IEF - Allete Stock Compares Favorably To Bond ETFs IEF And ILTB

Summary

- At current share price levels, Allete offers an attractive and safe dividend yield of 4.3%.

- Being primarily a regulated utility, Allete's profit margins are insulated to a considerable extent against the impact of cost inflation.

- Allete stock compares favorably to two bond ETFs, both on capital preservation and dividend yield.

Investment Thesis

Allete ( ALE ), which is primarily a regulated utility, provides regular income through dividends, and has an ability to recover cost inflation through regulated price increases. These two factors also tend to support market price of the stock. ALE's degree of safety of income and capital value could be seen as bond-like attributes, but not to the extent the stock could be considered risk-free. What sets Treasury bonds apart is the regular fixed amount coupon payments and the certainty of redemption at face value, if held to maturity, giving them risk-free status. But if an investor finds themselves unable or unwilling to hold to maturity, then capital value is a function of the market at the time of exit.

The two bond ETFs I am comparing ALE to are the iShares Core Long-Term U.S. Bond ETF ( ILTB ) and the iShares 7-10 Year Treasury Bond ETF ( IEF ). IEF might be considered risk-free due to investing solely in treasury bonds, and ILTB might be considered a very safe investment due to an investment mix of treasury and corporate bonds. But both of these ETFs are designed to not hold bonds to maturity, thus introducing market risk. Possibly the best way to demonstrate the potential for market risk imacting an investment in ALE and these two ETFs is to look back at history. Figure 1 below shows price movements for ALE, ILTB, and IEF over ~8 years from Dec. 31, 2014, through Nov. 11, 2022.

Figure 1.1

YCHARTS

Fig. 1 shows that there appears to be a degree of correlation in price movements for ALE, ILTB, and IEF from Dec. 31, 2014, through the beginning of 2020. Through the height of the COVID-19 pandemic the two bond ETFs shone, presumably due to the perceived safety in bond investments. From the beginning of 2022, the prices of all three declined sharply, which is to be expected as interest rate increases started to bite. But that is not the whole story. The story is expanded on below.

Table 1.1

{kind=link}

Table 1 above shows over the ~8 year period - Dec. 31, 2014, to Nov. 11, 2022 - the price/dividend ratio for ALE and ILTB declined by similar percentages of 17.0% and 17.9%, respectively. Over the same period, the dividend yield for ALE and ILTB increased by similar percentages of 20.5% and 21.8%, respectively. Despite these statistics, ILTB's price declined by 21.4%, while ALE's share price increased by 10.1%. The reason for this disparity is due to ALE's yearly total dividend per share increasing by 32.7% over the ~8 year period, while ILTB's yearly total dividend decreased by 4.3%. A dividend decrease of 22.4% also contributed to a 9.5% decline in IEF price.

The price decrease for IEF would have been greater but for a 16.7% increase in the price/dividend ratio, which might not be sustainable in the event of further interest rate increases. Figure 1 shows healthy yields to maturity for both ILTB (5.48%) and IEF (3.83%), but as the underlying bonds will not be held to maturity, these figures are fairly meaningless. I consider the ultimate measure of stock performance is total average yearly rate of return. Table 1.2 below shows the comparative returns for ALE, ILTB, and IEF across a range of investment periods, commencing Dec. 31, 2014, Dec. 31, 2015, and each year to Dec. 31, 2021, and all ending Nov. 11, 2022.

Table 1.2

{kind=link}

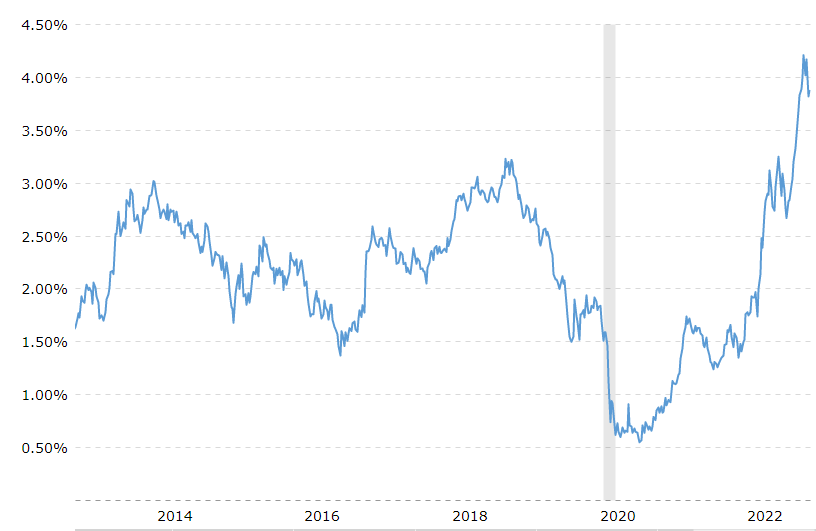

Table 1.2 shows, on a total return basis, that ALE has significantly outperformed the two ETFs in the majority of years. For IEF, investing solely in treasury bonds, that might be understandable due to the perceived risk-free nature of the investment. But the structure of the IEF ETF precludes IEF holding bonds to maturity, so the value of the bonds disposed is subject to market pricing at time of exit, making the investment no longer risk-free. Investor A's 0.5% average yearly return for an investment period ~8 years is far below historical 10-year bond rates, as per the chart below from Macrotrends .

{kind=link}

If investor A had invested directly in treasury bonds with ~8 years to maturity at end of 2014, they could have expected an average yearly risk free return of ~ 2.0%.

Based on all of the above, it would appear that ALE has generally outperformed the two ETFs. Neither ALE nor the two ETFs could be considered risk-free, but a growing dividend ameliorates some risk for ALE. The comparative historical performance appears to be a reasonable guide to future comparative performance for ALE and the two ETFs, making ALE possibly the preferred investment

Additional detail for ALE, ILTB, and IEF appears below.

Allete Stock

Figure 2

Figure 2 shows ALE dividend yield has increased from ~3.6% on Dec. 31, 2014, to 4.25% at Nov. 11, 2022, and the share price has increased by 10.1% from $55.14 to $60.69 over the same time frame. ALE in its current form has 11 consecutive years of dividend growth and 16 years of consecutive dividend payments. There have been dividend increases in 15 of the last 16 years, with 2010 being the only year without a dividend increase. But ALE's underlying business has a far longer dividend history, as per this excerpt from the 2005 10-K filing :

We have paid dividends without interruption on our common stock since 1948. A quarterly dividend of $0.30 per share on our common stock will be paid on March 1, 2005 to the holders of record on February 15, 2005. Our common stock is listed on the New York Stock Exchange under the symbol ALE and our CUSIP number is 018522300 (formerly 018522102).

As a result of a spinoff of a segment of the business in 2005, the present business was allotted a new CUSIP number, and so the dividend history started afresh from that time.

Description of ALE Business

The company is aggressively developing wind power and, perhaps more importantly, investing in transmission infrastructure to get wind and hydro power to where it's needed, and to deal with intermittency. The recent acquisition of New Energy Equity also positions it well to take advantage of solar power in addition to wind and hydro power, and to leverage its transmission network. New Energy Equity specializes in the development of distributed-generation solar facilities from one to 10 megawatts.

Here is an excerpt from the FY2021 10-K filing :

ALLETE is predominately a regulated utility through Minnesota Power, SWL&P (Superior Water, Light & Power Company), and an investment in ATC (American Transmission Company LLC). ALLETE's strategy is to remain predominately a regulated utility while also investing in ALLETE Clean Energy and our Corporate and Other businesses to complement its regulated businesses, balance exposure to the utility's industrial customers, and provide potential long-term earnings growth... plans include expanding its renewable energy supply to 70 percent by 2030, achieving coal-free operations at its facilities by 2035, and investing in a resilient and flexible transmission and distribution grid.

ALE Total Returns 2015-22

Table 2

{kind=link}

iShares Core Long-Term U.S. Bond ETF

Figure 3.1 below shows the iShares Core Long-Term U.S. Bond ETF price movement and dividend yield from the end of 2014 to date.

Figure 3.1

Figure 3.1 shows ILTB yield has increased from ~3.6% on Dec. 31, 2014, to 4.4% on Nov. 11, 2022, and the share price has decreased by 21.4% from $63.52 to $49.92 over the same time frame.

Description of ILTB Bond Holdings

As per the iShares website , the "iShares Core 10+ Year USD Bond ETF seeks to track the investment results of an index composed of U.S. dollar-denominated bonds that are rated either investment grade or high-yield with remaining maturities greater than 10 years."

Figure 3.2

{kind=link}

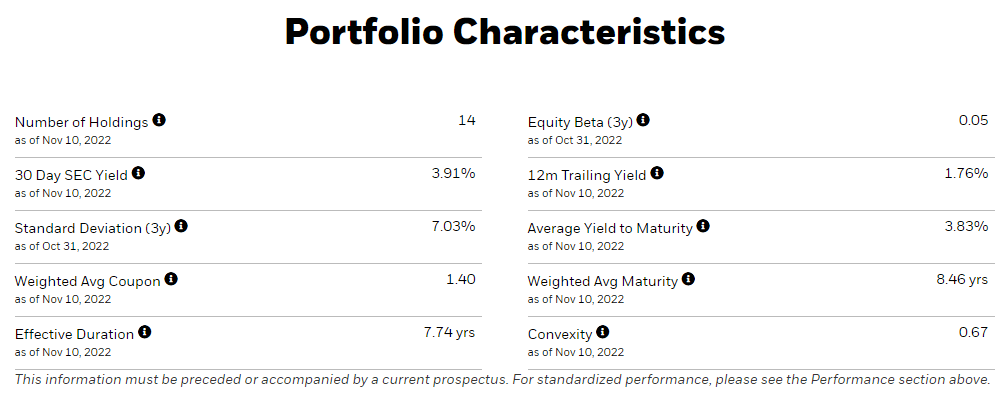

As the name implies, ILTB only holds bonds with 10+ years to maturity. This requires ILTB to sell bonds at market price when they reach 10 years to maturity. For this reason, the average yield to maturity of 5.48% as per Fig. 3.2 is largely irrelevant because bonds are never held to maturity. The result is the safety aspect of a guaranteed face value at maturity is lost.

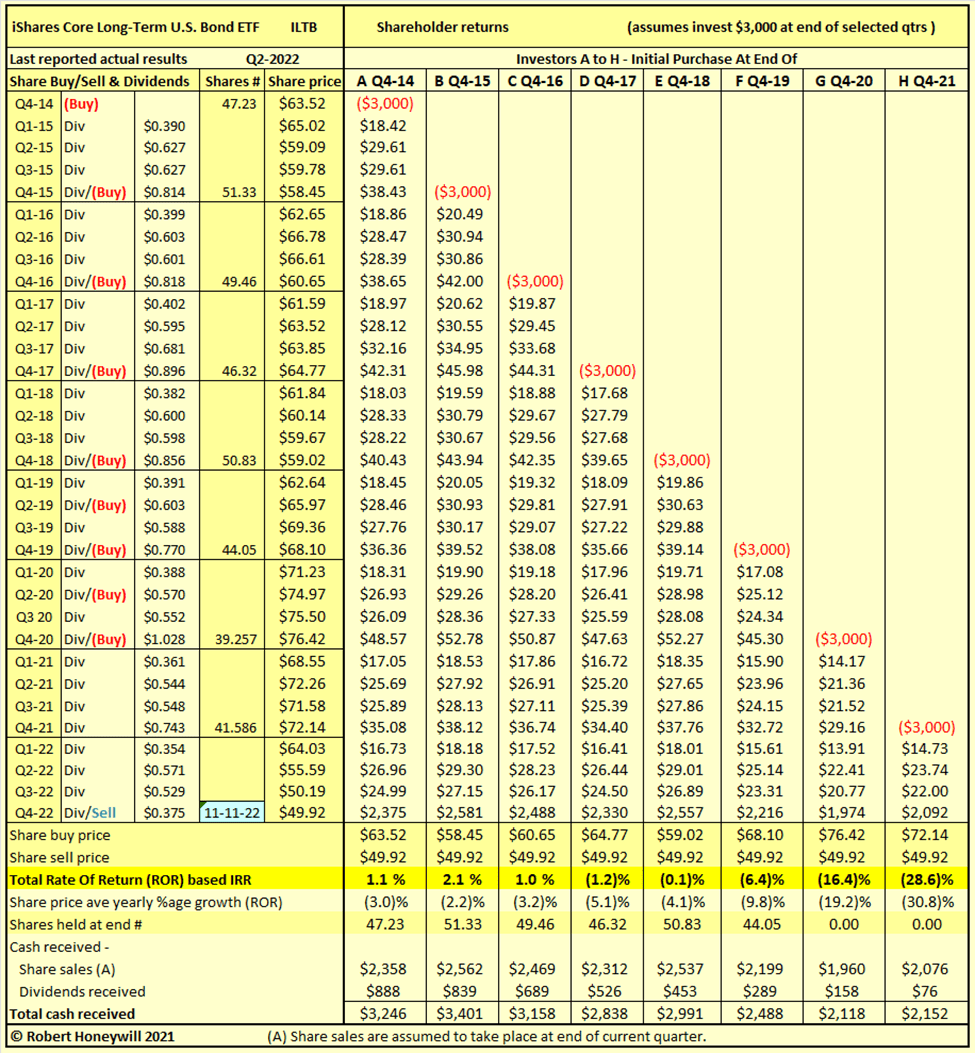

ILTB Total Returns 2015-22

Table 3

{kind=link}

iShares 7-10 Year Treasury Bond ETF

Figure 4.1 below shows the iShares 7-10 Year Treasury Bond ETF price movement and dividend yield from the end of 2014 to date.

Figure 4.1

Figure 4.1 shows that IEF's yield has decreased from 2.05% on Dec. 31, 2014, to 1.76% on Nov. 11, 2022, and the share price has decreased by 9.5% from $105.99 to $95.94 over the same time frame.

Description of IEF Bond Holdings

As per the iShares website , the "iShares 7-10 Year Treasury Bond ETF seeks to track the investment results of an index composed of U.S. Treasury bonds with remaining maturities between seven and 10 years."

Figure 4.2

{kind=link}

As the name implies, IEF only holds bonds with at least seven-plus years to maturity. This requires IEF to sell bonds at market price when they reach seven years to maturity. For this reason, the average yield to maturity of 3.83% is largely irrelevant, because bonds are never held to maturity. The result is the safety aspect of a guaranteed face value at maturity is lost. This is illustrated in the returns in Table 4 below.

IEF Total Returns 2015-22

Table 4

{kind=link}

Investor A in Table 4 above is showing a 0.5% total return based on market value on Nov. 11, 2022, after holding for nearly eight years. As per table 1.1 above, the dividend yield at purchase was 2.05%. If Investor A had invested directly in a bond with a yield to maturity of 2.05%, and with eight years to maturity, by holding another approximately seven weeks, that is the average yearly return that would be achieved. Bond ETFs might be an investment in bonds, but investors in ETFs lose one of the key safety attributes of a direct investment in bonds.

Summary and Conclusions

An investment in a regulated utility such as ALE is a particularly safe investment, but it's not without risks. Management could execute poorly and/or catastrophic losses could occur (e.g., wildfire events causing disruption and even bankruptcy for Californa utilities). On the other hand, market risk appears relatively low for ALE with a growing dividend providing fairly assured income and supporting the share price.

While Treasury bonds are risk-free if held to maturity, the structure and operation of the bond ETFs, as discussed above, introduce market risk. This market risk becomes apparent in times such as now, with inflation driving higher interest costs.

Over the past eight years ALE has provided superior returns to the two bond ETFs. With the prospect of further interest rate increases, this is likely to continue into the foreseeable future.

For further details see:

Allete Stock Compares Favorably To Bond ETFs IEF And ILTB