ALLE - Allegion: Capturing Demand Efficiently As Security Becomes More Important

2023-08-03 07:29:36 ET

Summary

- Allegion plc's share price has increased by around 17% this year, reflecting impressive growth and a raised guidance for 2023.

- The company's margins are improving despite rising interest rates and material costs, allowing for a decent dividend and share buybacks.

- Allegion operates in the building products industry, manufacturing and selling mechanical and electronic security products, with a focus on convenience and security.

Investment Summary

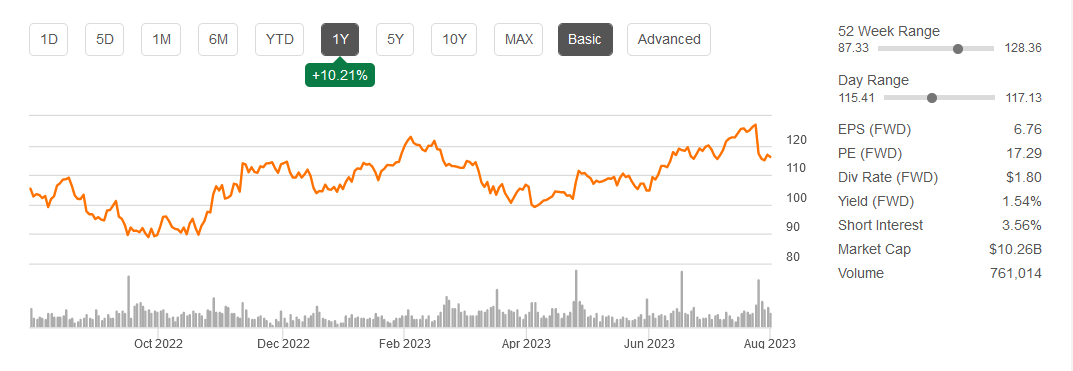

Allegion plc ( ALLE ) has had its share price increase significantly this year, up around 17%. The company is a part of the industrial sector but more specifically the building products industry. Here the company has gathered up a significant presence and has a market cap of $11 billion. Growth seems to be recovering to impressive levels which have been reflected in the rising share price. Back in late April, the Q1 report was released which resulted in a raise to the guidance for 2023. That seems to have been a strong support of the rising share price also.

With momentum set to continue many investors are looking at how margins are improving in the face of still rising interest rates and material costs. The margins right now are slightly below the historical margins, but they are by no means disappointing, quite the opposite. The net margins are at 14% and FCF margins are at nearly 9%. This has led ALLE able to have a decent dividend and buyback share at a strong rate. Going forward there seems to be a lot of positive and I am rating ALLE a buy as a result.

Catalyst

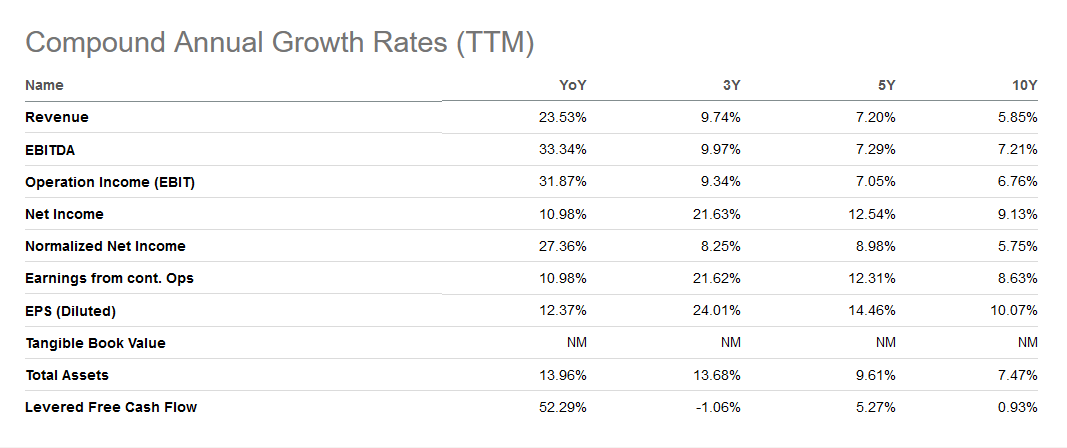

The company was founded back in 2013 so it's still quite new, but the impressive growth it has had so far hasn't landed it an outrageous valuation. During the last 10 years, the EPS has grown 9.6% CAGR which is a key indicator to look at since it's not only supported by stronger sales but also by buybacks from the company.

Apart from the building products industry, the company revenues can be slightly volatile and fluctuate between market demand and the cycles of it. In times of high growth, they pass on earnings to shareholders.

As for what the company does, it circles manufacturing and selling mechanical and electronic security products. These products and solutions include door controls and systems for exit devices like locks and portable locks. Some of the more service-related offerings include time and attendance but also workforce productivity systems. These help companies have security for their facilities and a broad hawkeye view of operations.

{kind=link}

Company Profile (Investor Presentation)

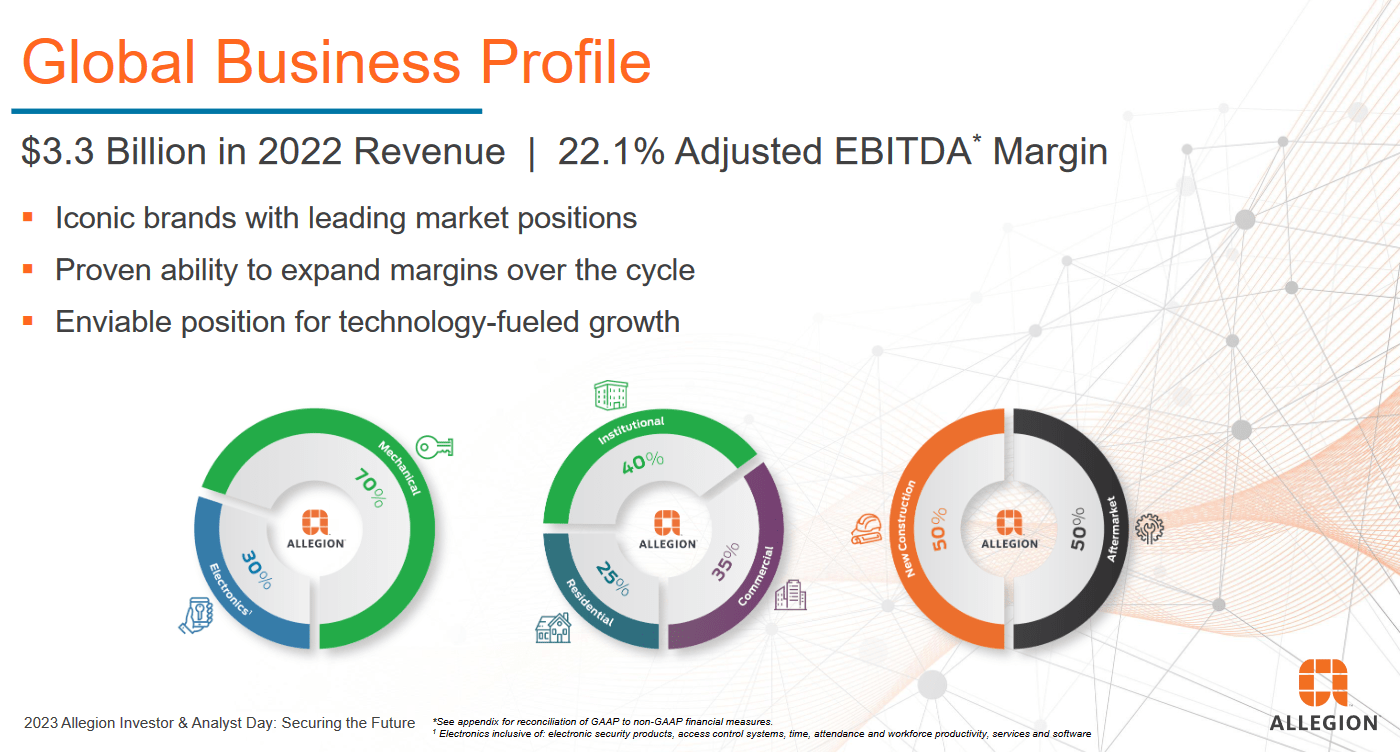

ALLE has grown its operations to an international level and has its headquarters in Dublin Ireland. As far as the revenue mix it's not that diverse, basically put into either mechanical or electronics. The first part is where most revenues come from. The TAM that ALLE has access to is valued at $40 billion and includes end markets like non-residential mechanical and non-residential electronics & software. The last mentioned set to grow at high single digits yearly. The pushing forces behind this growth come as more and more companies want to create seamless operations where convenience and security are prioritized.

Capital Allocations (Investor Presentation)

The capital allocations for ALLE have long been to benefit shareholders in balance with fueling more growth. The company has a quite decent dividend yield at 1.42%. As for share buybacks, the company spent $61 million in 2022 buying shares, but in 2022 it was $412 million. The share price for 2022 was quite high and with more growth ahead I think the management would do well in buying back more aggressively to appease investors.

{kind=link}

Company Growth (Seeking Alpha)

Looking at the historical growth of the business the revenues and the cash flows have been very solid, both growing impressively over the last 10 years. Going forward I think that as the market becomes less tense and building projects start once again the demand will grow and ALLE can leverage this to grow FCF at a similar rate. Going forward I dont see it as unreasonable for the FCF to grow around 10% annually. Going into the coming months and quarters I think that growth in the share price will come from positive news about material costs in the industry. But also if interest rates are on the decline, that could generate strong demand and lead to ALLE experiencing revenue growth at a fast pace. This would translate to a higher share price and a higher multiple to reflect the growth projections.

Management Comments

In the last report from the company there were some comments from the CEO John Stone that caught my attention.

"Our vision of enabling seamless access in a safer world. What does that mean? It means if you have the right credentials, whether that's a metal key, an encrypted proximity card, or a digital identity in a mobile wallet, we will provide you the most convenient and secure experience possible".

The focus on providing the market with a superior product is making ALLE out to be a growth opportunity here. The management is keen on achieving a comapny profile that can be correlated with quality and reliability. This I think is what will drive growth for ALLE as reputation in the business is incredibly important to drive more customer acquisitions.

Looking at some peers for ALLE I think it trades at an appealing valuation. In comparison to A. O. Smith Corporation ( AOS ) which is in the same industry the valuation of ALLE is lower at a p/e of around 18 and p/FCF of 16. Compared to AOS it's trading at a discount and I think this offers investors less immediate risk for an investment. But in comparison to the sector, ALLE is also looking appealing. The p/e is 5% below the sector and as I think eventual returns of demand in the industry will bring higher earnings this seems like a decent time to get in. Profit margins are also impressively above the sector, with the FCF margin at 90% above the sector and the ROC at 14.2% compared to the sector at 7%. This paints the picture that ALLE can handle some headwinds without it resulting in detrimental margins. The business model is robust and this clearly showcases that.

Risks

The remarkable surge in revenue and EPS growth for the company can be attributed to multiple factors, chiefly driven by robust demand in its North American non-residential business and the increasing global demand for its electronics solutions. The company's ability to capitalize on these thriving markets has been instrumental in bolstering its financial performance.

Furthermore, the company's focus on enhancing its cash flows and EPS stems from the solid market demand it experiences in its non-residential sectors, where it continues to witness steady growth. Additionally, the improved supply of electronic components and favorable pricing dynamics have contributed significantly to the company's positive financial outlook.

But where the risks are arising is a potentially slowing construction market in the US could see and are seeing signs of already. Rising interest rates make it less incentivizing to begin large projects are debt isn't as cheap as it used to be before. Companies need to factor in far higher costs these days. This is reducing the customer pool that ALLE has access to and will most likely result in slowing growth. Keynotes to watch for here is is volumes and prices. We have so far seen a steady increase here which displays the current market environment as full of demand and still able to digest higher prices from companies like ALLE.

Valuation & Wrap Up

Investors that want to have some exposure to residential markets but don’t want to be in companies filled with debt and highly leveraged may want to look into ALLE. Operating as a security company of sorts, offering locks and security systems to individuals but also for commercial applications. They have been growing steadily as the construction market has been booming. As more houses are being built, more security systems are needed.

{kind=link}

Stock Price (Seeking Alpha)

The valuation of the company is quite decent and the p/e sits at just under 19. This seems like a good price to get in at. The company has been displaying a good ability to pass down costs and deliver results even in a higher interest rate environment. The p/e sits below the 5-year average and is in line with the materials sector. I think investors can reasonably expect a decent 7 - 9% yearly return from here on out as ALLE continues to scale and return earnings to shareholders.

For further details see:

Allegion: Capturing Demand Efficiently As Security Becomes More Important