ALCO - Alico: Buy The Low-Hanging Fruit

2023-11-14 02:36:47 ET

Summary

- Alico’s shares sold off following a dividend cut and hurricane damage to its citrus harvest. Shares continue trading at a discount to NAV despite substantially all trees remaining intact.

- Strategic project to invest in additional citrus tree plantings increased tree density within Alico citrus groves. Many new trees are now mature enough to produce meaningful fruit quantity.

- Alico has a significant amount of capital tied up in legacy assets that are non-core to the citrus business.

Editor's note: Seeking Alpha is proud to welcome Legacy Investments as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Alico ( ALCO ) is a small cap agribusiness company that utilizes its ownership of approximately 72,000 acres of Florida land for cultivating citrus trees to produce citrus for delivery to the processed and fresh citrus markets. The damage from Hurricane Ian to the company's 2022-2023 citrus harvest harmed the company's short-term ability to generate any income from operations and shares trade at a significant discount to NAV.

Increased operating revenues from a recovery in the company's citrus production during the 2023-2024 harvest will provide management with significant options take advantage of the company's shares trading at a significant discount to NAV. Improvements in grove efficiency and any pickup in the pace of non-core asset sales will amplify the positive effect of a recovery in operations and would generate substantial value for Alico shareholders.

The Market Is Frustrated By A Write-Off Year

The 2022-2023 citrus harvest has been difficult for Alico. Sustained high winds from Hurricane Ian caused a significant drop of fruit from its citrus trees. Although crop insurance is maintained on all Alico's groves for catastrophic events, not all of the groves had suffered enough damage for insurance claims. This meant Alico would need to record an impairment charge to its inventory, in addition to reducing the expected quantity of 2022-2023 citrus fruit that would be available for conversion to operating revenues. Faced with essentially a write-off year, in December 2022 management announced a 90% reduction in the quarterly dividend from $0.50 to $0.05.

In response to the dividend cut, Alico shares have declined -22.94% with little sign of recovery:

{kind=link}

Since the wind damage primarily affected citrus fruit inventory growing during the 2022-2023 harvest and did not have a substantial effect on the expected future ability of Alico's citrus trees to produce fruit, my belief is that Alico will not be facing the same revenue constraints during the next harvest. CEO John Kiernan expressed a similar sentiment in the management comments of Alico's press release for Alico's Q3 2023 financial results:

Our consistent grove caretaking practices, combined with the new citrus greening therapy we began to apply this year, gives us confidence that Alico's production will substantially increase for the 2023-24 citrus harvest season, as compared to the 2022-23 citrus harvest season. Of the millions of trees we planted beginning in 2017, many are now mature enough to produce meaningful quantities of fruit this season and help support a level of expectation for a better upcoming harvest for Alico.

It is my belief that the tree plantings referenced in the second sentence will have a separate favorable effect on future operating revenues in excess of the Hurricane Ian recovery since these trees were planted as part of a decision to increase density at Alico's groves, rather than replace aging trees.

Alico 2.0 Modernization Program

Alico had announced in 2017 the start of a modernization program that would make several changes, with the goal of improving operational efficiencies and optimizing asset returns. One of the changes focused on by the program was to increase the overall density of Alico's citrus groves. This was to be done by investing in a level of tree planting that substantially exceeded the attrition rate of old trees.

According to a press release by Alico, the optimization of grove density was completed in early 2021:

Alico expects its increased plantings of approximately 1.5 million trees over the last four years has the potential in the long term to return the Company's annual citrus production to 10 million boxes, a level last experienced in fiscal 2015. Citrus trees typically take approximately four years after planting to generate meaningful production and usually reach mature production after seven or eight years.

Confirmation from Alico that many of the trees from its density optimization strategy are mature enough to produce meaningful quantities of fruit during the 2023-2024 citrus harvest should then have a favorable impact on operating revenues that is separate from and in addition to the favorable impact of not experiencing the sustained high winds from Hurricane Ian that had caused fruit drop in the 2023-2024 harvest.

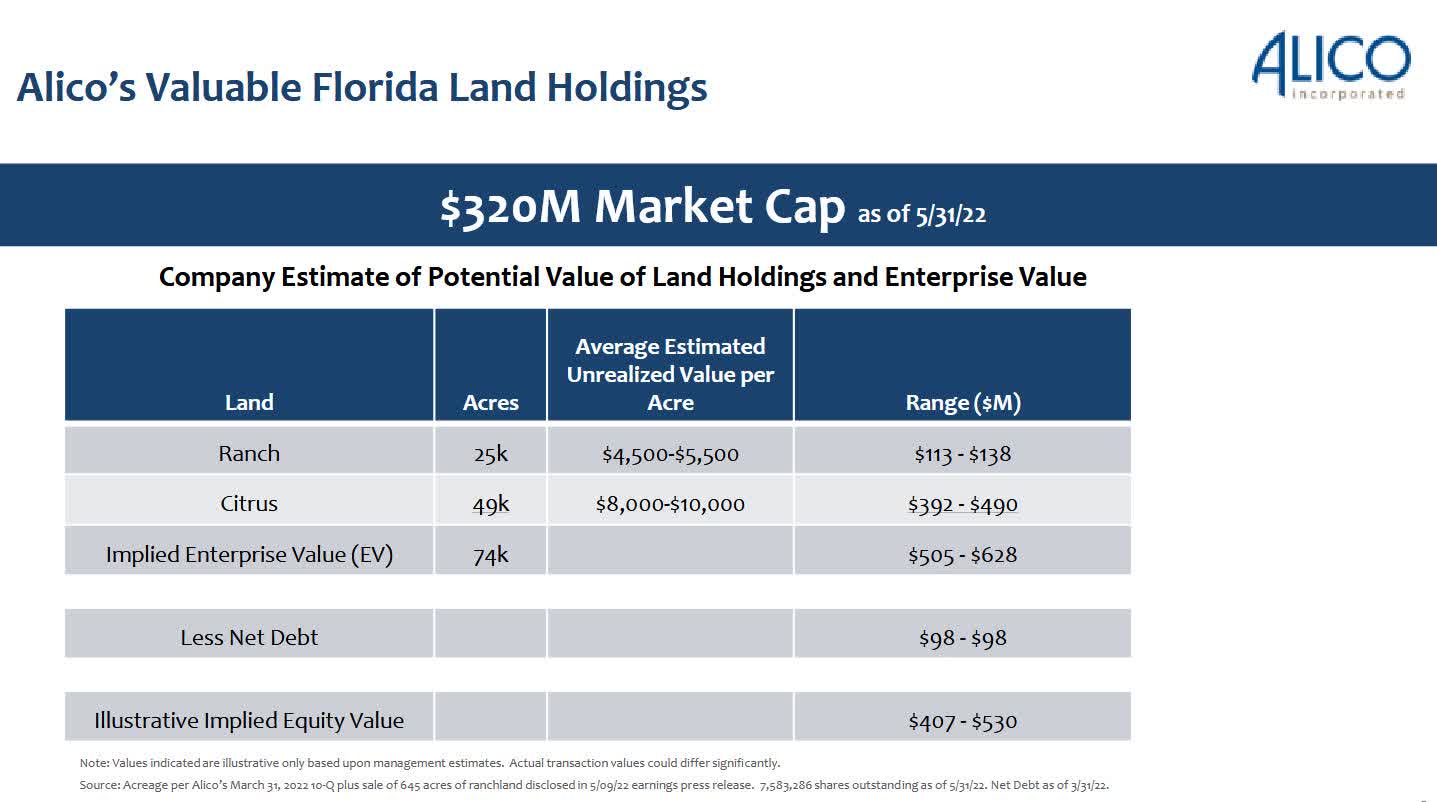

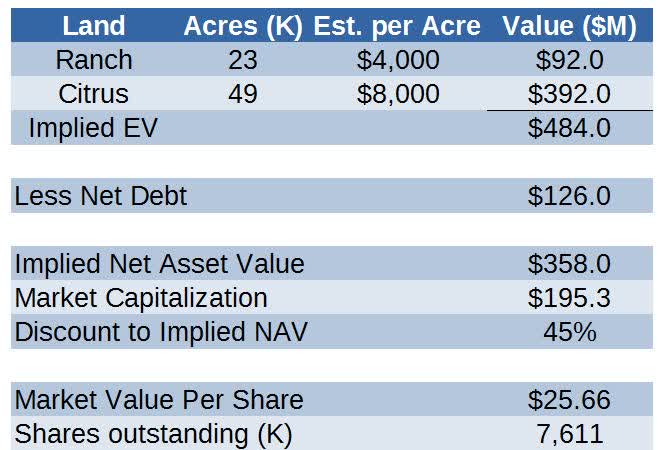

Estimating Current Discount To NAV

Alico has calculated and published estimates for the potential value of its land holding in the past, although the latest presentation is from early 2022:

{kind=link}

A few figures have changed, such as the sale of certain ranch acres. I've updated an estimate for NAV based on the latest 10-Q and used a conservative estimate for the value per acre that appears reasonable based on approximately comparable land sales and listings:

{kind=link}

Based on the above calculations, the implied discount to NAV for Alico shares has moved from trading at a conservatively valued 21% discount in May 2022 to my estimated discount of 45%.

Non-Core Assets Tie Up Significant Capital

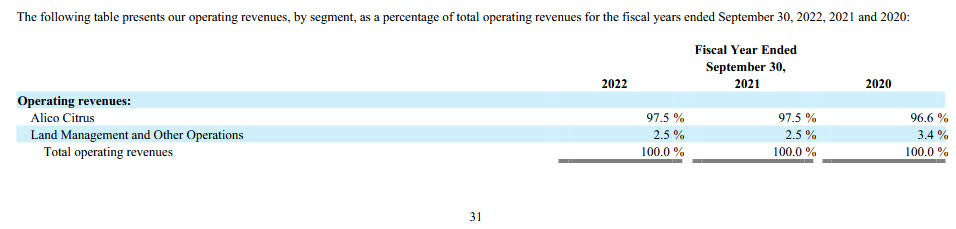

Operating revenues at Alico have historically been overwhelmingly generated by Alico Citrus:

{kind=link}

I maintain that Alico ranch lands should be considered non-core assets since they have not historically generated any material operating revenues and since there does not appear to be any future plans to utilize them in producing significant revenues beyond plans to opportunistically sell the acreage at favorable prices. Since the implied value of these non-core ranch assets are equivalent to approximately half of Alico's market capitalization and Alico shares are trading at a 45% discount to NAV, significant value could be unlocked if management makes strong efforts towards marketing and selling the remaining ranch acreage.

There could be reason for optimism on this front since CEO John Kiernan commented on the most recent 10-Q's media release:

The Company is actively engaged with interested third parties on certain parcels of additional ranch land at prices we continue to believe are competitive

However, optimism could be misplaced since in Alico's most recent 10-Q filing they indicate that only 1,436 ranch acres have been sold since June 2022. Those ranch acres were sold over several smaller transactions and it would be disappointing if the "certain parcels" referenced in the media release are of a similar size.

Concentration Risks

Significant risks exist stemming from the company's concentrations in geography, customers, and industry.

All citrus groves owned by the agribusiness are located in parcels in central and south Florida in relatively close proximity to one another. Florida has historically been particularly susceptible to weather-related events, such as hurricanes and tropical storms. Lacking groves in another area, the loss of fruit and destruction of trees from a weather event has the potential to materially impair the company's ability to generate revenue from operations for a multi-year period. This is only partially offset by catastrophic insurance carried on the company's fruit-bearing trees.

During the prior fiscal year , the company's contracts with Tropicana accounted for 90.1% of total revenues. The loss of Tropicana as a customer, or a significant reduction in business, would require Alico to find replacement buyers and would take time and expense, with potentially less favorable terms of sale. This risk was heightened by the recent sale of Tropicana by PepsiCo to a French private equity firm, although Alico has since extended their contract with Tropicana with a two-year extension through the 2024-2025 harvest season.

The citrus business has historically provided the overwhelming majority of Alico's operating revenues, at 97.5% in the prior fiscal year. Citrus greening is one of the most serious citrus plant diseases in the world and has devastated citrus crops throughout the United States and abroad. Once a tree is infected, it produces fruits that are green, misshapen, and bitter, which are unsuitable for sale. Although there is currently no known cure, earlier in 2023 the EPA approved the trunk injection of a formulation to combat citrus greening which is expected to increase yield and fruit quality. If mitigation efforts to this industry-wide problem are unsuccessful, the reductions in available citrus could have significant adverse effects on Alico's operating revenues.

Conclusion

Alico's share price has still not recovered since last year's dividend cut triggered a selloff, leaving shares trading at an estimated 45% discount to NAV. Management appears to have options to take advantage of this share mispricing and generate significant value for Alico shareholders. Substantially all citrus trees appear to be intact from the hurricane-related problems that affected the last harvest, and many of the new citrus trees planted as part of the Alico 2.0 modernization project have reached fruit-bearing maturity in time for the 2023-2024. harvest. Management continues to work towards the opportunistic sale of non-core ranch acreage that has an implied value of approximately half the company's market capitalization.

In my opinion, the market has not yet reacted appropriately to the potential operating revenue of Alico's citrus groves in light of the recovery from hurricane Ian and the increased density of mature fruit-bearing trees. Although the sale of non-core assets has been proceeding slower than shareholders would like, a more aggressive effort by management in the sale of Alico ranch assets could unlock significant liquidity for shareholders. Based on these factors and the margin of error created by a 45% discount to NAV, I rate Alico a buy at the current share price of $25. I currently own a position in Alico and intend to further add to that position. If we see further pricing weakness in Alico shares, if positive information emerges regarding the 2023-2024 citrus harvest, or if we see more aggressive ranch land sales, then I will keep adding shares to my position.

For further details see:

Alico: Buy The Low-Hanging Fruit