VRAI - All Eyes On CPI

Summary

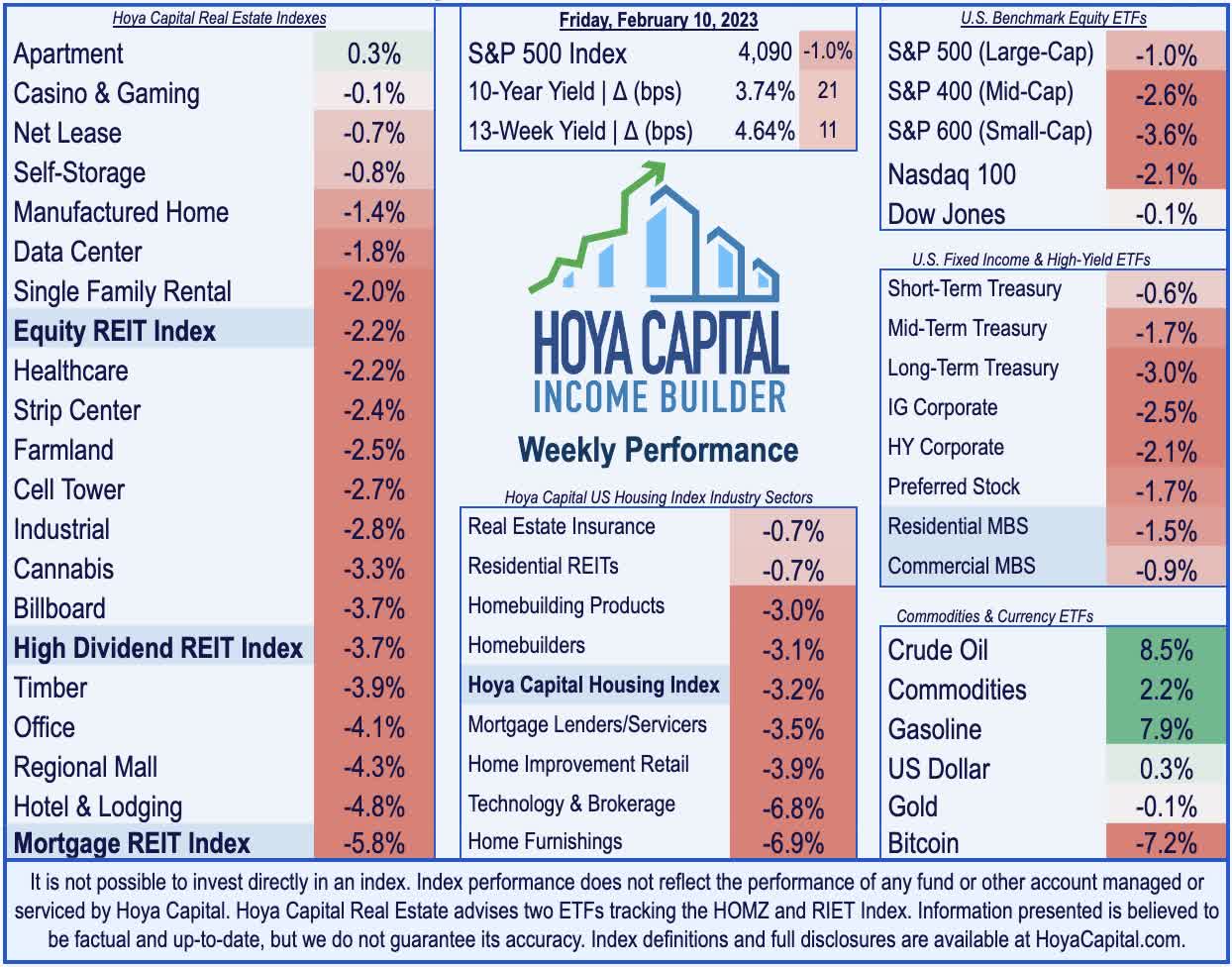

- U.S. equity markets declined while benchmark interest rates jumped this week as hawkish commentary from Fed officials, heightened geopolitical tensions, and mixed corporate earnings results weighed on sentiment.

- Posting just its second weekly decline of the year, the S&P 500 slipped 1.0% on the week, while the tech-heavy Nasdaq 100 declined 2.1% - its first down week of 2023.

- Real estate equities were also under pressure this week as the jump in benchmark interest rates offset a generally solid slate of earnings results. The Equity REIT Index declined 2.2%.

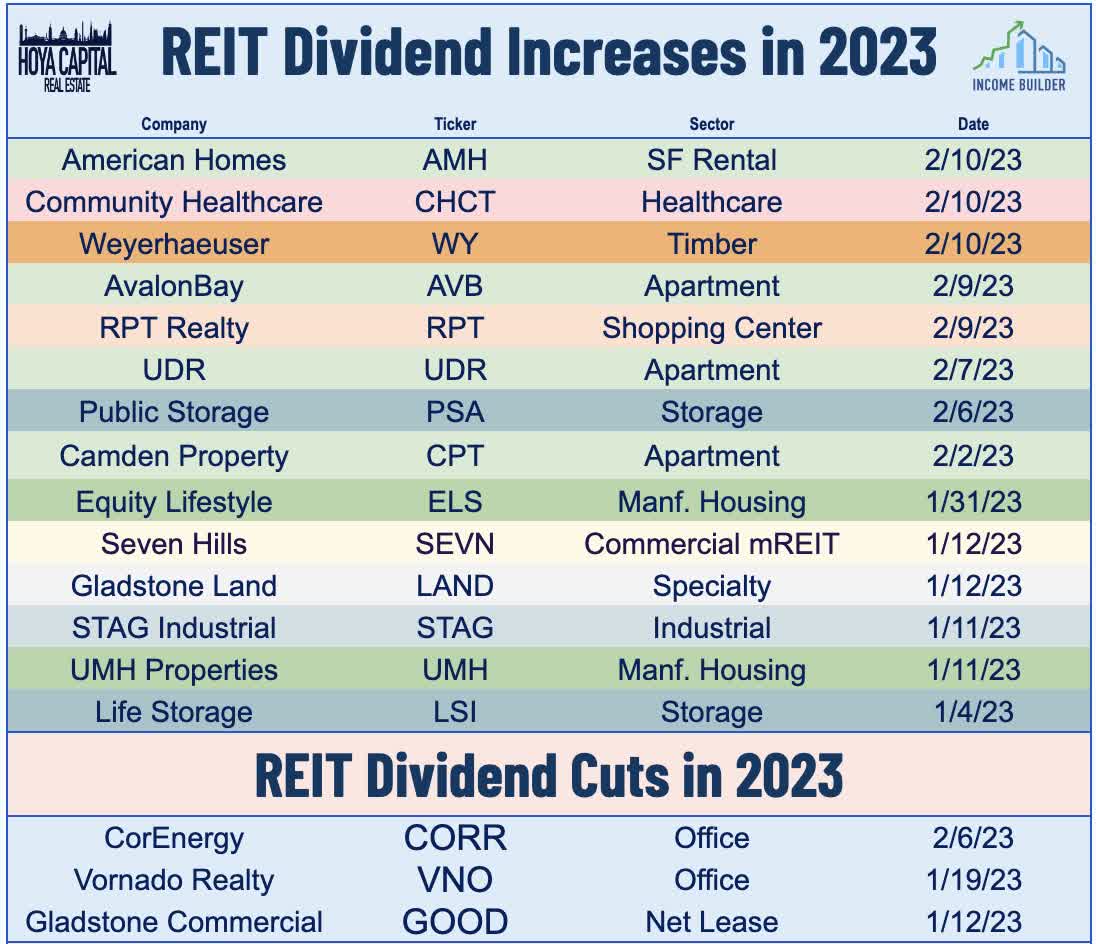

- Major M&A news preceded the busy week of REIT earnings results. Life Storage surged 11% following a takeover bid from Public Storage. REIT dividend hikes have been a major theme thus far in earnings season with another 8 REITs hiking their payouts this week.

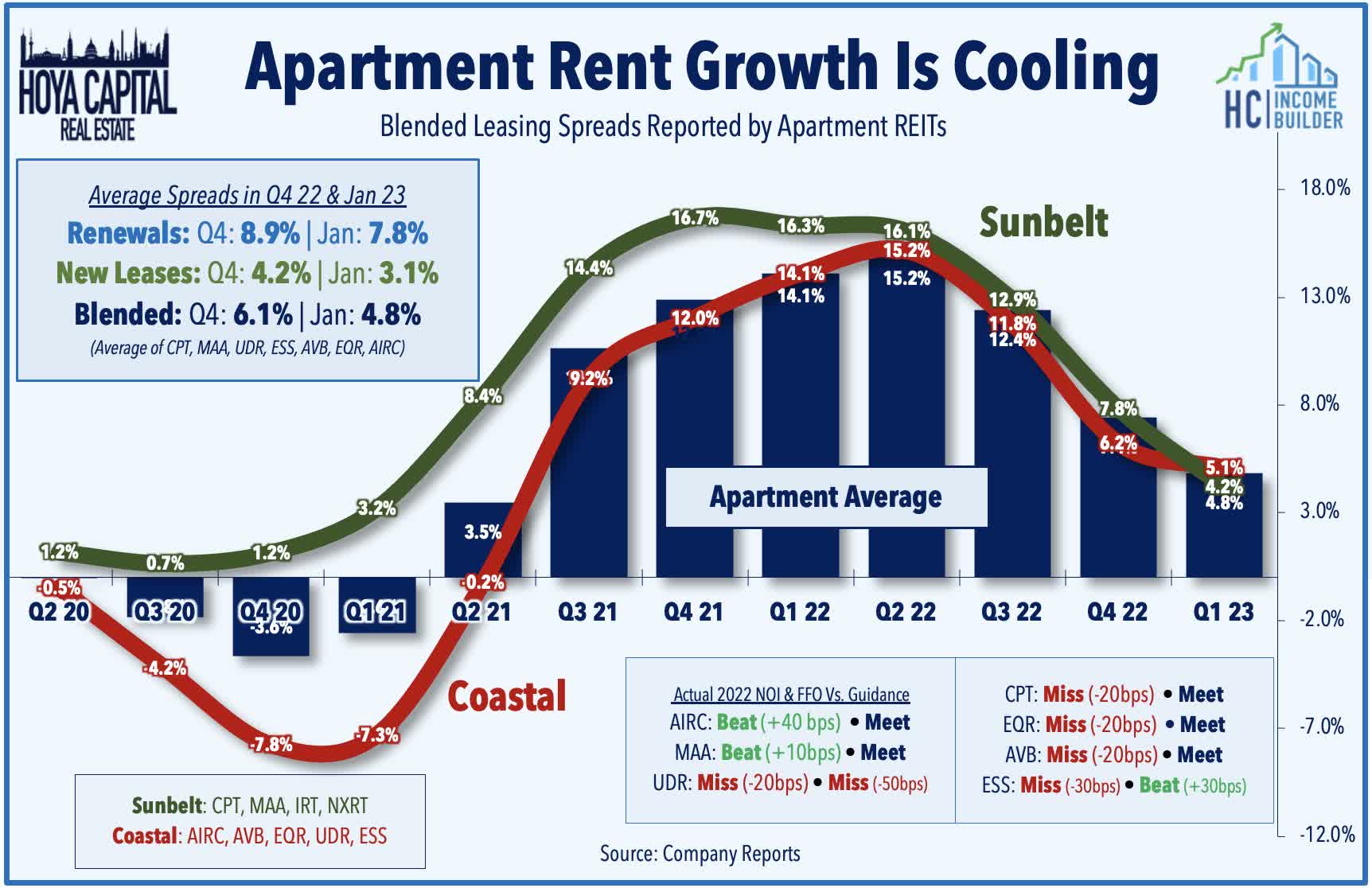

- Apartment REITs were the upside standouts this week with results showing surprisingly resilient rent growth in Q4 and into January. Industrial and Strip Center REITs also reported strong results while Office and Mall REITs forecast FFO declines for 2023.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on February 10th.

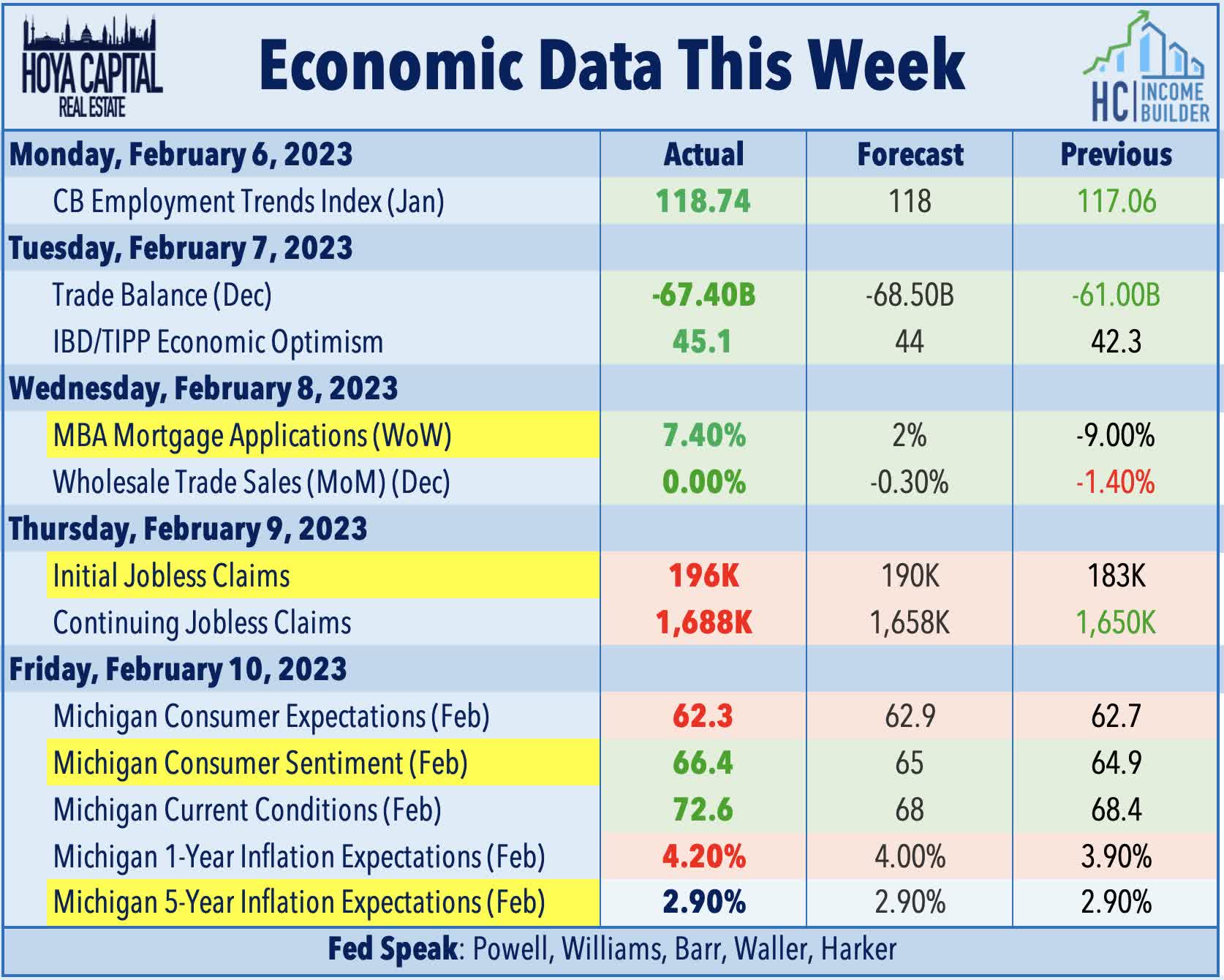

U.S. equity markets declined while benchmark interest rates jumped this week as hawkish commentary from Fed officials, heightened geopolitical tensions, and mixed corporate earnings results weighed on sentiment. Ahead of the closely-watched CPI inflation report in the week ahead, the relatively slow slate of economic data this past week amplified the focus on commentary from Fed officials, who struck a decidedly hawkish tone in public remarks with the notable exception of Chair Powell, who passed on the opportunity to project a more aggressive tone following the blowout jobs report in the prior week.

{kind=link}

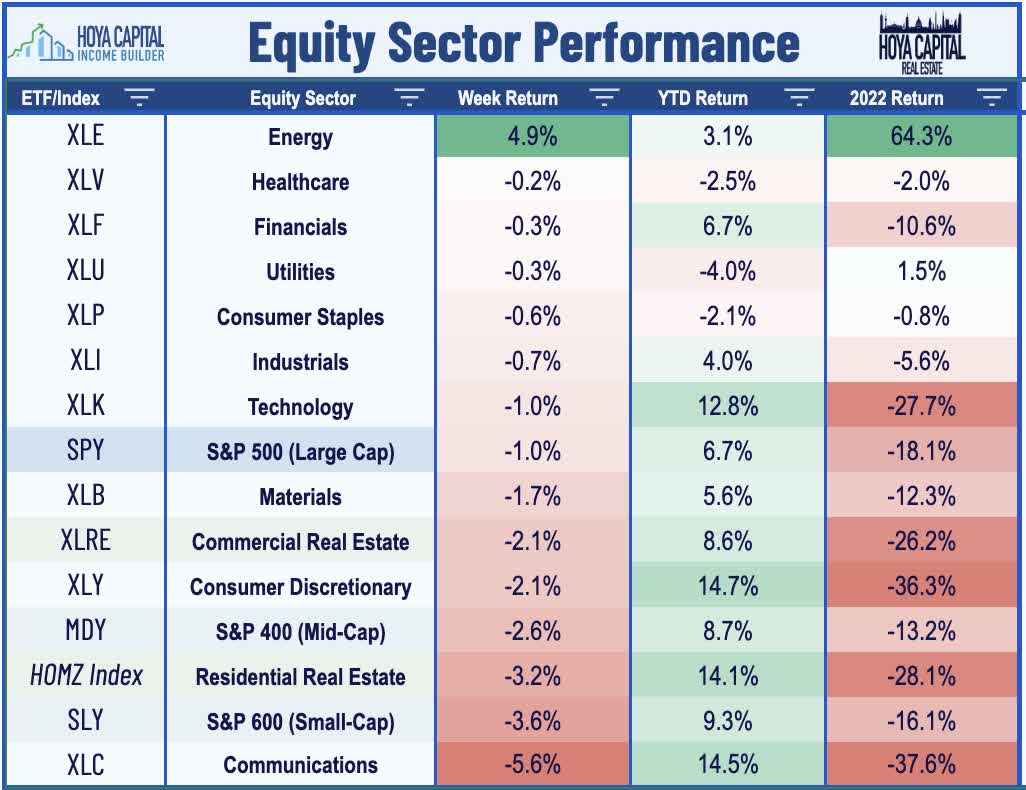

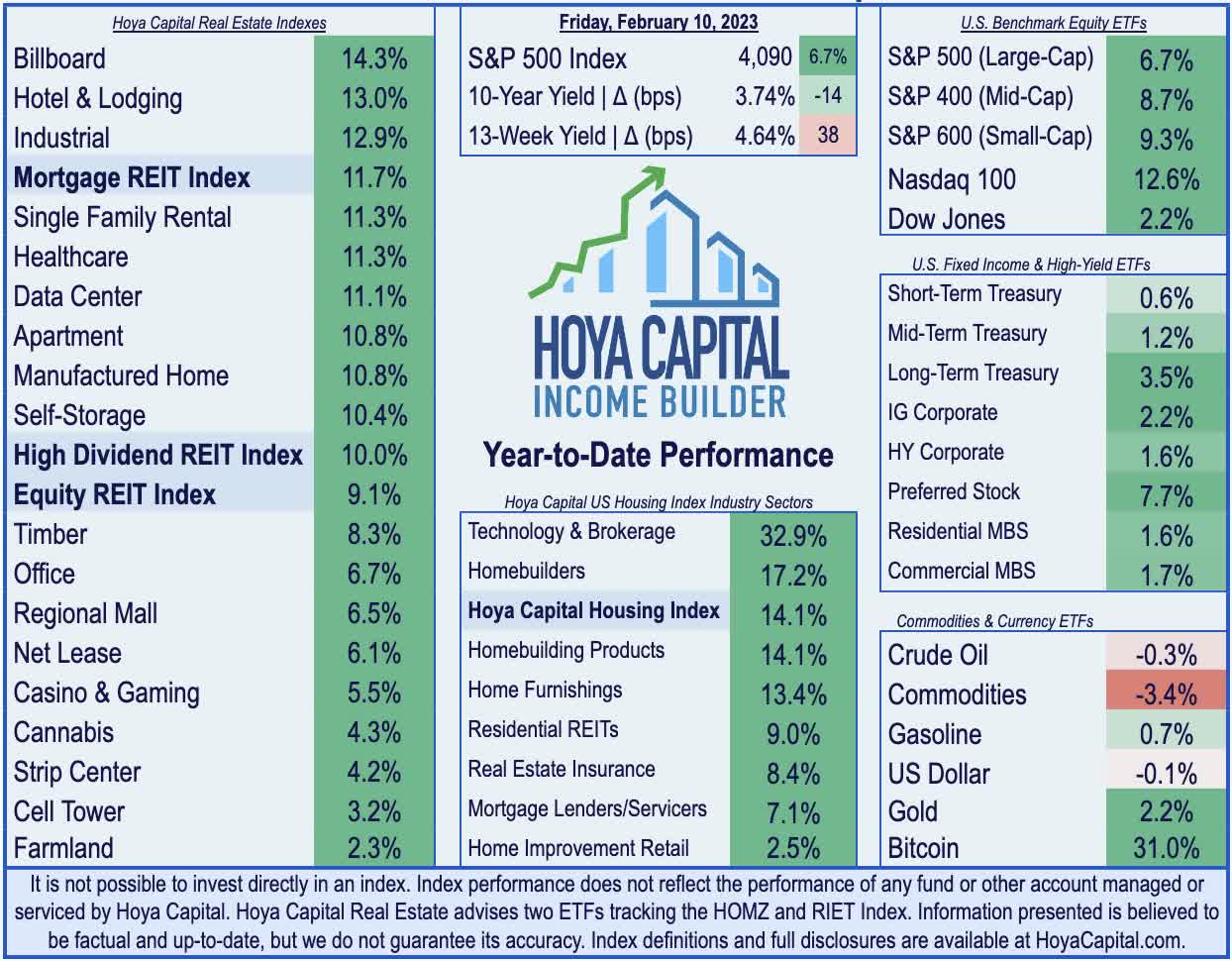

Posting just its second weekly decline of the year, the S&P 500 slipped 1.0% on the week, while the tech-heavy Nasdaq 100 declined 2.1% - its first down week of the year. Consistent with the "risk-off" performance pattern this week, the Mid-Cap 400 and Small-Cap 600 posted steeper declines of 2.6% and 3.6%, respectively. Real estate equities were also under pressure this week as the jump in benchmark interest rates offset a generally solid slate of earnings results. The Equity REIT Index declined 2.2% with 17-of-18 property sectors in negative territory, while the Mortgage REIT Index slid 5.8%.

{kind=link}

Sharp pressure was seen in fixed-income markets across the credit and maturity curve this week as attention turns to a critical slate of inflation data in the week ahead. After dipping to four-month lows around 3.40% before the nonfarm payroll report, the 10-Year Treasury Yield closed at 3.74% - up 21 basis points on the week. With inflation concerns re-emerging, the price action in commodities markets certainly didn't help with Crude Oil prices surging more than 8% after Russia announced plans to reduce oil production next month while Natural Gas prices rebounded after hitting their lowest levels since late 2019 last week. Ten of the eleven GICS equity sectors were lower in the week with particularly sharp declines from Communications ( XLC ) stocks.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

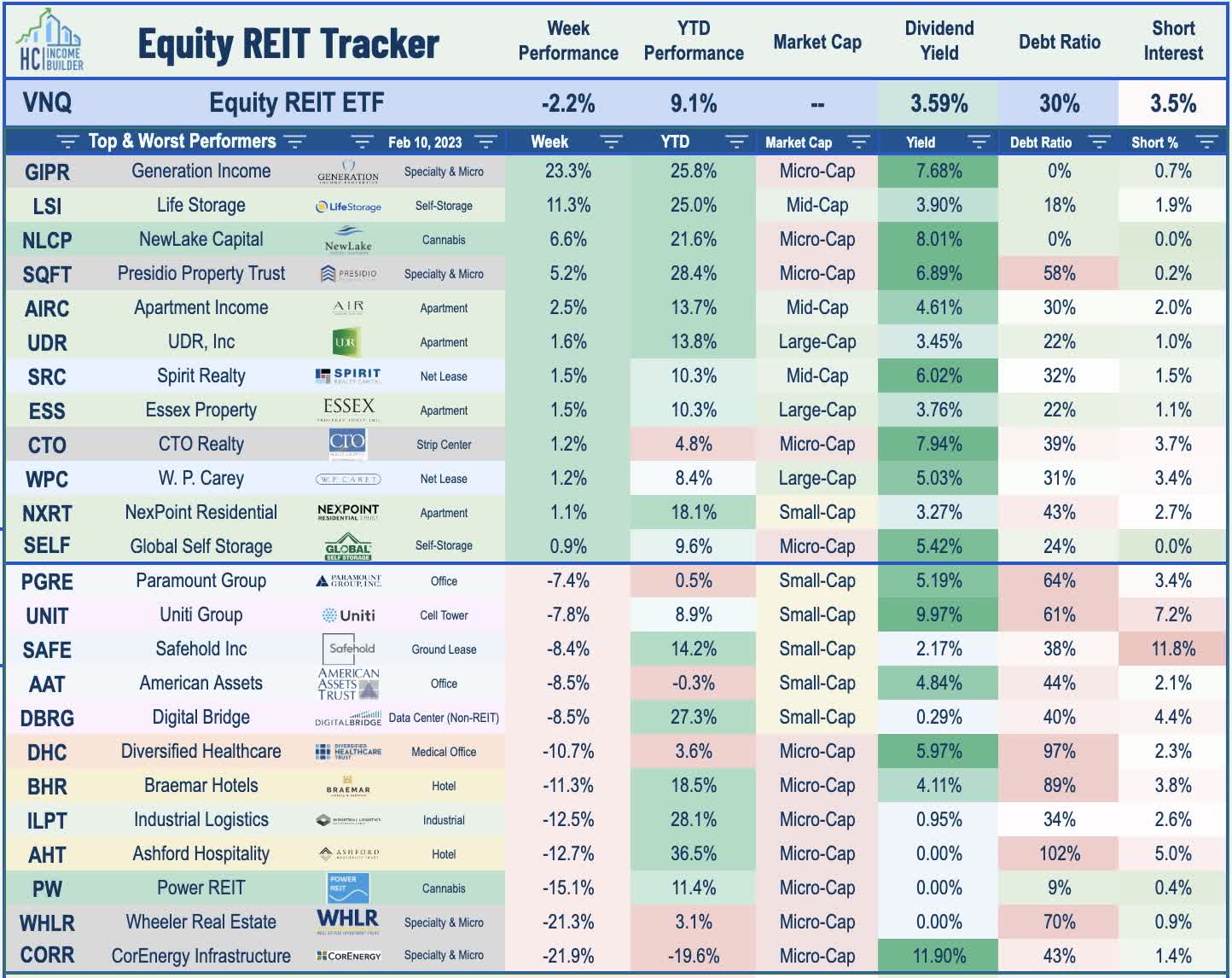

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

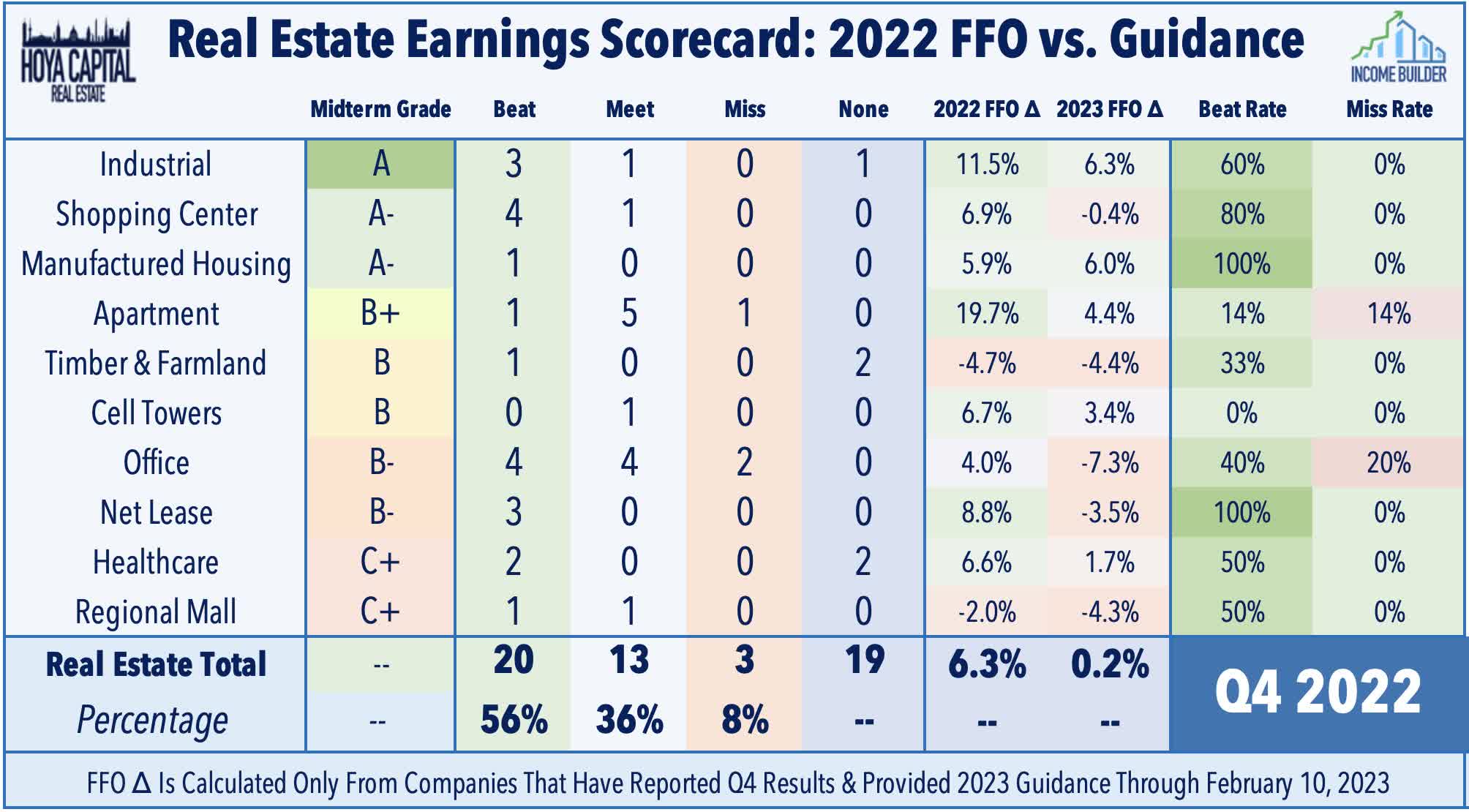

Real estate earnings season kicked into gear this past week with reports from 30 equity REITs and 8 mortgage REITs. We've now heard from roughly 50% of the U.S. real estate sector by market capitalization. This week, we published our REIT Halftime Report which noted that REIT earnings results to this point have modestly exceeded expectations. Of the 36 REITs that provide guidance, 20 (56%) reported 2022 Funds From Operations ("FFO") above their prior guidance while 3 (8%) missed. Industrial and Residential REITs have been upside standouts - forecasting mid-single-digit FFO growth in 2023. Strip center, net lease, and healthcare REIT FFO is expected to be roughly flat in 2023 while office and mall REITs forecast FFO declines for the year.

{kind=link}

Continuing with the major theme of the past two years, REIT dividend hikes have been a focus with eight REITs raising their payouts this past week, highlighted by a 50% dividend hike from Public Storage ( PSA ), a 22% hike from single-family rental REIT American Homes ( AMH ), a 10% hike from apartment REIT UDR ( UDR ), and an 8% increase from strip center REIT R PT Realty ( RPT ). Apartment REIT AvalonBay ( AVB ) also hiked its dividend by 4% - its first hike since 2019. Following two consecutive years of over 120 REIT dividend hikes in 2021 and 2023, we've seen 14 REITs hike their payouts through the first six weeks of 2023 - roughly tracking the pace of the past two years. Three REITs have lowered their payouts this year, however, including a cut this week from micro-cap CorEnergy ( CORR ), which suspended dividends on both its common stock and its preferred stock, citing a combination of declining volumes and increased costs in its California systems.

{kind=link}

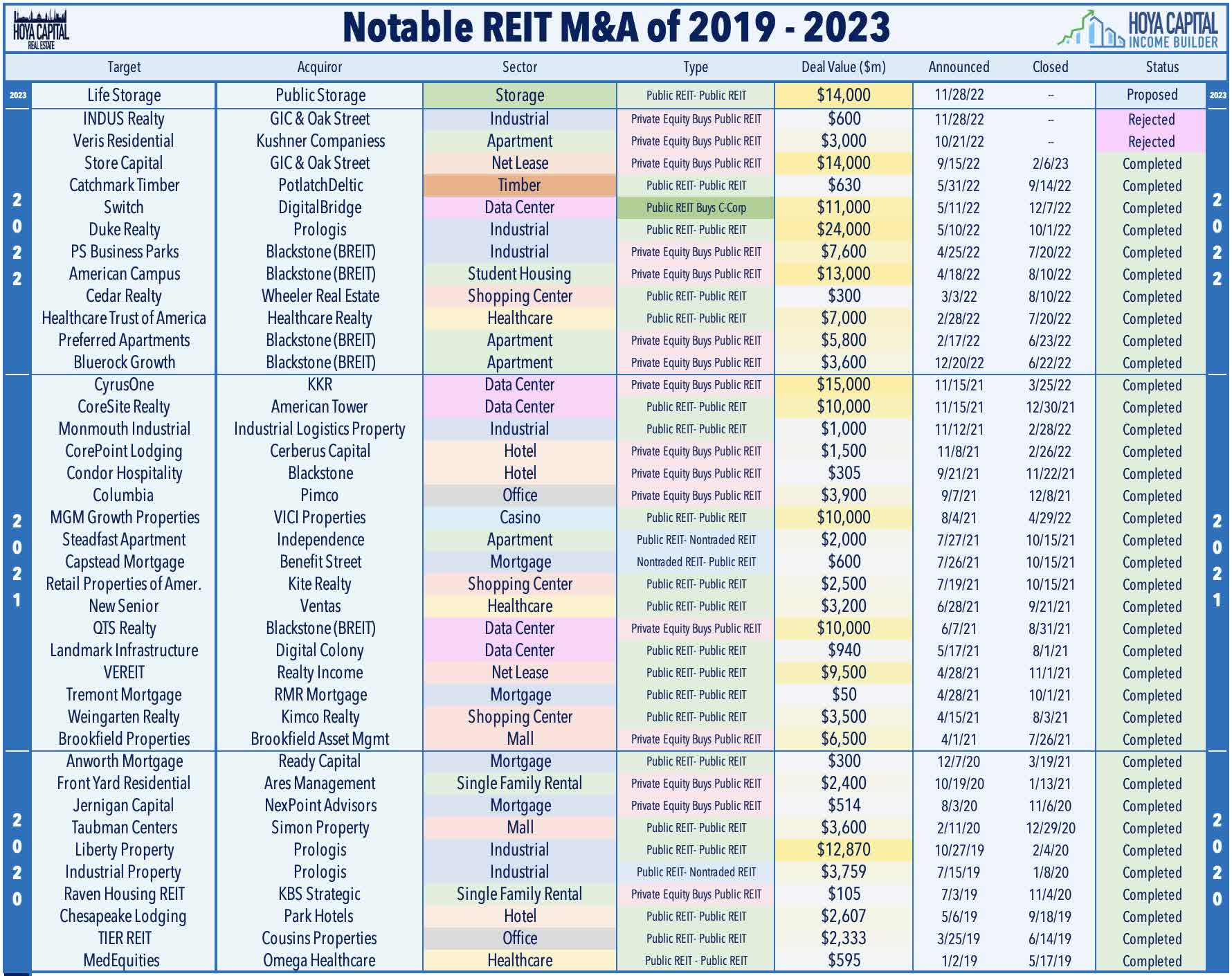

Storage : Major M&A news preceded the busy week of REIT earnings results. Life Storage ( LSI ) - which we recently added to the REIT Dividend Growth Portfolio - surged more than 11% on the week after it received an $11B takeover bid from its peer Public Storage ( PSA ) in a proposed all-stock deal worth about $129 a share - a 17% premium to LSI's prior closing price - but about 15% below LSI's 52-week high at $152. LSI - the fourth-largest storage REIT with a market cap of $9.5B - noted in a release that PSA had privately made an earlier "substantially similar" offer that was rejected. PSA noted in its release that LSI was "not willing to engage in further dialogue" after the initial private offer. Public Storage traded lower by about 3% on the week. Last week in Storage REITs: Downsized Demand , we analyzed why storage REITs have stumbled of late amid a post-pandemic demand normalization and pressure from elevated supply growth.

{kind=link}

Apartment : Residential REITs were the upside standouts this week following a strong slate of earnings reports. Apartment Income ( AIRC ) - which we own in the REIT Focused Income Portfolio - gained nearly 3% after reporting a sector-leading blended leasing spread of 11% in both Q4 and January - far exceeding the sector average of 6.1% and 4.8% for those periods. UDR ( UDR ) gained nearly 2% after reporting solid results and projecting FFO growth of 7.1% at the midpoint of its 2023 range, well above consensus estimates and the highest in the apartment REIT sector. Essex Property ( ESS ) gained 1.5% after reporting decent results despite ongoing headwinds from an uptick in unpaid rents in its California markets attributable to the state's ongoing eviction moratorium. Results from AvalonBay ( AVB ) and Equity Residential ( EQR ) - which traded roughly flat this week - shed light on market-level fundamentals, which showed relatively strong fundamentals in the Northeast and Southeast markets, but weakening out West - trends discussed in further detail in an Armada Advisors report linked here .

{kind=link}

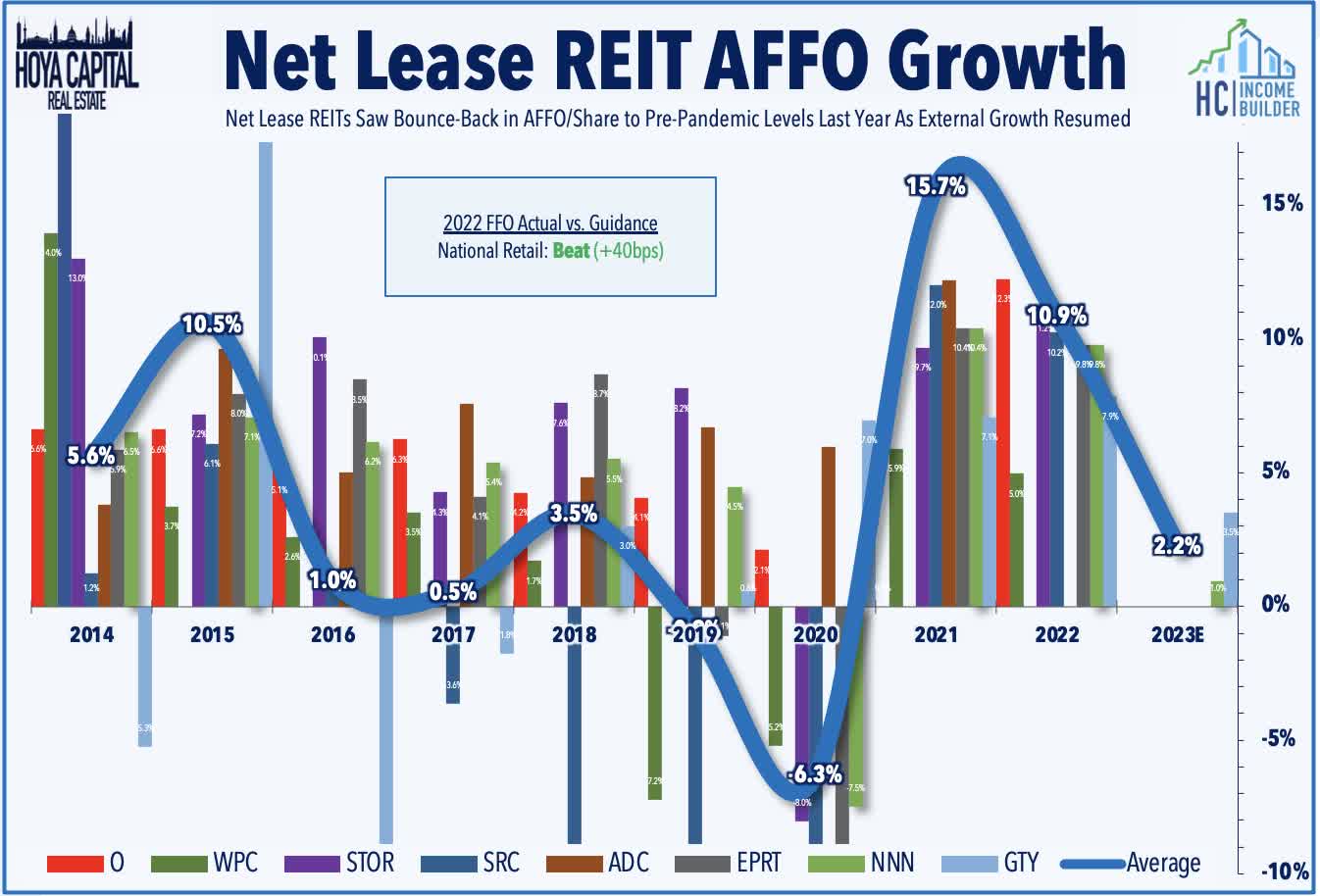

Net Lease : W. P. Carey ( WPC ) - which we own in the REIT Focused Income Portfolio - was also among the upside standouts this week, reporting very strong results this morning and issuing 2023 guidance that exceeded analyst estimates. WPC forecasts that same-store rent growth will increase to around 4% for the full-year 2023 as the effects of its CPI-linked escalators take full effect. National Retail ( NNN ) finished slightly lower this week after reporting line results, noting that its full-year FFO rose 9.8% in 2022 - 40 basis points above its prior guidance - and forecasting FFO growth of 1.0% for full-year 2023. Of note, while NNN reported muted cap rate movement - rising just 10 basis points from the same quarter last year, WPC observed more material widening with acquisition cap rates averaging 6.8% in Q4 - up 80 basis points from Q4 of 2021 while Alpine Income ( PINE ) reported that its acquisition cap rates rose to 7.2% in Q4 - up 120 basis points from Q4 of 2021. In Net Lease REITs: Calling The Fed's Bluff , we noted that asset owners seemingly haven't bought into the idea of a "new normal" of sustained higher interest rates.

{kind=link}

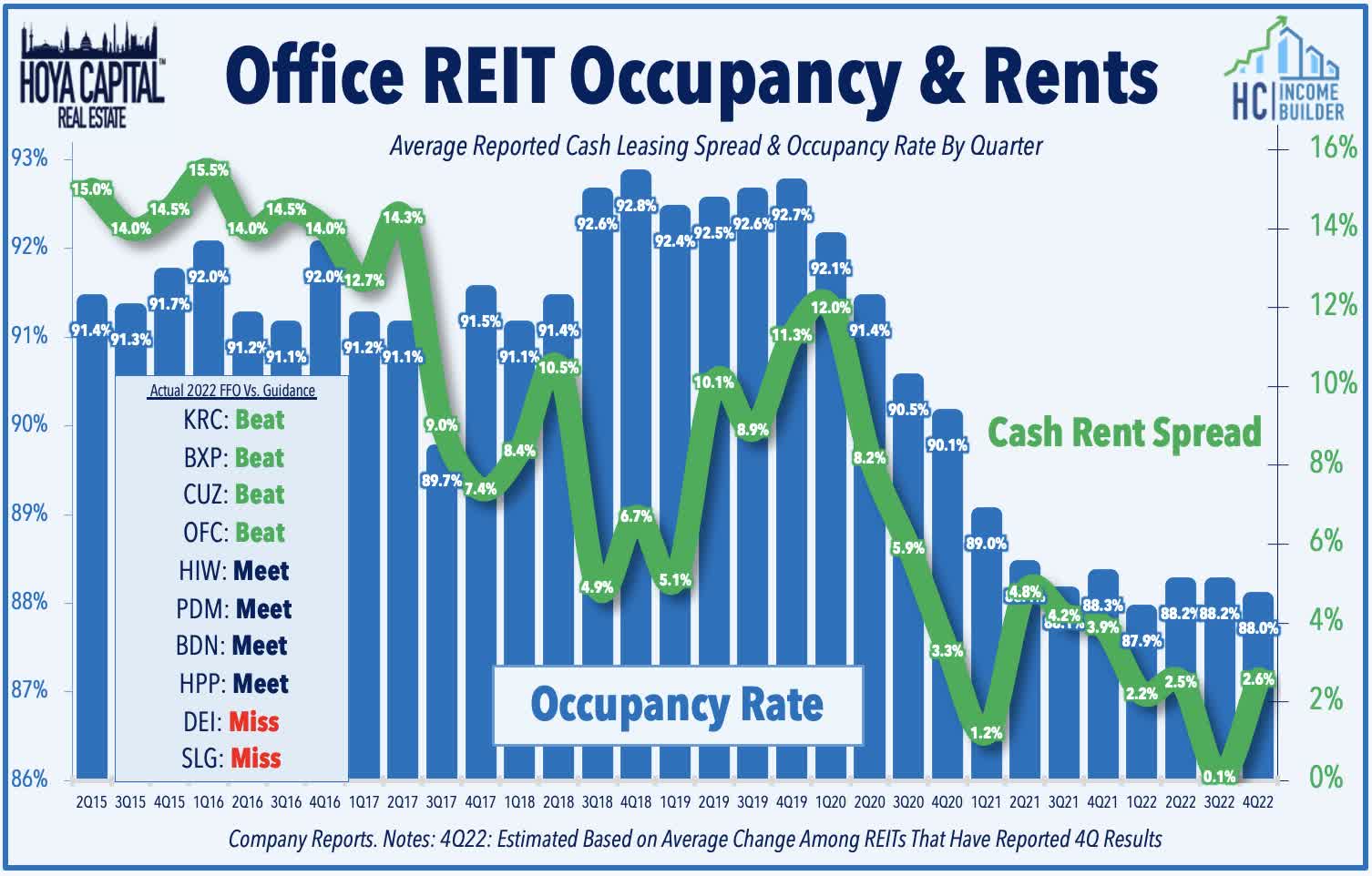

Office : A busy week of office REIT earnings results provided reasons for both optimism and pessimism and showed a continued bifurcation in fundamentals between sluggish urban coastal markets and faster-growing secondary and Sunbelt markets. Sunbelt-focused Cousins Properties ( CUZ ) - which we added to the REIT Dividend Growth Portfolio this week - advanced nearly 3% this week after reporting better-than-expected results highlighted by an acceleration in rent spreads to 7.3% and total leasing volume that was essentially in-line with its pre-pandemic levels from 2019. Highwoods ( HIW ) was outperformed its peers this week after reporting in-line earnings results highlighted by FFO growth of 4.4% in full-year 2022 and a sequential increase in occupancy rates. HIW - which focuses on Sunbelt markets - recorded solid total leasing volume of 924k SF in Q4 which lifted its full-year total to 1.5 million - the highest in eight years. Douglas Emmett ( DEI ) - which focuses primarily in Los Angeles - declined about 5% this week after reporting softer results with leasing volume, occupancy, and rent spread metrics showing ongoing demand softness with cash rents declining 9.9% from last year while occupancy rates declined another 20 basis points sequentially to 83.7%.

{kind=link}

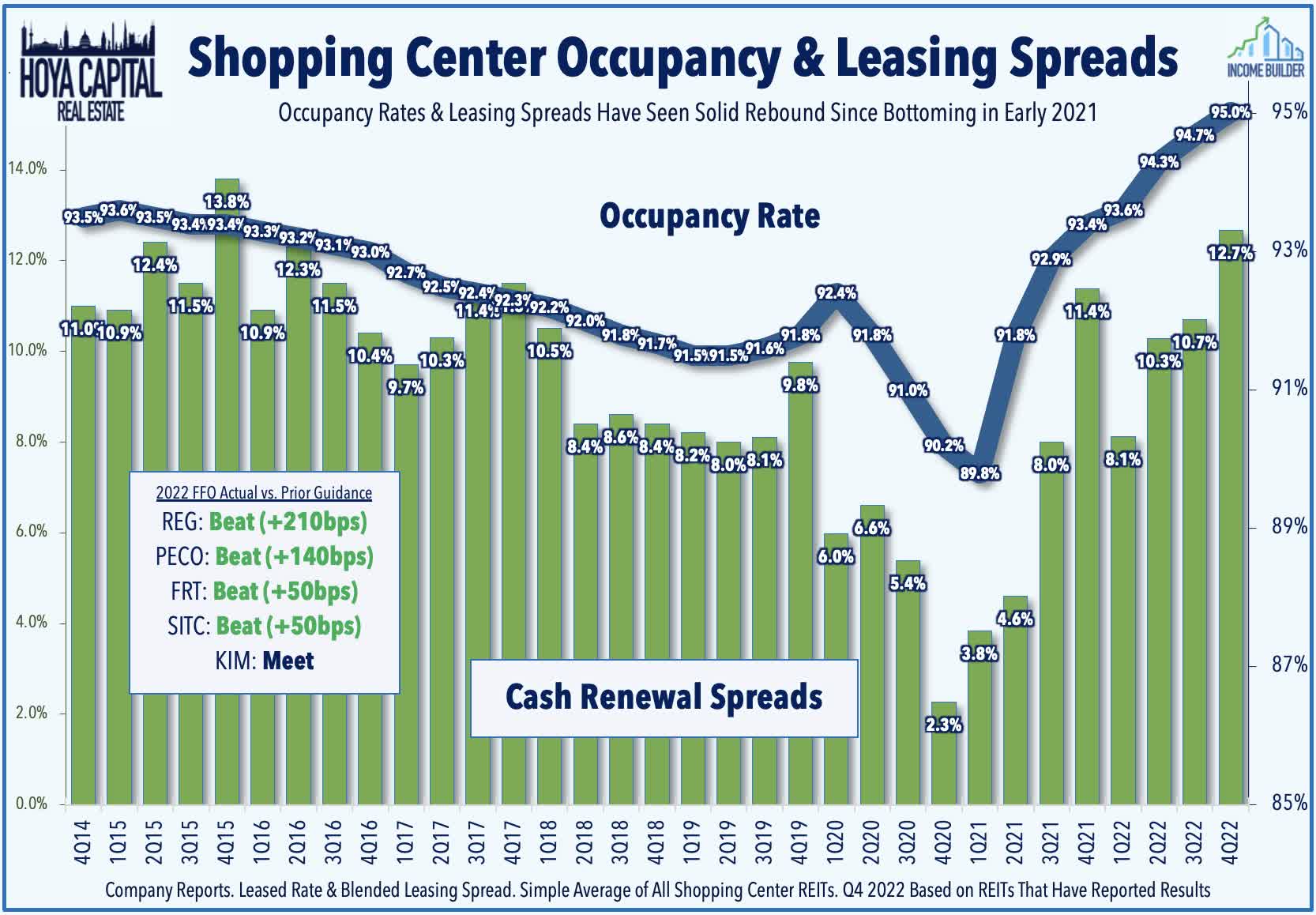

Strip Centers : Earnings season is still young for the retail sector, but results thus far have been quite solid - continuing a trend of better-than-expected results stretching back to late 2021 as demand for "big box" space has significantly exceeded the available supply. SITE Centers ( SITC ) was an upside standout this week, reporting a continued acceleration in rental rates with new lease cash spreads of 55.2% and renewal spreads of 7.6%. Comparable occupancy rates climbed to 95.4% - up 40 basis points from last quarter and 270 bps from last year. Notably, SITC commented that several tenants are eying potentially-vacated space from Party City and Bed Bath ( BBBY ) and that it expects to pursue an "aggressive recapture of space" given the backlog of demand rather than renegotiate leases. A pair of grocery-focused shopping center REITs - Regency Centers ( REG ) and Phillips Edison ( PECO ) - also outperformed their peers this week after reporting strong fourth-quarter results. Kimco ( KIM ) finished lower by about 3% on the week despite reporting decent results, achieving its highest year-over-year occupancy rate increase in 15 years alongside solid rent growth trends with blended cash leasing spreads of 8.7% - its strongest in nearly three years.

{kind=link}

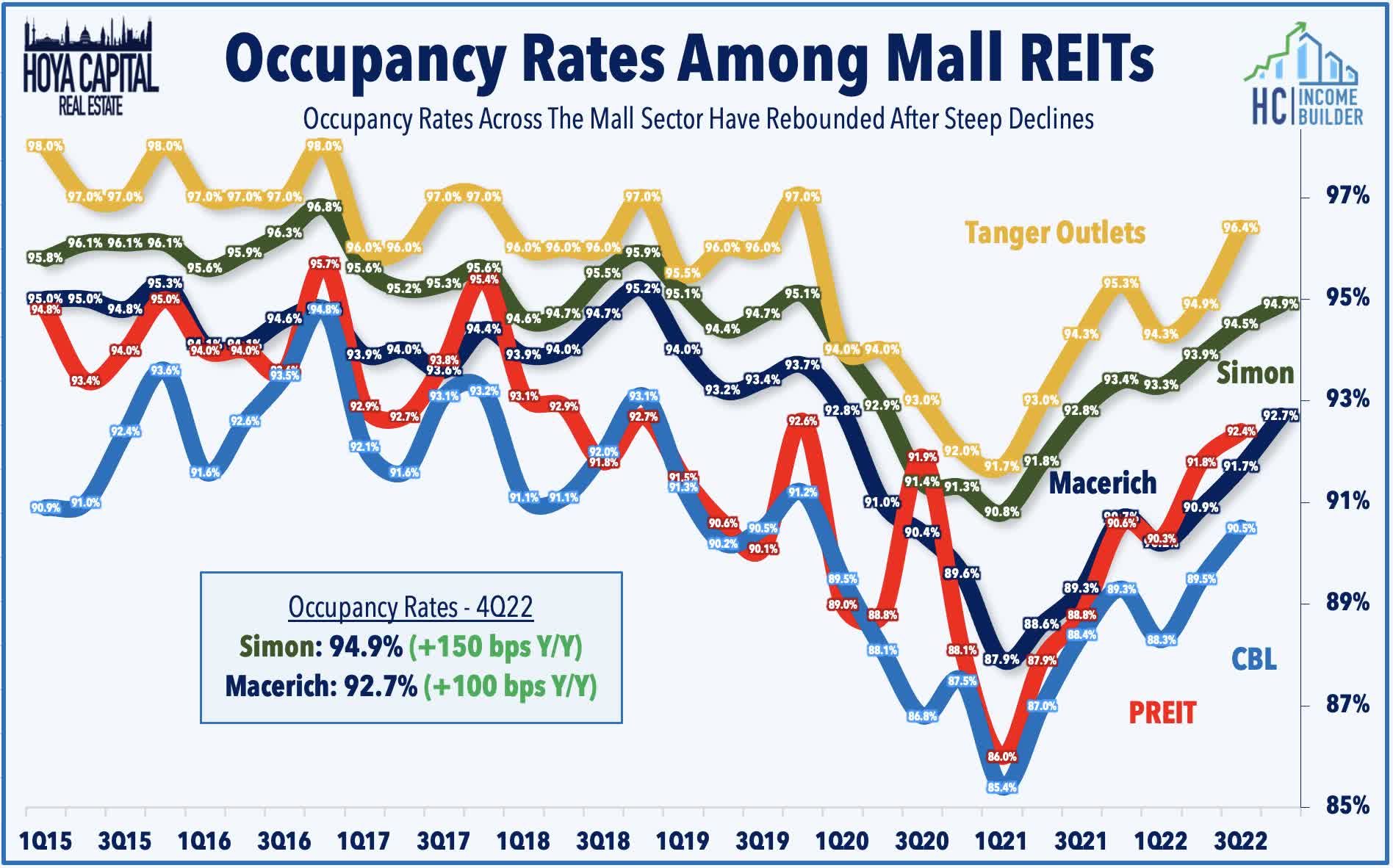

Mall : While not displaying the outright strength seen in the strip center format, mall fundamentals have stabilized in recent quarters for properties in the upper-end of the quality tiers. Simon Property ( SPG ) declined 4% on the week despite reporting fairly upbeat results, noting that its FFO declined 0.6% in 2022 - slightly above the midpoint of its prior guidance - while projecting that its 2023 FFO will be roughly even with 2022. Comparable occupancy climbed to 94.9% in Q4 - up 150 basis points from last year and exceeding the average pre-pandemic occupancy rate of 94.8% in full-year 2019. Average base rents rose 2.3% in Q4, which was the highest since Q1 2020. Macerich ( MAC ) dipped nearly 6% on the week after reporting relatively weaker results, noting its FFO declined by 3.4% in 2022 - matching the midpoint of its prior guidance range - but projected an 8.2% decline in FFO for full-year 2023. MAC's comparable occupancy rates rose to 92.7% - up 100 basis points from last year but still 100 basis points below its pre-pandemic level.

{kind=link}

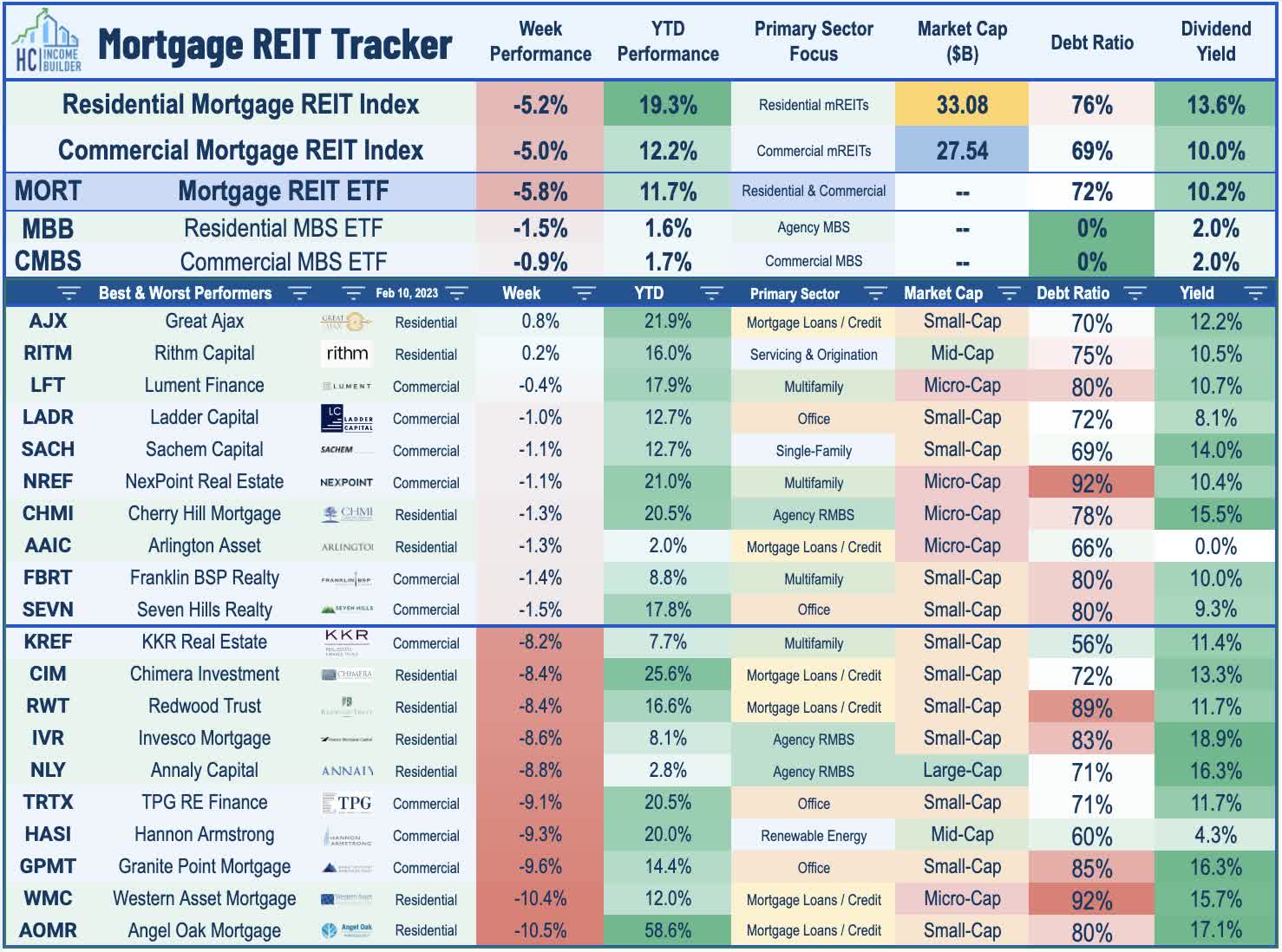

Mortgage REIT Week In Review

Giving back a chunk of its year-to-date gains following a stellar start to 2023, Mortgage REITs finished sharply lower this week amid pressure across fixed-income-related securities with the iShares Mortgage Real Estate Capped ETF ( REM ) dipping nearly 6% on the week. In our Earnings Halftime Report, we noted that residential mREITs have reported an average 2% increase in BVPS in Q4 from the prior quarter - led by a rebound in agency-focused mREITs - while commercial mREITs have reported a 1% decline. Upside standouts this week included Rithm Capital ( RITM ), which reported better-than-expected EPS and noted that its Book Value Per Share ("BVPS") was little changed at $12.00 - a solid report after reporting the strongest BVPS among residential mREITs last quarter. Ladder Capital ( LADR ) was also an upside standout after reporting that its Book Value Per Share ("BVPS") increased 2.1% with no major issues with loan performance despite its heavy exposure to office loans.

{kind=link}

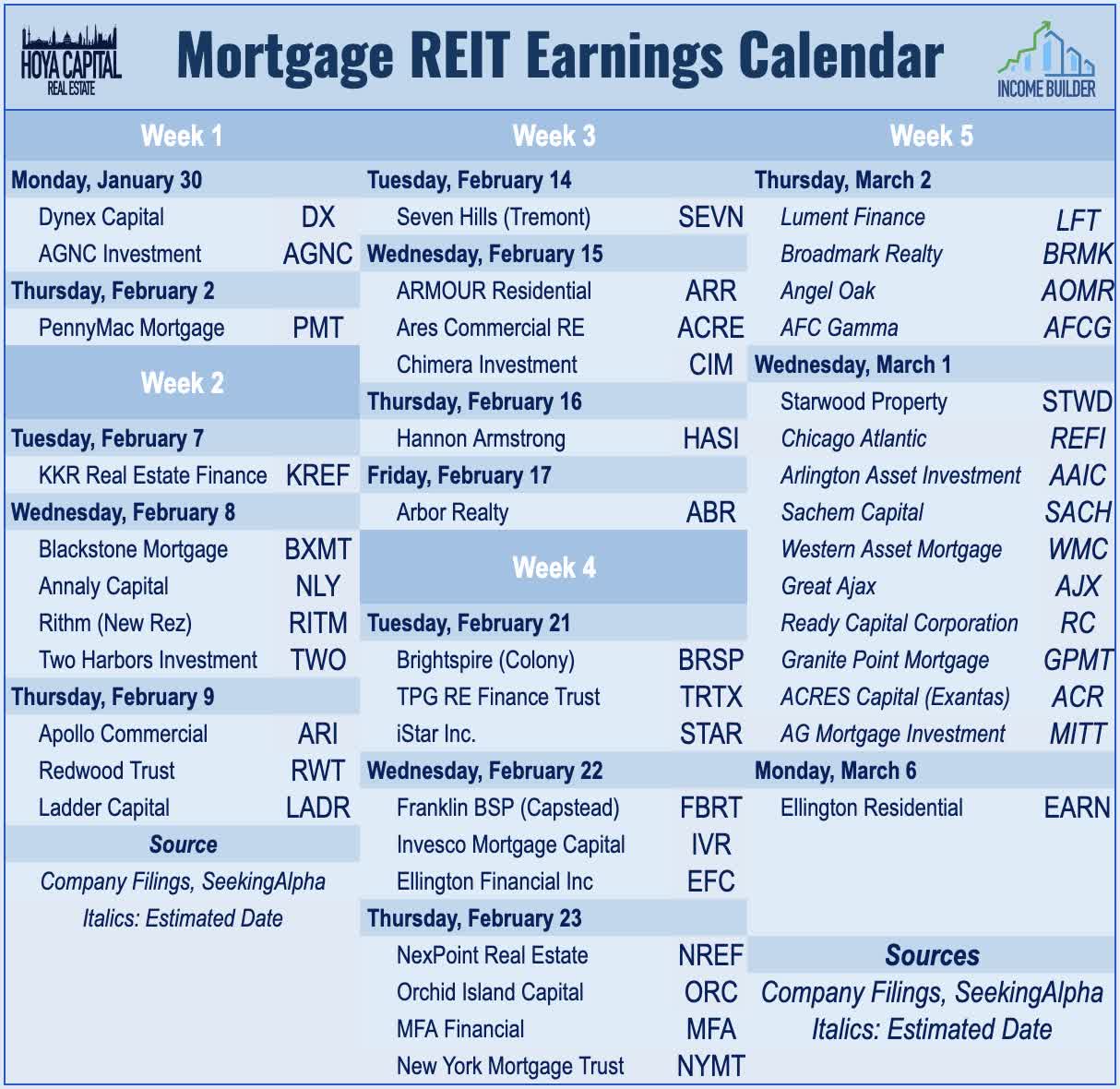

On the downside this week, Annaly Capital ( NLY ) - the largest mREIT - dipped more than 8% despite reporting better-than-expected EPS results and a decent 4.3% increase in its BVPS, but warned of a likely dividend reduction in anticipation of "some further pressure on Earnings Available For Distribution going forward." Redwood Trust ( RWT ) declined 8% after reporting that its BVPS declined 6.2% in Q4, but commented that its seen a quarter-to-date increase of 2% in its book value and estimates that its earnings available or distribution will "re-approach our dividend level." Back on the commercial mREIT side, Blackstone Mortgage ( BXMT ) and KKR Real Estate ( KREF ) each declined about 8% as well this week after reporting mixed results with modest declines in their BVPS. We'll hear results from six mREITs next week: Seven Hills ( SEVN ), ARMOUR Residential ( ARR ), Ares Commercial ( ACRE ), Chimera ( CIM ), Hannon Armstrong ( HASI ), and Arbor Realty ( ABR ).

{kind=link}

2022 Performance Recap & 2023 Check-Up

Through the first six weeks of 2023, the Equity REIT Index is higher by 9.1% on a price return basis for the year while the Mortgage REIT Index is higher by 11.7%. This compares with the 6.7% gain on the S&P 500 and the 8.7% advance on the S&P Mid-Cap 400 . Within the real estate sector, all 18 property sectors are in positive territory on the year led by Billboard, Hotel, Industrial, and Single-Family Rental REITs. At 3.74%, the 10-Year Treasury Yield has dipped 14 basis points since the start of the year and remains well below its 2022 highs of 4.30%. The US bond market has rebounded following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 1.5% this year.

{kind=link}

Economic Calendar In The Week Ahead

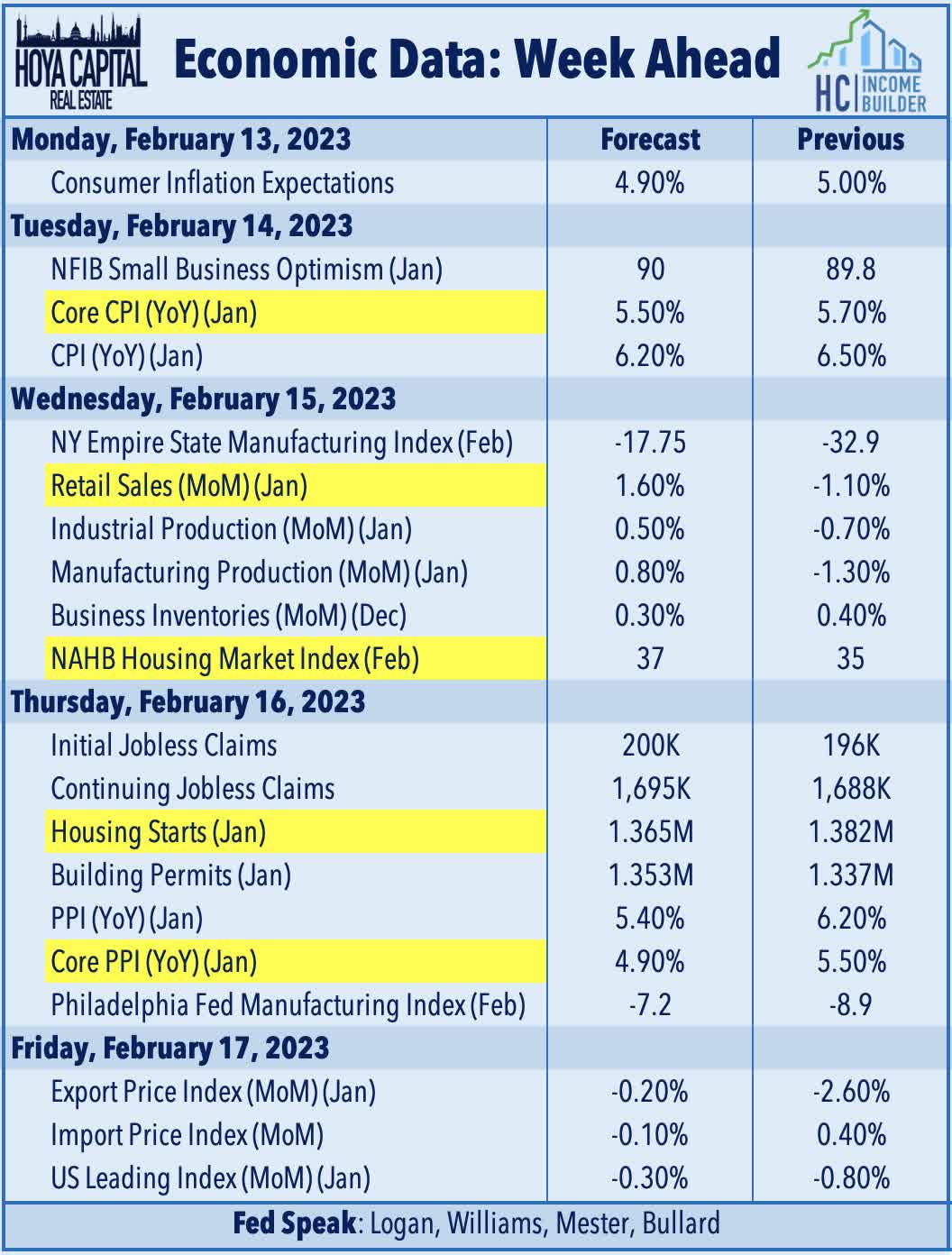

Inflation, retail, and the U.S. housing market are in the spotlight in another jam-packed week of economic data in the week ahead. The main event comes on Tuesday with the Consumer Price Index for January, which investors and the Fed are hoping will show a continued cooling of inflationary pressures. The headline CPI is expected to moderate to a 6.2% year-over-year rate while the Core CPI is expected to decelerate to 5.5%. As with recent months, the metric we're watching most closely is the CPI-ex-Shelter Index - which since July has averaged a -3.2% annualized rate - among the most deflationary five-month periods on record. Later in the week on Thursday, we'll see the Producer Price Index which is expected to slow to similar signs of cooling. The headline PPI is expected to slow to a 5.4% year-over-year rate - down from the recent peak in March at 11.8%. We'll also see an important slate of housing market data with NAHB Homebuilder Sentiment data on Wednesday and Housing Starts and Building Permits data on Thursday which are expected to show a modest thawing of the once icy-cold housing market. On Wednesday, we'll also see Retail Sales data for January which is also expected to show a rebound in spending following a disappointing month of December.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

All Eyes On CPI