BIRD - Allbirds: Stabilizing But Not Yet Out Of The Woods (Ratings Upgrade)

2023-08-24 04:14:01 ET

Summary

- Allbirds, the sustainable shoemaker, has lost 40% of its value year to date, but sentiment is slowly improving after better-than-expected Q2 results.

- The company's turnaround strategy includes cost-cutting measures and improving gross margins.

- However, risks remain, including being out of fashion and competing in a promotional retail environment. Investors should wait and see before buying Allbirds stock.

- Interestingly, Allbirds currently trades below book value, which is one reason to not be too bearish on this name.

Even after a sharp correction in the month of August, most small-cap stocks remain up a healthy amount in the year to date as investors waded their toes back into risk-taking. There are a few exceptions here, including and especially Allbirds ( BIRD ), the shoemaker known for its wool products and sustainable practices.

The troubled company has lost 40% of its value year to date, pushing its market cap below the $250 million threshold. Sentiment in the stock, however, has been slowly regaining steam over the past couple of weeks as Q2 results turned out better than feared. The question for investors now: where does Allbirds go from here?

I wrote a bearish opinion on Allbirds back in May, citing the company's sharp revenue declines and profitability concerns as the primary driver. Now with Q2 results in the rearview mirror, however, I'm starting to see some elements of the company's turnaround strategy play out and am revising my opinion on the stock to neutral.

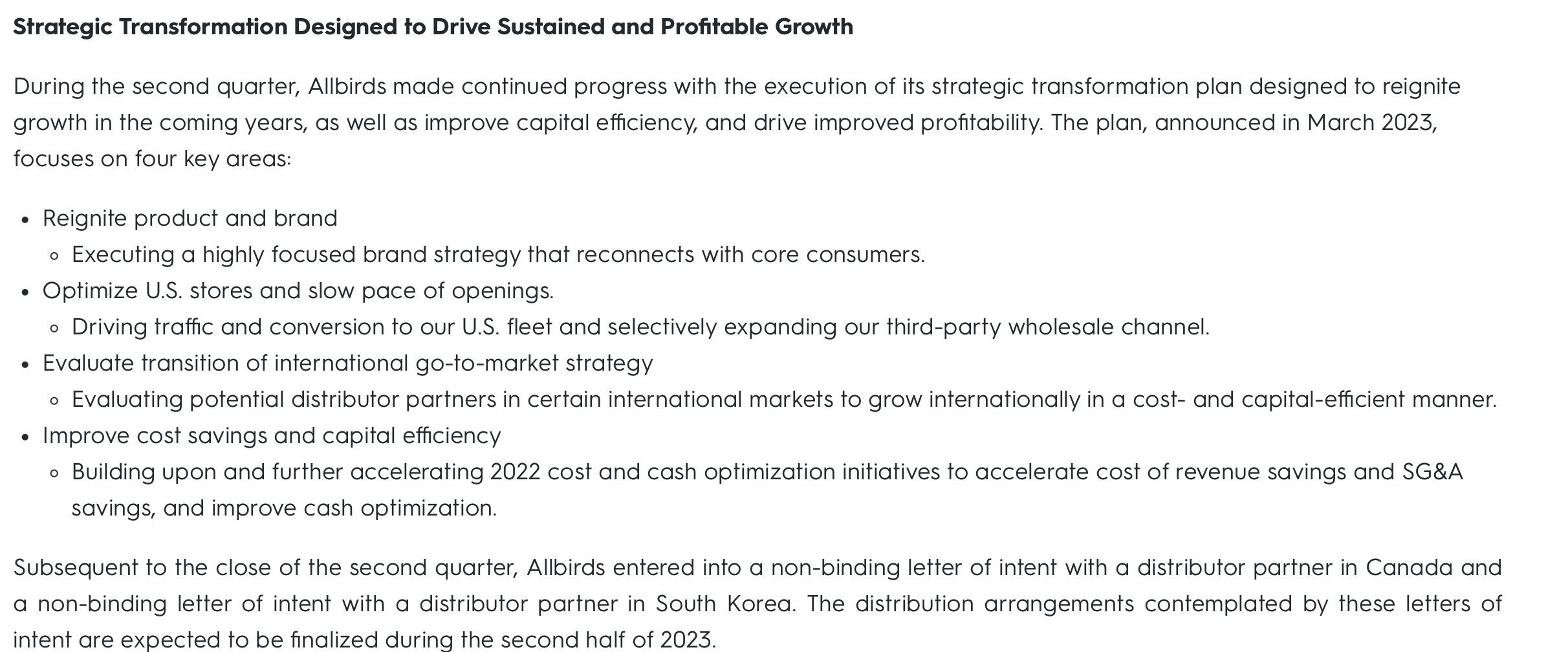

Earlier this year, Allbirds released a four-point plan to revitalize its business. The core tenets of that plan are laid out in this snapshot below:

{kind=link}

The element most directly under Allbirds' control, of course, is cost. The company has done an excellent job trimming down operating expenses as a percentage of revenue by dramatically slowing down its pace of store openings. It has also improved its gross margin profile - due to better inventory management and fewer write-downs, while also benefiting from market-driven reductions in logistics and freight expenses.

It's due to this improvement in bottom-line losses, plus slightly better revenue trends, that are turning around my opinion on Allbirds. It isn't completely smooth sailing for Allbirds going forward, however, because I still see two very prevalent risks for this company:

- Fashion is fad-based, and Allbirds is decidedly out. Sneaker collecting rose during the pandemic, and while sneakerheads continue to chase the latest releases from NIKE ( NKE ) and Yeezy, Allbirds - which for a very brief time was considered part of the Silicon Valley uniform - is out. It's difficult for a brand to reclaim its "cool" factor once it has fallen out of favor.

- The retail industry is in a very promotional environment. The dominant theme in the retail industry this year is heavier promotions to stimulate consumer spending in a tough macro environment. Competing in this environment may be damaging to Allbirds' margins.

All in all, though I'm incrementally more positive on Allbirds with the latest earnings print showing margin lifts, I'm not rushing off the couch to buy Allbirds stock just yet. I'm in "wait and see" mode to assess whether Allbirds can successfully execute on its turnaround plan - and in particular, revitalize its brand and top-line trends with expansion both domestically and internationally. Cost-cutting and slowing down store expansions in the current macro environment is prudent, but for Allbirds to have a future, it has to prove that it can scale its brand - and at the moment, this remains a big question mark.

Keep this stock on your watch list, but don't leave the sidelines just yet.

Q2 download

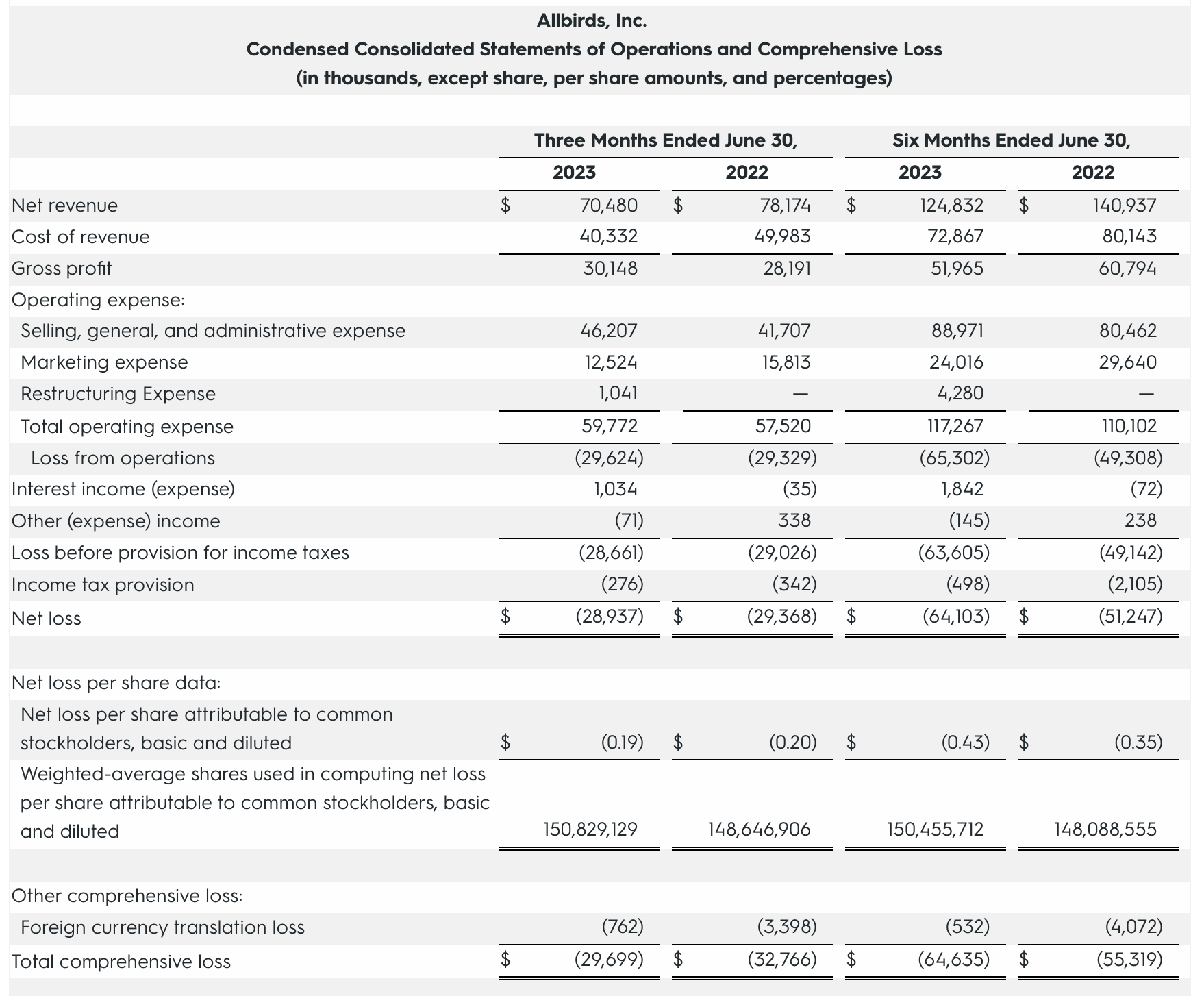

Let's now go through Allbirds' latest Q2 results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Allbirds' revenue declined -10% y/y to $70.5 million, ahead of Wall Street's expectations for $67.5 million (-14% y/y) and accelerating three points above Q1's decay rate of -13% y/y. Sequentially, revenue also grew 30% versus Q1, though there's an element of seasonality as Q1 has a typical post-holiday revenue decay and channel inventory unwinding.

Though Allbirds doesn't report unit sales, the company noted that average selling prices were down this year driven by higher promotional activity. This implies a single-digit decline in unit volume sales, but highlights the need for Allbirds to offer sales and incentives to compete against aggressively discounted peers.

The company is experimenting with product innovation in order to drive volume growth. The company noted that its new "Golf Dasher" show has been met with positive reviews and strong traction, coinciding with the lead-up to the PGA Tour season. It also introduced a new "Superlight" collection in April made of a new foam material. Lastly, the company is also starting to experiment with collaborations, a strategy that has produced very lucrative and highly sought-after limited releases for brands like Nike and Adidas.

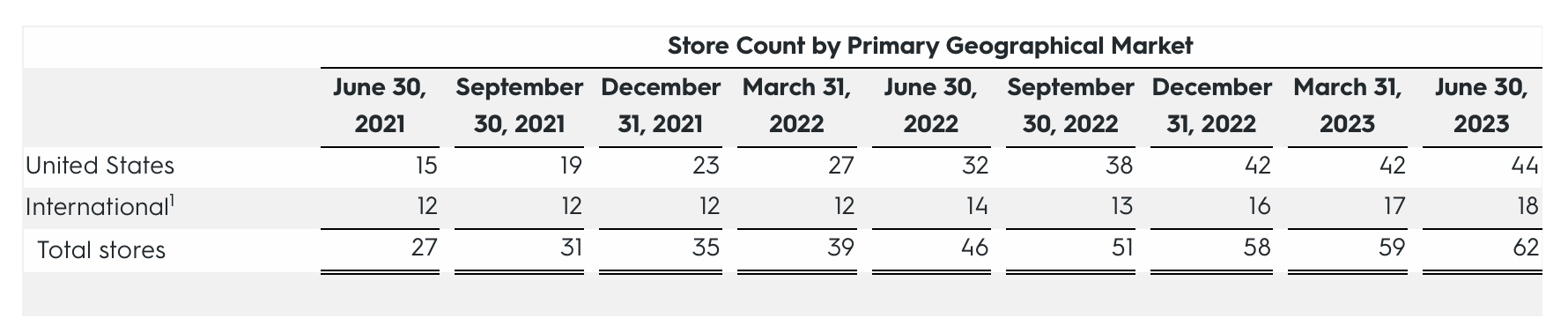

Allbirds opened three net-new stores in the quarter, two in the U.S. and one abroad - which brings the YTD store opening count to just four. This is a massive slowdown from the prior several years, where opening at least four net-new stores per quarter was the norm since 2021.

{kind=link}

Especially overseas, Allbirds intends to rely more on channel partners to drive sales growth - which, hopefully, will reduce overhead as a percentage of revenue. Speaking to the international channel strategy on the Q2 earnings call , CEO Joey Zwillinger noted as follows:

One noteworthy example of the strength of our third party relationships is the opening of our Selfridge carbon concept pop up store in mid-July, located in a premier location in London Oxford Street, the six-week immersive experience highlights our mutual commitment to sustainability, while delivering style and comfort to their global case making shoppers. The buzz has been tremendous, bringing visibility to our brand in the UK, enhancing our credibility, and paving the way for future collaborations and partnerships.

Now onto our third pillar, transitioning our direct go-to-market strategy towards a distributor model in international markets. We believe today's announcement of our expected transition to distributors in Canada and South Korea will mark the beginning of a more profitable path to growth for the Allbirds brand in overseas markets.

We've been searching for the right partners with strong merchandising capabilities to drive the right products for the right channels. As well as the ability to connect with a local consumer, enhance brand equity and fuel customer engagement.

The goal of this strategic shift towards the distributor model is multi-faceted and is designed to position the Allbirds brand for long term and scalable growth internationally."

One of the big highlights in Q2 was gross margin, which improved 670bps y/y to 42.8%, driven by a combination of lower inventory write-downs and favorable freight and logistics costs. This, in turn, was coupled by an intentional 240bps y/y reduction in marketing costs as a percentage of revenue, as Allbirds - like many other consumer brands - has pulled back on brand awareness activity at a time that consumer demand is weak.

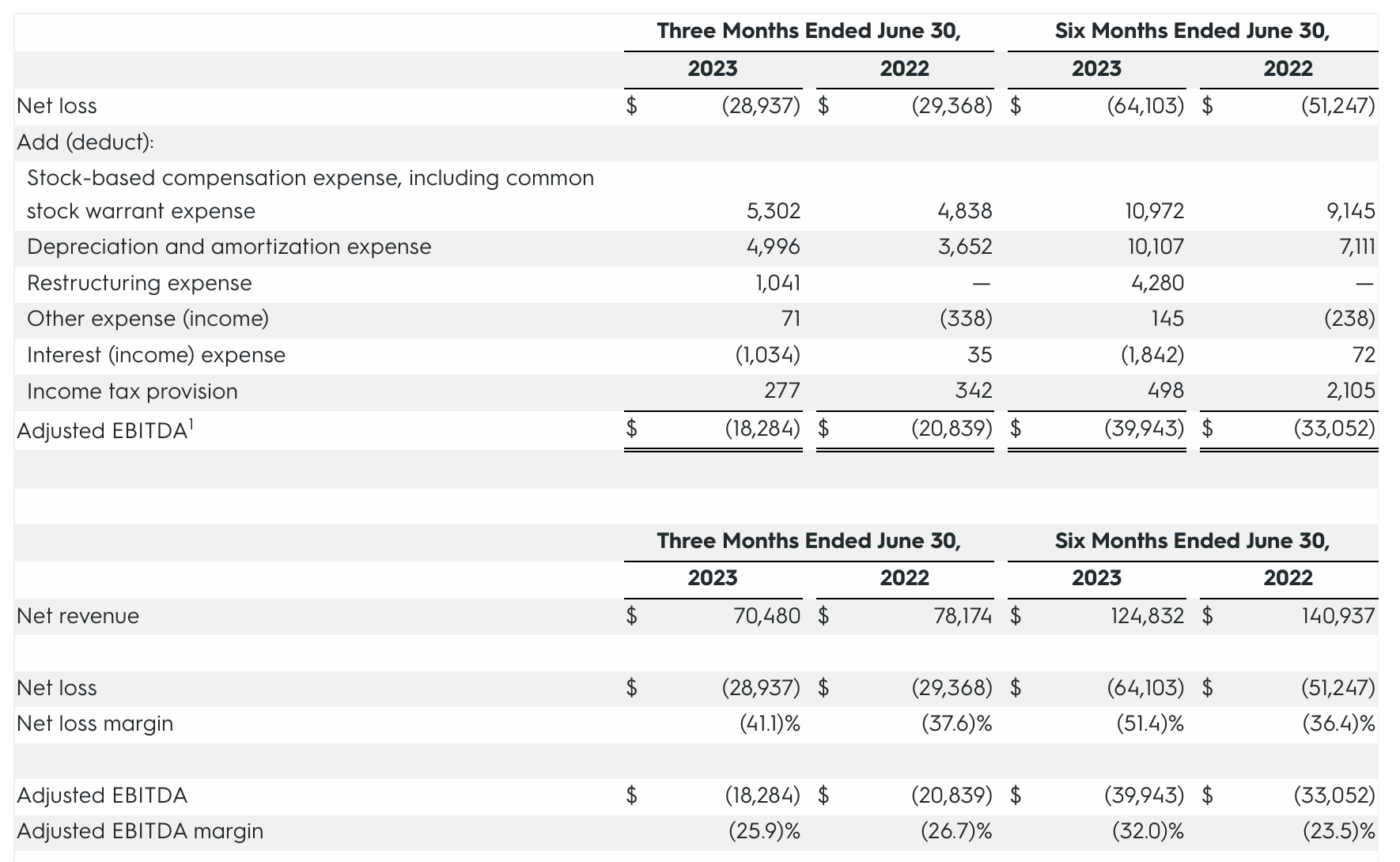

All of these gains, however, were almost fully offset by a 12-point increase in selling, general, and administrative expenses to 65.6% of revenue, all primarily associated with the higher store count this year (62 in Q2 versus 46 in the year-ago period, or a 35% increase in store fleet). Overall, adjusted EBITDA losses reduced -12% y/y to $18.3 million, but on a margin basis remained roughly flat at -25.9% (80bps better than the year-ago period).

{kind=link}

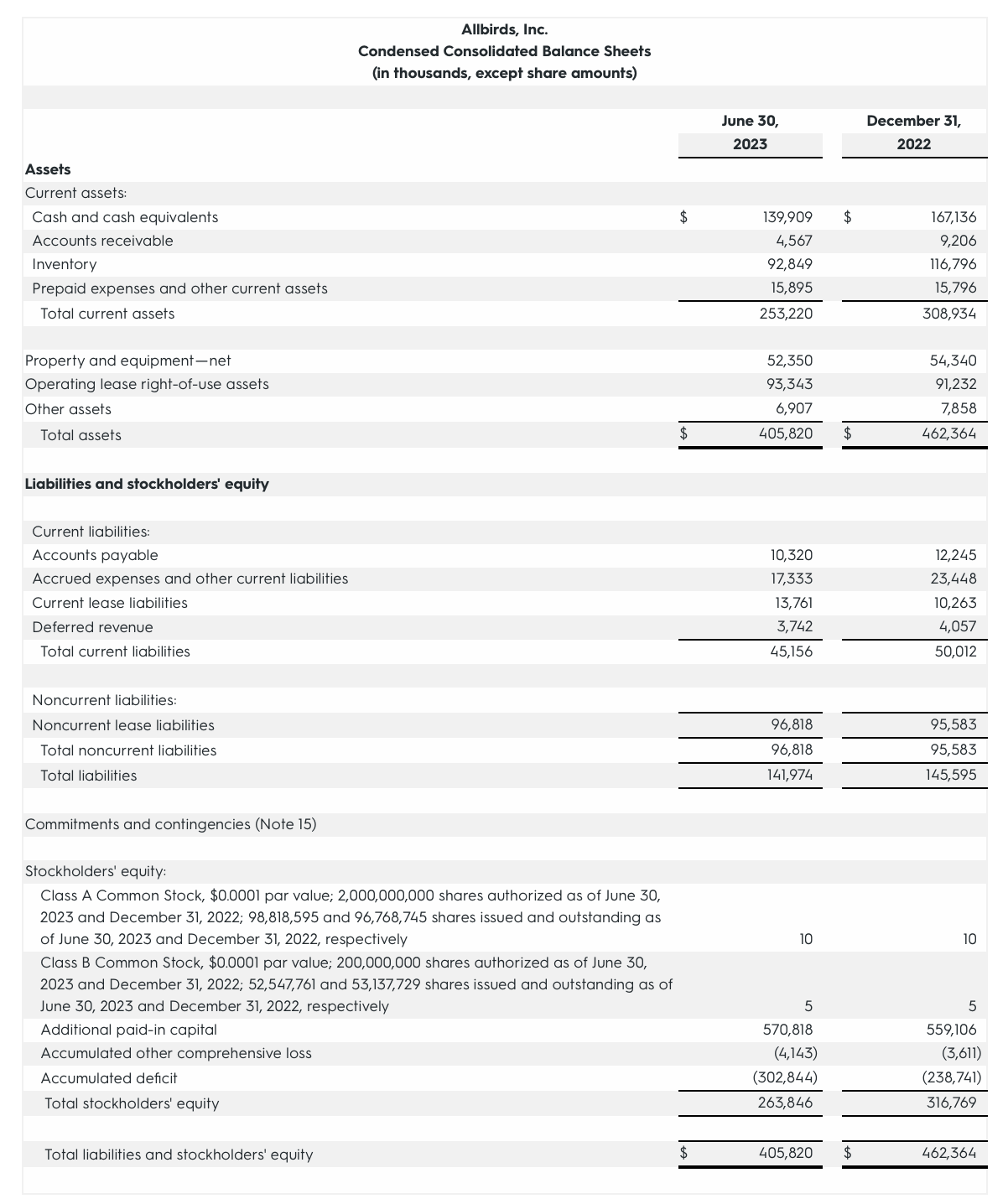

Importantly, however, YTD operating cash burn of -$20.1 million was significantly better than a -$64.6 million loss in the year-ago period, driven largely by the company's reduction in held inventory. Running the business leaner is critical at a time that Allbirds has only $140 million of cash left on its balance sheet - which, fortunately, comes unencumbered of debt.

Key takeaways

One last angle that's worth exploring here: Allbirds is trading below book value at the moment; as its Q2 balance sheet (unencumbered of debt, as just mentioned) shows $264 million of equity versus a current ~$200 million market cap (or roughly a 0.8x price to book valuation).

{kind=link}

This effectively showcases the market's lack of faith in Allbirds' profitability, and that the company's losses will eventually water down the balance sheet.

The low valuation is one of the core reasons I'm not willing to be completely bearish on Allbirds' stock price just yet, but at the same time I'll reiterate the fact that top-line trends continue to be weak: and if Allbirds can't find a way to be fashionable again, its losses will only continue to build.

For further details see:

Allbirds: Stabilizing, But Not Yet Out Of The Woods (Ratings Upgrade)