EQH - AllianceBernstein: 6 Reasons To Consider Buying

2023-12-20 07:12:50 ET

Summary

- AllianceBernstein has a strong history of solid returns for shareholders.

- The company's partnership structure provides tax advantages and results in the company having a high dividend yield.

- AB's private wealth business is a key part of its revenue and offers a valuable distribution channel for the firm's investment fund offerings.

- AB is trading at a highly attractive valuation based on an intrinsic valuation analysis.

- I am initiating AB with a buy rating.

AllianceBernstein Holding LP (AB) is an asset management company with a strong history of delivering results for its own shareholders. AB stands out as different from its peers in that it is a partnership, has a large private wealth business, and has a key strategic partner.

Over the past 10 years, AB has delivered a total return of 225% compared to a total return of 213% delivered by the S&P 500. AB has also posted strong performance relative to most of its peers over the same time period.

There are six reasons why I believe investors should consider buying the stock at current levels:

1. Partnership structure provides tax advantages

2. Private wealth business represents a key part of the company's business

3. Strong performance track record provides competitive advantage vs peers

4. Strong and rapidly growing alternatives business

5. Strategic partnership with Equitable Holdings provides key advantages

6. Attractive valuation

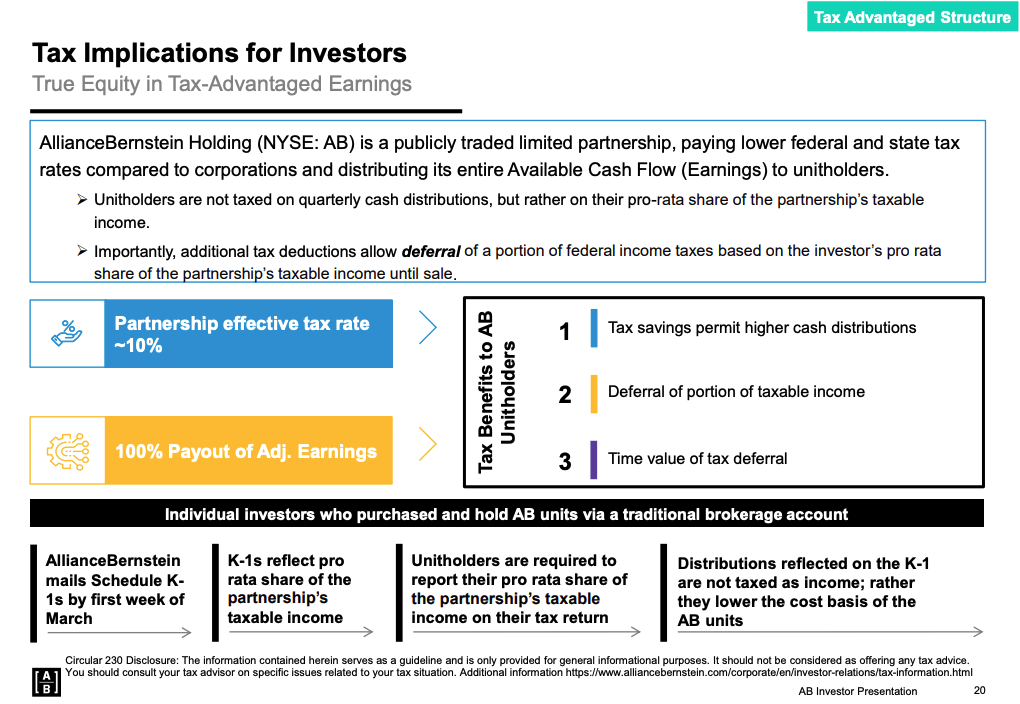

1. Partnership structure provides tax advantages

AB is different from its peers in that it is structured as a partnership. Yes, this means investors have to deal with the dreaded K-1. However, the partnership structure provides a number of key advantages.

The most significant tax advantage related to AB's partnership structure is that its effective tax rate is much lower. For FY 2022, AB's effective tax rate was just 10.3% compared to a 21% U.S. Federal Corporate Tax rate.

As a partnership, AB is required to payout the vast majority of its earnings each year to shareholders. This results in AB having a very high dividend yield which grows over time with earnings growth. As shown by the chart below, AB almost always offers a much better dividend than its peers.

Unitholders are generally not taxed on the full amount of the distribution and are able to defer payment of taxes until sale. This allows investors to compound their investments on a tax-deferred basis, which is a key benefit for investors related to this structure. Another key benefit is that if units are held until death, the basis will generally step up and tax may be entirely avoided. This represents a major tax advantage compared to investments held in AB's peers, which are C corporations.

For this reason, AB is a particularly attractive investment for individuals in high tax brackets who may be able to hold AB shares until death.

AB Investor Presentation

{kind=link}

2. Private wealth business represents a key part of the company's business

AB's private wealth business has ~$113 billion in AUM which accounts for 17% of the firm's total AUM. However, the business accounts for 34% of the company's base fees. This is due to the fact that private wealth fees tend to be higher than funds charged on investment funds. The company's private wealth business has been a bright spot in recent years and has posted three straight years of organic growth.

The private wealth business provides a key distribution channel for AB's products and is a differentiator vs competitors who do not have a captive wealth management business. While large banks such as UBS (UBS), Goldman Sachs (GS), J.P. Morgan (JPM), and Morgan Stanley (MS) have their own wealth management businesses which serve as a distribution channel for its products, independent asset managers such as Franklin Resources (BEN), Invesco (IVZ), and T. Rowe Price (TROW) have very small or non-existent private wealth businesses. TROW's private wealth business has ~$6 billion in assets while BEN and IVZ are not in the business.

The private wealth business is mostly relationship-driven and tends to be more immune to the threats related to passive low fee options compared to the traditional asset management business. A recent example of the staying power of the traditional advisor-based wealth management business can be seen in J.P. Morgan's recent decision to wind down its Robo-Advisor business.

With $113 billion in AUM, AB is not one of the large players in the industry and thus I believe has significant growth potential. For FY 2023, the company is on track to increase total advisor headcount by ~5%.

3. Strong performance track record provides competitive advantage vs peers

It is no secret that the vast majority of actively managed funds have failed to beat their benchmarks over long periods of time. According to Morningstar, over the past 5 years, just 29.5%, 29.5%, and 30.8% of active U.S. Large Blend, U.S. Large Value, and U.S. Large Growth funds have beaten their benchmarks.

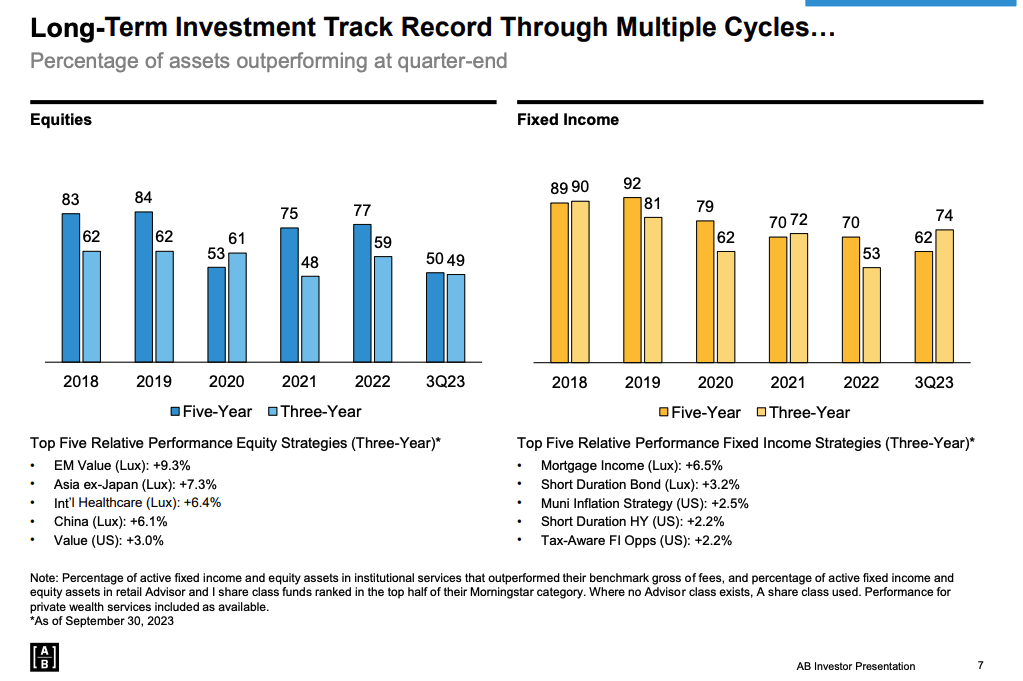

AB benefits from a fairly strong track record. This is especially true in fixed income which accounts for ~39% of the firm's total AUM.

The company's strong performance track record is an important selling point with customers and serves as an important part of the company's competitive advantage. Strong performance has helped allow AB to post a 5-year active AUM annualized organic growth rate of 2.1%. Comparably, based on the same metric, peers have posted a decline of 2.4%.

{kind=link}

4. Strong and rapidly growing alternatives business

Alternative and multi-assets solutions account for $126 billion in AUM accounting for ~19% of the firm's total AUM. Total private markets AUM is $61 billion which represents ~9% of total firm AUM. The company believes it can grow its private markets business at a 10-12% CAGR through 2027 resulting in $90-$100 billion in AUM.

As of FY 2022, private markets revenue accounted for 9.2% of asset management revenue. AB expects this number to increase to at least 20% by 2027. I believe it could be even higher if AB is able to find more attractive M&A targets.

AB significantly expanded its alternatives business with the acquisition of CarVal Investors in March 2022 which added $14.3 billion in alternatives AUM. I believe AB could continue to acquire smaller players and bulk up its alternatives business via strategic M&A. In particular, it may make sense for AB to acquire a midsized private equity firm to complement its strength in private credit. One of the key drivers of the CarVal acquisition was the idea that AB's strong distribution platform would allow CarVal to grow assets more rapidly than would have been possible on a stand-alone basis. The same argument would apply to a potential private equity deal in the future. One recent example of a traditional asset management firm buying its way into the PE space is Franklin Resources, which acquired Lexington Partners in 2022.

5. Strategic partnership with Equitable Holdings provides key advantages

Equitable Holdings (EQH) is AB's controlling shareholder with a 61% ownership interest in the company. EQH is a financial services company that provides insurance and other financial services.

In addition to being AB's majority investors, EQH is also the company's largest client with $109 billion in permanent capital. This accounts for ~16% of AB's total AUM. EQH also provides AB a $900 million lost-cost line of credit and an additional $300 million uncommitted facility.

EQH's ownership interest in AB represents a major part of its own value (~30% of EQH cash flow) and thus EQH is highly incentivized to help AB grow. EQH has been a seed investor in many of AB's alternatives strategies and has committed more than $6 billion to seed past funds.

A recent example of EQH providing seed capital to launch a new product can be seen in the launch of AB's NAV Lending fund on December 5, 2023. EQH has provided the initial anchor investment.

I view AB's relationship with EQH as a significant positive as a large percentage of AB's AUM is effectively captive. This is an advantage that most large peers, with the exception of PIMCO which has a similar relationship with its controlling shareholder Allianz, do not have. While EQH could move its assets elsewhere, it would have little incentive to do so given its controlling interest in AB. Moreover, AB is also poised to benefit from future AUM growth related to EQH's growing investment portfolio going forward.

Having EQH as a key strategic partner and the associated capital base allows AB to operate with a lower level of assets compared to most peers. Thus, AB is able to generate a higher return on assets.

6. Attractive valuation

Given AB's high level of dividends and correlation with earnings growth, I believe a dividend discount model represents a reasonable valuation method.

Key assumptions in my analysis include a levered beta of 1.05, an equity risk premium of 5.5%, FY 2024 dividend of $2.79 per share (this is inline with consensus earnings estimates and AB normally pays out 100% of earnings as a dividend), and a dividend growth rate of 3.5% into perpetuity. Based on these inputs, I find that AB should be worth $42.9 per share. While AB's dividend has been somewhat volatile historically as earnings can be volatile due to market moves, the company has grown its dividend at a 5.1% CAGR over the past 10 years.

Based on the trading level of the company stock of ~$32.4, the stock is pricing in perpetual earnings growth of just 1.4%. I view this as much too conservative as it is well below AB's historical growth rate and well below annual nominal GDP growth which has averaged 6.2%.

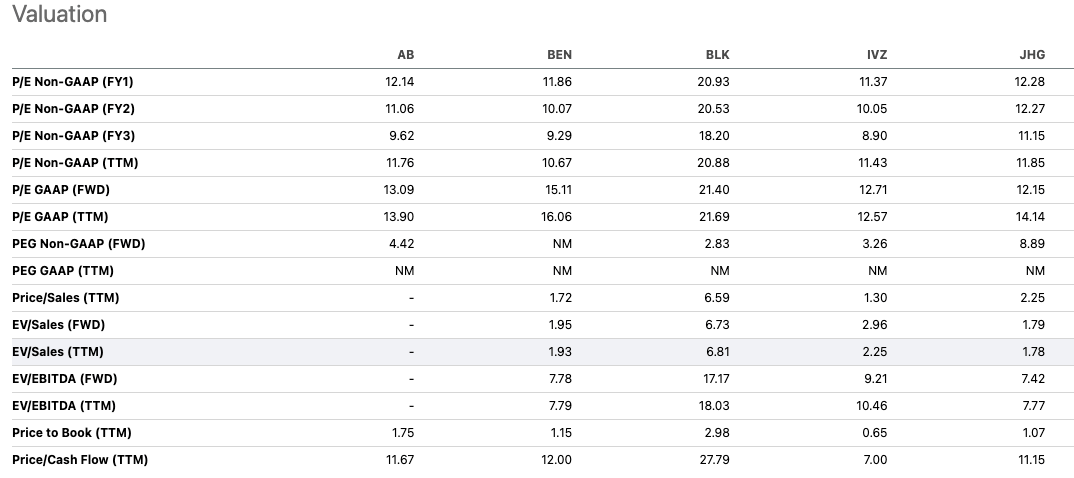

In addition to being attractive based on an intrinsic valuation, I also find AB attractive relative to its historical valuation range. AB trades at 11x consensus FY 2024 EPS. This compares to a historical average P/E ratio of 16.4x and a more recent average forward P/E ratio of 13.2x.

In terms of peer valuation, AB trades inline with peers such as Franklin Resources, Invesco, Janus Henderson, and others. AB trades at a discount to BlackRock, but I find that discount to be appropriate given BlackRock's stronger position in passive.

{kind=link}

Risks To Consider

One key risk to consider with AB is the fact that the company has been late to embrace ETFs. The company has just $1 billion in ETF assets and only launched its ETF platform a year ago. ETFs have become popular for a number of reasons, including their tax advantages over mutual funds and typical lower cost structure. Early movers BlackRock, Vanguard, and State Street are market leaders and hold a combined ~76% of total U.S. ETF market share. The next largest U.S. ETF platforms Invesco and Charles Schwab have an estimated 5.6% and 4% market share respectively. Thus, the top five players have a total market share of ~85.6%.

Part of the reason for this is the benefits due to scale have made it challenging for other players to gain share. Larger ETFs have a larger asset base to spread fixed costs against and thus are able to maintain profitability at very low fee levels. Comparably, smaller ETFs with less assets have a much smaller asset base to spread fixed costs across. This dynamic makes it difficult to new ETF issuers to break into the market in a profitable way unless products are highly differentiated from existing ETFs. Currently, an estimated 33%-50% of ETFs are running at a loss for issuers.

As a late mover in what is a fairly saturated ETF marketplace, AB faces the risk that a secular shift away from mutual funds towards ETFs results in market share losses as investors opt for lower fee ETFs offered by existing products with large AUM. For example, consider the recently launched AB US Low Volatility Equity ETF (LOWV) which was launched in March 2023, charges an expense ratio of 0.48%, and has just $16 million in assets. Comparably, the iShares MSCI USA Min Vol Factor ETF ( USMV ) charges an expense ratio of 0.15% and has assets of $27 billion. Given LOWV's small size, it is very difficult for this fund to compete with USMV on price and thus investors are likely to favor USMV given the cost advantage.

While AB was slow to enter the ETF space it has grown rapidly and is one of just five active ETF sponsors to reach $1 billion in assets within the first year of launch. This data is encouraging and suggests that the firm is having traction with its offerings and is offering products which investors view as differentiated. I expect AB to continue growing its ETF business but investors should pay close attention to its success going forward given the competitive advantages enjoyed by entrenched leading ETF providers.

Another key risk to consider is that AB fails to deliver better than average fund performance vs peers and benchmarks. A sustained period of below-average fund performance would deliver a considerable blow to traditional active franchises and may lead to outflows.

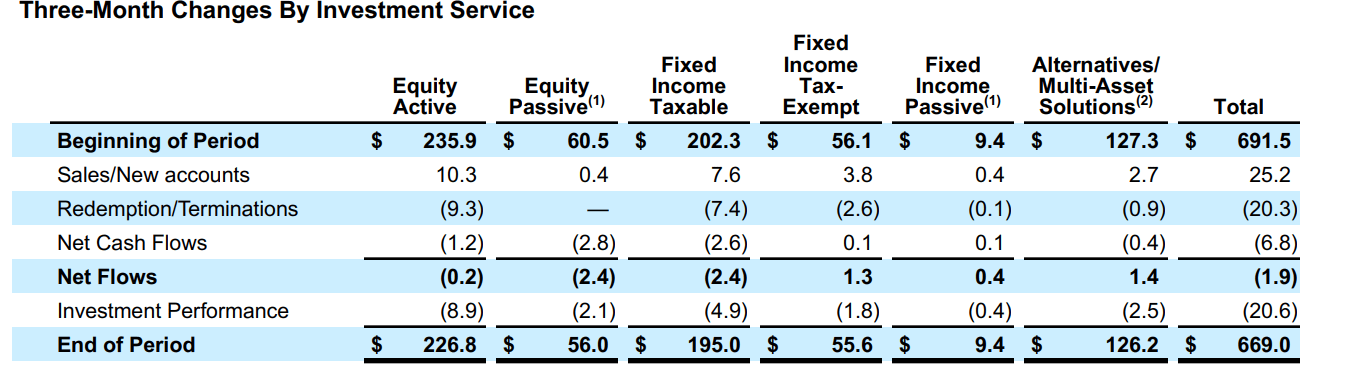

While recent equity product performance has been weaker than historical performance it has not significantly impacted fund flows as AB is still generating flows which are mostly inline with peers. During Q3 2023, AB posted net outflows of $1.9 billion on an asset base of $691.5 billion. Comparably, Franklin Resources posted long-term net outflows of $6.9 billion on an asset base of $1.4 trillion while BlackRock posted long-term net out outflows of $13 billion on an asset base of ~$9.1 trillion.

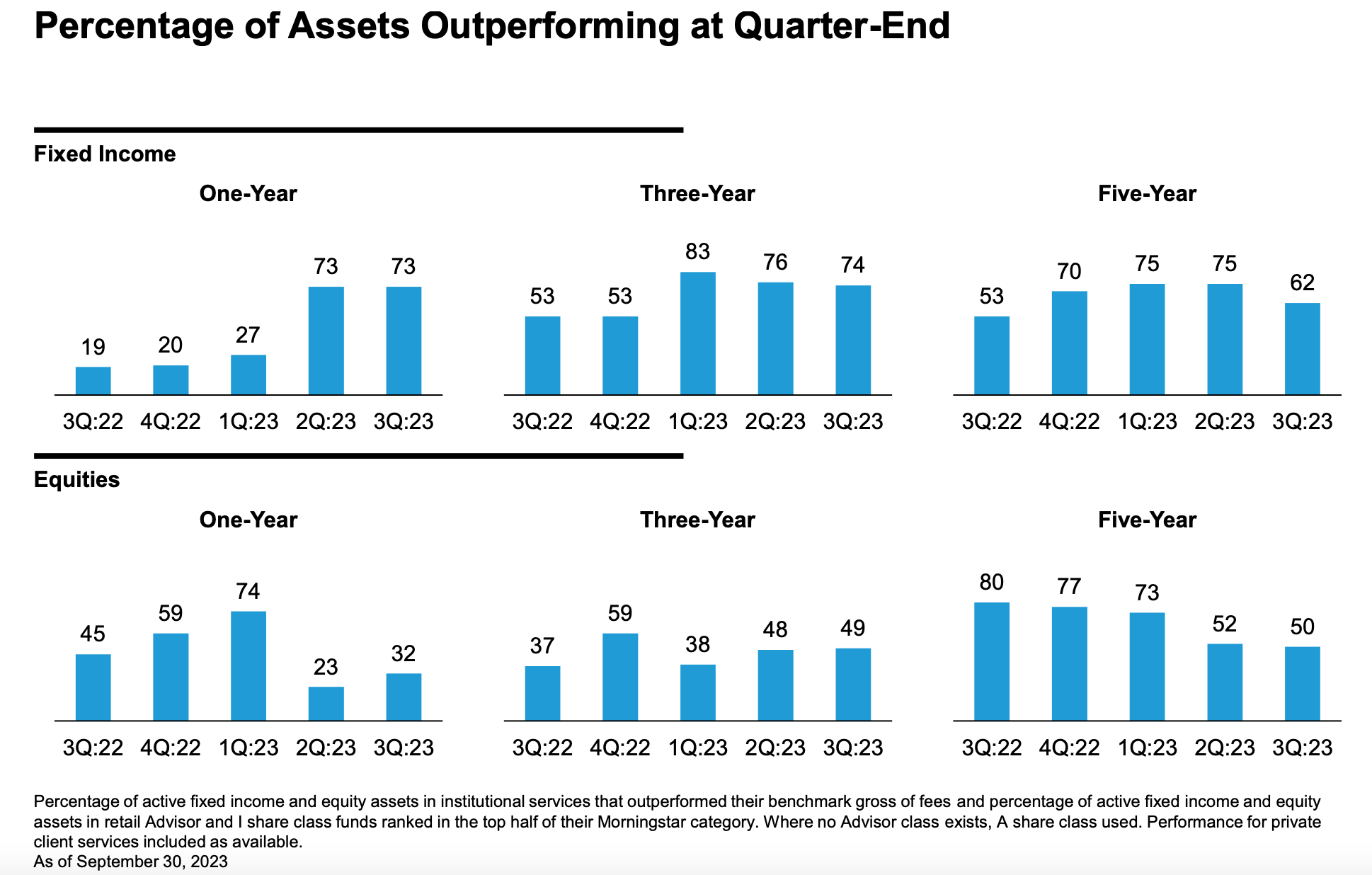

As of Q3 2023, just 50% of AB's equity assets were outperforming over the past 5-year period. Comparably, this number was 80% just a year ago. One driver of this has been that benchmarks tend to be tilted more towards mega cap names while AB products tend to be more diversified. For example, AB Large Cap Growth Fund (APGAX) has ~26% invested in its top 5 holdings. Comparably, the Russell 1000 Growth Index has ~35% exposure to its top 5 holdings. Overtime, I expect the market advance to broader out which should help performance.

Recent fixed income performance has been better with 62% of assets outperforming over the past 5 years compared to 52% during the same period a year ago. Thus, in aggregate, I believe recent performance has been reasonably strong, but investors should continue to monitor performance for signs of sustained weakness relative to benchmarks.

AB Investor Presentation AB Q3 2023 Flows Data (AB Q3 Earnings Release)

{kind=link}

{kind=link}

Conclusion

AB has a strong history of delivering solid results for shareholders. One unique characteristic of AB is its partnership structure. This structure allows the company to save on taxes while allowing investors to benefit from tax deferrals.

In certain cases, individuals may be able to own AB and pay very little tax if they never sell and the basis steps up upon transfer.

AB stands out from peers due to its strong historical performance track record, substantial private wealth business, and strategic partnership with EQH.

The company has a rapidly growing alternatives business which represents a significant growth opportunity for the company.

I find AB highly attractive based on an intrinsic valuation and relative to its own historical norm.

I am initiating AB with a buy rating and would consider downgrading the company if that valuation were to become less attractive.

For further details see:

AllianceBernstein: 6 Reasons To Consider Buying