BIRD - Allbirds: Pitfalls Abound

2023-05-12 01:44:31 ET

Summary

- Shares of Allbirds have tanked this year as the company struggles to comp strong sales last year.

- Revenue is down double-digit, and leverage is also contributing to sharp gross margin pressures.

- The company is also resorting to promotions to drive sales, which is bringing down both ASPs and margins.

- At the same time, though the company has announced layoffs, overhead costs as a percentage of revenue are soaring.

Recessions hit all companies hard, but especially those that were struggling before bad times erupted. Such is the case for Allbirds ( BIRD ), the shoemaker known for its sustainability practices and comfortable wool shoes. Once one of the dominant footwear brands among younger generations especially in tech-heavy San Francisco, Allbirds is now struggling to maintain its relevance as well as stay afloat on top of a heavy cost structure from when the company was expanding aggressively.

With a stock price that is now down more than 40% year to date, Allbirds' market cap has sunk below $250 million, putting the company firmly in risky small-cap territory. The question for investors now is: does Allbirds have room to rebound?

My view on Allbirds has soured dramatically after seeing this year's consistent string of disappointing results. I am downgrading my view on the company to bearish, as I see no new near-term catalysts that can help save this company from decline.

Here, in my view, are the top concerns with Allbirds at present:

- The market has gotten more competitive, and Allbirds' star is fading. We shouldn't be surprised that fashion is subject to fads. The pandemic and its era of collectibles has brought sneaker collections back into the limelight, and now Allbirds' street cred is starting to fade.

- Promotional macro environment. Consumers are pinching their wallets amid this recession, and retailers are sitting on unsold inventory - which, in the apparel business, loses its value faster than in other industries. That has driven a tremendous promotional environment that has led to deep discounting, and Allbirds has needed to participate in the discounting to remain competitive - hurting its margin profile.

- Profitability at risk. Deleverage from lower volumes as well as lower average selling prices has put a huge dent on Allbirds' gross margin profile. And while its margins are still high relative to other apparel makers, the company is sitting on large overhead levels from its startup-expansion days, and its long string of adjusted EBITDA losses as well as a constrained balance sheet are going to make investors more nervous.

Now, of course, there are silver linings underneath the recent doom and gloom in Allbirds. The company is trying hard to push into different market sets - for example, the company launched its first golf shoe . Allbirds' foray into specialized athletic shoes has so far been restricted to running, and in the future the company could diversify its revenue streams into product like cleats and boots.

The other long-term driver for Allbirds is its status as a B corp and its ethos around sustainability - trends that are going to remain present among younger consumers for quite some time. The company has attempted more focused marketing around this ethos, in particularly recently announcing its M0.0NSHOT initiative - which is a goal to create the world's first net zero carbon shoe. The company noted that this announcement generated strong social media impressions. Greater resonation of this message is likely the biggest upside risk for Allbirds; but at the same time, it is difficult to see brands regain popularity once its initial star has dimmed.

Net net, I see more risk than upside in Allbirds, especially as the company battles declining sales and a very crowded footwear market. Steer clear and invest elsewhere.

Q1 recap

There unfortunately weren't too many positive highlights coming out of Allbirds' recent Q1 earnings print. Take a look at the earnings summary below:

{kind=link}

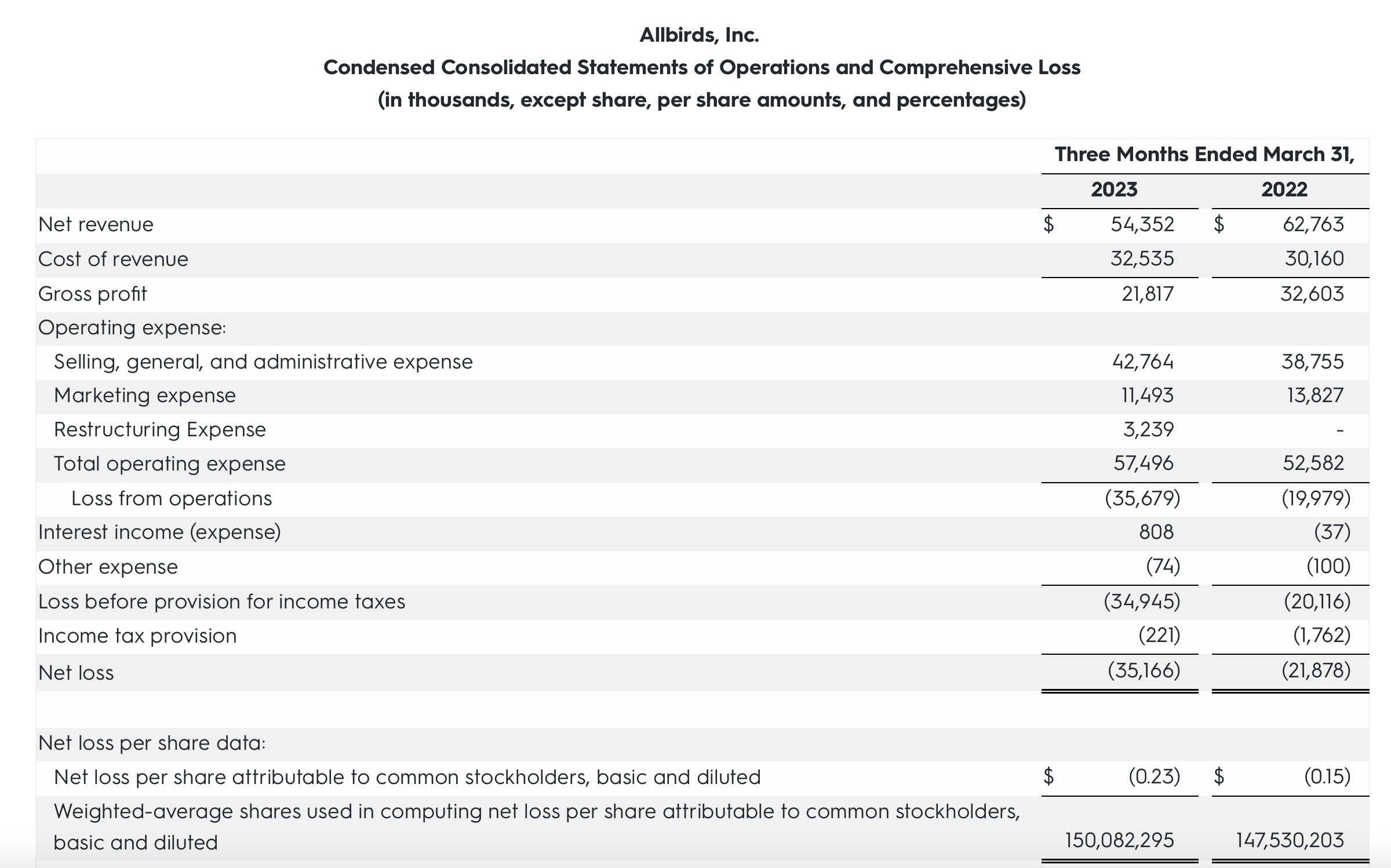

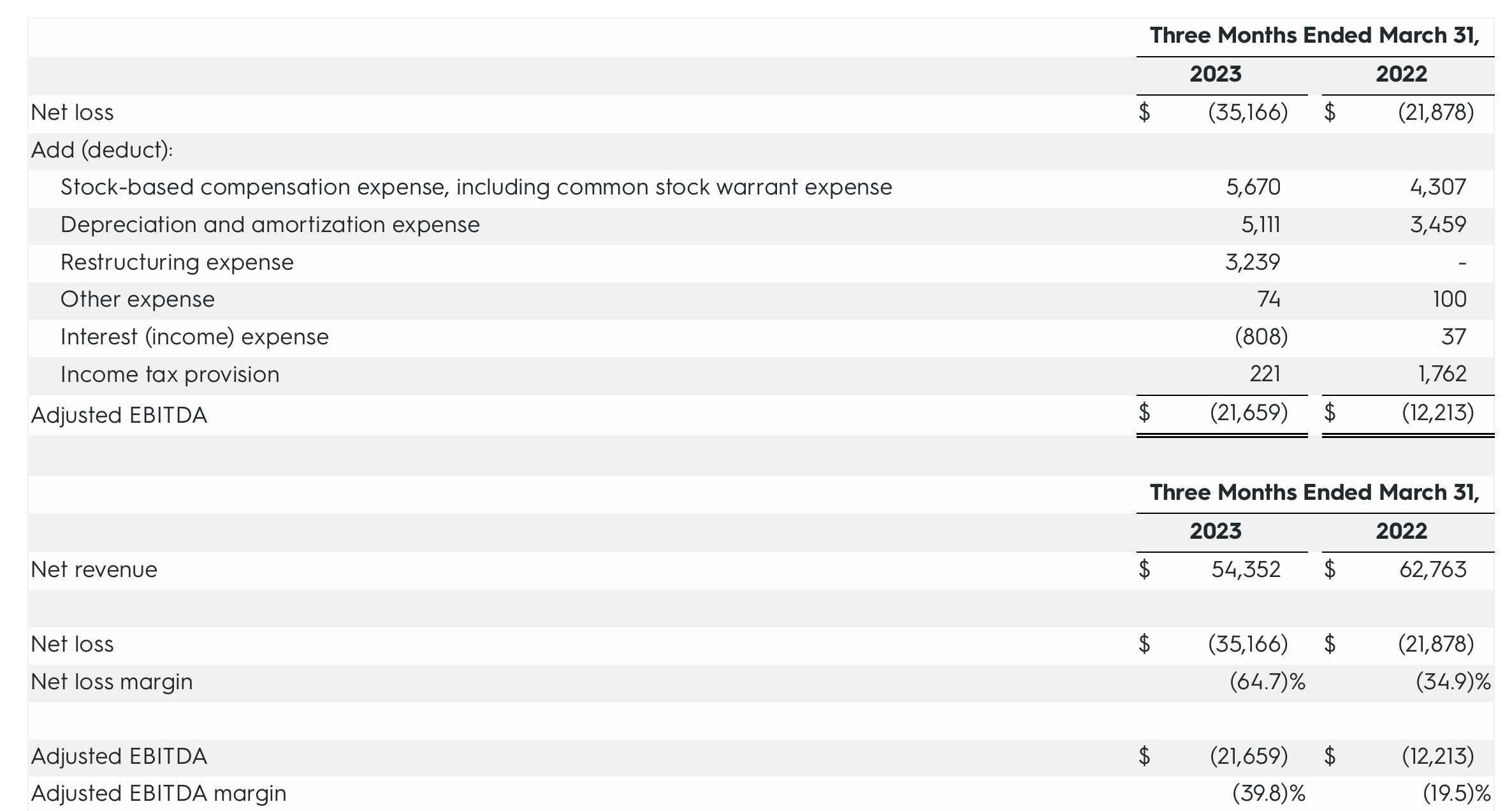

Allbirds' revenue declined -13% y/y to $54.4 million. Though a double digit decline, there are three silver linings here: first, it did beat Wall Street's expectations of $47.9 million (-24% y/y) by a fairly large margin, and second, revenue was up 10% y/y versus the same quarter in 2021. And third, Allbirds' international business has continued to grow, with revenue growth of 6.5% y/y in local currency terms. Of note in particular is Japan, which grew 50% y/y.

All in all, however, the company's message was one of retrenchment. The company is pulling back on store openings. Per CEO Joey Zwillinger's remarks on the Q1 earnings call:

Moving now to US distribution. As a reminder, we have slowed the pace of new store openings to focus on driving four-wall profitability. We are pleased with our real estate portfolio of 40 full price stores and 3 outlets in the US. In Q2, we opened one new store in the US, with two more to follow later in the year. We continue to focus on driving traffic and conversion, and are making inroads with several store pilots under the leadership of our new head of stores."

Revenue declines have led to deleverage. Gross margins dropped substantially to 40.1%, a loss of nearly twelve points versus 51.9% in the year-ago quarter - driven by a number of factors including higher promotions, write-offs on older products, manufacturing transition costs, and a channel mix shift to third-party resellers. Note that as Allbirds is planning to slow down the pace of its storefront expansion, it plans to invest more heavily in its third-party reseller channel.

Overall adjusted EBITDA, meanwhile, saw nearly double the amount of losses at -$21.7 million, or a -40% margin: versus a -20% margin in the year-ago quarter. Allbirds continues to expect losing roughly $20 million in adjusted EBITDA next quarter in Q2.

{kind=link}

Liquidity here is fairly limited - Allbirds has just $143.3 million of cash left on its balance sheet, plus $50 million of committed funding in the form of a revolving line of credit. The company won't be running dry anytime soon, but it's unclear if Allbirds has a path to breakeven while its sales continue to see persistent shrinkage.

Key takeaways

In my view, there's not much to like about Allbirds at the moment. Poor sales momentum, a tough competitive environment that has led to heavy promotions, and a heavy cost profile that is leading to consistent quarterly losses. Steer clear here and invest elsewhere.

For further details see:

Allbirds: Pitfalls Abound