ALIT - Alight: Sticky Business Model And A Discounted Multiple

2023-04-16 23:57:20 ET

Summary

- Alight is well positioned to benefit from secular tailwinds such as the fight for talent, WFH, and globalization of the workforce.

- The company has a highly recurring and durable revenue model, with 80% of revenue recurring under multi-year contracts.

- Alight's transition to BPaaS is a significant growth driver, combining SaaS capabilities, automated service delivery, and data and AI for cloud-hosted solutions.

- My end-of-year price target of $15 on the stock is based on a 12.0x EV/EBITDA multiple applied to CY24 Adj. EBITDA estimate of $835 million.

Thesis

Alight, Inc. ( ALIT ) offers solutions for employee management, such as benefits, payroll, and wealth services, through a single integration point. Due to the complexity of managing employees during the pandemic, Alight's services have become increasingly important for employers. As a result, the company has a strong and stable business model with high recurring revenue and customer retention rates, and I anticipate that the company's BPaaS transformation will accelerate growth and increase profit margins, leading to significant upside potential. My end-of-year price target of $15 on the stock is based on a 12.0x EV/EBITDA multiple applied to CY24 Adj. EBITDA estimate of $835 million.

Company Description

Alight is a prominent provider of cloud-based integrated digital solutions for human capital and business. The company leverages data analytics and AI to provide BPaaS (Business Process as a Service) for payroll and benefits administration, all of which are centralized onto their Worklife platform. Alight serves clients across various industries and has expanded globally into 100 countries through a combination of organic and inorganic growth strategies. The company has a workforce of over 16,000 employees and caters to more than 4,300 clients and 30 million employees and their families.

Business Model Overview

Alight generates its revenue through three categories, namely Employer Solutions, Professional Services, and Hosted Business. The majority of the revenue, about 86% in 2021, is from Employer Solutions, which provides benefits administration and payroll and HR management services. Alight typically charges a contracted fee per employee per period, with the contract usually lasting 3-5 years. Implementation fees may sometimes be included in the contracts, but they are not payable until the ongoing administration phase. The fees become payable on a monthly basis once due.

Alight's Professional Services category contributes about 13% of its revenue and is responsible for providing assistance with SaaS deployment and integration, testing and data conversion. The company has formed partnerships with major organizations such as SAP, Workday, Oracle, Cornerstone OnDemand and SuccessFactors to deliver their Cloud Deployment Solutions and Cloud Application Services. Alight is highly experienced in this area, having completed over 800 Workday deployments and currently serving over 400 Workday customers, with 2.7 million employees on the Workday payroll.

Highly Recurring Revenue Model

Alight has a vast client base, serving over 30 million individuals, including 14% of the US working population, through 3,000 enterprise clients , half of which are in the Fortune 500. Its position as the top provider of tech and admin solutions in health, the largest independent provider of wealth solutions in wealth, and a top employer of Workday-certified engineers in HCM is a result of its 25-year operating history, which has prepared it to serve the shift towards digital human capital management and employee engagement.

Approximately 80% of Alight's revenue is derived from recurring multi-year contracts with established enterprises, including 70% of the Fortune 100. The company has a high client retention rate of 98% , and its top clients have an average tenure of over a decade, indicating strong client loyalty. The majority of revenue is based on a per participant per year (PPPY) fee model for core health and wealth administration rather than on AUM or wages paid. This fee structure leads to highly recurring and visible revenues as employers and employees prioritize wellness.

Transformation to BPaaS

Alight's transition to BPaaS (Business Process as a Service) is a significant growth driver, as it combines SaaS capabilities, an automated service delivery model, and data and AI to provide cloud-hosted solutions for businesses. Unlike traditional on-premise solutions that require installation on local computers and servers and internal IT management, BPaaS solutions are managed remotely by an external vendor and accessible via the internet. This transition will accelerate the prospecting-to-implementation period from 12-18 months to 6-9 months.

BPaaS accounted for 18% of Alight's revenue and around 30% of bookings in 2022. As BPaaS becomes a larger portion of revenue, margins are expected to expand due to revenue benefits and cost reductions. For instance, Alight earns an average uplift of 1.5x annual recurring revenue on bundled health BPaaS deals. In 2022, Employer Solutions gross margin was 33.5%.

Company Presentation

Valuation

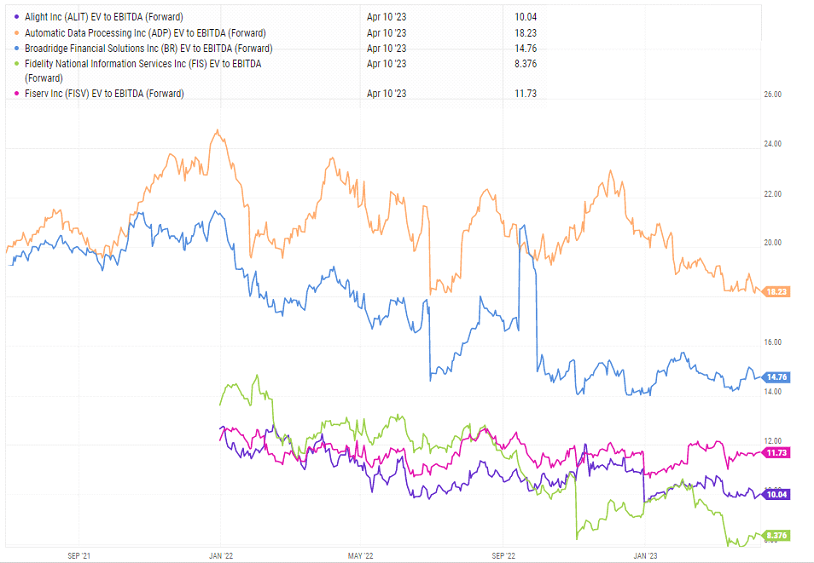

While I don't expect ALIT's multiple to hit the high-teens EV/EBITDA benchmark of established payroll peers like Automatic Data Processing, Inc. (ADP), I believe that over time these best-in-class HR providers could become aspirational valuation comps if ALIT is able to show consistent and stable results. Particularly given its slightly faster growth profile and line-of-sight into solid margin expansion off a lower base (~21% EBITDA margin vs. ADP at 29%).

I see Broadridge Financial Solutions, Inc. ( BR ) as a reasonable valuation comp, given its role as a core enterprise infrastructure provider with high switching costs. BR trades at mid-teens forward EBITDA multiple, a significant premium to its mid-single-digit EBITDA growth, demonstrating the value investors assign to stable and consistent enterprise software + service names. BR (similar to ADP and PAYX) pays a healthy low-single-digit yielding dividend, which creates a value floor for the stock. However, I still see an upside to ALIT's current valuation relative to BR given faster revenue growth and margin expansion.

My end-of-year price target of $15 is based on a 12.0x EV/EBITDA multiple applied to CY24 Adj. EBITDA estimate of $835 million. This multiple is roughly consistent with ALIT's historic multiple. I view my price target as justified, considering similar growth horizontal or vertical scale processing peers all trade at double-digit multiples. As such, I see significant multiple expansion potential if ALIT is able to establish a track record of stability and consistency as a core enterprise infrastructure provider.

{kind=link}

Risks

In the event of an economic downturn, Alight's revenue growth could be negatively impacted as new sales and client participation rates may decline, particularly with enterprise clients who may be less willing to switch critical infrastructure, slowing Alight's transition to BPaaS, which is critical for its medium-term operational improvements. As a result of its exposure to enterprise clients, Alight's revenues may suffer if these employers reduce their labor force, as a Federal Reserve study found that they are at least as likely if not more so, to do so during recessionary periods. Alight's performance is also reliant on its Partner Network and Cloud HCM Partners, who deploy and operate HR management solutions, and the company is dependent on third-party software licenses to provide services, although the performance of its Worklife integrations is beyond its control.

Final Thoughts

I believe that now is the opportune time for Alight to capitalize on its position as the leading scale platform provider of modern benefits programs to enterprises, with a heightened focus on employee wellness following the pandemic. Alight's business model is sticky, with a high rate of recurring revenue and exceptional retention rates. The transformation to BPaaS has the potential to accelerate growth and improve margins, providing significant upside potential. I anticipate that Alight will experience strong revenue growth until 2025, along with double-digit EBITDA growth. My end-of-year price target of $15 on the stock is based on a 12.0x EV/EBITDA multiple applied to CY24 Adj. EBITDA estimate of $835 million.

For further details see:

Alight: Sticky Business Model And A Discounted Multiple