ALGT - Allegiant Travel Stock Crashes After Disastrous Buy Call

2023-12-09 06:51:29 ET

Summary

- Allegiant Travel Company's stock has lost half of its value since May 2022, despite improved performance among airlines.

- The company's most recent results show stability in revenues, but higher costs have resulted in a loss.

- Competitors adding capacity and lower pricing may challenge Allegiant's ability to maintain pricing strength, and delays in the Sunseeker resort opening pose additional challenges.

In May 2022, I put a buy rating on Allegiant Travel Company stock ( ALGT ) and admittedly that has been a disastrous call as the stock has lost half of its value ever since. It brings us to the somewhat unsettling reality that while performance among airlines has materially improved over the course of the past years, the stock prices in many instances are not reflecting it. In this report, I will be discussing the most recent results for Allegiant Travel Company and use my newly launched stock rating system to assess whether Allegiant Travel Company still deserves the previously issued buy rating.

Allegiant Travel Company Aims For Stability

{kind=link}

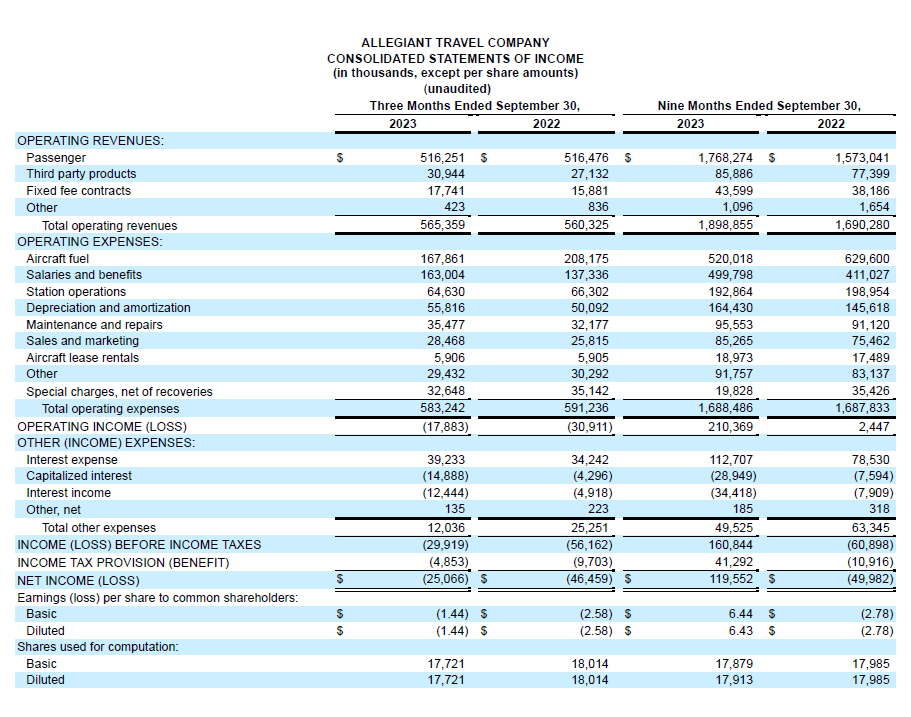

Allegiant’s most recent results show stability on revenues, with stable passenger revenues and slightly higher fixed fee contract and third party product revenues resulting in <1% revenue growth. Operating income was a $17.8 million loss, compared to a $30.9 million loss in the prior year period. What we do see is that on cost, a $40 million loss did not translate to the bottom line favorably due to roughly $25 million higher salaries and benefits, higher depreciation and amortization, maintenance and sales and marketing costs. What I think is important to point out is that whereas many other airlines are choosing to add capacity to add little to no benefit to the top line, but in an effort to reduce unit costs, Allegiant is not taking that approach.

{kind=link}

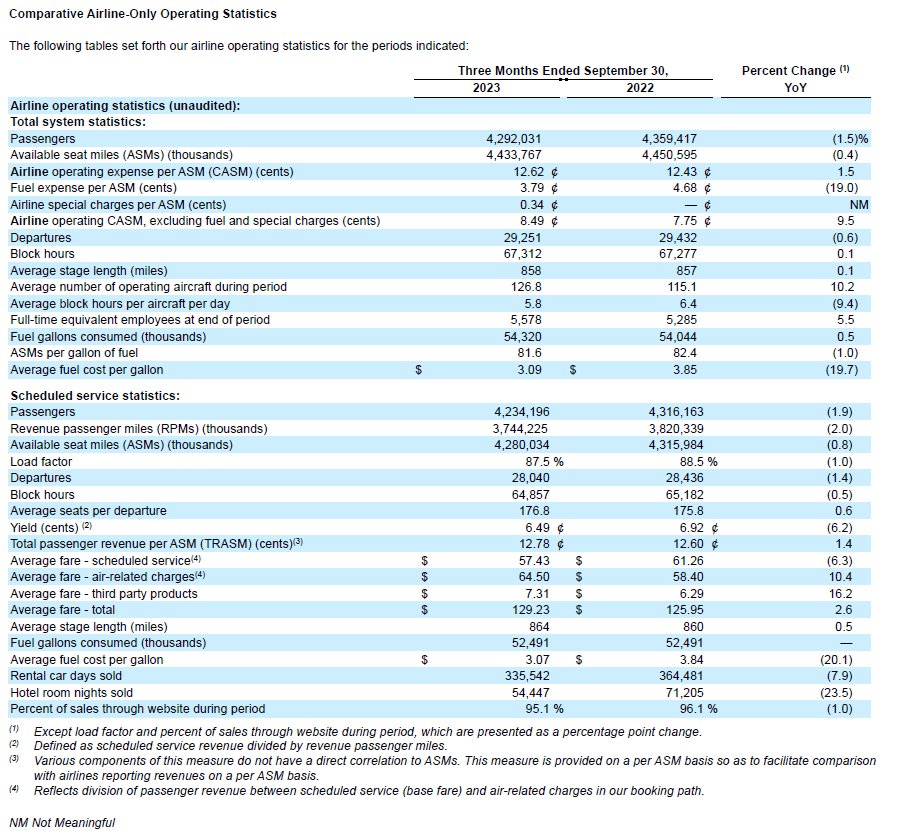

Capacity has been more or less stable, supporting slightly higher average fares. The company is actively matching its capacity and utilization with demand and that translates into stable average fares as the market is softening somewhat. As this is happening on a higher cost basis excluding fuel, the unit cost progression is not at all favorable, having grown nearly 10% year-over-year.

Allegiant Travel Company: Low Alpha Triggers Hold Rating

While I do like Allegiant’s approach towards the business matching capacity with demand instead of eroding pricing strength, I do wonder whether that will help the company. Competitors are adding capacity and forcing prices down in an effort to control unit costs, and that could ultimately hurt Allegiant’s ability to maintain pricing strength. The company is also facing normalization in seasonal effects with off-peak travel periods being softer, which provides a challenging operational environment in combination with elevated fuel prices but also somewhat supports the company’s decision to not aggressively grow capacity as this would size the company for peak periods but leave the company way too big in off-peak segments. Furthermore, the Sunseeker resort opening has been delayed by two months, which provides additional challenges for Allegiant.

{kind=link}

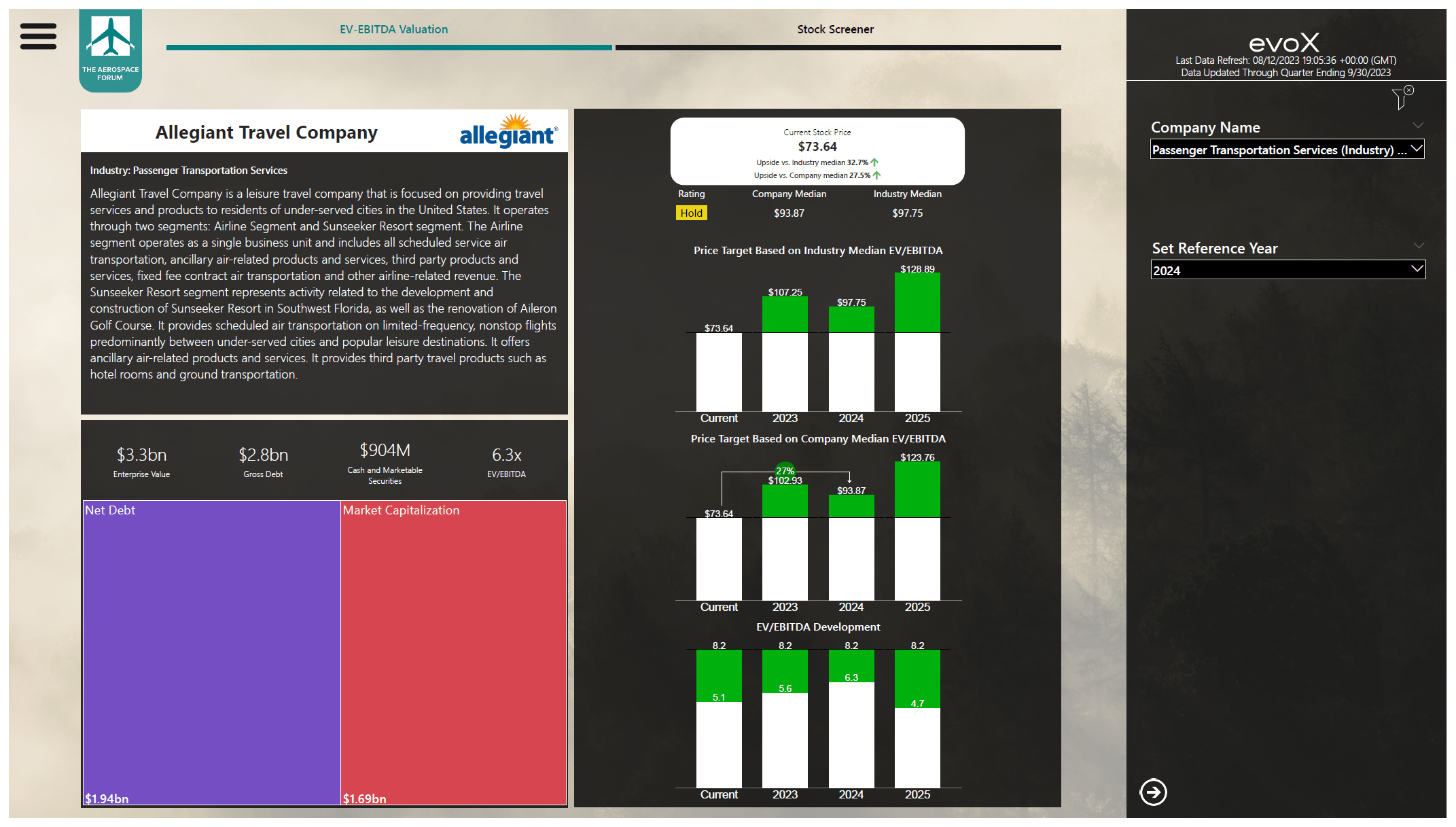

I entered the balance sheet data and forward projections for Allegiant into my stock screener and there is no doubt that there is upside, but driven by the 3-year alpha for ALGT stock, Allegiant appears to be a hold rather than a buy with 27% upside. Overall, I do like the company’s upcoming fleet renewal and capacity plan, but there are also some clear headwinds as the fleet renewal will decrease free cash flow and in my projections will require additional borrowings in 2024.

Conclusion: Allegiant Travel Company Is A Hold

I previously had a buy rating on Allegiant Travel Company stock, but after a careful review as well as the use of an automated scoring algorithm, I believe a Hold rating is better suited. I do like the fact that Allegiant is not throwing capacity on a market that is seeing unit revenues decline, but for Allegiant it also means that costs can be amortized over less seats. So, the company has to prudently navigate the current cost environment as not adding capacity to preserve pricing strength might still be challenged by competitors even though Allegiant believes it has a strong business flying from secondary cities to the sun. The Sunseeker Resort and the introduction of the Boeing 737 MAX 8 200 will be big opportunities for Allegiant, I believe, but it also comes at a cost. The Sunseeker Resort has caused $261 million in capital expenditures in 9M 2023 and $229 million in 9M 2022, and it is suffering from delays, while the Boeing 737 MAX also provides a CapEx headwind. So, I do see some long-term growth drivers, but currently they are also reason why we see pressure on free cash flow and need for additional debt increases.

For further details see:

Allegiant Travel Stock Crashes After Disastrous Buy Call