BABA - Alibaba Stock: Undervalued With Substantial Risks

2024-01-20 08:06:50 ET

Summary

- Alibaba's stock has faced challenges due to the pandemic and Chinese government regulations, but it is currently undervalued.

- The company's sales and gross profit have remained stable despite negative news and regulatory pressures.

- Upside risks include opportunities in artificial intelligence, chip design, content strategies, and the evolving landscape of streaming and TV.

- Alibaba is a Chinese company. American investors might be concerned with the country's accounting standards and also the US-China relations.

The last couple of years were really tough for Alibaba (BABA) and its stock. First, the coronavirus pandemic, second, the Chinese government's regulations rattled the country's tech sector. Right now many risks remain and the stock might fall further. However, BABA does seem undervalued right now.

Recap of my previous article on Alibaba

In my last article, I issued a "Bullish" rating on Alibaba for the following reasons:

- The company's stock was quite undervalued. At the same time, most of the sales growth decline was due to the suffering Chinese economy. Note that there was no sales decline . Only the growth pace has slowed down. This is still quite an achievement, given the complicated external factors.

- Alibaba had departments that performed well and were very profitable.

- Most of the stock price declines were due to the Chinese government's attempts to regulate the largest high-tech companies, Jack Ma's retirement and also the coronavirus-related economic slowdown.

- I also compared BABA to the ultra-popular Amazon (AMZN), saying that the latter seemed worse value for money than BABA.

However, the fact the fundamental factors are all there does not mean Alibaba's stock will rise dramatically overnight. Moreover, even if all the fundamental factors are against the company, this does not necessarily mean its stock price would collapse immediately.

Generally speaking, this is particularly true of popular high-tech growth companies. Even if the results are not improving much and the stock valuations are incredibly high, there is still a chance its loyal army of fans will keep pumping the stock price upwards. A lot of investors, or better said speculators, do not quite realize this.

In fact, my first ever article on Alibaba was written in October 2020 and was published under the title " Here Is Why I Dumped My Entire Alibaba Stock Position In Spite Of My Love For The Company ". After my analysis was published, BABA stock increased in value. This only lasted for a couple of months, however. But as I am writing this, the company's stock has lost almost 50% of its value since the publication of my article. The point I am making is that you never know what will happen next. In this article I will mostly focus on the new factors.

Alibaba's news

Since Q4 of 2020 has Alibaba's stock been depreciating due to negative news. First, Jack Ma retired. The Ant Group IPO was cancelled, whilst the Chinese authorities charged Alibaba heavy fines. There were also plenty of economic concerns about China, including the country's real estate bubble, its demographics, a potential recession ahead, and the cancellation of a cloud business spin-off.

However, in spite of the negative flow of news, the company's sales and gross profit have not suffered much. In fact, they have remained quite stable. The only exception was 2022, when the net profit was substantially lower compared to 2021. But still, no net loss was recorded. Moreover, as concerns TTM performance, Alibaba is recovering.

{kind=link}

In this respect, I fully agree with my fellow Seeking Alpha contributor Steven Fiorillo that the financial performance has not been poor all these years. The only problem here is that Alibaba has not performed like a growth company.

Upside risks

But bears should be aware that BABA stock has plenty of upside risks. The first and foremost is its exposure to artificial intelligence and chips.

In 2022 Alibaba Group's cloud computing division presented a platform for developers to produce AI-enabled edge chips leveraging the RISC-V instruction-set architecture.

The Wujian 600 platform was developed by Alibaba's in-house chip development business. The platform supports edge-AI computing, a form of machine learning that sees AI applications used in physical devices.

Thanks to the platform firms are enabled to design edge-AI Systems-On-Chips that combine multiple computing systems into one package.

The platform will reduce development costs and shorten the design cycle of chips to facilitate the mass production of these AI Systems-On-Chips.

The Wujian 600 will support the development and prototyping of Alibaba Cloud 's SoC TH1520, which has already been used inside Alibaba's ecosystem.

As I have mentioned in the previous section, the company's earnings results are not terrible either. In other words, they do not suggest Alibaba is facing incredible earnings and sales growth but they do not show the company is struggling at all. So, the market might eventually realize that and the stock would eventually appreciate.

The fact the tech sector faced some regulatory pressures from the Chinese authorities does not mean it will do so forever. In fact, the country's government is clearly supporting platform companies, meaning that there will be potential easing of probes. Premier Li Qiang's called for regular communication with platforms. Also, the NDRC's endorsed investment projects. All that shows China is willing to use new technologies to drive economic growth and job creation. According to China Briefing , this means the end of the tech crackdown is near. In other words, this too shall pass, whilst the market seems to assume the regulatory crackdown is here to stay.

Another very important factor that investors should be aware of is the company's leadership position in China. JD.com (JD), the country's second e-commerce company, does not have the market share equivalent to that of Alibaba. Although China does, indeed, face problems of slowing demographics and an economic slowdown, it still remains one of the leading growth economies in the world. The Bank of China is increasingly dovish. It has recently held the interest rates unchanged at 2.5% but added some additional liquidity . If the outlook deteriorates further, the Bank of China will highly likely ease further, thus stimulating the country's economy, including the high-tech sector.

Valuations

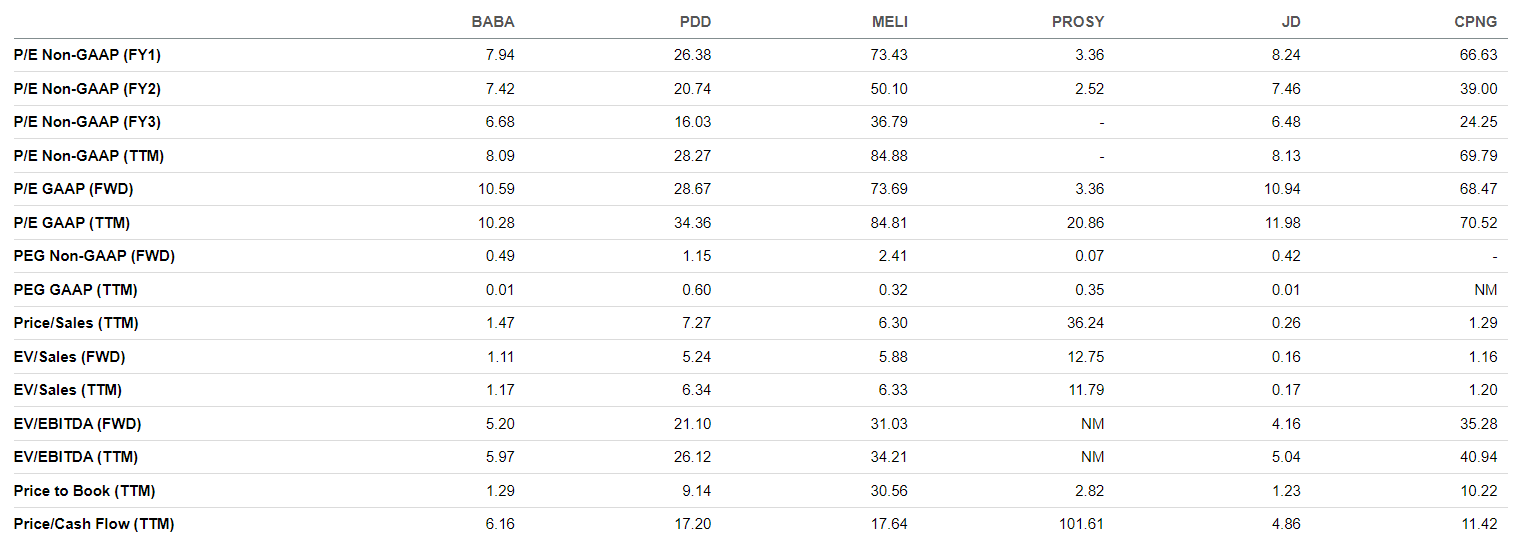

As I have mentioned above, the company's stock is far too undervalued. Only Prosus (PROSY) is cheaper than BABA in terms of P/E Non-GAAP and even FWD P/E GAAP. As concerns the EV-to-EBITDA and the price-to-book (P/B) ratios, Alibaba's are really low. Only these of JD.com are lower.

{kind=link}

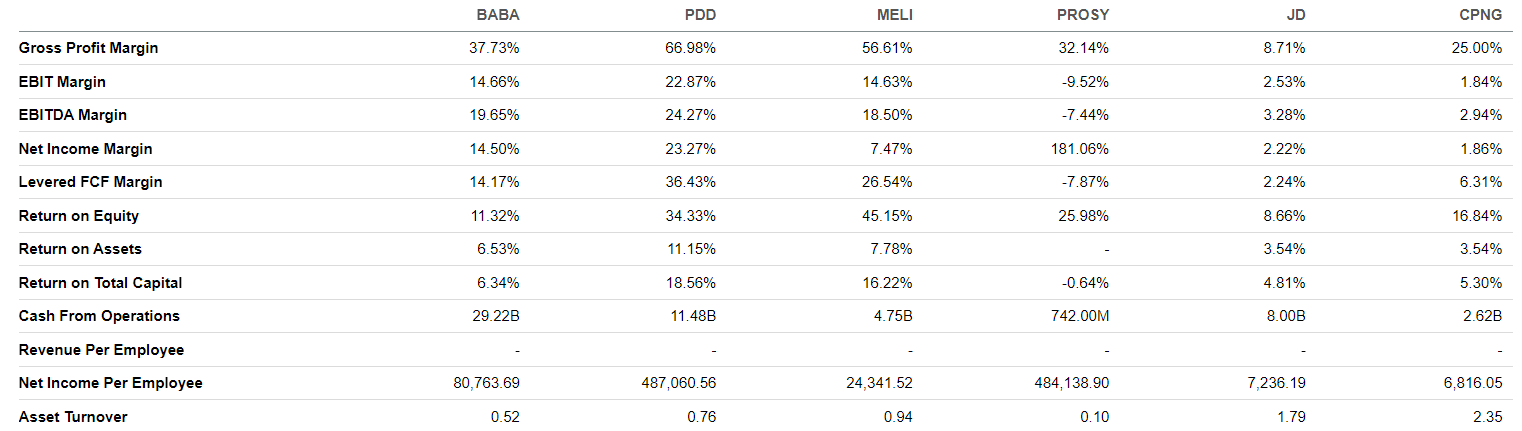

Simultaneously, BABA has reasonable profitability margins, including the net income margin and the return on assets, compared to these of its peers.

{kind=link}

Not to mention that Alibaba's stock is trading near multi-year lows.

Alibaba's earnings have been performing much better than its stock price, another sign of undervaluation.

So, overall, we can clearly say that BABA stock is undervalued.

Risks

The first and foremost risk that some analysts do not take into account is the fact the accounting standards in China are different from the ones in the US. Indeed, Chinese companies listed in the US need to publish their accounting reports in accordance with the GAAP regulations.

According to CNN , US inspectors, namely The Public Company Accounting Oversight Board (PCAOB), discovered significant shortcomings in audits of companies based in China and Hong Kong that are listed on US stock exchanges. Some time ago the PCAOB received access to auditors' books for the first time. Although this additional regulatory scrutiny was most probably due to the US-China trade war, some US investors might want to be extra cautious, whilst investing in Chinese companies.

Moreover, the relations between the US and China are also getting worse due to tensions around Taiwan. So, there might be additional pressures from the US authorities on Chinese companies. Obviously, Alibaba will also be affected.

As I have mentioned before, the Chinese government now seems to be more lenient towards high-tech companies. But this risk cannot be fully disregarded.

Another obvious risk is that of a full-scale recession. Obviously, the Chinese economy will also record poor performance, whilst Alibaba's EPS indicators will go down.

Conclusion

Although Alibaba is cheap compared to where it is in terms of earnings and sales, many risks remain. The Chinese government has become more lenient towards the high-tech sector. But the deteriorating US-China relations and tensions around Taiwan remain the most obvious political risks. Moreover, investors might remain cautious towards buying Chinese companies' shares, even though Chinese companies listed on US exchanges have to abide by GAAP accounting standards. Finally, many market players want to see high EPS and sales growth, which was not exactly the case with BABA.

For further details see:

Alibaba Stock: Undervalued With Substantial Risks