VVNT - Allegion: Security And Earnings Growth As Operations Improve

Summary

- Allegion continued growth during Q2 with revenue increasing by 3.5% and the completion of the Access Technologies acquisition from SWK.

- Inventory remains high, but pricing has shown improvements though the International segment remains challenging, particularly with the outlook for slowing economic growth in Europe.

- Allegion appears to be slightly overvalued compared to peers, but the improvements made and potential for future earnings growth make this a Buy at the current prices.

My rating for Allegion PLC ( ALLE ) is a Buy. In this article, I will explain their recent successes, some areas to watch carefully, and provide insight into future growth and their capital allocation choices.

Allegion is a spin-off from Ingersoll-Rand (IR) in 2013 and is now a leader in security products. They remain a well-recognized and prominent player in the building products industry. Their portfolio of brands includes LCN, von Duprin, CISA, Interflex, and Schlage. While they have a strong international focus, about two-thirds of their business remains U.S. based. Their solutions include locks, controls, key systems, electronic security systems, access systems, and other security management accessories. They serve commercial, institutional, and residential facilities using a range of channels such as specialty distributors, e-commerce, wholesalers, and home improvement stores.

Earlier this year, I would have rated Allegion as a Hold. However, the recent weakness in price and the continued operational performance within this environment suggests we are now at a point where investors should buy. Further, the continued effectiveness of capital allocation remains attractive.

There are a lot of things to like about Allegion and its management. They have a strong emphasis on operational effectiveness and efficiency. Since 2015, the ROIC (return on invested capital) has been between 16% and 23% at a consistent level. This suggests careful use of capital to enhance returns and the ROIC is in the upper quartile of the security and protection services industry.

They have a 40.8% gross profit margin and a reasonable 0.9x asset turnover rate (Source: Finbox).

Recent results and challenges

There are several points that I am watching carefully.

First, Allegion appears to have declining rates of sales growth over the last few years. Their five-year average sales growth was 4.7%, their three-year sales growth was 1.4%, and their one-year growth was only 0.9%. Analysts' expectations are for reasonable growth moving forward, with expectations of $3,238 million in sales for 2022 growing to $3,729 million in 2024. However, Q2 revenue was up 3.5% on a reported basis.

Second, the EPS (normalized) growth at Allegion has been lower in recent years. After recording double-digit growth in 2016 through 2018, it has slipped to lower single-digit growth in 2020 and this looks set to continue in 2022. However, analyst expectations are for a resumption of normalized EPS growth of single digits in 2023 through 2025. We return to this point later when looking at the future prospects for investment in Allegion.

Third, there is an expected economic slowdown in Europe, with the IMF suggesting a reduction of GDP growth by 1 percentage point against their January projections, which represents a significant component of Allegion's International market, which is about a quarter of their revenue. In particular, the IMF expects Germany to see only 1.2% GDP growth in 2022. This will impact Allegion's EPS growth in 2023 and 2024.

Fourth, they have been continued to be impacted by supply chain problems. However, their earlier initiatives which they note on the Q2 earnings call :

have resulted in improving component availability for mechanical products. Electronic component challenges continue, however the product redesigns and alternative sourcing actions we have taken set us up better for the remainder of the year and 2023.

While many firms have increased inventory levels in an effort to improve resilience and ensure availability, this is expensive and Allegion has experienced a run-up in inventories as they grapple with the unprecedented supply chain issues (Figure 1). As Allegion executives note in the Q2 earnings call, holding this inventory "will position us to manage backlogs, which are expected to be elevated entering 2023 due to strong non-residential demand." It's easy to say that, but inventory backlogs can also be painful to reduce. However, they noted that component availability is improving.

Figure 1. Inventory increases at Allegion

Fifth, there have been difficulties in the Allegion International segment. Allegion noted a 8.5% decline in revenue in Q2, driven by currency movements, but balanced by a 1.9% increase on an organic basis. However, the International segment also faced adjusted operating margins decreasing by 100 basis points. They did note in the Q2 investor presentation that the segment's price realization was 5.5%, demonstrating their commitment to improving the pricing issues that were identified as a weakness earlier.

One bright point coming from Q2 results is that Allegion has been able to improve the pricing situation in the Americas segment in both non-residential and residential businesses showing strong pricing. Together, the pricing and volume growth propelled the non-residential business to strong growth for the quarter, with revenue of $592.3 million compared to $549.4 million in Q2 2021.

Peer comparisons

For a comparison with peers, I've used those focused on safety and security solutions, the core of Allegion's business. The following are reasonable comparisons, I believe:

- The Brink's Company ( BCO )

- Brady Corporation ( BRC )

- Fortune Brands Home & Security, Inc. ( FBHS )

- MSA Safety Incorporated ( MSA )

- Napco Security Technologies, Inc. ( NSSC )

- Resideo Technologies, Inc. ( REZI )

- Vivint Smart Home, Inc. ( VVNT )

I make the comparison over EV/EBITDA, Price/Book, and Price/Sales. In each case, Allegion looks slightly more expensive than its peers.

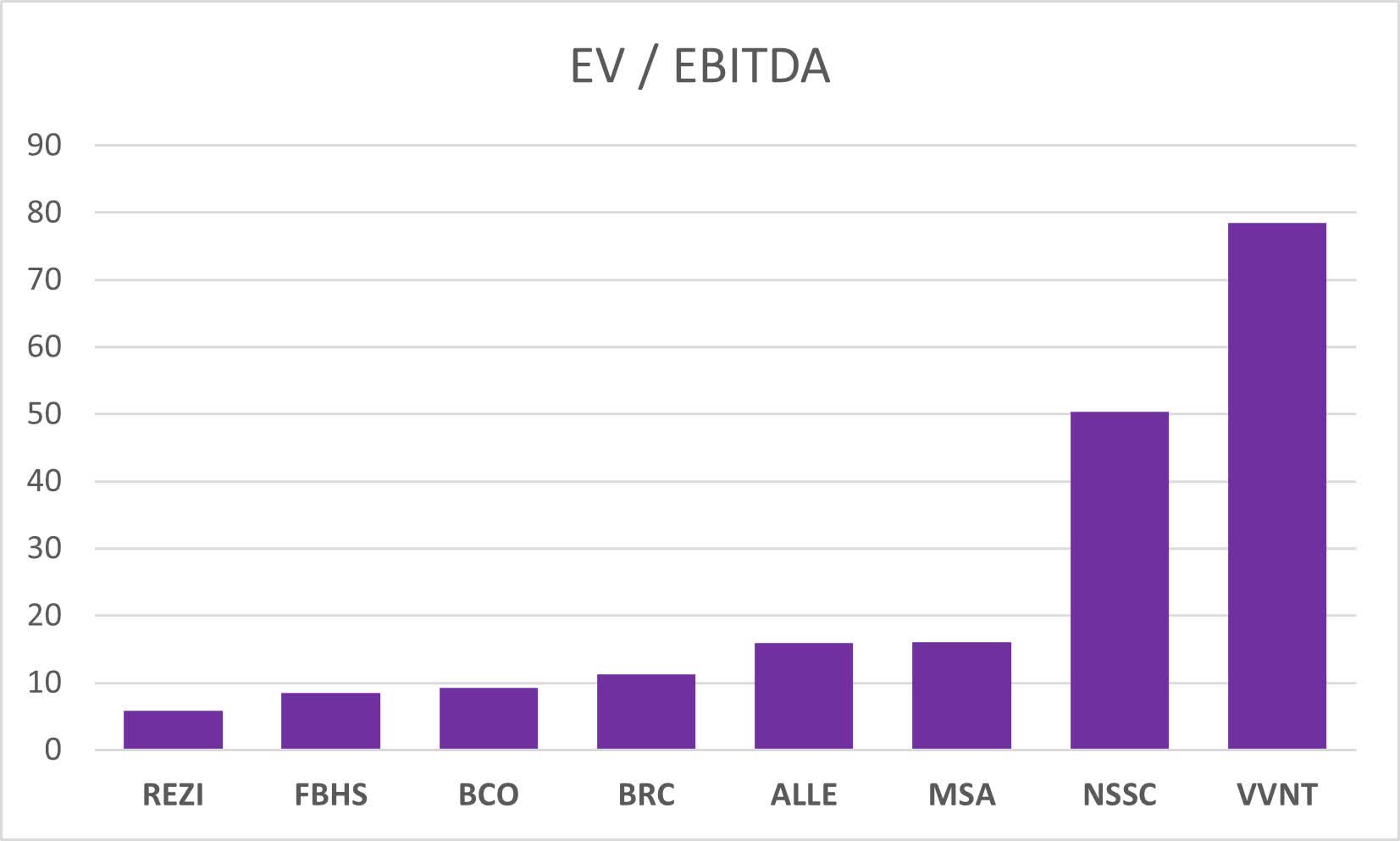

Figure 2. ALLE comparison with peers in terms of EV to EBITDA (Finbox.io)

{kind=link}

When we first consider the EV to EBITDA values, Allegion appears overvalued with the exception of NSSC and VVNT, which are substantial outliers (Figure 2).

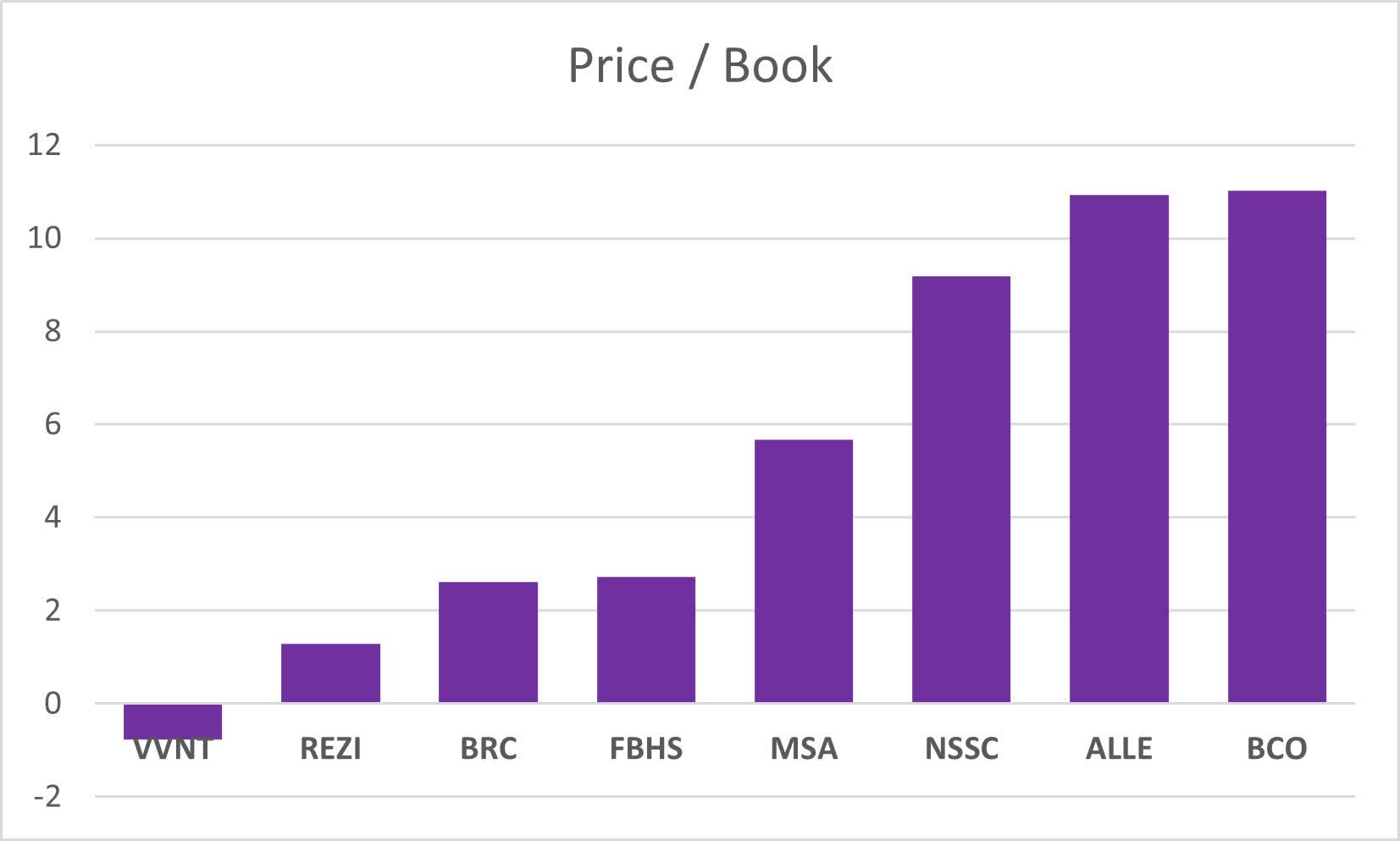

Figure 3. ALLE comparison to peers in terms of Price to Book ratio (Finbox.io)

{kind=link}

With respect to the P/B ratio, Allegion appears as a richly valued company, relative to the book value it holds. It is essentially the equal-highest in terms of the P/B ratio (Figure 3).

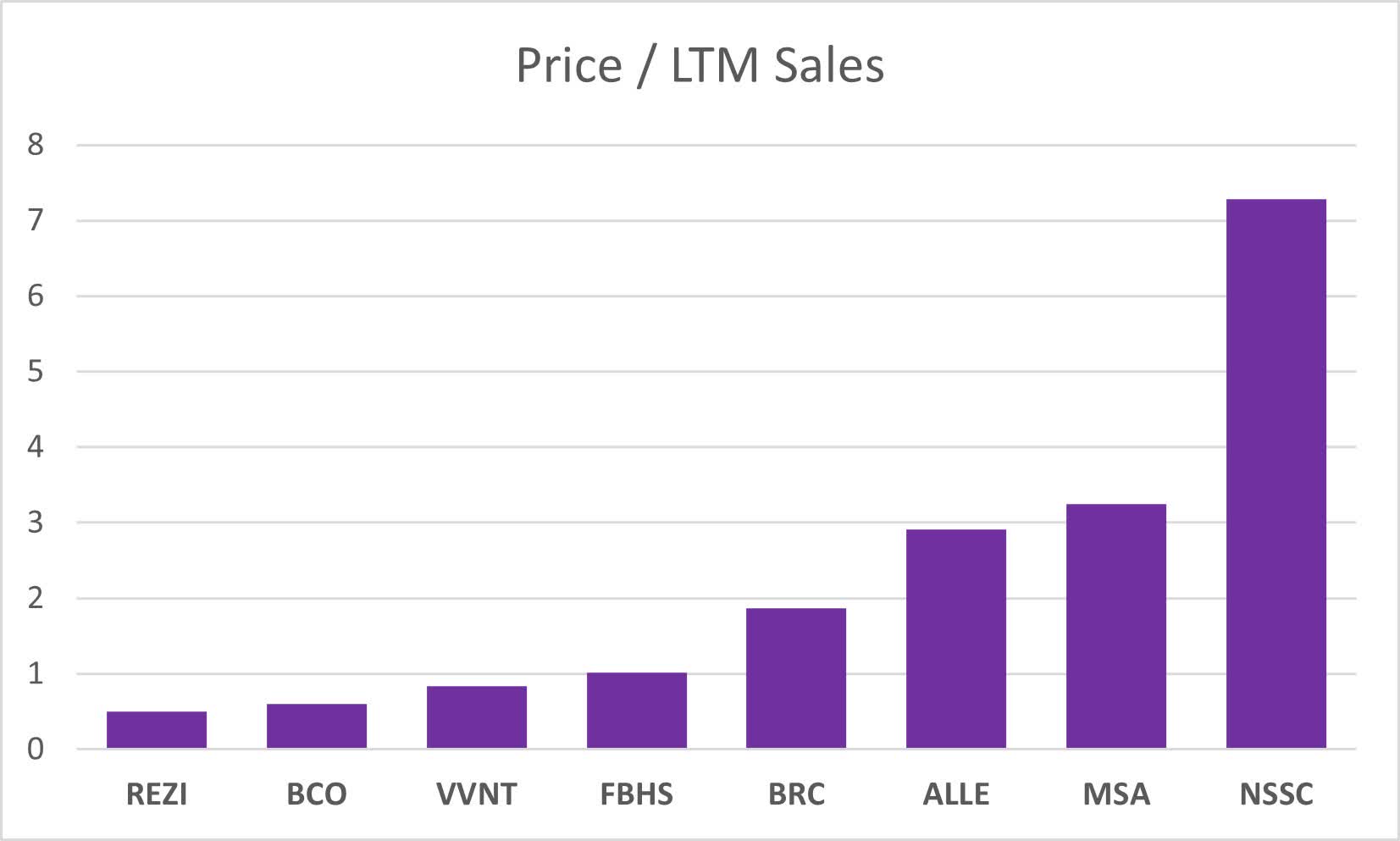

Figure 4. ALLE comparison to peers, Price to Sales ratio (Finbox.io)

{kind=link}

Finally, in comparison to peers in terms of the Price/Sales (LTM) ratio, Allegion again appears on the more expensive end of the chart with, again, NSSC appearing as an outlier (Figure 4).

Together, I think this paints a picture of Allegion as priced slightly higher than the peers. Allegion appears on the higher end of each of the comparisons made.

Capital allocation appears mixed

Allegion continues to balance its investments in the continued growth of its business and its efforts to return capital to shareholders.

In July, Allegion completed the purchase of the automatic doors business ("access technologies") from Stanley Black & Decker ( SWK ), paying $900 million in cash. This is a good fit with Allegion's focus on security operations and generated approximately $340 million in revenue in 2021. However, this implies a 12.5x (including synergies) 2022 estimated EBITDA multiple, which seems to be a high price to pay. I acknowledge that this acquisition extends service revenue opportunities and strengthens Allegion's distribution, service, and support network and they may benefit from this in the long-run, but it seems an expensive acquisition in the near-term.

Allegion has also allocated capital to share repurchases (Figure 5). Given the relatively higher prices during the period of higher buybacks, from 2019 onwards, and the current peer comparisons suggesting that Allegion is richly priced relative to peers (Figures 2-4), and this does not appear to be effective capital allocation, given the EV/EBITDA during this period was over 20x for quite some time while the P/E ratio was well past 30x. The buybacks appear to have continued in late 2021 and early 2022 at lower multiples, as the shares are less richly valued.

Figure 5. ALLE share buybacks with higher levels in 2019 onwards, positioned against the EV/EBITDA and P/E ratios

However, Allegion appears to be effective at maintaining an effective ROIC ratio. Allegion's 17.71% ROIC (Figure 6) puts them as the leader of the pack of their peers used earlier in this comparison. I believe this puts Allegion high in the upper quartile for the Security and Protection Services industry, suggesting a level of effectiveness. However, Figure 6 also demonstrates the deterioration in the gross profit margin and slight weakening of the operating margin, which are issues we will continue to monitor.

Figure 6. ROIC and margins for ALLE

Allegion has continued to provide its strong support capital return, with the current yield of 1.7% complemented by a jump from $0.36/share in 2021 to $0.41 in 2022. This raise contributes to a five-year dividend CAGR of 20.7% for ALLE. The track record length is not as impressive as other firms but looks to be of growing importance to the company.

Valuation and investment prospects

As I note, there are several areas for concern when considering Allegion. I note that analysts have a price target average of $119, suggesting some good upside. However, I consider this to be somewhat optimistic, even with Allegion's improvements regarding previous issues of pricing. If I look at the analyst scorecard on FAST Graphs, it suggests a perfect record of two-year forward estimates (20% margin of error) and 75% meet and 25% beat on the one-year forward estimates (10% margin of error). I take this with the fact that Allegion is a recent spinoff and so there is not a significant track record here.

I've been relatively conservative. While the analyst scorecard suggests that they have a good handle on Allegion's prospects, my earlier notes suggest Allegion remains slightly overvalued, lessening the likelihood of being able to participate in the returns as the company earnings grow. As a consequence, to assess the likely future returns at the end of 2024, I've taken the analyst expectations of earnings and used a 15x P/E multiple as a conservative multiple. This is below the current 18.3x and the five-year 21.8x P/E multiple. As such, I think this strikes a reasonable balance.

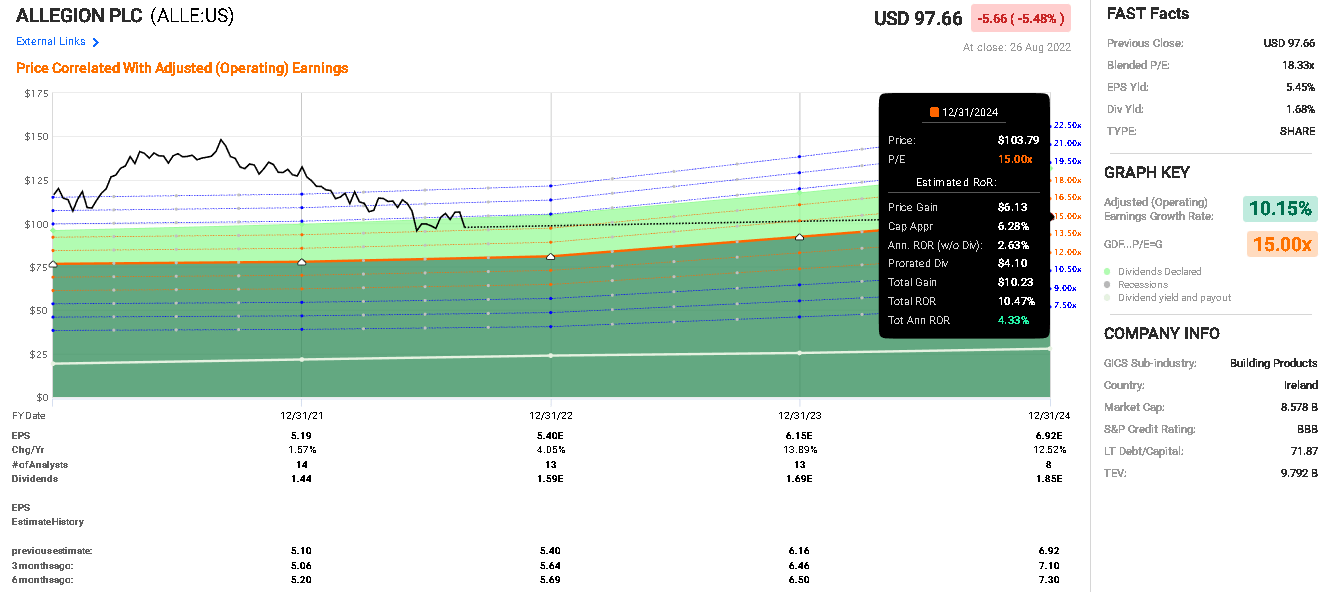

From Figure 7, if the earnings and P/E multiple are met at the end of 2024, we might expect a price of $103.79, representing an increase of $6.13 over the current price at the time of my analysis, and giving a 10.47% total rate of return for the period (including the dividends), or a total annualized rate of return of 4.3%.

Figure 7. Analyst expectations of Allegion's future earnings and expected prices at a 15x P/E ratio (FAST Graphs)

{kind=link}

However, if the P/E ratio hits the five-year normalized value of 21.8x, using FAST Graphs as a calculator, this would suggest that prices hit a $151.37 level, giving a total rate of return of 59% and an annualized rate of return of 21.89%. This outcome seems less certain as I suspect the P/E will trend closer to the 15x level, particularly given the estimated growth rates seem to be slowing down and analyst estimates of earnings have been revised downwards (see data at the bottom of Figure 7).

Thesis

The future prospects for Allegion remain difficult. As a company, they have made some headway in tackling pressing issues, such as pricing, but remain lumbered with higher levels of inventory. As growth is expected to slow, their earnings growth may slow further (and at the bottom of Figure 7, we can see the analyst revisions downwards that serve as a caution).

The firm has a relatively short history as a stand-alone firm and so it will be difficult to judge how effectively they may respond to changing macroeconomic environments. As such, my conservative estimate presents an annualized rate of return of 4.3% until the end of 2024, with a reasonable dividend growth off a low starting yield. If the company continues to trade at high P/E multiples, the annualized rate of return may be as high as 22.89% through to the end of 2024.

Personally, I take the more conservative view. I see this as an investment with potential upside, but facing some challenging situations and the company remains somewhat overvalued. However, the price declines since the start of the year have made it possible, in my estimation, for an investor buying stock now at a lower price to benefit from the future growth of the company, with expectations of about 14% earnings growth in 2023 followed by 12.5% earnings growth in 2024 (Source: FAST Graphs). The range of possibilities here are also reflected in a divergence of the nine analyst ratings I've seen on Stock Rover; five Strong Buys (up from three only three months earlier) are balanced by three Holds and one Sell.

As such, I rate Allegion as a Buy but note the potential for further downside risk.

For further details see:

Allegion: Security And Earnings Growth As Operations Improve