CLOV - Alignment Healthcare: This Next-Generation Medicare Startup Is Fully Valued

- ALHC belongs to a group of managed care startups recently going public, using tech to enhance efficiencies and product offerings.

- The company adopts a holistic approach to healthcare, leveraging recent regulatory changes that expanded Medicare supplementary benefits.

- At current prices, ALHC is fully valued.

Investment Thesis

Alignment Healthcare's ( ALHC ) guiding philosophy of "doing well by doing good" underpins its comprehensive approach to healthcare, earning it a place among the richest Medicare Advantage "MA" carriers in the industry. For example, the company offers 24/7 concierge service, free transport, companion services for the lonely elderly, monthly allowance for over-the-counter healthcare items, pet-sitting, and other services that encourage a healthy lifestyle, such as free gym membership.

ALHC proved the sustainability of its business model. By investing in supplementary healthcare benefits, the company lowered the frequency of hospitalizations, reducing the overall medical expenses, as mirrored in its profitable Medical Benefits Ratio ((MBR)).

GAAP profitability is still a work-in-progress, anchored by non-cash expenses, including Stock-Based Compensation "SBC" for upper management. ALHC has a narrow scope compared to peers, operating in only four states (California, Nevada, Arizona, and North Carolina.) Nonetheless, I expect the company to leverage its successful model into profitability as it expands into new geographical regions, namely Florida and Texas, this enrollment season.

The main issue in ALHC is its share price, which seems to mirror its attractive business model, and growth prospects.

Industry Overview

It is not difficult to start a Managed Care company, and in many states, you can start with as little as $100,000. You can find specific requirements for each state here, but broadly speaking, beyond a pro forma financial statement prepared by an employee with actuarial qualifications, you are set to go. The bottom line is that barriers to entry to the sector are low, partially offsetting the benefits of expanding markets, manifested in favorable demographic trends often cited by MA companies. Hundreds of firms of all sizes participate in the MA-CMS program each year. You can find a directory of all 2022 plans and parent organizations here .

Theoretically, an MA plan provider, such as ALHC, can ask the CMS any amount to cover its members during the bidding process. However, on average, the Federal government will pay $12,000 per member per year and pass the remaining costs to ALHC members. Given the high competition, most plans ask for a conservative capitated payment per member, mostly at or under what the CMS covers, i.e., $12,000, so their members don't have to pay extra above the $170 monthly premium they pay the CMS. This is how Medicare Advantage companies can offer $0 premium plans, often with no coverage limits. Practically, seniors eligible for Medicare pay the CMS $170 per month in premiums (usually deducted from Social Security payments), so it is not exactly free. The CMS then pays roughly $12,000 per month per member to ALHC (and all other companies participating in the program) for the coverage. In fact, 32 out of ALHC's 38 plans have zero premiums, and the company mostly earns its revenue from the CMS.

Insurers also have little incentive to cut service quality to increase margins because the Affordable Care Act set a maximum limit to gross margin at 15%. This profit should cover all non-medical expenses, including overhead, management compensation, marketing, and administrative costs. However, because of the high competition, insurance companies seek to lower costs anyway and reinvest what they save into a more robust offering, thus attracting more members and achieving profitability through scale instead of margin. Moreover, service quality factors in the CMS's payment mechanism through a star rating system.

MA plans offer more value to seniors compared to Traditional Medicare. For example, Traditional Medicare deductibles for Part A and B are $1,556 and $233 for each claim, respectively. After a member pays these expenses, the CMS will cover 80% of hospitalization and ambulance costs, with no limits on Out Of Pocket total payments by the member (the remaining 20% co-pay). On the other hand, ALHC's most popular plan in California is a $0 premium plan, with free Part D drug coverage, $0 deductible, $0 co-pay, and a maximum out-of-pocket of $999.

ALHC negotiates favorable pricing with physicians and hospitals in return for traffic. ALHC channels its members to its network by charging extra for out-of-network healthcare services. For example, in-network consultation co-insurance costs $0 compared to $50 for an out-of-network provider. This negotiation underpins the superior efficiency of the private sector in dispensing healthcare coverage compared to the CMS, which has an open network and doesn't negotiate for better prices (notwithstanding last week's Inflation Bill, passed by the Lower House of Congress last week, which allows the CMS to negotiate drug prices.)

Revenue Trends

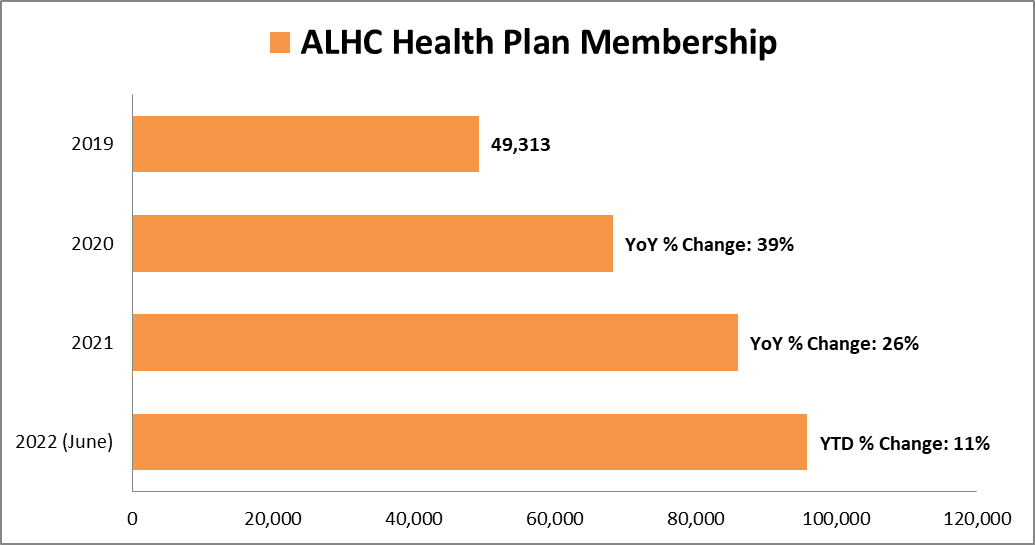

There is limited data to assess ALHC's growth drivers. The company was formed in 2013, but only went public last year. Nonetheless, here are some factors to consider when looking at its membership figures in the graph below.

As mentioned above, increasing competition from new entrants partially offsets the benefits of demographic trends manifested in the US aging population. Seasonality exists in the managed care sector due to the timing of the enrollment season, starting in October and ending in December. Thus, ALHC records most of its growth in Q1 of each year.

Beyond demographic trends, growth depends on the number of counties the company operates. ALHC can only expand geographically during the bidding process, which from my understanding, starts in January and ends in August, applying to enrollees the following year.

For example, earlier this year, the company announced it is expanding in two new states; Florida and Texas. Most likely, it already won a bid for several counties in these states. From my understanding of how management operates, they most likely already established a provider network and marketing strategy (including agreements with healthcare brokers within these counties), fully prepared when enrollees start signing up for Medicare this enrolment season, commencing October and ending December 2022.

ALHC grew its members by 11% this year, after expanding its geographical coverage from 22 to 38, which isn't exactly a spectacular performance. One can say that t he success of its anticipated geographical expansion is not guaranteed and depends on many factors, including the concentration of Medicare-eligible citizens in targeted counties. For example, California has more Medicare-eligible seniors than the smaller 19 states combined. Another example is its dim performance in Nevada and North Carolina. The company has been operating in Nevada since at least 2018 and expanded in North Carolina in 2019 for CY 2020. Yet almost 90% of members are in California. Understanding these dynamics is a reality check as we assess the company's planned expansion in Texas and Florida.

{kind=link}

Valuation

ALHC is not cheap, whether compared to second-generation managed care startups such as Clover Health ( CLOV ) or incumbent healthcare insurance giants such as Humana ( HUM ) and UnitedHealth ( UNH ).

One would argue that CLOV and ALHC have different market positions, warranting higher valuation for the latter. For example, ALHC's MBR ratio has been below 100% since at least 2019, mirroring a sustainable business model, despite its holistic approach towards healthcare, encouraging its members to claim benefits it deems necessary for healthy living, the same approach that helped its flagship plan gain a four-star rating from the CMS, above that of CLOV's 3.5 stars. CLOV MBR for MA members turned positive this year after disruptive COVID dynamics pushed it above 100%. CLOV's direct contracting MBR remains above 100% with about 170,000 members, compared to 5,000 for ALHC. One would ask, what is direct contracting, and why does ALHC have a few of these? To answer this question, one must know the difference between Preferred Provider Organization "PPO" and Healthcare Management Organization "HMO."

Seeking Alpha

CLOV primarily maintains PPO insurance plans, a term that describes coverage with fewer restrictions on specialist consultations and referrals. In an HMO, the primary structure of AHLC plans, each member is assigned a primary care physician who organizes a member's treatment, including giving authorization for a specialist physician visit. Because of CLOV's more open network, it is assigned more members in CMS's direct contracting business. I have been covering CLOV for a while now, and I don't believe that ALHC's price premium is warranted, despite their differences.

ALHC's price premium over market incumbents such as HUM and UNH reinforces this conclusion. On average, mature healthcare insurance companies earn around a 4% net income margin. Applying this figure to AHLC's revenue run rate based on its latest quarterly sales yields a pro forma net income of $59 million or $0.31 EPS (based on 184 million shares outstanding), translating to a 47x PE ratio, more than double its more established peer UNH and HUM. In other words, the company needs to triple its revenue to reach a 15x PE ratio. These dynamics are mirrored in Seeking Alpha Quant Score, as shown below.

Seeking Alpha

Summary

ALHC maintains profitable MBR , verifying its comprehensive healthcare model that encourages members to use supplementary benefits, leveraging recent regulatory changes that extended CMS coverage to include transportation, companion services, and over-the-counter grocery and health products. As the company grows, I believe there is a high chance it will leverage its way into profitability.

However, the company is fully valued at current prices. Possibly, its revenue will grow enough in the long term to create capital gains. Still, in relative terms, the company is expensive compared to other opportunities in the market today, underpinning our hold rating.

For further details see:

Alignment Healthcare: This Next-Generation Medicare Startup Is Fully Valued