ALLG - Allego: Negative Shareholders' Equity And Underwhelming Q3 2023 Results

2023-11-18 08:31:03 ET

Summary

- Allego booked revenues of €28.6 million ($31 million) in Q3 2023 and its operating loss almost doubled.

- The company is far behind on the revenue and EBITDA estimates presented during its 2022 listing.

- With cash running out fast, it seems that significant stock dilution in the near future is inevitable.

- The short borrow fee rate is over 50% and I think that risk-averse investors should avoid this stock.

Introduction

In October 2022, I wrote a bearish article on SA about European electric vehicle (EV) charging company Allego (ALLG) in which I said that it was behind on its 2022 revenue and EBITDA targets and cash was running out fast.

I think this is a good time to revisit Allego as it released its Q3 2023 financial results on November 14. In my view, the situation is grim as the operating loss doubled due to soaring general and administrative expenses while shareholders' equity is in negative territory. However, short-selling remains dangerous. Let's review.

Overview of the Q3 2023 financial results

If you aren't familiar with the company or my earlier coverage, here's a short description of the business. Allego was founded in 2013 and it had a network of almost 30,000 EV charging ports across 16 counties in Europe as of September 2023. Just over 25,000 of the charging ports are owned while the remainder are installed across partner sites. In addition, Allego has developed two proprietary software platforms - Allamo and EV Cloud. Allamo can identify premium charging sites and it also forecasts demand. EV Cloud, in turn, offers software solutions for EV charger owners. Allego currently employs about 200 people across 11 countries.

{kind=link}

{kind=link}

In March 2022, Allego listed on the NYSE through a merger with a special-purpose acquisition company (SPAC) and back then it had ambitious goals. Revenues were expected to surpass €220 million ($238.7 million) in 2023 while operational EBITDA margin was forecast to exceed 20% for that year.

Allego

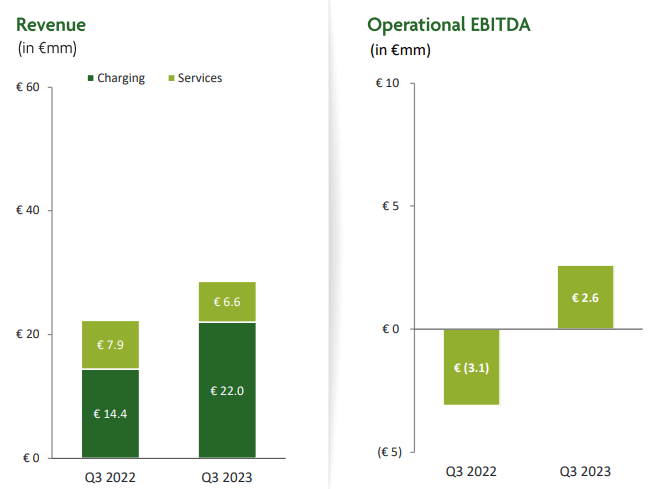

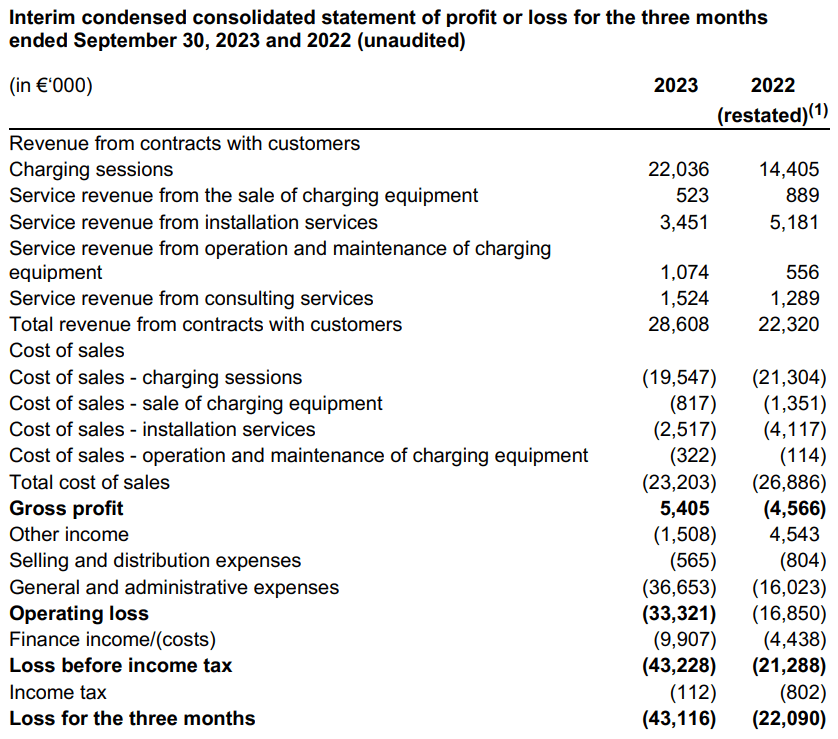

Turning our attention to the Q3 2023 financial results, we can see that Allego is far behind on those goals. Total revenues for the quarter came in at €28.6 million ($31 million) thanks to an increase in the utilization rate to 12.8% from 11.5% a year earlier as well as a 29.2% increase in energy sold. However, revenue from installation services and operation and maintenance of charging equipment declined by 16.5%. While operational EBITDA was positive for the fourth consecutive quarter, it stood at just €2.6 million ($2.8 million) for Q3 2023.

{kind=link}

Allego's outlook for the full year includes total revenues of between €180 million ($195.3 million) and €185 million ($200.7 million) as well as operational EBITDA of between €30 million ($32.6 million) and €35 million ($38 million). This represents a slight downgrade compared to three months ago when the company expected to book total revenues of between €180 million ($195.3 million) and €200 million ($217 million) and operational EBITDA of between €30 million ($32.6 million) and €40 million ($43.4 million) for 2023.

Looking at the income statement, I find it concerning that the operating loss soared by 97.8% to €33.3 million ($36.1 million) in Q3 2023 despite the improved margins. The main reason behind this was a significant increase in general and administrative expenses and I'm concerned that Allego could be years away from generating positive net income, especially as finance costs are rising rapidly.

{kind=link}

Turning our attention to the balance sheet, we can see that shareholders' equity is negative while working capital is shrinking fast. Net debt, in turn, stood at €283.3 million ($397.4 million) at the end of September while cash and cash equivalents were down to €28.8 million ($31.2 million). Considering free cash flow was minus €92.6 million ($100.5 million) for the first nine months of 2023, it seems that an equity offering in a month of two could be inevitable.

Allego Allego

Overall, I think the Q3 2023 financial results of Allego were underwhelming and the estimates during the 2022 listing seemed ambitious, especially in terms of profitability. To be fair, the writing was on the wall as soon as the SPAC deal was completed. As I mentioned in my previous article about Allego, the company was projected to emerge with $490 million in cash from the SPAC transaction, but redemptions reached 98% and it thus received only €146.1 million ($144.8 million). This has severely limited investments since the listing and CAPEX for the first nine months of 2023 was just €48 million ($52.1 million). In my view, Allego is in a catch-22 situation here. The company can't keep up with competitors as well as improve EBITDA without investing heavily in opening new high-margin fast and ultra-fast charging sites. However, CAPEX needs in this sector are high and the balance sheet is in a rough state. Even a major equity offering is unlikely to provide enough funding for the original investment plans of the company.

My rating on Allego continues to be a strong sell despite the share price losing two-thirds of its value since my previous article. Yet, short selling seems dangerous here as data from Fintel shows that the short borrow fee rate is at 53% as of the time of writing. In addition, risk hedging opportunities seem limited as the lowest available strike price for call options is $2.50. It could be best for risk-averse investors to avoid this stock.

Turning our attention to the upside risks, I think that the major one is that the prices of microcap stocks can increase significantly without clear catalysts, and this can result in major losses for short sellers. This is an illiquid stock with the daily trading volume rarely surpassing 50,000 shares, which means that significant volatility is likely. Another risk here is that Allego could become a takeover target despite the lack of fast and ultra-fast charging sites. It has a large EV charging network and a competitor or a new company entering the market could find its assets appealing.

Investor takeaway

In my view, the business of Allego is close to worthless in its current state as there is no clear path to reaching a positive net income due to the lack of CAPEX as well as the rising debt levels. Without more fast and ultra-fast charging sites, the company is likely to be left behind by rivals in the coming years. With cash running out fast, it seems that significant stock dilution in the near future is inevitable. However, short selling seems dangerous as the short borrow fee rate is above 50% and the lowest available strike price for call options is $2.50. I think risk-averse investors should avoid this stock.

For further details see:

Allego: Negative Shareholders' Equity And Underwhelming Q3 2023 Results