ANCTF - Alimentation Couche-Tard Investor Day Suggests More Profitable Growth Ahead

2023-12-13 10:00:00 ET

Summary

- Alimentation Couche-Tard (ATD) announces its five-year strategy with a focus on growth, cost improvements and M&A.

- ATD aims to drive a total of $4.3 billion in incremental EBITDA by FY28.

- M&A and integrating the TotalEnergies acquisition will play a big part.

- The stock continues to be fairly priced with room for upside.

Alimentation Couche-Tard (ANCTF) held its Investor Day on October 1 1th and released its Q2 earnings report on November 29th . The company laid out the plan for the next five years and how earnings could almost double again.

Since my last article , the stock has made another leg up, continuing its steady outperformance. The article focused on ATD's ambitions in leveraging technology to gain an edge and grow through M&A, now that the deal environment is improving. The company announced that the Total Energies store acquisition is almost ready to close and has delivered good results since then. M&A is an integral part of my thesis, and it is good that this transformational deal is close to going through. The Investor Day shared updates about future value creation for the company. Without further ado, let's get right to it.

I will refer to the company as ATD, its Canadian ticker or Couche Tard throughout this article.

ATD 10 year outperformance (Seeking Alpha)

{kind=link}

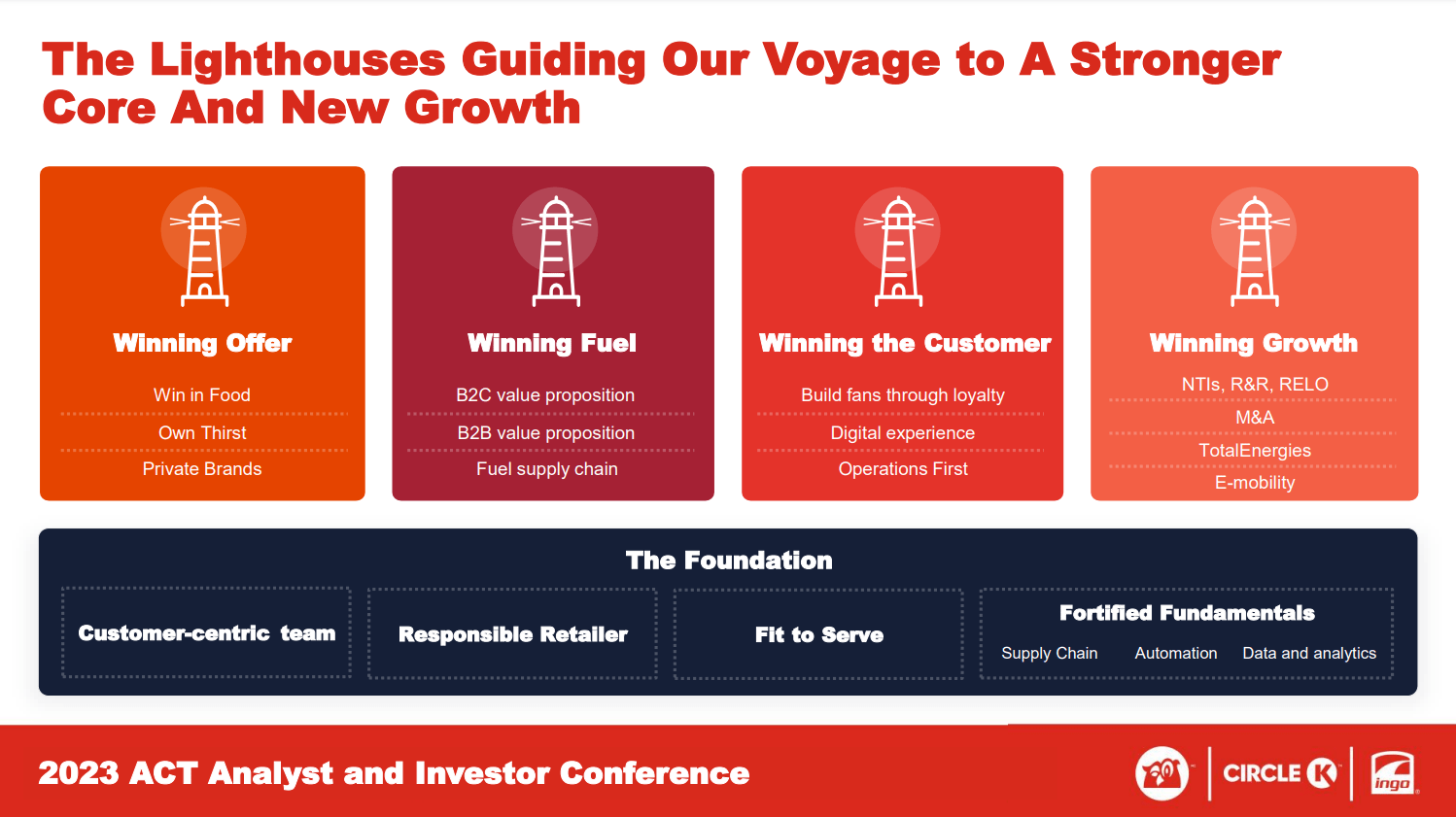

ATD announced its next five-year strategy with a lighthouse analogy for the four key pillars of growth and the underlying foundation, as seen in the picture below. Let's review each of these pillars.

ATD Lighthouse Strategy (ATD Investor Day)

{kind=link}

Winning Offer

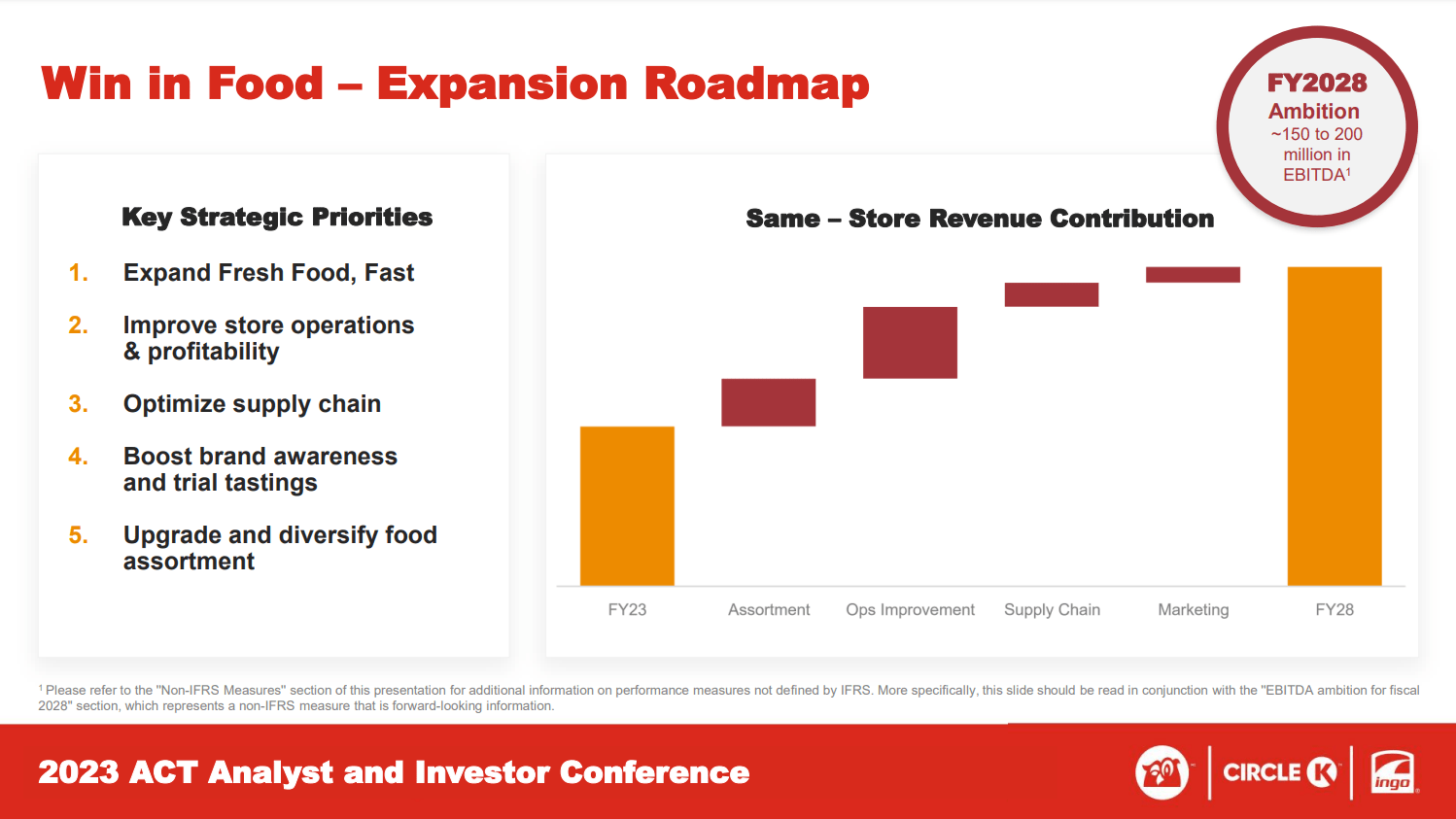

The first part of the strategy is Winning Offer aims to generate $0.5-$0.6 billion in EBITDA , consisting of food ($150-$200m), drinks ($250m) and private brands ($120m). Fresh food and drinks are a vital part of the thesis and, in my opinion, a large opportunity. According to the company, 59% of fast-food customers consider purchasing a meal from a C-store. By growing this business, ATD can benefit from scale economics through its supply chain and marketing and operational improvements (one of the key parts of the ATD culture of continuous improvement). Private labels have long been a winning strategy for ATD, making them less dependent on large players like Coca-Cola ( KO ) and PepsiCo ( PEP ), driving higher gross margins. ATD expects to grow gross profit on Food and Private Labels by mid to high teens CAGR over the next five years, while drink is expected to grow 6%. I think it is vital to focus on the offerings within the C-stores. There is uncertainty regarding the disruption of the fuel business with EVs. By getting customers to come into the store outside of fuel visits, ATD can secure its revenue against this disruption potential. Furthermore, it will expand gross margin, especially as private labels increase in the sales mix.

ATD Win in Food (ATD Investor Day)

{kind=link}

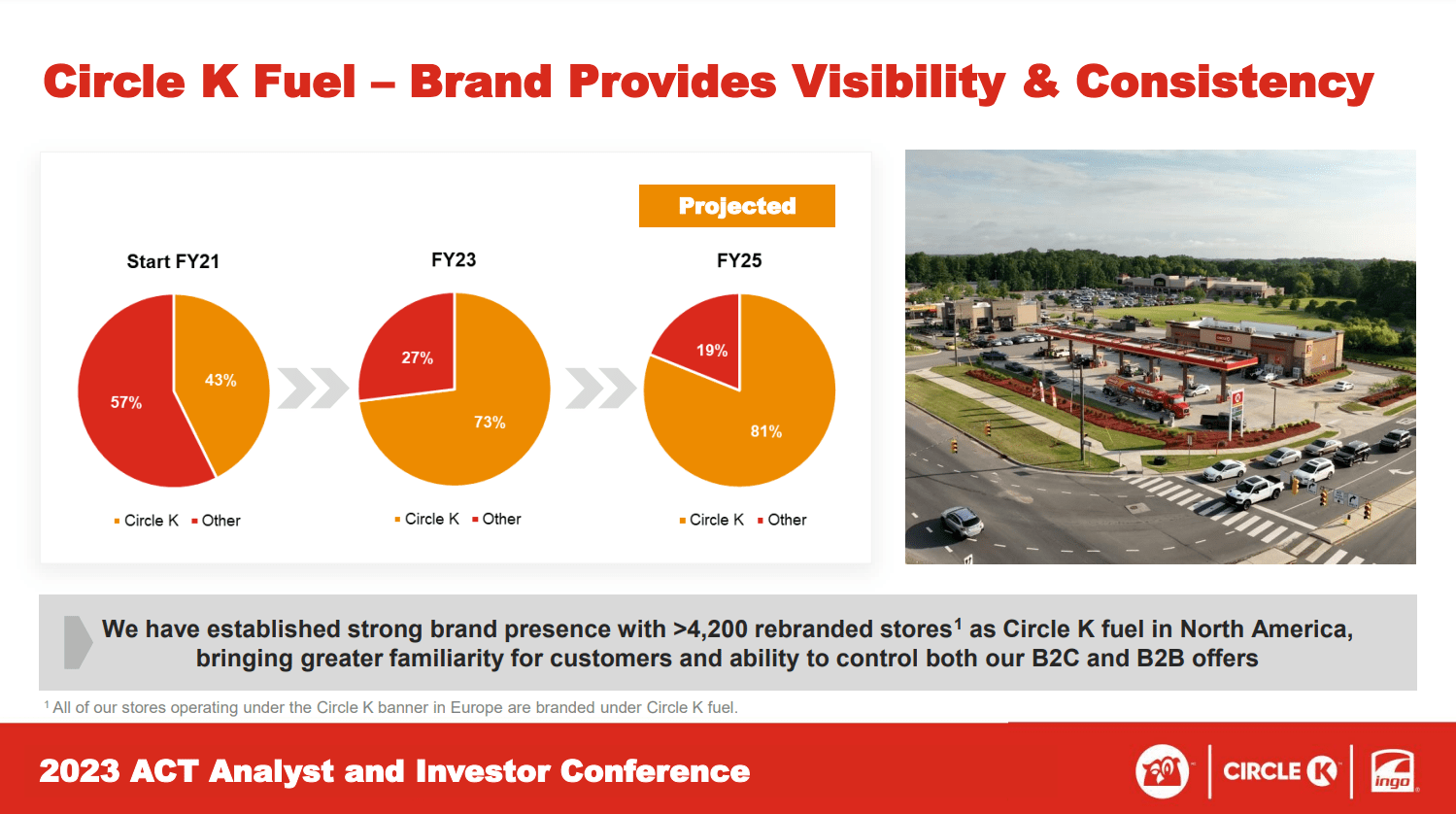

Winning Fuel

My main takeaway from Fuel is that ATD wants to grow its brand recognition to improve customer relationships and realize scale economics. While EV adoption continues, demand for Fuel should remain stable, and the players within it should become more consolidated. Optimizing the supply chain is also a key factor, as well as sourcing. Overall, ATD expects to drive an additional $0.4-$0.6 billion in EBITDA from its Fuel operations. Buying power and network can benefit ATD here as well. Through better purchasing and transport margins can be improved.

ATD Winning fuel (ATD Investor Day)

{kind=link}

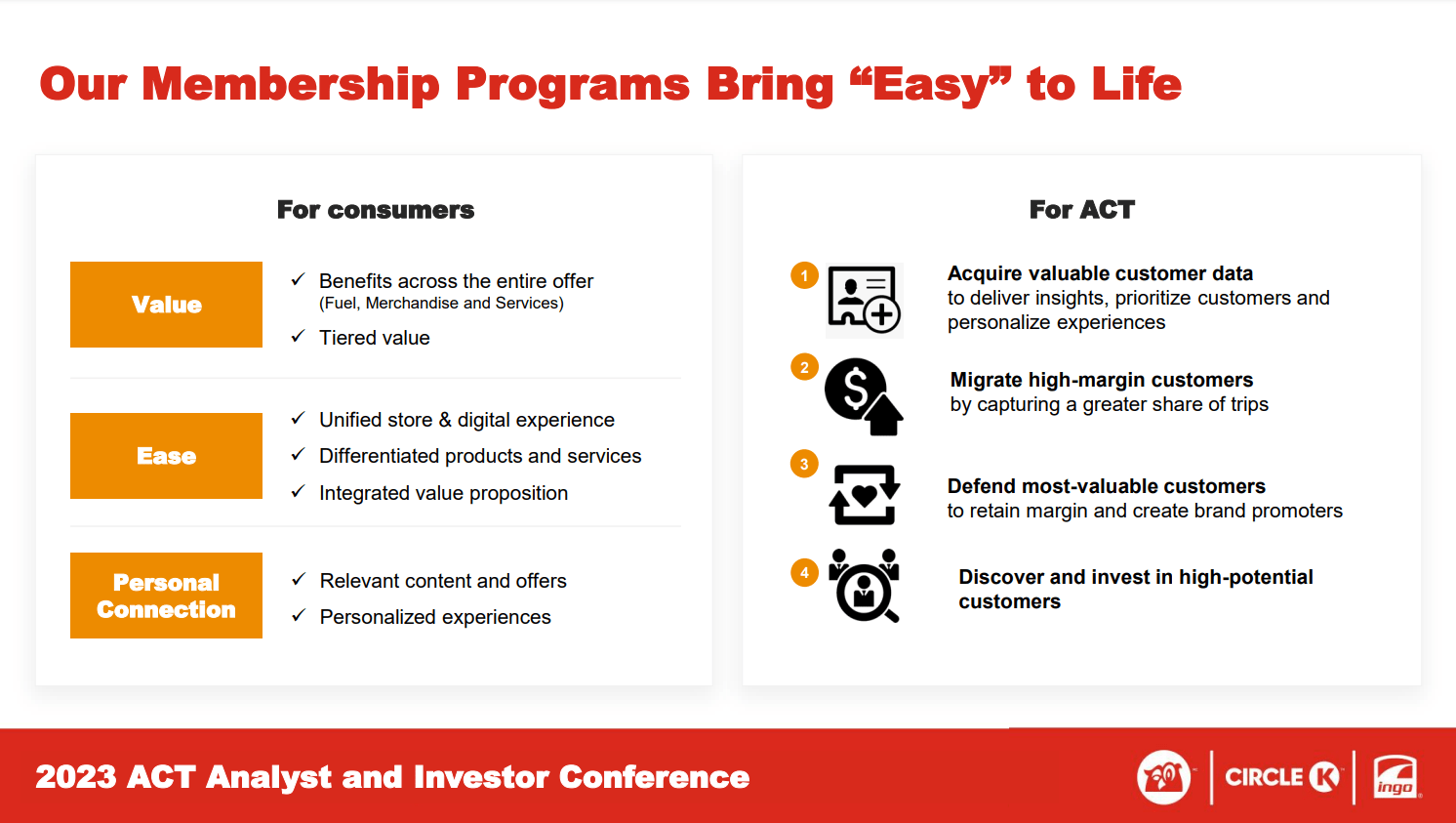

Winning the Customer

C-stores typically have a small percentage of their customers as high-value customers. Through its loyalty programs, ATD aims to grow and defend (against competitors) these high-value customers as well as identify customers with high potential and invest in converting them. Right now, only 20% of transactions are from members, leaving a lot of room for improvement. Another factor is customer data, which ATD leverages in its LIFT system, a screen that displays attachment offers to the customers at checkout and enables a frictionless way to upsell better than employees can do. So far, ATD has seen a 15% conversion rate on 600 million offers in the past 12 months. These are great examples of my thesis for ATD: Investing into technology to gain an edge over competition. Especially LIFT has huge potential to lift the lifetime value of a customer.

Another interesting cost-saving program is Easy Office: ATD invests in administration automation and has reduced admin hours from 73 at the start of FY 22 to 47 today and aims to improve to 38 hours by FY 25. Inventory management is another area where ATD will optimize the business by leveraging technology to optimize inventory levels and what inventory they have to avoid out-of-stock situations. These initiatives are expected to generate incremental EBITDA of $0.2-$0.4 billion.

ATD Membership program (ATD Investor Day)

{kind=link}

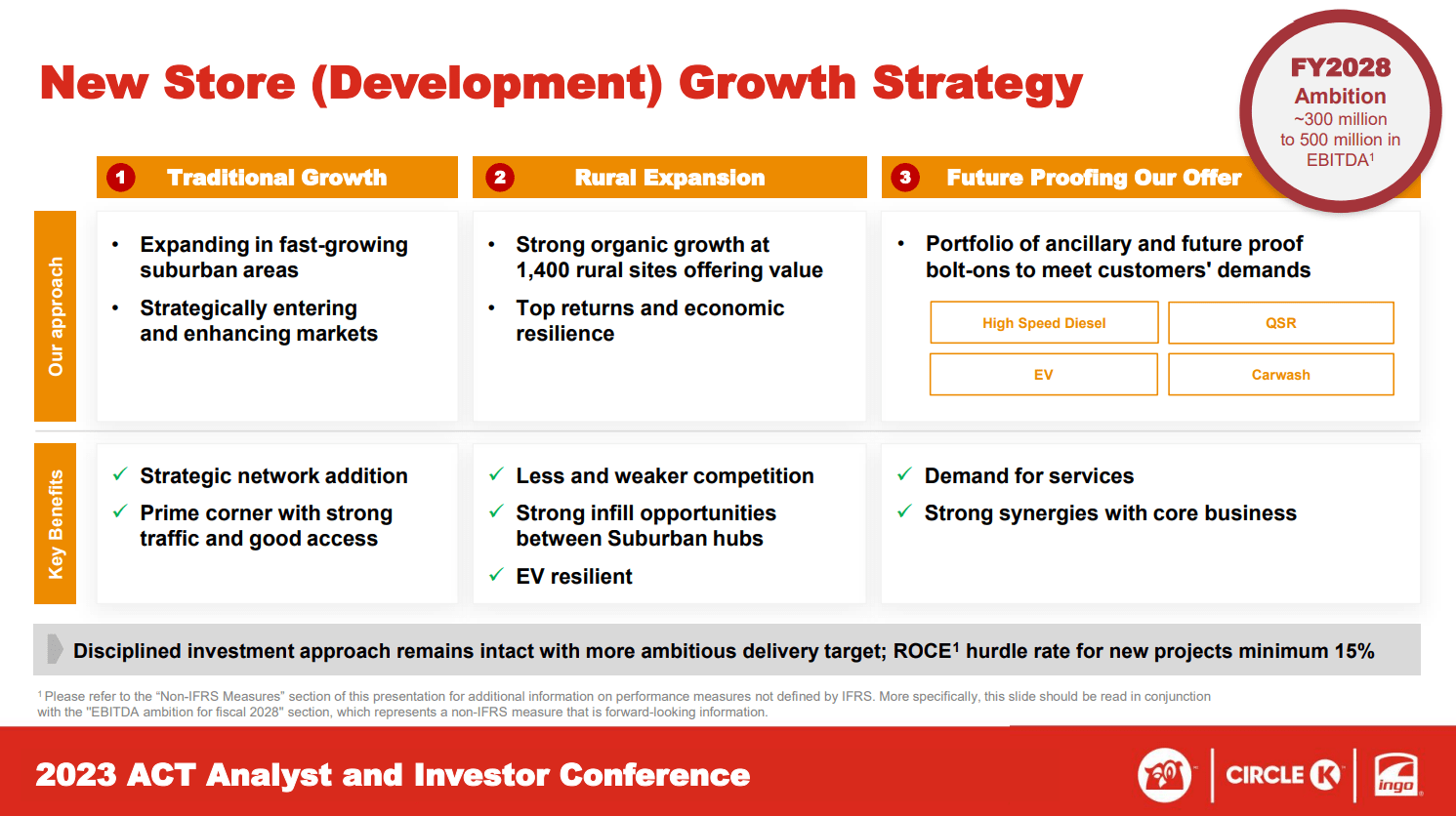

Winning Growth

Growth is by far the most important pillar, estimated at $2.1-$2.3 billion in incremental EBITDA. Organic growth through new stores is projected to contribute $300-$500 million with a focus on future-proofing the locations (impact/chances of EV development as well as scale synergies and overall demand) and a 15% ROCE hurdle rate with a pipeline of around 1,000 projects. Depending on the location, ATD is looking to add additional services like EV charging, Car washes or quick service restaurants to its sites.

Once again, ATD is diversifying its revenue streams. Car washes and quick service restaurants will drive customers to the location no matter if they drive an EV or an ICE vehicle. Car washes, in particular, can drive subscription revenues and increase customer loyalty further.

ATD switched its strategy a bit. In the last years management announced a shift to higher contributions from organic growth, because it was harder to get good M&A deals in an exuberant market. After the Total Energy deal and this investor day we see a shifted picture, where M&A again is expected to contribute the majority of growth. I like this development, M&A was always a backbone of ATDs growth strategy and they know how to do it properly.

New Store development (ATD Investor Day)

{kind=link}

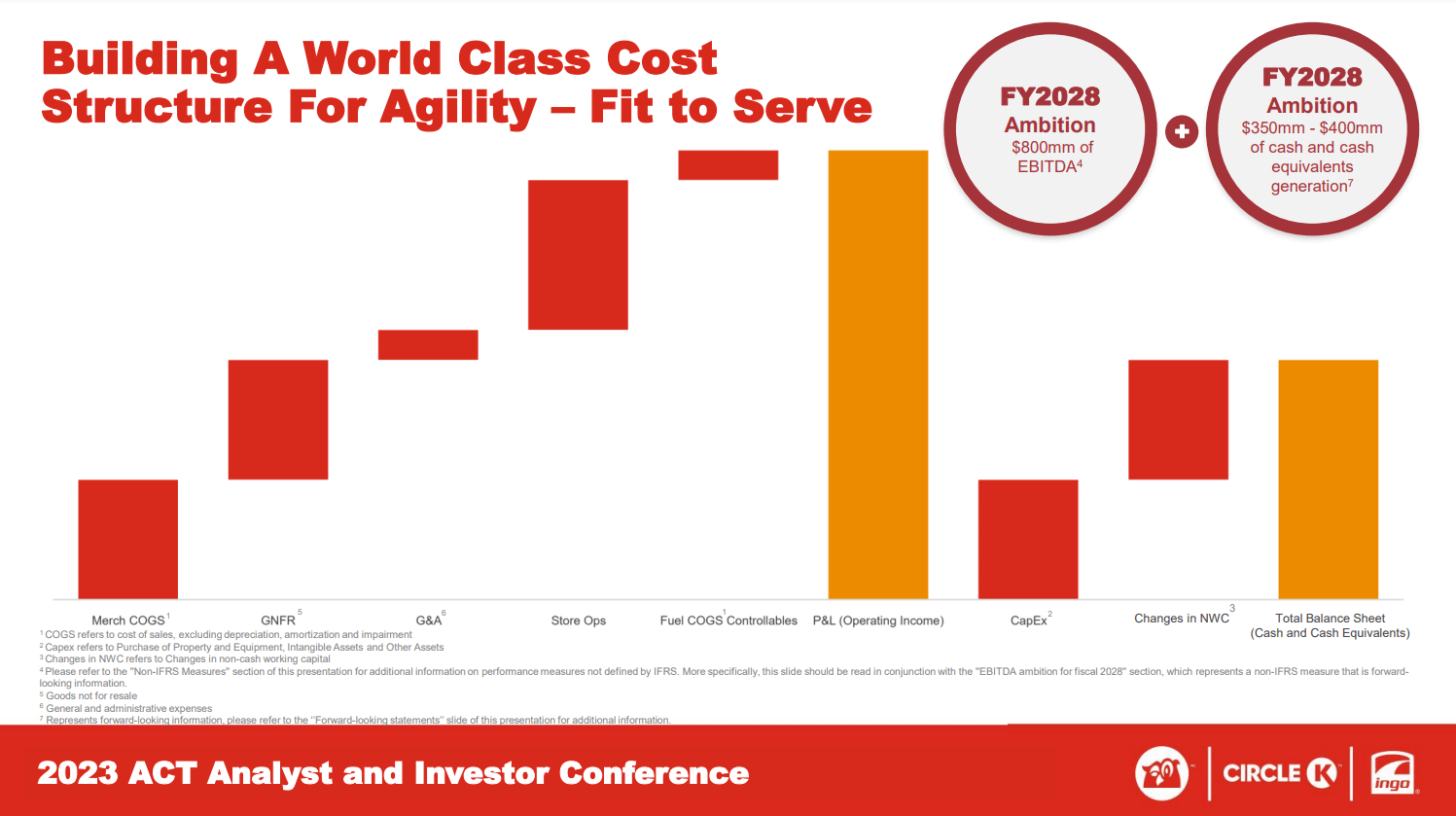

The Foundation

Besides the pillars, ATD also sees a lot of incremental EBITDA in its core operations by improving COGS ($200m) and goods not for resale ($200m, this means reducing costs for services and investments like payments, repairs or marketing costs), G&A ($50m), c-store operations ($250m) and fuel costs ($50m), resulting in a total of $800 million in EBITDA, alongside $350-$400 million in freed up cash from improvements in NWC. Especially freed-up cash will come in handy as the company aims to be more active in M&A again.

ATD's Foundation (ATD Investor Day)

{kind=link}

M&A represents the biggest lever ATD has and it expects $700 million from the closed TotalEnergies deal and another $1.1 billion from new opportunities. The company has around $10 billion in capacity for all-cash acquisitions, significantly more than it paid for the TotalEnergies acquisition at 3.1 billion Euros. The company isn't highly levered right now, so there is no need to delever and we could see another deal shortly if opportunities present themselves; ATD is a very disciplined buyer and happy to wait to swing.

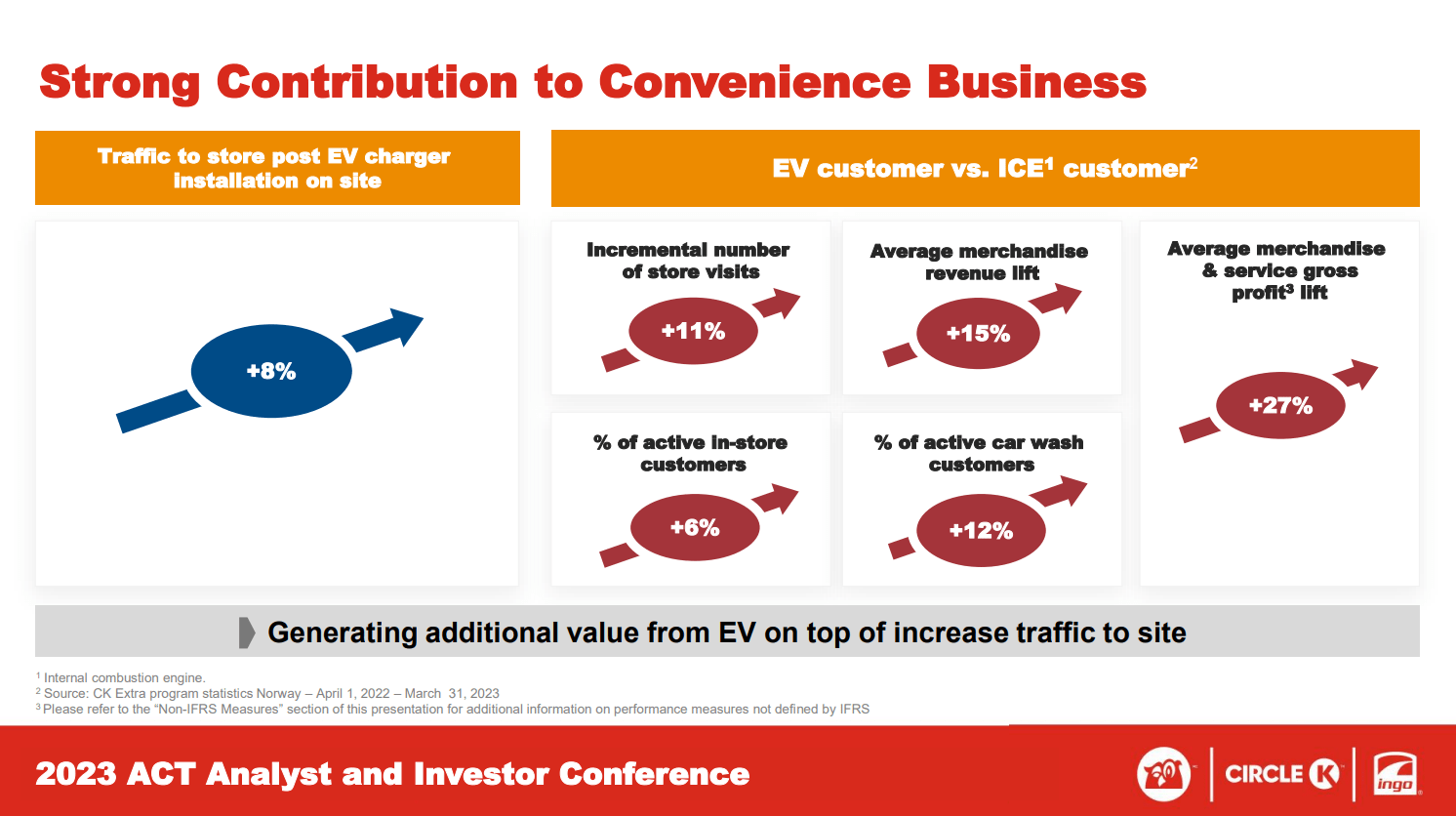

The EV-Risk

My highlight from the Investor Day was the following slide: We can see that EV customers so far show to be beneficial to the business in all aspects, from traffic to store, to number of store visits, use of car wash services and overall spending. So far High Power Charging has generated a 30-40% EBT margin and between 18-30% ROCE, both above the consolidated business. We need to keep in mind that this is still a small sample size and it is not clear if this will apply to all locations, but it helps against the omnipresent bear argument of EV adoption and the negative effects for ATD's business.

EV contribution to the business (ATD Investor Day)

{kind=link}

Q2 Earnings

I will keep earnings short, as I believe the Investor Day to be much more important for shareholders. ATD beat expectations slightly by 4% on EPS and <1% on sales. Merchandise and service revenues grew somewhat (1%), offset by fuel revenues declining 3%. Merchandise gross margins improved by 2.8% in the quarter. The highlight of the quarter was the dividend increase by 25% to CAD 0.175, continuing ATD's history of growing its dividend above 20% annually.

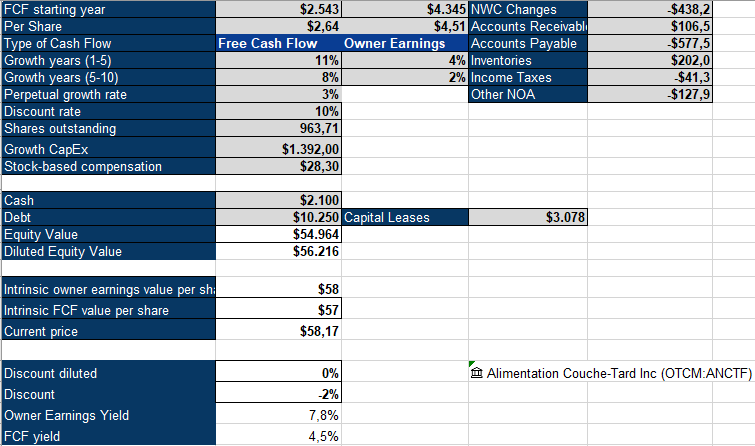

A Compelling Buy

Using an Inverse DCF Model for ATD, we get to a required growth rate of 4% on Owner Earnings or 11% on Free Cash flow over the next five years. The large difference is due to the large portion of growth CapEx I added back and the adjustments for changes in NWC. ATD invests around 75% of its CapEx into growth, while just 25% is required to maintain the business. The global convenience store industry is expected to grow at 6% annually and is highly fragmented. With an improving deal environment, ATD should be a beneficiary and able to increase its network and capture scale economics. The Total Energy deal is accretive and allows a better expansion into Europe. Together with margin improvements from upselling and gaining new customers, as well as cost reductions from technological investments, I believe that the required 11% FCF growth rate is not far-fetched. ATD has a history of growing EBITDA by 11%, in line with the required growth. The balance sheet looks clean with a capacity of $10 billion for new deals.

ATD Inverse DCF Model (Authors Model)

{kind=link}

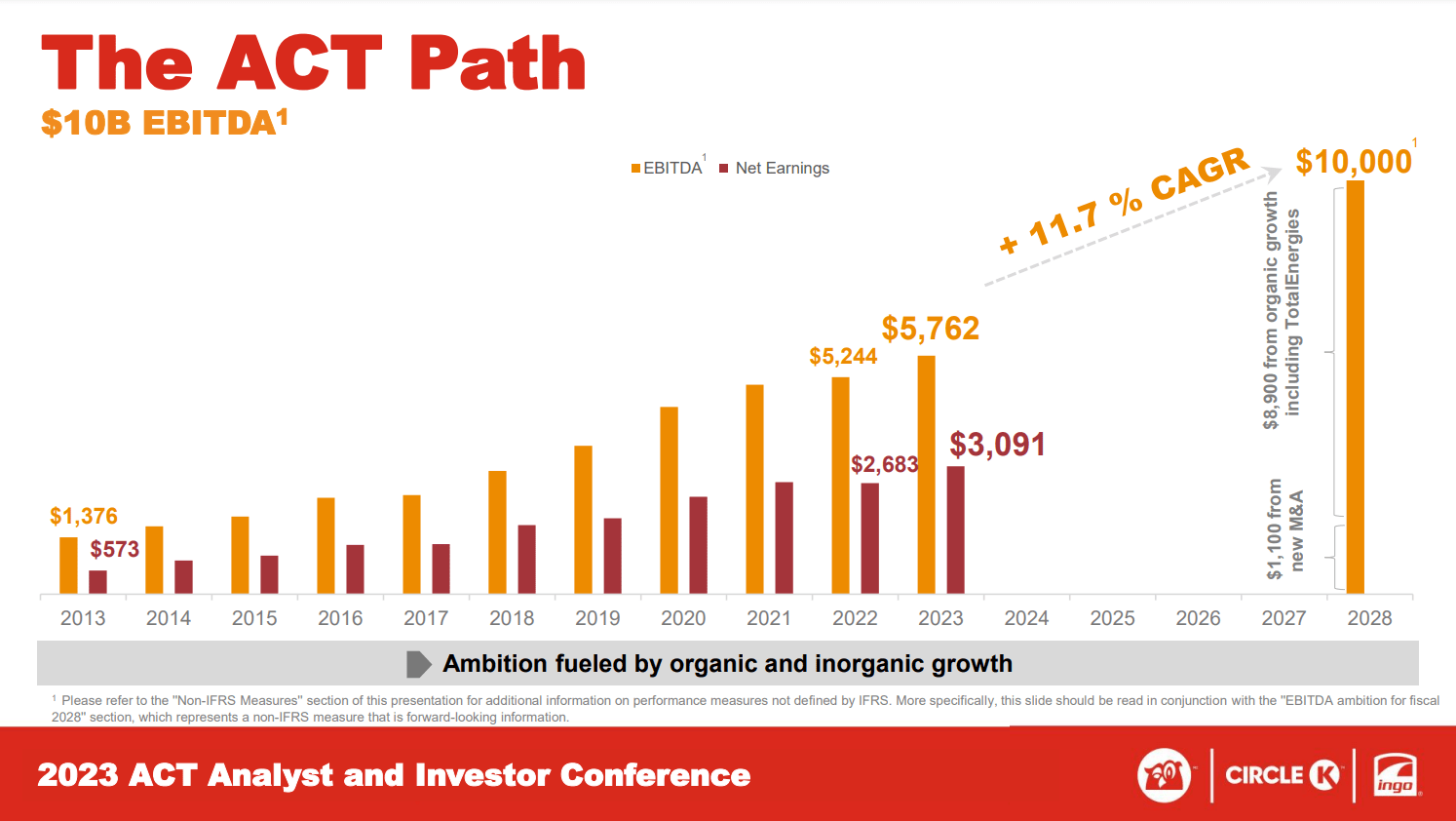

To summarize the Investor Day, ATD expects to grow EBITDA by 11.7% CAGR over the next five years, representing almost double the current $5.7 billion. We can expect that cash flows will align with this development (assuming they manage to hit their target, as they usually do), which makes me confident that the business will continue to outperform the general market. ATD has shown that it can expand while increasing its returns on capital employed. With this continued value creation paired with a market multiple valuations, the stock looks appealing. ATD is in a great position to consolidate and organically grow in its market while improving its business and margins and repurchasing shares. I continue to hold ATD in my portfolio as a core position and would be looking to add on weakness or if there aren't better opportunities within my portfolio.

The ACT Path to $10b EBITDA (ATD Investor Day)

{kind=link}

For further details see:

Alimentation Couche-Tard Investor Day Suggests More Profitable Growth Ahead