ANCTF - Alimentation Couche-Tard: The Transition To Charging Stations Is Possible

2023-09-28 15:00:11 ET

Summary

- Alimentation Couche-Tard is a Canadian multinational convenience store and gas station operator. As you can imagine, at first glance, it appears this business has no place in a world where electric vehicles dominate the streets.

- The company is heavily rolling out charging stations in Scandinavia and plans to replicate this in North America. Thanks to its existing gas station locations, this transition should be easy.

- The turnaround seems feasible, but the valuation is not attractive. That's why I decided to give it a hold rating.

Investment Thesis

The transition towards electric vehicles is becoming increasingly evident. Governments and society are making concerted efforts to facilitate this shift, which raises questions about the future of businesses currently dedicated to supplying the fuel required by internal combustion vehicles.

However, companies like Alimentation Couche-Tard ( ATD:CA ) ( ANCTF ) are taking steps to transform their business models and continue to serve as energy providers, but now in the form of electricity. These businesses already have strategic locations, making the transition relatively smooth. Moreover, they possess certain advantages that could benefit the company in a world dominated by electric vehicles.

Business Overview

Alimentation Couche-Tard is a Canadian multinational convenience store and gas station operator. The company is one of the largest operators of convenience stores and gas stations in the world. It's known for its various retail brands, including Circle K, which is widely recognized in North America and other parts of the world.

Alimentation Couche-Tard was founded in 1980 in Quebec, Canada, and has since expanded its presence through acquisitions and partnerships. The company's operations extend beyond Canada and the United States, with a significant presence in Europe and other parts of the world.

Transition to Electric Vehicles

As it is already well-known, society is transitioning towards electric vehicles ('EVs') and more environmentally friendly energy alternatives, such as renewable energy.

While this poses a significant challenge for Alimentation Couche-Tard gas stations, it is also true that the transition to EVs will be rather slow. Estimates suggest that by 2030, 50% of annual sales will still be internal combustion vehicles. Therefore, the point at which EVs will constitute 100% of annual sales is still distant, and even further away is the point at which 100% of cars on the streets are electric. This demonstrates that ATD will continue to be a necessity for the millions of internal combustion cars that will remain on the road in the next decade.

{kind=link}

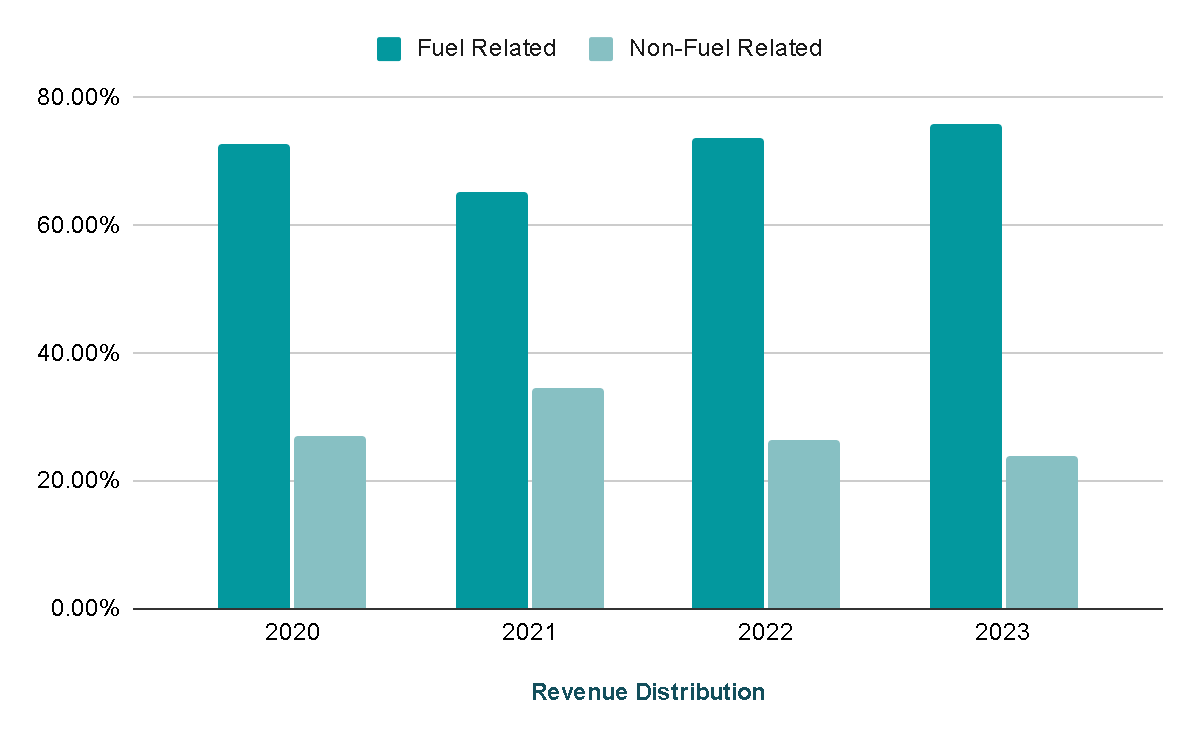

Another highly relevant aspect is that the company derives approximately 25% of its sales from convenience stores located at gas stations, such as Circle K. These revenues have consistently remained at around 25% for several years, which is of great importance because they have demonstrated clear resilience to crises and are expected to be less affected by the transition to EVs. For instance, in 2020 (FY2021), when the COVID-19 crisis led to a 25% decrease in fuel revenues, non-fuel-related revenues grew by 8%.

{kind=link}

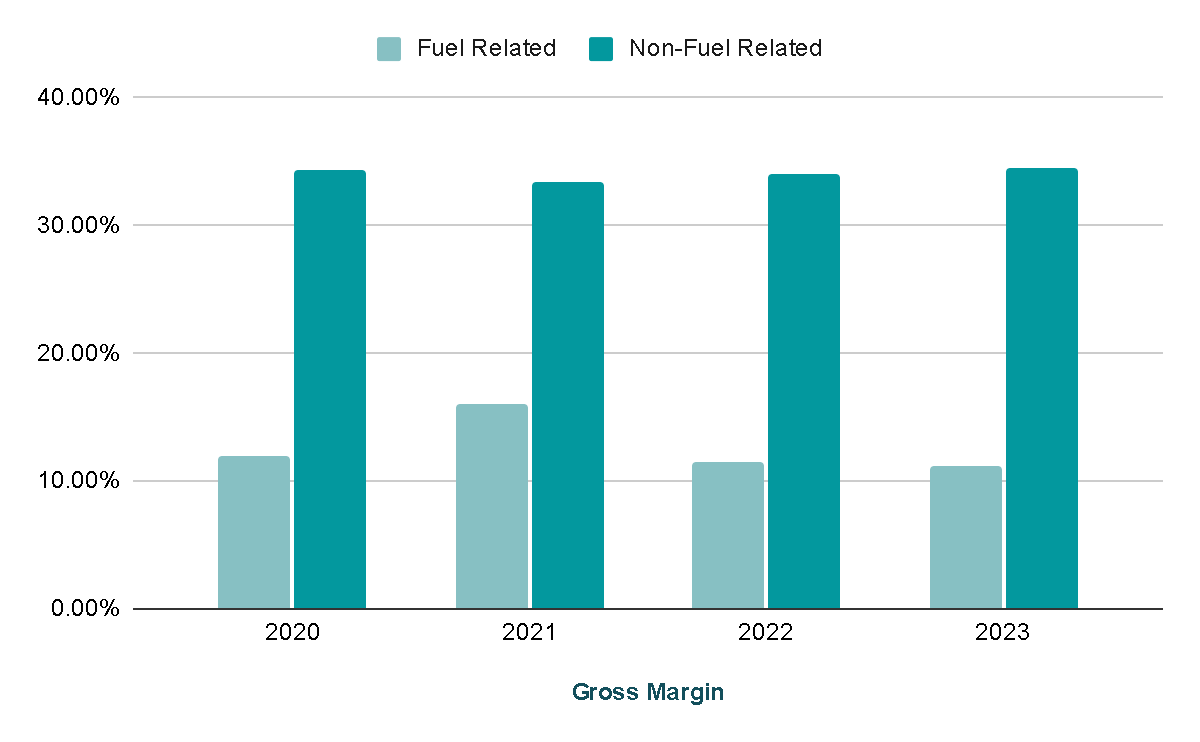

And, what's even more crucial, the gross margins for these products are twice as high as those for fuel-related products. For FY2023, the margins for this revenue segment stood at 35%, and they have consistently maintained this level in recent years, whereas fuel-related revenues have had gross margins of only 11% or 12%.

{kind=link}

Charging Stations Implementation

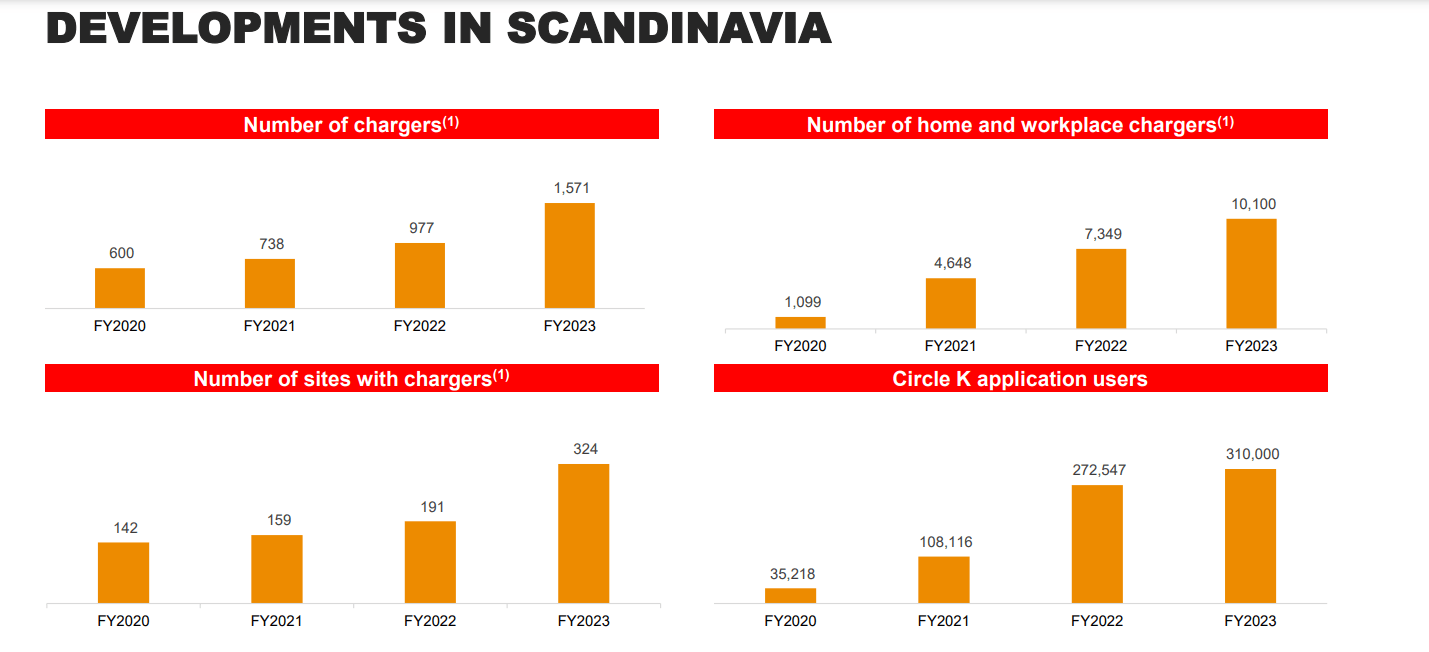

It's not just the coexistence of electric and internal combustion vehicles for several more years that's important; ATD will also need to transition its business model to increase its terminal value. This transformation has already begun in the Scandinavian region, where EV adoption is much more advanced than in other parts of the world.

By the end of FY2023, the company had already established 324 locations with available chargers, and there are plans to further expand its presence in Europe. Additionally, it began entering North America in 2022 with a station in Quebec and another in South Carolina, and it also hopes to expand more aggressively in 2024.

Charging Stations in Scandinavia (Alimentation Couche-Tard)

{kind=link}

A positive aspect of this is that currently, charging an electric vehicle from empty to full takes between 20 minutes to an hour , while filling a gasoline car typically takes no more than 10 minutes. This waiting time could potentially lead to increased sales within the stores as customers pass the time while their electric vehicle is charging. So, not only is the transition to chargers feasible, but it could also benefit the resilient and higher-margin segment of the business.

Valuation

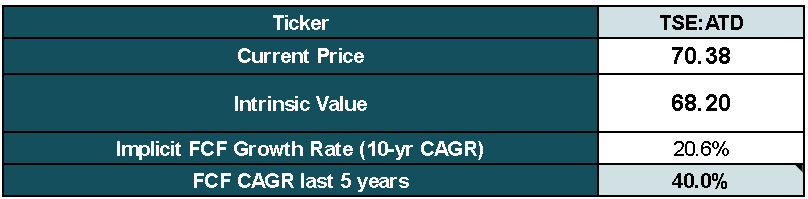

For the valuation, I will use the FY2023 numbers and perform a Reverse DCF analysis to determine the implicit growth rate of Free Cash Flow in the shares. This will indicate what level of FCF growth is required to achieve the desired return from the current share price.

Here are the data points I will use:

- Free Cash Flow: $2,540 million

- Shares Outstanding: 1,009 million

- Cash: $834 million

- Debt: $9,559 million

- Expected Return: 12%

- Terminal Growth Rate: 3%

- Share Reduction: 3% as observed in recent years

With these data, it would be necessary for Free Cash Flow to grow by approximately 20% annually for the next 10 years to justify a 12% Compound Annual Growth Rate from the current share price. However, this level of growth seems unrealistic to me, even considering the company's historical performance, which often includes acquisitions.

My more conservative assumptions would project a growth in Free Cash Flow of around 10-12% annually. This would imply an expected return on investment of approximately 8% annually over the next 10 years based on the current share price.

Reverse DCF Results (Author's Representation) Reverse DCF Model (Author's Representation)

{kind=link}

{kind=link}

Final Thoughts

Couche-Tard is one of the best alternatives to be exposed to the new charging station networks since the company has been investing in this for some time and convenience stores also have a great weight in sales compared to some peers such as Parkland Corporation. In the end, quality costs and that is why the current valuation does not offer an interesting upside from my point of view, which is why I will give it a 'hold' rating.

The company is not exempt from risks that could impact its operations and financial performance. These risks include intense competition in the retail sector, where it is really difficult to differentiate from other convenience stores or gas stations. Typically, the consumer tends to go to the nearest gas station without caring about the brand, which is why a war for the best locations occurs and subsequently a war over prices when there are already two gas stations in nearby locations. Also, its high exposure to fuel price volatility can affect profit margins when commodity prices decline, therefore, it is a company exposed to the economic cycle and that is why I would like to see a better margin of safety in the valuation.

For further details see:

Alimentation Couche-Tard: The Transition To Charging Stations Is Possible