ALCO - Alico: Raising To A Buy On Valuation

Summary

- Alico is one of the largest citrus growers in the U.S with ~49,000 acres of citrus groves.

- Hurricane Ian is set to make F2023 a writeoff year for Alico.

- This has caused the stock price to be dislocated, trading at roughly half of the real estate value.

- I believe value investors with a long-term investment horizon may find Alico's shares attractive.

A few months ago, I wrote a cautious article on Alico, Inc. ( ALCO ), noting that although the company has a lot of underappreciated real estate, near-term results would be negatively impacted by Hurricane Ian.

In my article, I warned:

The biggest near-term risk to Alico is Hurricane Ian's impact to the upcoming fiscal year. If the upcoming season is as bad as F2018 (37% decline YoY), then Alico could be looking at significant operating losses.

Indeed, the negative impacts of Hurricane Ian was the main focus of the most recently reported Q4 earnings report and earning conference call.

Brief Company Overview

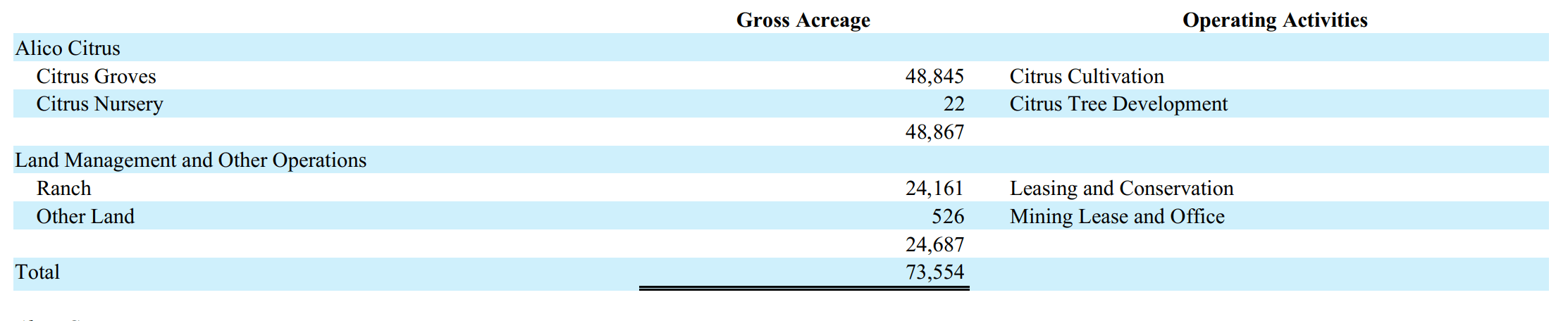

First, a brief review of the company for those not familiar. Alico, Inc. is a Florida citrus grower that owns and/or manages 83,000 acres of land in eight Florida Counties (Charlotte, Collier, DeSoto, Glades, Hardee, Hendry, Highlands and Polk). Alico derives the vast majority of its revenues and earnings from tending ~49,000 acres of owned citrus groves and ~7,000 acres for third parties. Alico is one of the largest citrus growers in the U.S. and supplies fruit for Tropicana juices.

In recent years, Alico has also been selling parcels of ranch land to third parties to reduce debt and fund capital returns to shareholders.

2022 Marred By Weather

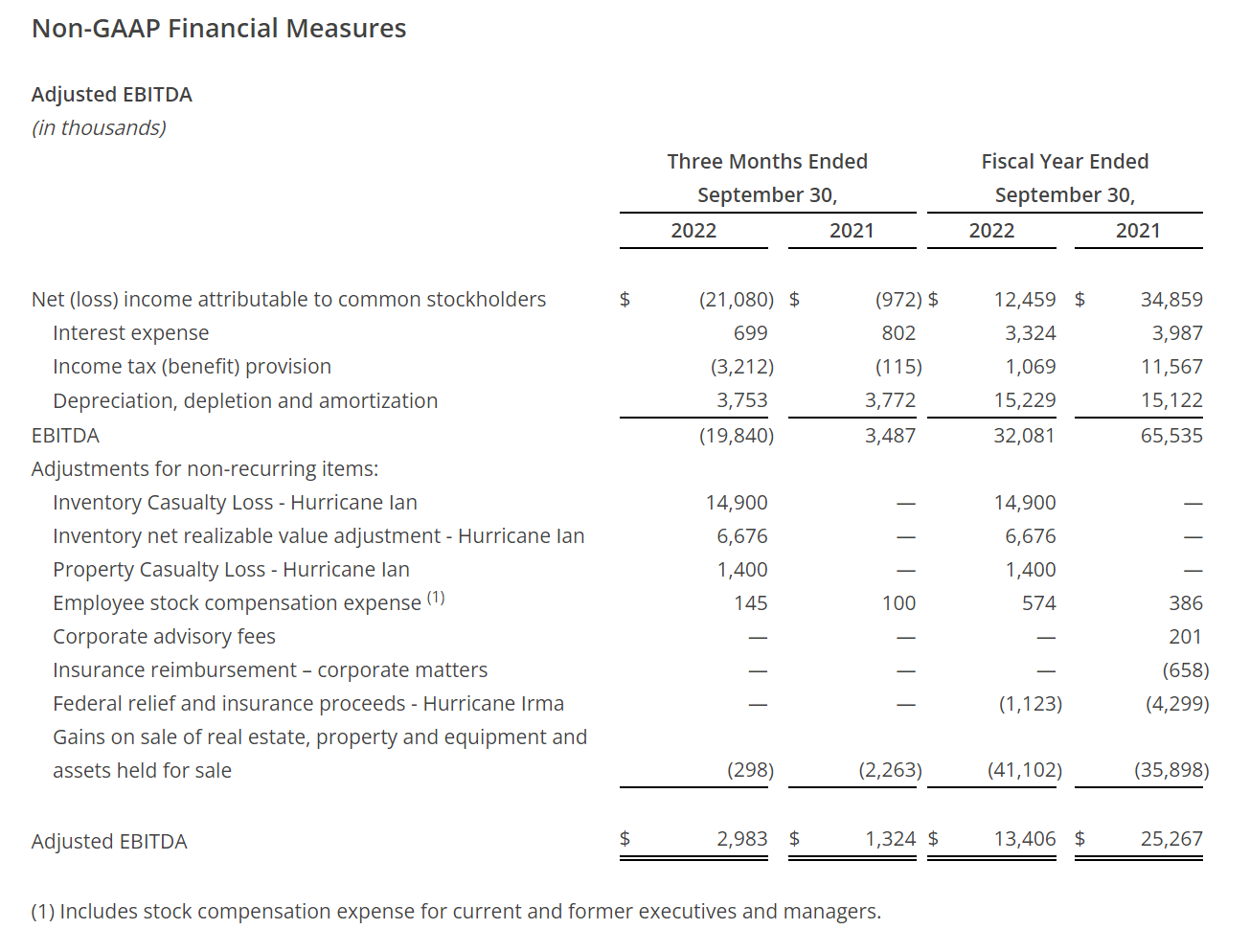

In the recently reported Q4 earnings, we can see Alico quantified Hurricane Ian's immediate impact as $23 million in one-time losses, split between $14.9 million in inventory casualty loss, $6.7 million in inventory net realizable value adjustments, and $1.4 million in property losses (Figure 1).

Figure 1 - One-time losses from Hurricane Ian (ALCO Q4/2022 press release)

{kind=link}

Despite the one-time losses, Alico was still able to report $1.65 in diluted EPS for fiscal 2022, primarily on the back of realized gains from the company's land sales. In fiscal 2022, Alico sold 9,400 acres of ranch land, and recognized $41 million in gains on sale.

2023 Will Be A Writeoff Year

However, the bigger impact from Hurricane Ian would be felt in Alico's F2023 revenues and sales, as the storm caused significant fruit drop and damaged the trees at one of Alico's groves. Management commented in the earnings press release that:

Fiscal year 2023 will see lower levels of revenue because we have less fruit available for sale. Based upon our prior experience with storms of this nature, we anticipate it may take up to two seasons or more for our groves to recover to pre-hurricane production levels.

As I warned in my prior article, 2023 will most likely be a writeoff year for Alico, and management's comments confirmed my thesis.

Due to the uncertainty regarding damages to Alico's citrus crop (it is too early to tell whether the remaining fruit on trees will continue to ripen), the company also declined to provide guidance for fiscal 2023.

Cuts Dividend To Conserve Capital

Also notable in the earnings report was management's decision to cut its quarterly distribution 90% to $0.05 / share for the upcoming quarter. I believe this decision is prudent, given the uncertainty surrounding the upcoming fiscal year.

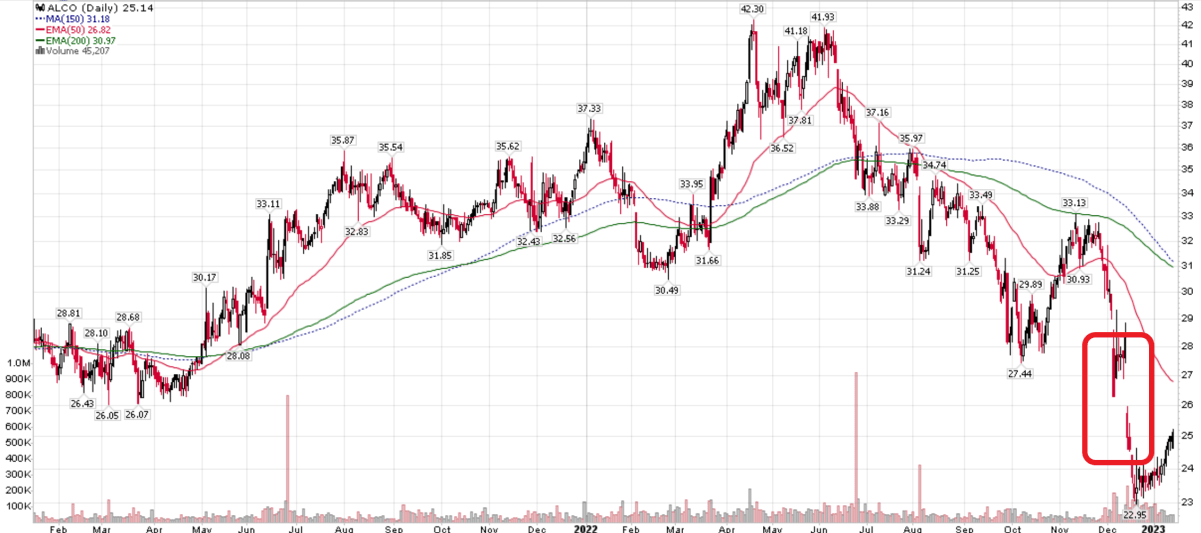

However, investors did not take kindly to the poor earnings report and dividend cut, punishing the stock with a 9%+ drop on the earnings report date (Figure 2).

Figure 2 - Investors punished Alico's stock on the poor earnings report (Author created with price chart from stockcharts.com)

{kind=link}

Why Didn't Insurance Cover The Losses?

From some of the comments I have seen regarding Alico's results, investors seem to be wondering why Alico's losses from Hurricane Ian haven't been covered by insurance.

Alico indeed does maintain catastrophic crop insurance on its citrus groves. However, filing insurance claims is a lengthy process, and Alico is currently working with its insurers to assess the damages from Hurricane Ian and to determine how much, if any, insurance payouts the company is entitled to.

To get a sense of how long it takes to make insurance claims and receive payments, consider this tidbit from the Q4 earnings call: (author highlight for emphasis)

During the fiscal year ended September 30, 2022, we received approximately $1.1 million of additional proceeds under the Florida Citrus Recovery Block Grant program relating to Hurricane Irma damage sustained in September 2017 . Through September 30, 2022, we received approximately $25.6 million of proceeds under this program. These federal relief proceeds are included as a reduction to operating expenses in the consolidated statements of operations.

During the first quarter of fiscal year 2023, we have received the remaining portion of the funds that are due under this program related to the reimbursement of certain crop insurance expenses incurred by us of approximately $1.3 million.

- CFO Perry Del Vecchio on the Q4/2022 earnings call

In the first quarter of fiscal 2023, Alico is still receiving federal relief payments relating to Hurricane Irma damages sustained in 2017!

Moreover, since Alico's citrus groves were not completely destroyed by Hurricane Ian (thankfully!), the company will have to wait until the end of the current crop season to measure the actual crop harvest to determine the hurricane's damages and insurance payouts.

Despite Near-Term Headwinds, Long-Term Value Remains

Although uncertainty has clouded the outlook for Alico's near-term results, I believe the company's long-term value remains relatively unscathed.

First, as I mentioned in my previous article, Alico made a strategic decision to increase the density of its groves after Hurricane Irma, planting ~700k trees above the historical replacement level. As citrus trees typically bear fruit 4-5 years after planting, we should begin to see the positive impact of Alico's densification in 2023 (Figure 3).

Figure 3 - Alico planted an additional ~700k trees beyond replacement level (ALCO investor presentation)

Furthermore, the significant land value that I highlighted in my prior article remains unchanged. Figure 4 shows Alico's land holdings as of the latest 10K report.

{kind=link}

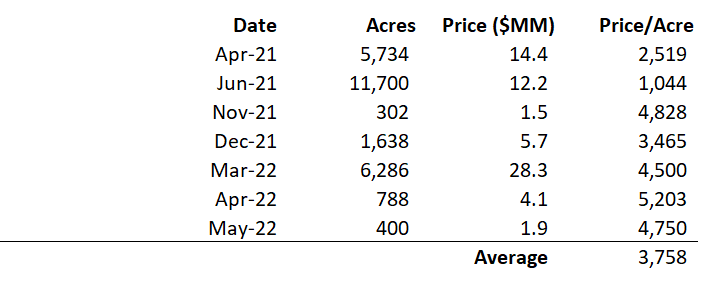

Figure 5 summarizes recent transactions on Alico's ranch lands. In the past two years, Alico's ranch lands have transacted at an average of $3,750 per acre, with the most recent 3 transactions averaging $4,820 per acre.

Figure 5 - ALCO ranch land transactions (Author created with data from 10K reports)

{kind=link}

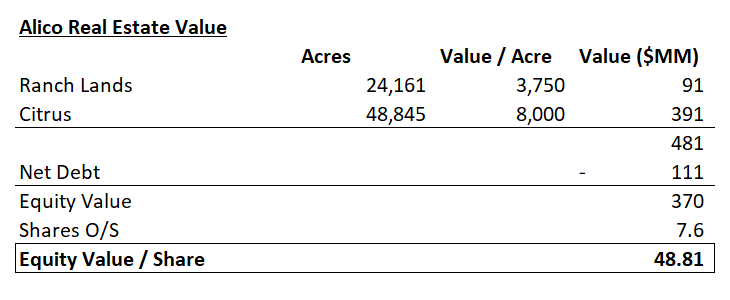

Applying the average $3,750 per acre value to Alico's ranch lands imply more than $90 million in value. Furthermore, citrus groves trade between $8-10k per acre. If we apply a value of $8,000 per acre to Alico's citrus groves, that implies more than $390 million in value. Putting it all together, I estimate Alico's real estate assets are worth $49 per share, almost a double from the current share price (Figure 6).

Figure 6 - ALCO asset value (Author created with balance sheet data from tikr.com)

{kind=link}

Risks

The biggest near-term risk to Alico remains the uncertainty in fiscal 2023 operating results. We know it will be bad, but so far, management has not provided guidance on how bad. Using Hurricane Irma as a guide, Alico's revenues declined by 37% in F2018. If history were to repeat, the upcoming F2023 could be an operating loss year. Furthermore, elevated labour and other costs could pressure operating margins.

In the long run, large storms appear to be occurring more frequently due to climate change. Changing climate patterns may even make citrus growing within a concentrated geography unfeasible, as a single large storm can ruin a whole season's harvest.

Perhaps one possible solution is to merge Alico with a west-coast citrus grower to diversify the company's geographical base, such that when a storm hits Florida and sends orange prices soaring, the company can take advantage by selling west-coast production at higher prices to recoup losses.

Conclusion

Alico's upcoming F2023 results are going to be negatively impacted by the effects of Hurricane Ian. However, the underlying asset value remains, underpinned by the company's ~49,000 acres of citrus groves and ~24,000 acres of ranch land. I estimate Alico's real estate to be worth $49 / share, almost a double from current share prices. With share prices falling another 20%+ since my initial report while long-term value remaining unchanged, I am raising Alico to a speculative buy, suitable for value investors who have a long-term investment horizon.

For further details see:

Alico: Raising To A Buy On Valuation