BIRD - Allbirds: Risky But Not Out Of The Race

2023-11-29 13:30:27 ET

Summary

- Allbirds has experienced a significant decline in market value and declining sales over the past year.

- The company is working on redefining its operating model, focusing on its U.S. distribution network and third-party distribution in international markets.

- Allbirds is trading below book value and has no debt, making it an attractive investment option despite its current challenges.

Shoemaker Allbirds ( BIRD ) has been a leading example of "disruptive commerce" companies that shone bright during the pandemic, but have performed terribly in this recessionary period. Once a trendsetter in Silicon Valley that many claimed to be the "most comfortable shoe ever," Allbirds has lost its cool factor and suffered declining sales for more than a year.

Since the start of 2023, Allbirds has shed more than half of its market value, briefly dipping below $1 and risking a de-listing (the jury is still out on that). A recent Q3 earnings print, which showed continued deceleration in revenue despite a step-up in promotional activity, did little to assuage investors' confidence.

Two reasons why Allbirds isn't dead money yet

I last wrote a neutral opinion on Allbirds in August , when the stock was trading ~30% higher at ~$1.30. Since then, the stock has fallen substantially and released yet another disappointing earnings quarter - which I think fairly counterbalance each other.

Allbirds' risks are well-known, and we'll discuss the fundamental weaknesses that the company has displayed in the next section. But it is worth highlighting, for a moment, the two chief reasons that I see buoying Allbirds and keeping it in the race to recovery.

The first is that the company is hard at work re-defining its operating model. Chief among that is reining in its international expansion strategy. The company closed three net stores in the third quarter, and is moving to primarily a third-party distribution network in international markets.

{kind=link}

At the same time, the company is drumming up its U.S. distribution network as well, recently opening a storefront on Amazon to boost its visibility. A deeper push by third-party distributors to a small yet core customer base may be the key that Allbirds needs to return back to growth.

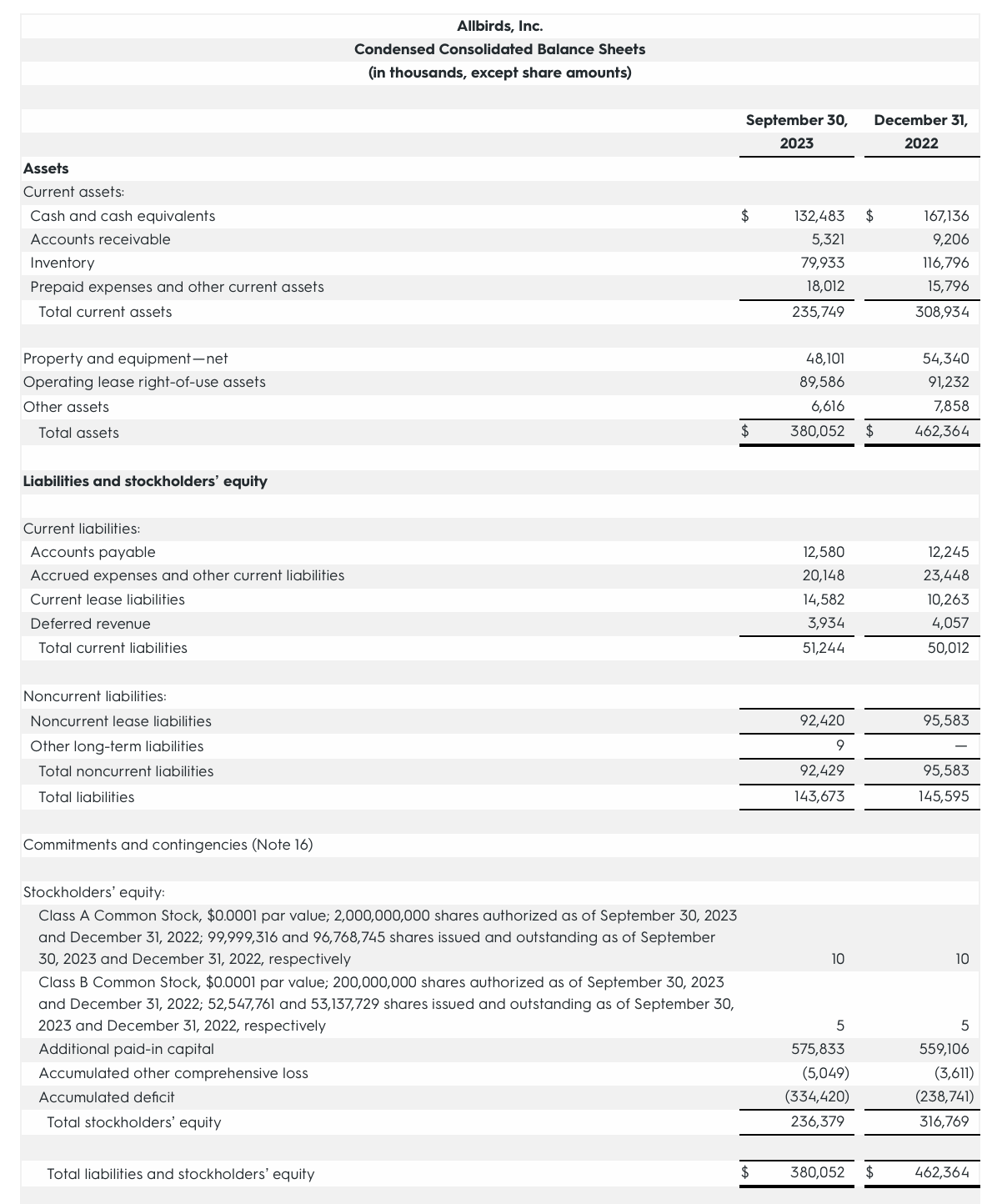

Secondly, and perhaps more importantly, it's worth noting that Allbirds continues to trade below book value, which is an absolute rarity in today's stock market. As shown in the chart below, Allbirds has a book shareholder equity of $236.4 million, so its current $155.2 million market cap (at just north of a $1.00 share price) sits at a 0.7x P/B ratio.

{kind=link}

Moreover, it's worth noting that Allbirds has no debt alongside $132.5 million in cash and equivalents - essentially, nearly the entirety of Allbirds' market cap sits in cash. The company could liquidate today - including inventory and fixed assets - and shareholders would walk away with more than $1/share in value.

Allbirds' stock price reflects the market consensus that Allbirds will continue to limp along and burn cash, eroding the value that is sitting on its balance sheet. In my view, however, the company's low valuation and its reasonable turnaround plan are solid reasons to invest a small position in Allbirds. I remain neutral on the stock - don't invest a large stake here - but I think expectations are low enough where any positive news will be met with a large upside surprise.

Q3 recap

That all being said, however, it would be remiss not to note that the company's latest trends - especially its top-line performance - do bear some concern.

{kind=link}

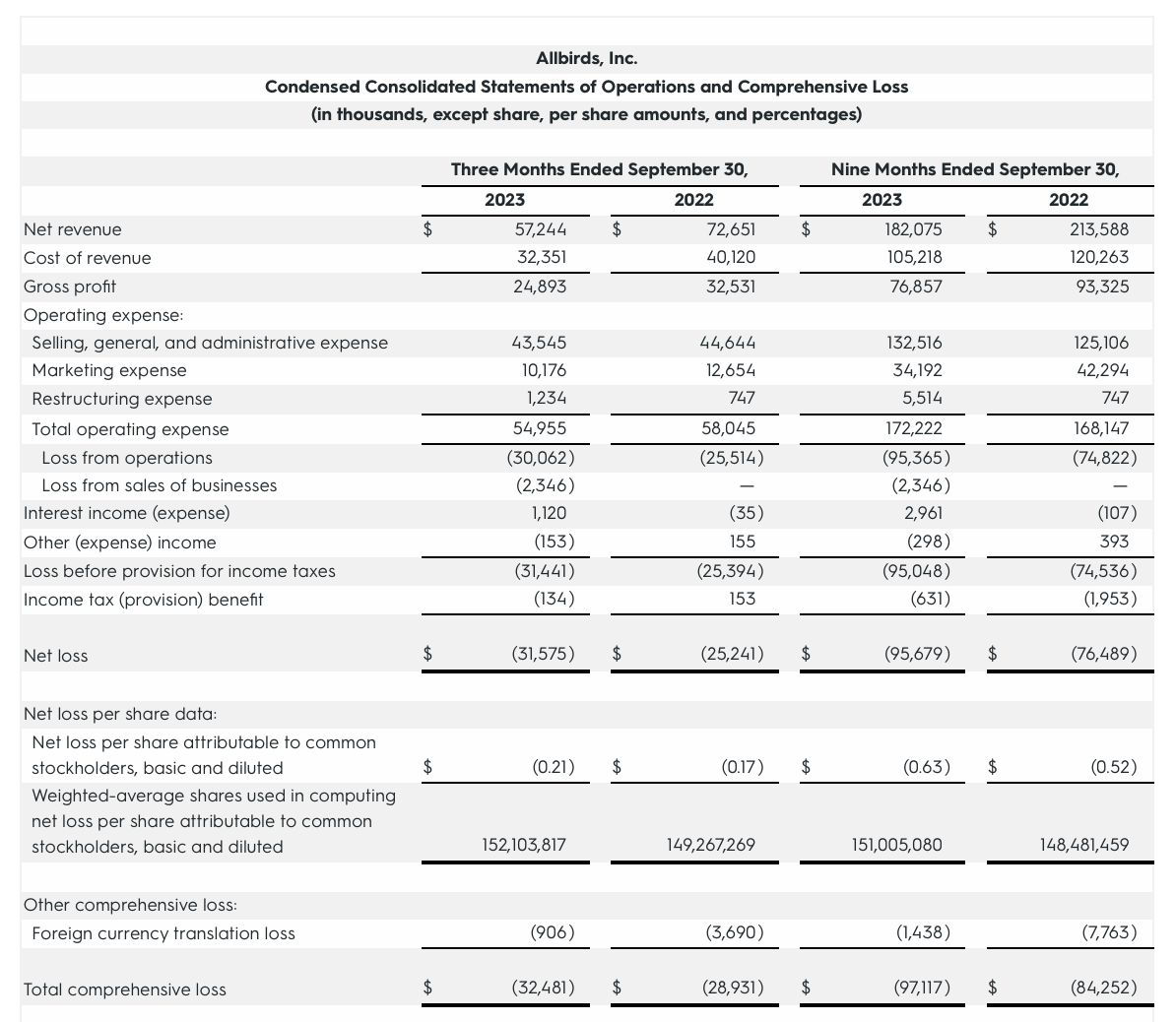

Revenue in the third quarter declined -21% y/y to $57.2 million, missing Wall Street's expectations of $59.4 million (-19% y/y) by a two-point margin. Making matters worse, revenue worsened relative to just a -10% y/y decline in Q2. This illustrates the core risk that Allbirds faces: fashion is a trend, and consumers are effectively voting that Allbirds is out.

Hope isn't lost, however. Retro styles have been known to make comebacks and drive renewed enthusiasm out of the blue - as this year's resurgence in popularity for the adidas Samba shoes has proven.

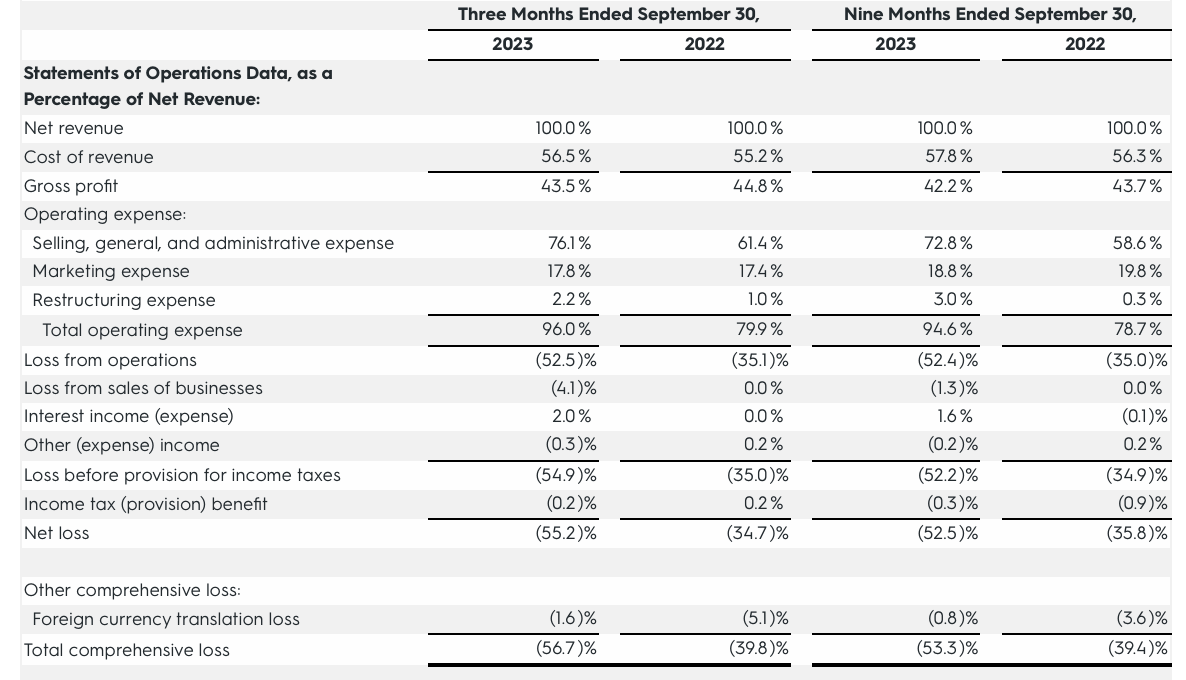

Still, volume deleverage - plus the fact that Allbirds has been pushing more discounts in order to stimulate demand - have hurt the company's margin as well.

{kind=link}

As shown in the chart above, gross margins fell 130bps y/y to 43.5%. And though total operating expenses on a nominal basis did fall -5% y/y to $55.0 million, driven by the company's layoffs and international store exclosures, revenue deleverage has total opex up to 96% of revenue, up sixteen points from 80% in the year-ago Q3 (of which ~1% is an increase in restructuring expenses).

The company is expecting the holiday season to be heavily promotional as well, though the company is reducing marketing spend year-over-year. Per CEO Joey Zwillinger's remarks on the Q3 earnings call:

As we approach another holiday selling season with consumers exercising caution around spending, we are prepared for an early and highly promotional holiday period industry-wide and prioritize getting inventory to a healthy position in early 2024 with an elevated pace of unit sales through 2023. We intend to remain competitive on price with reduced marketing spend. In fact, Q4 will mark our fourth consecutive quarter of moderated marketing spend, which is expected to be down more than 15% for the full year in '23 versus 2022."

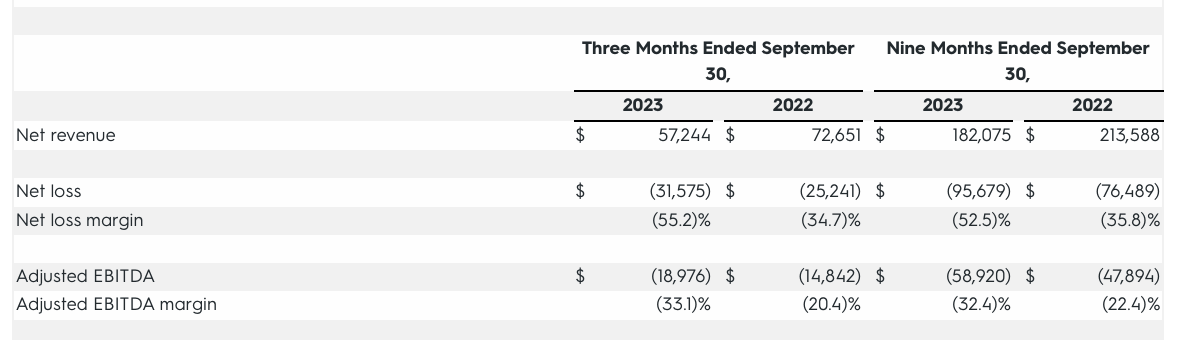

Adjusted EBITDA losses widened to -$19.0 million, a 28% greater loss than in the prior-year quarter, while adjusted EBITDA loss margins suffered 13 points to -33%:

{kind=link}

The bright side here: cash burn is down. Year to date operating cash burn of -$25.5 million is ~70% lower than -$82.2 million in the prior-year period: reflecting inventory shrinkage as the company reduces storefronts and clears out old models to make room for the latest Wool Runner 2.

Key takeaways

I'd hardly call Allbirds a slam dunk investment, but with a stock trading below book value, it's hard to not at least take a look and a small position. With expectations low, there's a good chance that Allbirds' performance during the holiday season may surprise us - especially as new distributor partnerships may open doors to new buyers.

For further details see:

Allbirds: Risky, But Not Out Of The Race