ALHC - Alignment Healthcare: An Attractive Entry Point After A Price Drop (Rating Upgrade)

2023-05-15 09:00:00 ET

Summary

- ALHC's patient-centric, proactive approach has earned it high scores in the CMS' 5-star rating benchmark, lowering hospitalization rates and overall costs.

- The company has demonstrated a promising growth trajectory, with total revenue increasing from $345 million in Q1 2022 to $434 million in Q1 2023.

- Despite an increase in medical expenses due to the onboarding of new members, ALHC has strategically managed these costs to aim for long-term efficiency.

- A significant 55% drop in share price, coupled with consistent profitability improvements, makes ALHC stock an attractive investment.

Author's Note: I have previously covered Alignment Healthcare ( ALHC ) in previous articles. This article builds on insights previously discussed, so I recommend revisiting the earlier coverage for context.

Investment Thesis

With an aging population and escalating healthcare costs, the need for innovative approaches to elderly care has never been more important. One company that has risen to the challenges is Alignment Healthcare . The company focuses on providing patient-centric, coordinated care for seniors, diverting from the fragmented and impersonal healthcare landscape. Through its integrated healthcare model, ALHC has better aligned its interest with its patients, capitalizing on the CMS' monetary incentives to innovative approaches that enhance the quality of service while decreasing costs.

The company's focus on proactive, personalized, and convenient care has earned its flagship plan a 4-star rating from the CMS, allowing it to stand out in a highly competitive market characterized by low barriers to entry. According to management, the majority of its growth stems from plan switchers rather than new Medicare Advantage enrollees. This holistic approach to care not only enhances care quality but, equally importantly, has resulted in lower hospitalization rates, thus, lowering overall costs, aligning its interest with patients and the CMS

The company is still unprofitable, but unlike many of its peers, the relatively new insurance start-up has demonstrated the validity of its business model, consistently delivering profits on a gross-margin level. The path to profitability through scale is more clear compared to its peers.

Recent Results

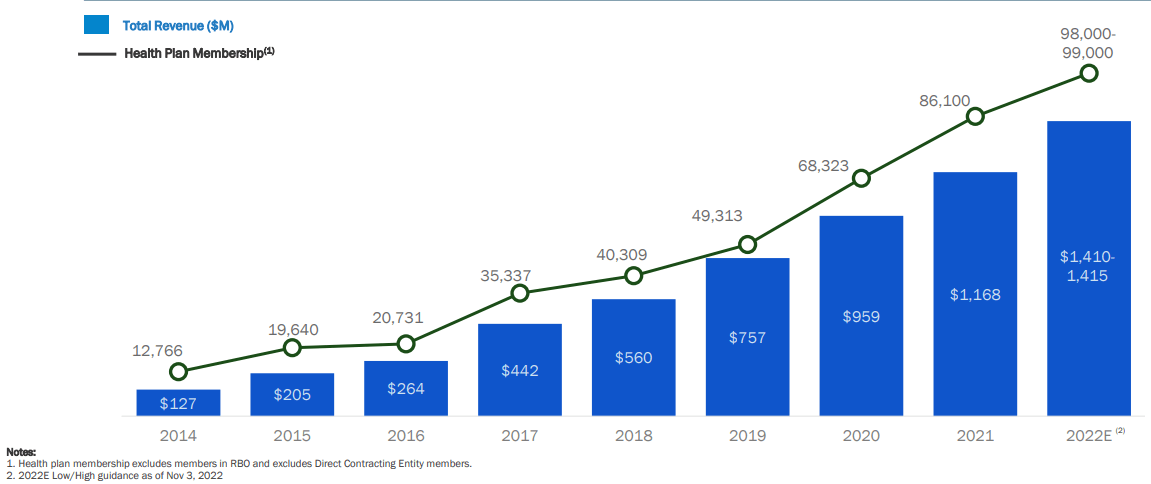

ALHC's total revenue has shown a promising uptick, growing from $345 million in Q1 2022 to $434 million in Q1 2023. This result mirror's ability to effectively market its healthcare plans, a feat that stands out particularly when compared to its struggling counterparts. Take, for instance, Bright Healthcare, which is now looking for a buyer for its last foot in the healthcare insurance market. Similarly, Clover Health ( CLOV ) membership declined in both its Accountable Care Organization "ACO" and Medicare Advantage "MA" segments in Q1, mirroring a tough enrollment season (October- December).

{kind=link}

ALHC

However, this revenue growth was outpaced by an increase in medical expenses, which jumped from $303 million to $396 million over the same period. These dynamics are expected in the industry and are linked to the costs of integrating new members into healthcare plans. New members often require more extensive and expensive healthcare services resulting in initially higher expenses.

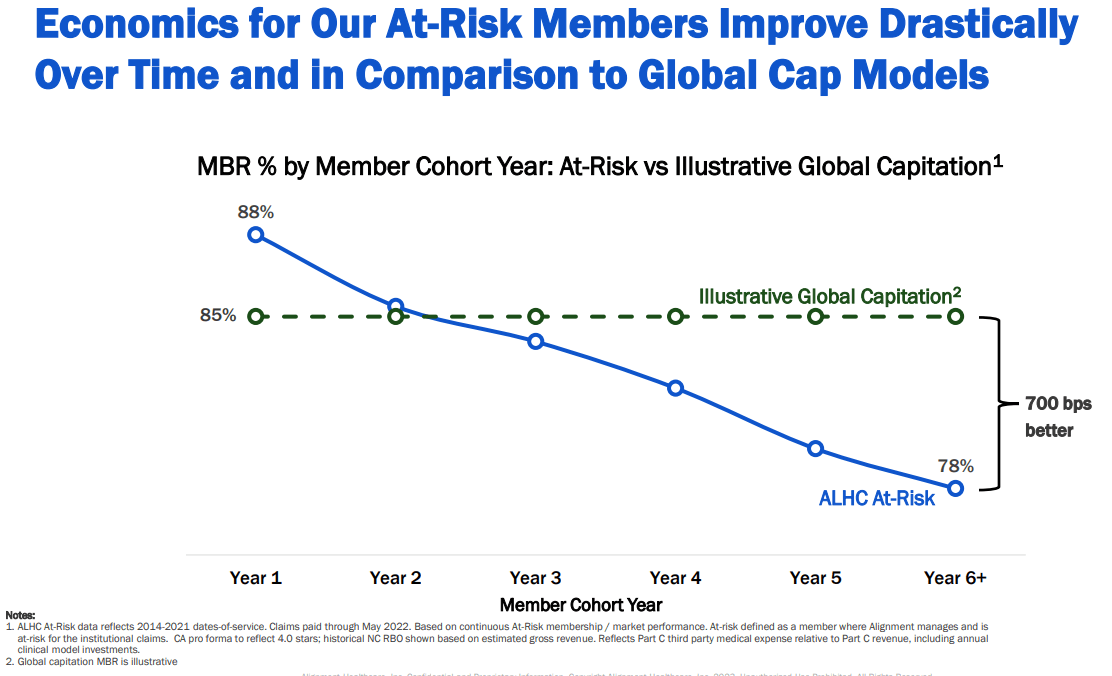

The business model of ALHC operates on a proactive approach to healthcare, with the objective of gradually reducing these costs over time. This strategy necessitates an increase in healthcare services as new members adjust to their plans. Thus, the surge in medical expenses can be interpreted as a calculated strategy aimed at achieving long-term cost efficiency rather than a mere financial challenge.

{kind=link}

ALHC

Moreover, ALHC succeeded in reducing net loss (and net loss per share) thanks to a reduction in SG&A expenses, which decreased from $74 million in Q1 2022 to $70 million in Q1 2023, mirroring operational efficiencies and scalability, crucial factors for long-term sustainability and profitability in the healthcare insurance sector, where gross margins are restricted to 15% to 20% by lawmakers.

The current positive cash flow reported in Q1, while encouraging, should be understood in the context of exceptional circumstances arriving from the CMS's premiums prepayment for the month of April, which was recorded as deferred revenue for the three months ended March 31st, 2023, quarterly report. It is reasonable to assume that the cash flow from operations will revert to a more typical pattern in the coming quarters. Still, overall, I believe that Q1 2023 was a successful quarter.

Verdict

Earlier this year, I shared my assessment that ALHC was fully valued. Since then, the ticker has declined 55%, underperforming its peers and the market. In light of these developments, I believe that at the current price, ALHC offers an attractive entry point for investors.

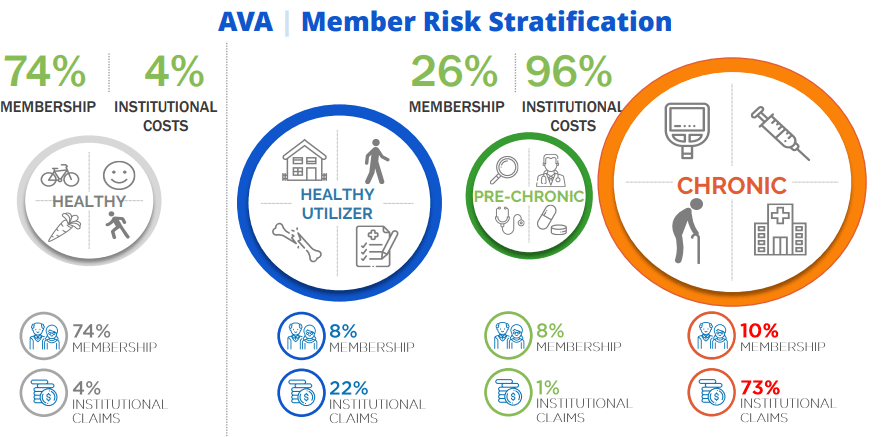

The company has consistently shown its ability to attract new members and effectively manage the initial onboarding costs, which are an integral part of its business model, rather than a setback. Approximately 26% of ALHC members represent 96% of costs. By providing a proactive care approach to a small group of patients, ALHC has been able to lower the number of emergency visits and ultimately lower medical costs.

{kind=link}

ALHC

The combination of ALHC's proven operational approach and a significant 55% drop in its share price since my previous article underlies my decision to upgrade the company's rating today. On average, a typical healthcare insurance company generates a net income return of about 5%. If we apply this rate to ALHC's projected revenue for the next year, we arrive at a forward income estimate of $86.5 million. Assuming a scenario where ALHC achieves profitability, this would correspond to a PE ratio of 14x. This figure is notably lower than the industry average PE ratio, which hovers around 20x, suggesting that ALHC's current valuation may offer an attractive entry point for potential investors.

Financial Position

In the past few years, ALHC maintained an average operating cash outflow of $40 million. Despite this, the company managed to sustain a robust balance sheet, with cash and cash equivalents totaling $384 million. This significant cash reserve allows ALHC to cover its operating expenses for an estimated eight more years, providing it with financial stability and flexibility to solidify its market position as it continues to implement its growth plans.

Moreover, unlike many of the other start-ups in the healthcare insurance sector, ALHC demonstrated confidence in its financial sustainability by maintaining a long-term debt balance of $161 million. When compared to its total current assets, which amount to $670 million, including $103 million in marketable securities and the above-mentioned $384 million in cash and cash equivalents, this debt load is relatively small. This strong financial position mitigates the company's need to raise capital, thus, insulating it from current volatile market conditions and the prevalent high costs of capital in both equity and bond markets.

How I Might Be Wrong

Although I believe that ALHC presents an attractive investment opportunity, there are several factors that could challenge my thesis. First, the competitive landscape in the healthcare sector is fierce. ALHC faces competition from both new market entrants and start-ups vying for a piece of the pie and more established players such as Humana ( HUM ) and UnitedHealth Group ( UNH ) with deeper pockets and wider provider networks.

Also, it is critical to note that ALHC is not yet profitable. While I am optimistic about the company's growth trajectory, both in terms of revenue and bottom line, the path to profitability is not guaranteed.

Summary

ALHC has risen to the challenge of providing innovative patient-centric elderly care in a market characterized by inflating healthcare costs and an aging population. The company is unprofitable. However, it stands out among its peers, showing potential for positive returns through its consistent gross margins, membership base growth, and improving net income and operating cash flow metrics, showcasing its ability to gradually leverage its operations into profitability through economies of scale. This feat is not to be taken lightly, given that the industry is fraught with companies whose financials cast doubts over the viability of their business model and approach to elderly care. For these reasons, I believe that the 55% share price drop in the past few months opens an attractive entry point to start accumulating ALHC shares.

For further details see:

Alignment Healthcare: An Attractive Entry Point After A Price Drop (Rating Upgrade)