKEX was the fourth largest in Asia and seventh in the world with a total market cap of $4.97 trillion, nowhere near US exchanges, with NYSE being the largest with a $25.85 trillion market cap , or 5x times larger than HK. Shanghai and Shenzhen Stock Exchange in China report a combined $12.65 trillion market cap which is half of what the NYSE currently has. However, this does not suggest that Alibaba stock cannot maintain its valuation and reach new highs.

{kind=link}

Largest Stock Exchanges (www.statista.com/statistics/270126/largest-stock-exchange-operators-by-market-capitalization-of-listed-companies/)

According to Goldman Sachs, Alibaba could receive up to $30 billion in capital inflows from Mainland China retail investors. However, Goldman's analysts have assigned a 50% probability that Chinese companies would be delisted from US exchanges, down by 95% compared to the chances of that event occurring back in March. Additionally, they estimated that Chinese stocks could crash by 13% in a forced delisting scenario, while a no-delisting scenario could boost shares by only 11% . The relatively low implied volatility indicates that most of the risk is already factored in the Chinese equities listed in the US. In the unfavorable scenario that BABA gets delisted from NYSE, there would be substantial support from mainland China.

Undoubtedly, delisting from NYSE will hurt Alibaba's market valuations and market sentiment to some extent, as a substantial portion of capital might not choose to convert their ADR shares in 9988. However, at this point, the odds of a delisting scenario have been improved in favor of BABA, with the delisting risk being already priced in the stock price, implying limited downside from current levels.

US-China Relations: Audits & De-listing Risk

Earlier in May , SEC's international affairs chief stated that the US Public Company Accounting Oversight Board (PCAOB), the SEC's accounting body, will need to complete China audit inspections by November 22 to meet a US deadline that will require non-compliant Chinese companies to delist by early 2023.

All publicly listed firms must make their audit work documents accessible for review by the PCAOB under the 2002 Sarbanes-Oxley Act. In addition, the board collaborates with more than 50 countries to allow reviews of companies listed in the US. Unlike other countries, China has not permitted the US to audit Chinese companies for years, primarily due to national security concerns, but things have changed.

When It All Started

The long-standing tensions between the two countries grew stronger when Luckin Coffee Inc. ( OTCPK:LKNCY ), a Chinese chain listed on the Nasdaq, was found guilty of intentionally fabricating its 2019 revenue. Just a year after the incident, the US Congress passed the Holding Foreign Companies Accountable Act (HFCAA), which prohibits companies from trading on US exchanges if their audits for the past three consecutive years are unavailable. Earlier this year, the SEC started publishing a list of companies that have not complied with the requirements, which has now grown to over 100 companies, including Alibaba .

As the US and China mull over crafting a workable deal, many Chinese companies have already started exploring alternative options in case of a delisting. In December, DiDi Global Inc. ( OTCPK:DIDIY ) chose to delist from the NYSE under pressure from Chinese officials on concerns related to the exposure of national data to foreign forces. Following in the footsteps of the ride-hailing giant, Aluminum Corp. of China, Sinopec Shanghai Petrochemical Co., China Life Insurance Co., PetroChina Co., China Petroleum & Chemical, and China Petroleum & Chemical have all stated that they plan to cancel their US listings.

What's Next For Alibaba

In its fiscal 2022 annual report, Alibaba also warned that the company might be censured by the SEC. However, a deal between the mainland and American authorities in the next 17 months on the extent of US access to audit work papers of Chinese entities that trade on the NYSE and Nasdaq may settle fears of forced delistings. Following the good news that the PCAOB and China Securities Regulatory Commission have recently agreed to cooperate in inspecting the audits of US-listed Chinese companies, sentiment in the market shows improvement.

Not surprisingly, Alibaba is among the first in line US-listed Chinese companies selected by the US regulators for audit inspection this month. Alibaba's auditor PwC has already been notified. Despite that, most of the working papers are stored in electronic format; some are also kept in their physical format creating logistical challenges in transferring the documents from HK to the US. Nevertheless, investors should stomach the volatility ahead and wait until the landscape clears out later in the year.

Who Audits Alibaba And What Can Go Wrong

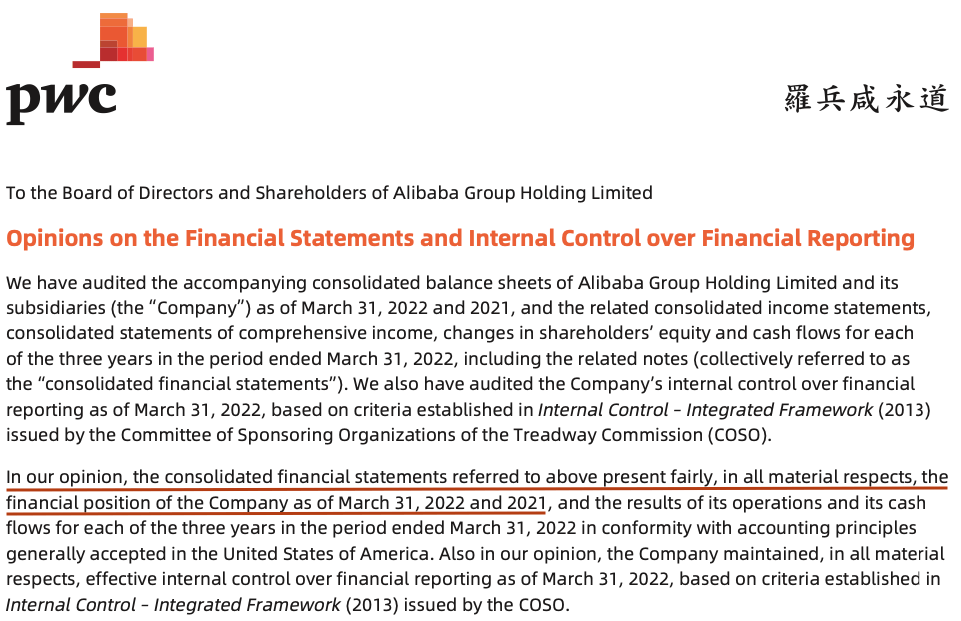

PricewaterhouseCoopers ((PwC) in Hong Kong, one of the big-four accounting firms, has served as the auditor of Alibaba since its inception back in 1999. Having a reputable and resourceful auditor since inception is a great advantage as the auditor can gain a deep understanding of the company's business, Internal Controls, and procedures and handle the massive amount of information and new risk arising yearly with the company's rapid growth.

In the latest annual report, PwC issued a clean audit opinion for the group. It is important to understand that an auditor provides an opinion based on reasonable assurance, meaning that the audit procedures are based on samples, specific audit methodology, and risk models. It is not absolute assurance since auditors can't audit everything. As a result, theoretically, a PCAOB inspection can still find some reporting irregularities, but such a scenario of finding material misstatements is remote, considering the above.

{kind=link}

PwC's Audit Opinion (data.alibabagroup.com/ecms-files/886023430/c330302f-bfdd-4c79-a5ac-614446292e68.pdf)

Why Softbank Group Cut Its BABA Stake

SoftBank Group Corp ( OTCPK:SFTBY ) has announced that it will reduce its stake in Alibaba Group Holding from 23.7% to 14.6% . As a result, the Japanese conglomerate will not sell its shares directly in the market. Instead, it uses a complex security called a "prepaid forward contract" and is set to post a gain of $34.1 billion from the transaction. However, these derivative contracts include the option of buying back those shares in the future. Thus, if Softbank does not exercise the option, it loses its seat on Alibaba's board.

Softbank - Alibaba stake (www.ft.com/content/ca7e1885-055c-43e8-8d2f-96ee5715cf0a)

The settled prepaid forward contracts correspond to a maximum of about 242 million American depositary shares of Alibaba, or roughly 9% of the Chinese company's total outstanding shares. The reduction in Alibaba's stake by Softbank is not due to a negative view of the company in the future, as it seems. On the contrary, Softbank has booked a $34 billion gain and will use the proceeds to finance other bets.

SoftBank booked a $50 billion loss at its investment arm, Vision Fund, in the year's first half as the company’s tech bets plunged. The CEO, Mr. Son, has pledged to reduce investment activity and cut costs. The tech sector has been beaten down during the current year, leaving Softbank cash-starved, which is the primary reason the group is reducing its stake in Alibaba.

The company mentioned in a filing that the reduction in Alibaba shares would help eliminate concerns related to future cash outflows and help the firm reduce costs associated with these prepaid forward contracts. Moreover, the increased cash position will help Softbank strengthen its defense against the “severe market environment."

As a result, the fact that Softbank walks away from Alibaba is a positive development considering the past events and actions of Mr. Son that go against CCP's policies and goals.

Dalio’s Bridgewater Exits BABA

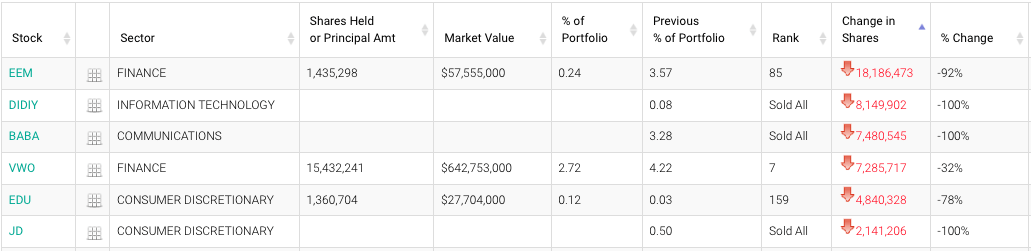

The largest hedge fund in the world, Bridgewater Associates, liquidated its $1 billion worth of holdings in five Chinese technology companies last quarter after the stocks took a beating from increased delisting pressure and regulatory crackdowns.

During the last quarter, Bridgewater sold all of its shares in Alibaba Group Holding, Bilibili, NetEase, and JD.com, according to its latest 13F filing . Moreover, the fund completely sold off its position in the controversial ride-hailing company, Didi. On the other hand, the fund retained its position in the Chinese tech giants Tencent and Baidu with minimal changes.

{kind=link}

Bridgewatter Associates (whalewisdom.com/filer/bridgewater-associates-inc)

Dalio’s decision to sell the Chinese stocks comes at a time of increasing Sino-US tensions and a slowdown in the Chinese economy. Although the firm has not officially commented on the reason for the exit, Dalio has given hints through his LinkedIn post as he stated that the ongoing escalation in US-China tensions over Taiwan is very “dangerous” and has sent the “conflict gauge” to the highest point ever.

I wouldn't view Dalio's decision as a bet against BABA but as more of a sector rotation for its all-weather portfolio towards Chinese EVs from the consumer discretionary sector. The latter is expected to shrink in the short term due to increasing interest rates and worsening consumer purchasing power.

Ant Group IPO To Be Further Delayed

Mr. Ma is planning to give up control of Ant Group, a change that would further delay the Chinese financial technology giant’s plans to launch an initial public offering. The mogul, who has no official positions at Ant, currently holds 50.52% of the company's voting rights . However, he may cede part of his voting authority to CEO Eric Jing and senior Ant leaders.

Giving up control for Mr. Ma would mean that Ant would hold off its hopes of restarting IPO for at least one year and potentially as long as three , depending on where the group eventually chooses to sell shares. If a company's controlling shareholder changes, it must wait up to three years before listing on the mainland, while Hong Kong requires a year-long hiatus.

Mr. Ma's exit might pave the way for Ant’s eventual IPO in the future, and the financial group will be relieved from a major 'key man risk'. Even though Ant’s wait for IPO will increase in case of this change, it won't necessarily be bad for Ant, as right now, the company is in no rush to be listed due to poor market conditions.

Cloud Business Remains The Growth Catalyst

Lastly, Alibaba's cloud business has been among its fastest-growing segments. The cloud business grew by 10% YoY to RMB 17.7 billion in Q1 2023, driven by recovering demand from non-Internet industries, including financial services, public services, and telecommunications. As demand from the internet sector slows, management believes the next leg of growth will come from the industrial internet and plans to capture opportunities in vertical industries. As a result, revenue contribution from non-Internet industries reached 53% during the quarter, indicating a 5% YoY increase.

On the technology side, Alibaba Cloud introduced a proprietary cloud infrastructure system called Cloud Infrastructure Processing Unit in June, and its AI language technology ranked second among global cloud AI developer service vendors, per Gartner’s report released in May. As a result, the cloud segment now captures 40% market share in China and roughly 5% worldwide.

Global Cloud Market Share (holori.com/cloud-market-2022/)

Concluding Thoughts

Undoubtedly, the headwinds for Alibaba are not over, and several key risks are attached to the stock. Indeed, the Chinese government has been more restrictive on fair competition, anti-trust, personal data protection, media, and content, cracking down on social media and vertical video platforms. In addition, data-driven advertising businesses could potentially see targeting ability impacted, thus their monetization capability.

However, despite the regulatory crackdown, Alibaba's profit margins and growth have not crashed as expected. Amidst the speedy recovery of China, the post-C ovid economy is resuming its growth trajectory, and the regulatory outlook has already started clearing up. Finally, there is light at the end of the tunnel, and we are getting closer to a new pivotal phase for the international markets, where Alibaba could come out stronger than ever.

For further details see:

Alibaba: All You Need To Know