ALLE - Allegion: Expecting Growth In A Weak Economy

2023-04-30 09:30:51 ET

Summary

- Allegion's optimistic growth projection for 2023 may face headwinds due to a fast-deteriorating economy.

- The stock looks overvalued based on valuation metrics.

- The low dividend yield is another reason to avoid the stock.

Allegion ( ALLE ) has shown resilient growth in the face of increasing economic headwinds. The company is optimistic about growing its organic revenues by mid-single-digit in 2023. But the economy is likely to deteriorate further, which may pressure the company’s growth and cash flow margins. The market is overvaluing Allegion, leaving the company no room for error in the execution of its growth strategy.

Allegion's Growth May Face Headwinds.

Allegion handily beat its Q1 2023 earnings estimates by a wide margin. The company booked revenue of $923 million, which was $76.7 million above expectations, and its GAAP EPS was $1.40, which beat expectations by $0.12. The company’s revenue growth was 27% in Q1, primarily driven by acquisitions. The company raised its revenue and earnings estimates for the rest of the year. It now expects organic revenue growth to range between 5.5% and 7.5% and EPS to range between $5.95 and $6.15. The company has beaten EPS estimates in the past four quarters.

The company credited this substantial revenue and EPS growth to robust demand in its North American non-residential business and strong global demand for its electronics solutions. The company credits its improving cashflows and EPS to solid market demand in its non-residential markets, improving the supply of electronic components and strong pricing. The company also sees the security and access control demand transition to smart electronic hardware, driving revenue growth.

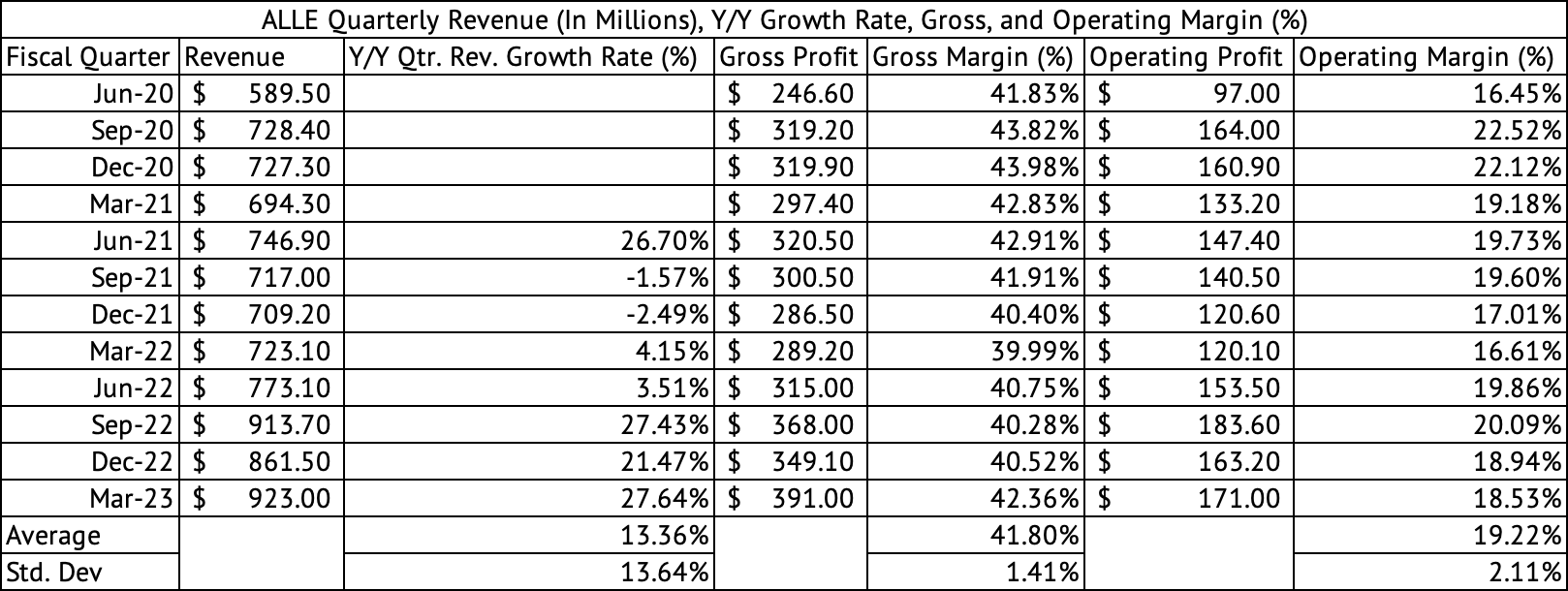

Since June 2020, the company has increased its revenue by 56%, primarily driven by acquisitions (Exhibit 1) . The company is on the brink of $1 billion in quarterly revenue, having booked $923 million in Q1 2023 (ended March 2023).

Exhibit 1:

Allegion Quarterly Revenue, Gross, Operating Profits, and Margins (%) (Seeking Alpha, Author Compilation)

{kind=link}

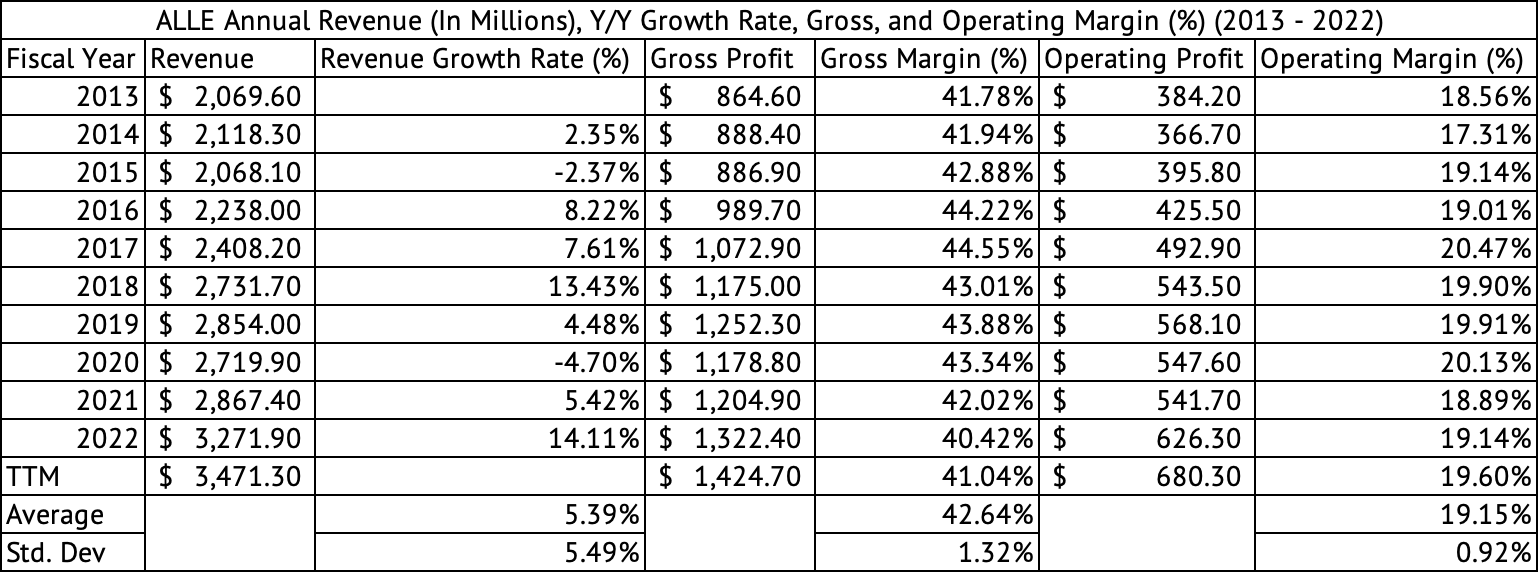

Exhibit 2:

Allegion Annual Revenue, Gross, Operating Profits, and Margins (%) (Seeking Alpha, Author Compilation)

{kind=link}

The company’s average quarterly gross margins have been 41.8% since June 2020 compared to its annual average of 42.6% over the past decade (Exhibits 1 & 2). But improving supply chains, robust demand, lower inflation, and higher pricing have helped the company improve its gross margins closer to its annual average in March 2023. The company’s GAAP gross margins improved by 184 basis points in Q1 2023 compared to Q4 2022.

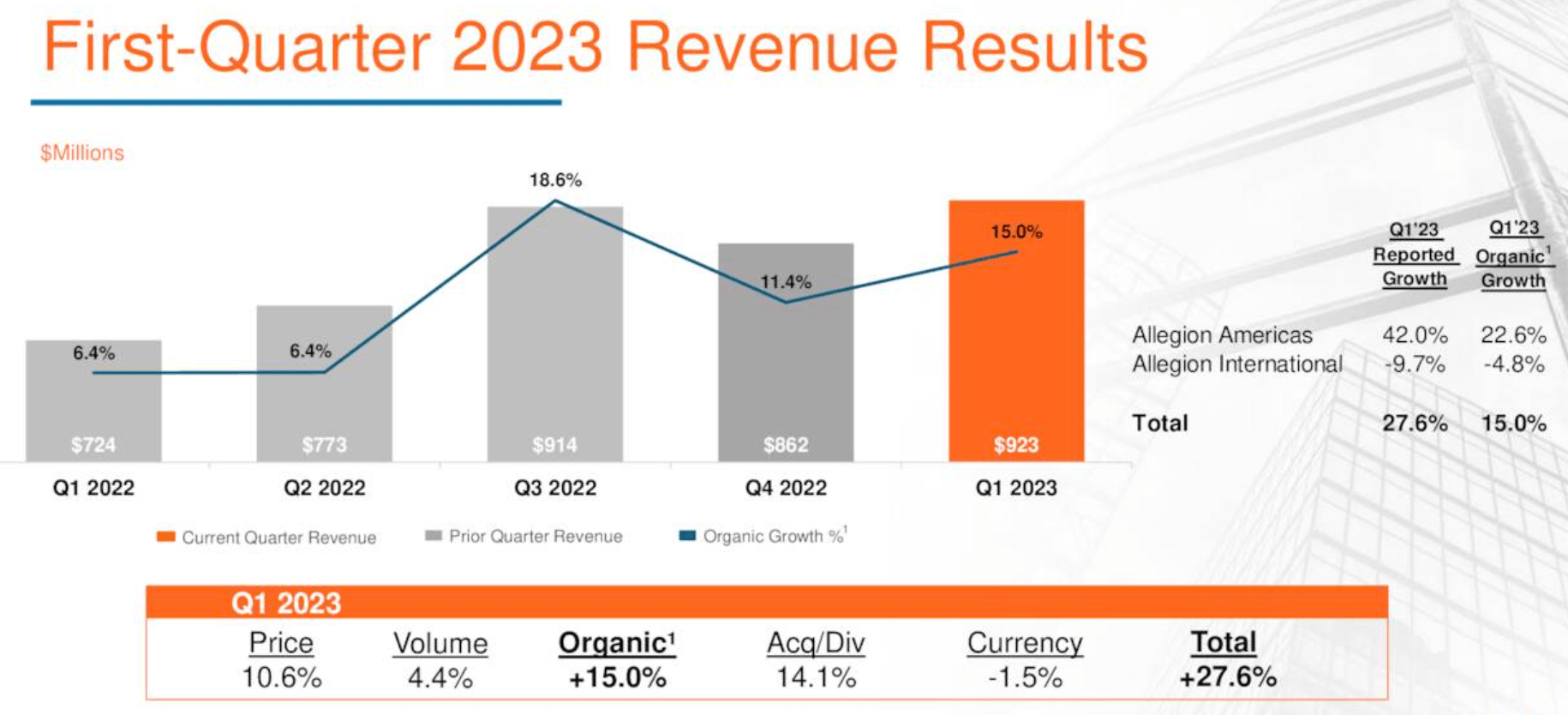

Over the past year, I have been surprised by the pricing power of many companies in the industrial and consumer staples sectors. Most companies have seen volumes decline in the face of double-digit price increases, but price elasticities were lower than what even the management had anticipated. In Allegion’s case, the company’s volumes increased by 4.4% in the face of a 10.6% price increase (Exhibit 3) . But the company’s growth was driven by its America segment , which grew revenues by 42%, while its International segment saw a nearly 10% decline in revenue and substantial erosion of margins.

Exhibit 3:

Allegion First Quarter 2023 Revenue Results (Allegion Investor Presentation)

{kind=link}

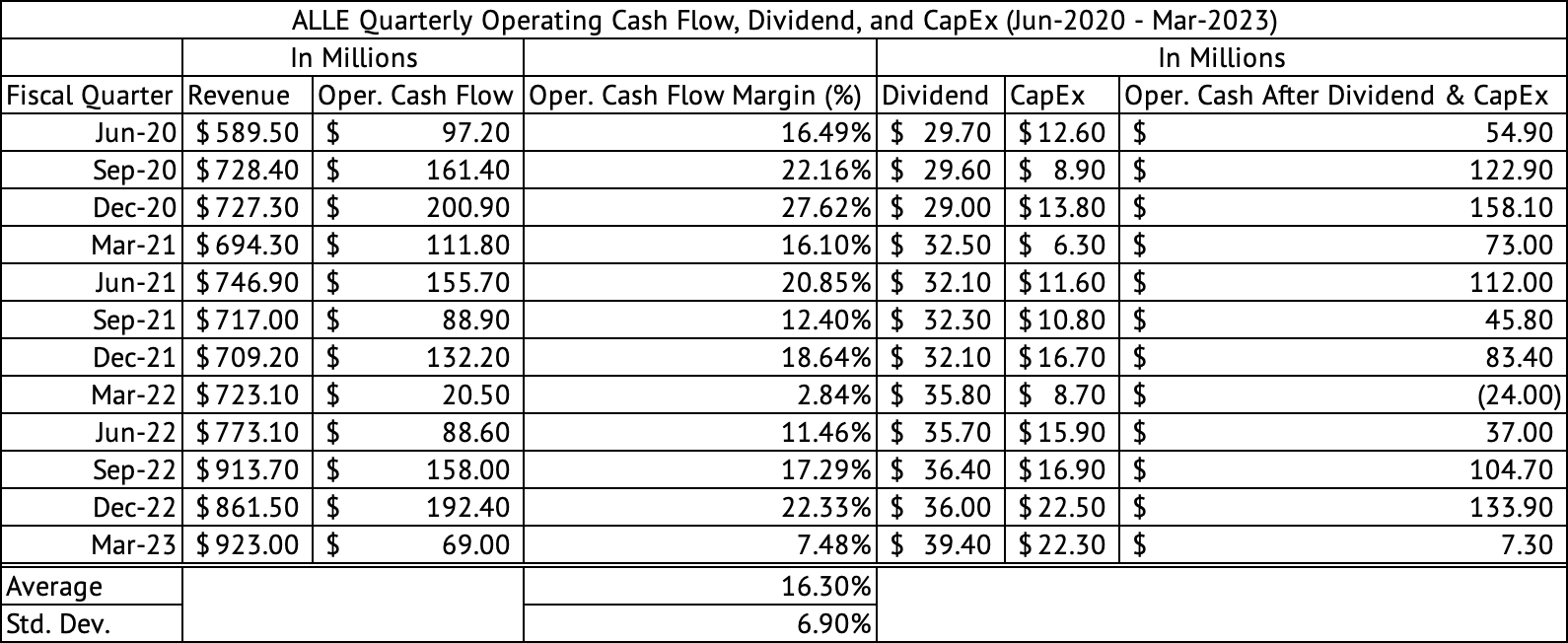

Cash Flows Take A Hit Due To High Inventory.

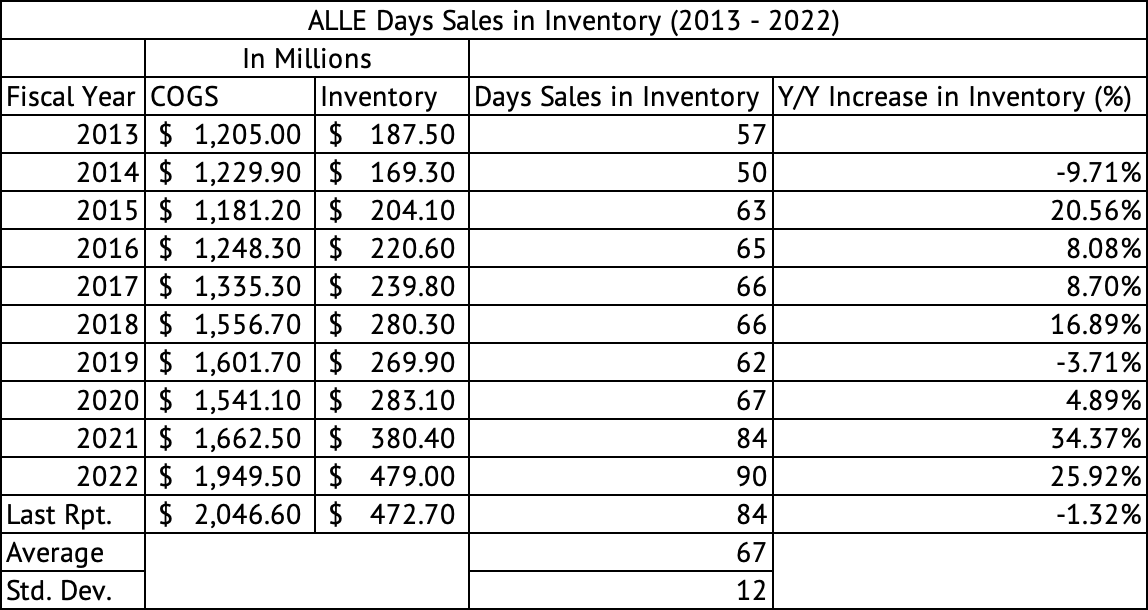

Although the company booked record revenues and cash flows, its operating cash flow was weak due to increased inventory driven by increased safety stock. Its quarterly operating cash flow and margin were $69 million and 7.4%, respectively (Exhibit 4) . The company has averaged 16.3% in operating cash flow margin since June 2020. The company’s elevated inventory levels contributed to declining operating cash flows. The company carried 84 days of inventory at the end of its March quarter, compared to its average of 67 days over the past decade (Exhibit 5) . The inventory levels are beginning to decline compared to the end of 2022. This declining inventory should lead to better cash flow generation in the rest of 2023.

Exhibit 4:

Allegion Operating Cash Flow (Seeking Alpha, Author Calculations)

{kind=link}

Exhibit 5:

Allegion Day's Sales in Inventory (Seeking Alpha, Author Calculations)

{kind=link}

The company hopes to attain its projected growth targets for 2023. Although the company is optimistic that it will achieve its growth targets for the year, it faces multiplying headwinds. Its International segment was weak, and demand may continue to soften. Commercial real estate is under much pressure in North America and can weaken further if the unemployment rates rise. The commercial real estate market segment is seeing higher vacancy rates pressuring rents, while the cost of capital for these companies has increased exponentially. Any decline in its growth could slow its inventory levels and leave the company with lower cash flows than anticipated.

High Valuation

The company’s current valuation has no buffer for any uncertainty that could negatively affect its business in 2023. The stock trades at a forward GAAP PE of 17.6 and a PEG ratio of 3.2x, a high multiple. It trades at a forward EV to EBITDA multiple of 13.5x, compared to the sector median of 10.4x. A reasonable valuation for the stock would be close to 10x EV to EBITDA multiple. A 10x EV to EBITDA multiple will put the stock around $90. It may be no coincidence that the stock’s 52-week low was $87.33. The valuation metrics seem to indicate that the stock is overvalued.

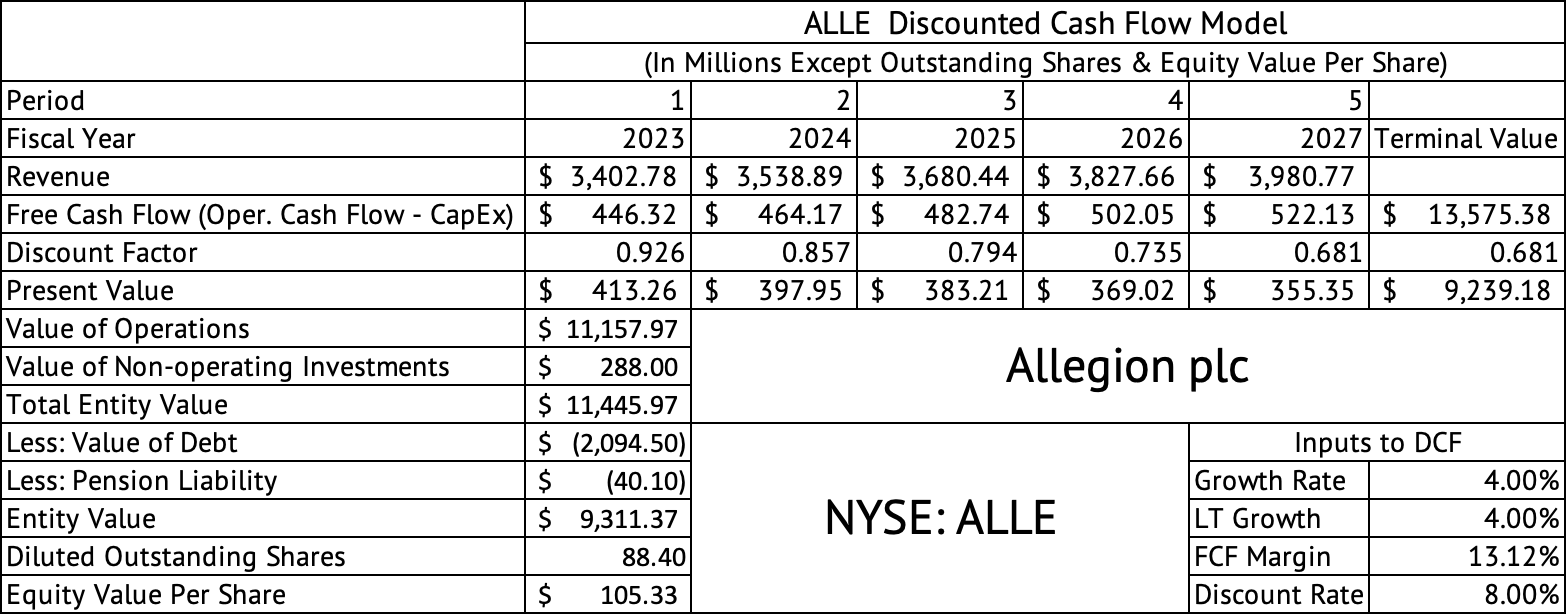

A discounted cash flow model estimates the per-share equity value at $105 (Exhibit 6) . This model assumes a revenue growth rate of 4%, a free cash flow margin of 13%, and a discount rate of 8%. These model assumptions are reasonable for the company. The company carries a debt-to-EBITDA ratio of 2.5x, not an excessive debt level.

Exhibit 6:

Allegion Discounted Cash Flow Model (Seeking Alpha, Author Calculations)

{kind=link}

This model assumes a lower revenue for 2023 of $3.4 billion, compared to a consensus estimate of $3.69 billion. If the model is based on $3.69 billion in revenue in 2023, the per-share equity value is $115, about 4% above its current price of $110.48. The company’s projected higher growth rate may be unsustainable over the long term, so a 4% assumption may be reasonable. The U.S. economy grew by just 1.1% in Q1 and is expected to optimistically grow at less than a 4% pace for the rest of the decade . A 4% growth rate would have the company growing faster than the GDP. Investors must have a margin of safety in valuing any stock, and Allegion is no exception. The stock is fully valued now, and investors may consider investing in it if it returns to the mid-nineties.

Low Dividend, Poor Buybacks, But Excellent Dividend Growth.

The stock yields a dividend of 1.6% , low compared to the yields available on U.S. Treasuries. The company has a conservative payout ratio of 27% and has grown its dividend by 19% over the past five years, an excellent growth rate. The company has spent $588 million on share buybacks since September 2020, reducing its share count by 4.3 million at an effective buyback price of $136 (Source: Seeking Alpha, Author Calculations) . The company may have overpaid for its buybacks, considering its intrinsic value is closer to $90 per share.

Economic growth is decelerating globally, with the latest U.S. GDP growth spotlighting a dramatic slowdown. The stock market’s volatility, as measured by the S&P VIX Index ( VIX ), is at 15.7, showing complacency. These market conditions can change on a dime. Long-term investors looking to buy Allegion may be left with regret if they purchase Allegion at current prices. A further slowdown in the U.S. economy and increased volatility may present a better opportunity to acquire this stock at a lower valuation.

For further details see:

Allegion: Expecting Growth In A Weak Economy