DTW - Alliant Energy: A Solid Utility Play To Ride Out The Coming Economic Uncertainty

2023-08-21 06:14:29 ET

Summary

- Alliant Energy is a midsized regulated electric and natural gas utility serving Wisconsin and Iowa.

- The company enjoys stable cash flow and pays a high dividend yield of 3.58%.

- Alliant Energy plans to invest $8.5 billion in its infrastructure to grow its rate base and earnings per share.

- The company is well positioned to deliver a total return of 9% to 11% annually through 2026.

- The dividend is barely covered with cash flow, which could be a concern. It is unlikely that investors need to worry about a near-term cut, though.

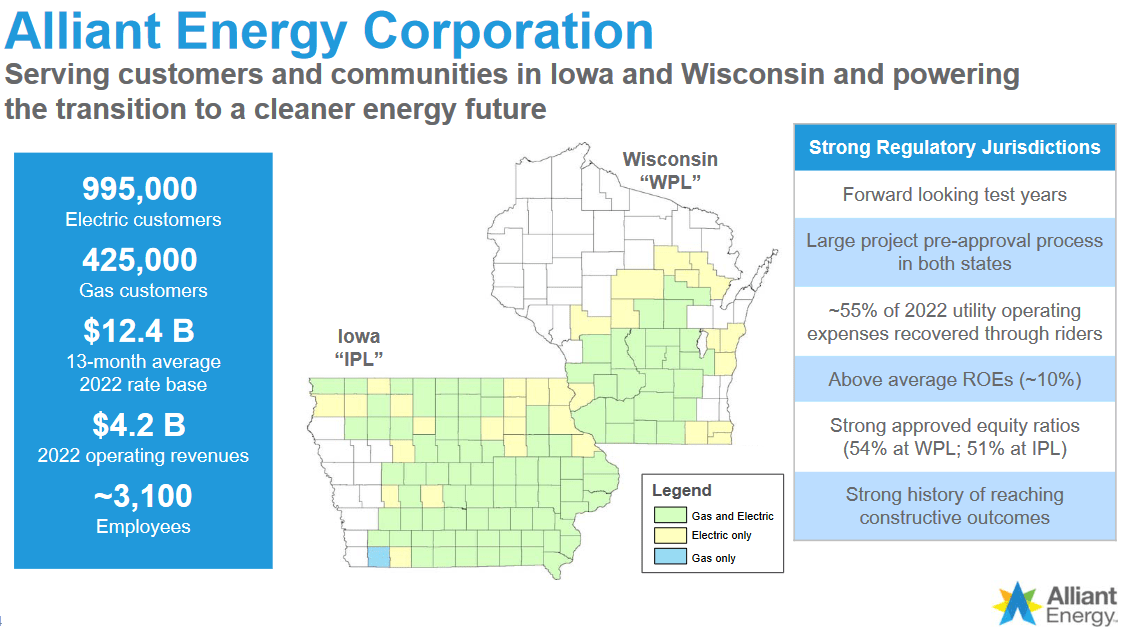

Alliant Energy Corporation ( LNT ) is a midsized regulated electric and natural gas utility serving most of the states of Wisconsin and Iowa. I call it a midsized utility despite its large service area because of the fact that most of its territory is not particularly populated. In fact, the company only has about 995,000 electric and 425,000 natural gas customers in its region:

{kind=link}

This certainly does not prevent the company from enjoying many of the characteristics that have long made regulated utilities popular investments for retirees and other conservative investors. In particular, these companies tend to enjoy remarkable cash flow stability and pay fairly high dividend yields. Alliant Energy is certainly no exception to this as the stock currently yields 3.58%, which is a lot higher than the 2.91% yield that the company had the last time that we discussed it. This is not unsurprising though as the share price has declined quite a lot since mid-July along with many other companies in the utility sector. This is almost certainly because the Federal Reserve is currently expected to be keeping interest rates high for a lot longer than the market was previously anticipating, making even a high-yielding stock like Alliant Energy somewhat unattractive relative to safe options available in the money market. Alliant Energy does have a reasonably nice valuation right now though, so long-term investors may still find a lot to like here. Let us investigate and see if Alliant Energy could be a good addition to your portfolio today.

About Alliant Energy Corporation

As mentioned in the introduction, Alliant Energy Corporation is a regulated electric and gas utility that serves most of the states of Wisconsin and Iowa. The company's territory includes some of the largest cities in each state, including Des Moines, Iowa, and Madison, Wisconsin. The company unfortunately does not serve Milwaukee, Wisconsin though, which is the largest city in that state. Regardless, we can still see that it has a total of 425,000 natural gas customers and just shy of one million electric customers within its service territory.

The fact that the company's electric utility has twice as many customers as its natural gas business is something that might be appealing to some investors. After all, politicians, activists, and media personalities have been heavily promoting the concept of electrification. At its core, this refers to the conversion of things that are historically powered by fossil fuels to the use of electricity instead. The proponents of this concept have targeted both space heating and cooking for conversion, which are two of the primary uses of utility-supplied natural gas. As such, some people might believe that natural gas utilities are likely to become obsolete in the near future. In a previous article , I pointed out that this is highly unlikely due to the cost and efficiency advantages that natural gas boasts relative to electricity. Nonetheless, the belief persists so the fact that the majority of the company's business comes from the provision of electricity might still prove attractive to some investors.

As might be expected based on the company's customer count, the majority of Alliant Energy's revenues come from the electric utility. In the first six months of 2023, about 78.74% of the company's total revenues came from the electric utility. It was a similar ratio in the prior-year period:

| H1 2023 |

| H1 2022 |

| Electric Utility |

| $1,567 |

| $1,586 |

| Gas Utility |

| $353 |

| $356 |

| Other Utility |

| $25 |

| $23 |

| Non-Utility |

| $45 |

| $47 |

| Total |

| $1,990 |

| $2,012 |

(all figures in millions of U.S. dollars)

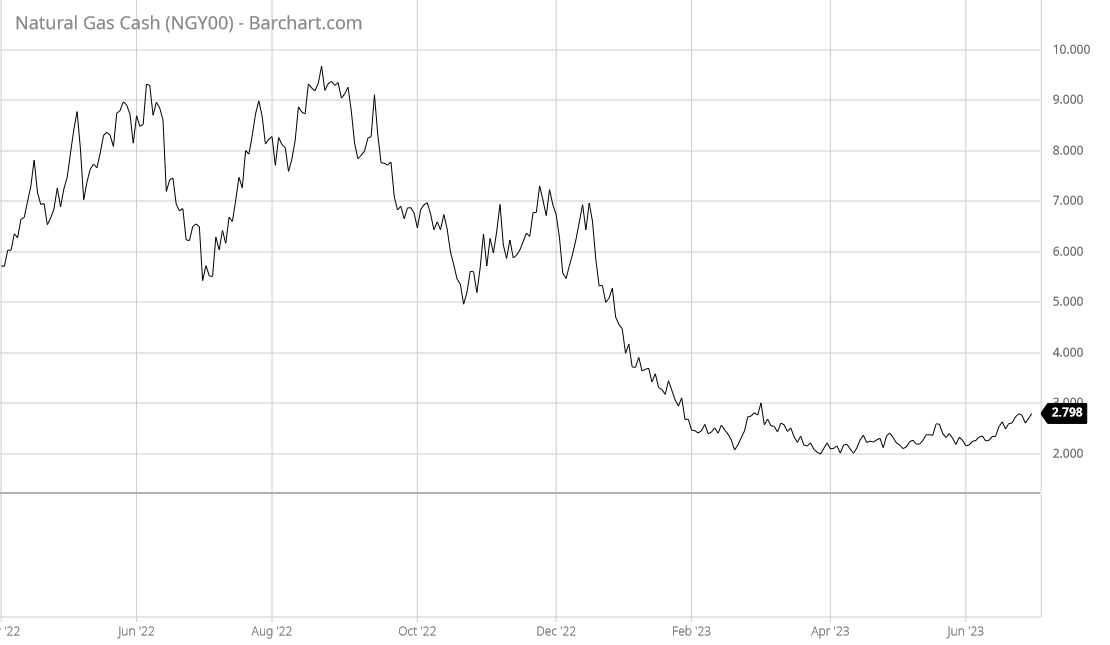

One curious thing here is that Alliant Energy's natural gas revenues were almost completely unaffected by the warm winter or the decline in natural gas prices that we saw over much of the first half of the year. The company did not provide a reason for this in its most recent conference call, but it did acknowledge that its performance was almost completely unaffected by the weather. This was in stark contrast to most other utilities, especially natural gas ones. During the first half of 2023, natural gas prices declined sharply in the United States:

{kind=link}

One of the biggest reasons for this is that the winter of early 2023 was a lot warmer than normal. As such, households consumed less natural gas than heating their homes than they usually do. The same is true for businesses that use natural gas for heat. As such, natural gas utilities sold fewer products than normal, which had a negative impact on revenue. It is curious that this was not the case for Alliant Energy, although as already stated management did not provide a reason for this.

This does overall support one of the items of our thesis for investing in Alliant Energy, however. One of the defining characteristics of most companies like this is that they tend to enjoy remarkably stable cash flows over time regardless of the conditions in the broader economy. This is certainly true for Alliant Energy. This chart shows the company's operating cash flows during each of the past eleven twelve-month periods:

{kind=link}

As we can clearly see, there was remarkably little variation from period to period. This is despite the fact that economic conditions changed wildly over the periods in question. For example, the early periods shown on the chart above include the COVID-19-related lockdowns that resulted in a massive number of business closures and unemployment. The economy experienced the highest inflation in more than four decades when this ended, and consumers began spending money instead of saving it. That caused energy prices to soar and prompted the Federal Reserve to raise interest rates to try and bring everything back under control. However, seemingly none of these things had any real impact on the company's cash flows, which is something that is very nice to see right now.

It should be fairly obvious why the company's cash flows are very stable regardless of the conditions in the broader economy. After all, Alliant Energy provides a product that is generally considered to be a necessity for our modern way of life. There are very few people in the United States that do not have electric service to their homes, and there are even fewer businesses that lack such utility services. The fact that we have all become accustomed to having electricity available has become so natural for us that we take it for granted and start to miss it when it is not available. The same necessity status is true of natural gas, for those people that use it as their primary heat source. As such, most people in the company's service territory will prioritize paying Alliant Energy for its products ahead of making discretionary expenses during times when money gets tight. As I pointed out in a recent blog post , money has been getting very tight for many consumers due to inflation outstripping wage growth over the past two years. As such, we are likely to see cutbacks in discretionary spending going forward. This could become even more severe once student loan payments restart in October and start stripping an average of $350 per month out of the budget of the average household that has student loans. Alliant Energy is thus exactly the sort of company that we would like to have in our portfolios during such an environment, as the company will not be impacted nearly as much as some companies that operate in other sectors of the economy.

Growth Opportunities

Naturally, as investors, we are unlikely to be satisfied with mere stability. We like to see any company in which we are invested grow and prosper with the passage of time. Fortunately, Alliant Energy is well-positioned to accomplish exactly that.

Unfortunately, the company will have difficulty achieving growth by increasing its customer base. That is particularly true for the electric utility. This is due to the fact that neither Wisconsin nor Iowa is growing at a particularly rapid pace. The U.S. Census Bureau estimates that Wisconsin's population is growing by 0.21% annually while Iowa's population is almost completely stable at 0.09% growth annually (see here and here ). While this is certainly better than a state such as Illinois or California which is experiencing a population decline, it is not rapid enough growth to make much of a difference to Alliant Energy's financial performance. At any rate, the sort of revenue growth that will result from growing its customer base at such low levels will not satisfy any investor that can get more rapid growth elsewhere.

Fortunately, Alliant Energy does have another method that it can employ to grow its earnings at a much more rapid rate than population growth alone would allow. This is by increasing the size of its rate base. The company's rate base is the value of its assets upon which regulators allow it to earn a specific rate of return. As this rate of return is a percentage, any increase to the company's rate base allows it to positively adjust the prices that it charges its customers in order to earn that specified rate of return. The usual way that a utility such as Alliant Energy increases its rate base is by investing money into upgrading, modernizing, or even expanding its utility-grade infrastructure. Alliant Energy is planning to do exactly that as the company has provided its investors with a four-year capital plan that involves the company investing $8.5 billion into its infrastructure:

Alliant Energy

I will admit that I would have liked to see a more expansive plan than this. Many of the company's peers have provided five-year plans extending out to 2027 or beyond. The fact that this company has not provided such visibility is disappointing, since the more information that we have the more accurate projections that we can make about where the company will be in the future. This is something that is very important for long-term investors.

Alliant Energy's capital plan as presented should be sufficient to grow its rate base from $12.4 billion at the start of this year to $16.7 billion by the end of 2026. Many readers will immediately note that this projected rate base increase is far less than the amount of money that the company will have to spend to achieve it. That is partially caused by depreciation, which is constantly reducing the value of the assets that the company has in service. Thus, in the absence of any spending at all, the company's rate base would actually decrease over time. The company needs to spend enough to overcome this effect and still grow the value of its assets.

Depreciation is not the only thing that weighs on the rate base growth relative to the amount of spending. Alliant Energy will also be retiring some assets during the projection period. One thing that we immediately notice above is that a substantial proportion of the company's capital spending is devoted to renewable generation assets. These are intended to replace some of the company's current generating assets. In particular, Alliant Energy has stated that it intends to take 1.6 gigawatts of coal generation capacity out of service between 2020 and 2026. That will remove the full remaining value of these plants from the company's rate base and thus offset some of the capital spending.

Despite these two factors reducing the impact that the company's capital spending will have on its rate base, we can still see that the company's rate base should grow over the 2023 to 2026 projection period. Overall, this projected rate base increase should be sufficient to grow the company's earnings per share at a 5% to 7% rate through the end of 2026. When we combine that with the company's current 3.58% dividend yield, we get a total projected shareholder return of 9% to 11% annually. That is a very reasonable return for a conservative utility company. We clearly have nothing to really complain about here.

Financial Considerations

It is always important to analyze the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. After all, very few companies have sufficient cash to completely repay their debt as it comes due. This newly issued debt will carry an interest rate that corresponds with the market interest rate at the time of issuance so the rollover can cause a company's interest expenses to increase in certain market conditions. As of the time of writing, the effective federal funds rate is at the highest level that we have seen since 2007. The target federal funds rate is actually at the highest level that has been seen since 2001. Thus, it is a near certainty that any debt rollover today will increase the company's interest expenses. In addition to interest-rate risk, a company must make regular payments on its debt if it wishes to remain solvent. Thus, an event that causes a company's cash flows to decline could push it into financial distress if it has too much debt. While utilities like Alliant Energy typically have remarkably stable cash flows over time, there have been bankruptcies in the sector before so this is not a risk that we should ignore.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity can cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of June 30, 2023, Alliant Energy has a net debt of $9.0230 billion compared to $6.4520 billion in shareholders' equity. This gives the company a net debt-to-equity ratio of 1.40 today. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity |

| Alliant Energy Corporation |

| 1.40 |

| DTE Energy Company ( DTE ) |

| 1.89 |

| CMS Energy Corporation ( CMS ) |

| 1.91 |

| WEC Energy Group ( WEC ) |

| 1.50 |

| Entergy Corporation ( ETR ) |

| 1.92 |

| Exelon Corporation ( EXC ) |

| 1.68 |

As we can clearly see, Alliant Energy compares fairly well to its peers in this respect, as its equity accounts for a higher proportion of its funding compared to other electric and natural gas utilities. As such, we can conclude that the company is probably not employing an excessive amount of debt to fund its operations. There does not appear to be a cause for concern here.

Dividend Analysis

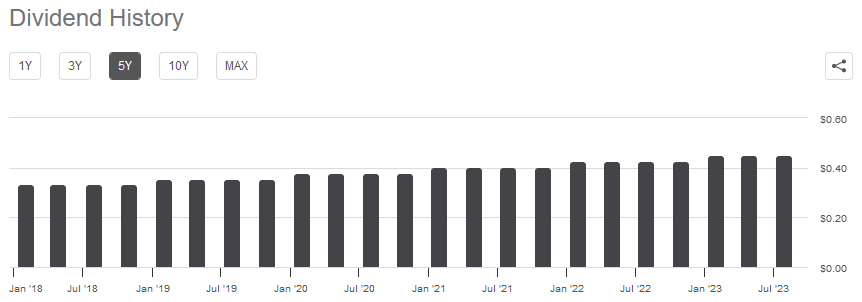

One of the biggest reasons why investors purchase shares of utility companies is because they tend to possess higher dividend yields than many other things in the market. This comes from the fact that they are usually relatively low-growth entities that would have difficulty delivering a competitive return through capital gains alone. These companies thus pay out a significant portion of their cash flows to the investors so that they can provide an acceptable total return for the average stock investor. Alliant Energy is no exception to this rule as the stock's current 3.58% yield is substantially higher than the current 1.49% yield of the S&P 500 Index ( SPY ). Alliant Energy's dividend yield is also above the 2.67% yield of the U.S. Utilities Index ( IDU ), which seems likely to appeal to income-focused investors. Alliant Energy has a long history of increasing its dividend on an annual basis:

{kind=link}

The fact that the company increases its dividend on an annual basis is very nice to see during inflationary periods, such as the one that we are experiencing today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it seem as though we are getting poorer and poorer with the passage of time, which is a particularly big problem for retirees or anyone else that is dependent on their portfolio to provide the income that they need to pay their bills or other expenses. The fact that Alliant Energy increases its dividend over time helps to offset this problem and ensures that the dividend maintains its purchasing power over time. The increases to the annual dividend also have the effect of boosting the effective yield-on-cost, which is nice for long-term investors.

As is always the case though, it is critical that we ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the company's stock price to decline.

The usual way that we judge a company's ability to pay its dividends is by looking at its free cash flow. Free cash flow is the amount of cash that was generated by a company's ordinary operations and is left over after it pays all of its bills and makes any necessary capital expenditures. This is the amount that is available to do things that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend.

During the twelve-month period that ended on June 30, 2023, Alliant Energy Corporation reported a negative levered free cash flow of $640.9 million. That was obviously insufficient to pay any dividend, but the company still paid out $439.0 million to its shareholders over the period. At first glance, this is certain to be concerning as the company did not have sufficient free cash flow to cover the dividends that it paid out.

However, it is not uncommon for a utility to finance its capital expenditures through the issuance of debt and equity. It will then pay its dividends out of operating cash flow. This is done because it is extremely expensive to construct and maintain utility-grade infrastructure over a wide geographic area. These expenses would otherwise prohibit the company from ever paying a dividend or providing any sort of return to its investors if it were to try and cover all of its capital expenditures without external financing. During the trailing twelve-month period, Alliant Energy reported an operating cash flow of $497.0 million. That was sufficient to cover the $439.0 million in dividends that the company paid out, but the coverage is extremely tight. Many of the company's peers have a bigger margin between operating cash flow and the dividends that are paid out. As such, Alliant Energy's dividend may be riskier than some other utilities, although the company can technically afford it.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a regulated utility like Alliant Energy, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few stocks that have such an undervaluation in today's richly valued market. As such, the best way to use this ratio today is to compare Alliant Energy to its peers in order to see which company has the most attractive relative valuation.

According to Zacks Investment Research , Alliant Energy will grow its earnings per share at a 6.47% rate over the next three to five years. This is in line with the earnings per share growth that we used earlier based on the company's rate base growth so it seems very reasonable. This growth rate gives Alliant Energy a price-to-earnings growth ratio of 2.73 at the current price. Here is how that compares to the company's peers:

| Company |

| PEG Ratio |

| Alliant Energy Corporation |

| 2.73 |

| DTE Energy Company |

| 2.85 |

| CMS Energy Corporation |

| 2.35 |

| WEC Energy Group |

| 3.24 |

| Entergy Corporation |

| 2.52 |

| Exelon Corporation |

| 2.70 |

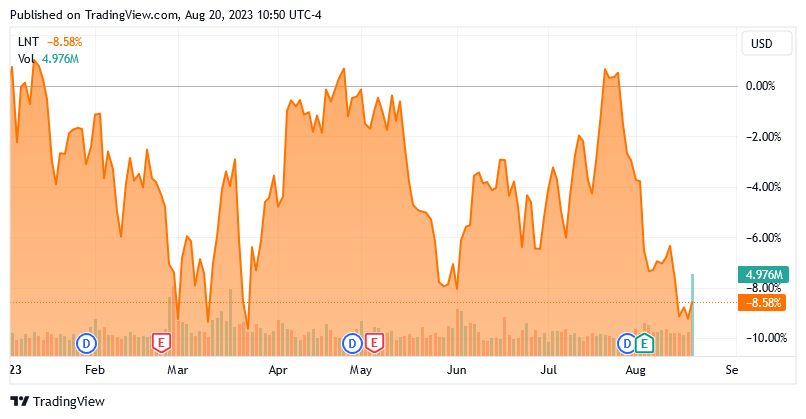

As we can see, Alliant Energy Corporation certainly does not appear to be undervalued relative to its peers. It does not appear to be overvalued either as its ratio is right around the median of this group. The company is much more attractively valued than the last time that we discussed it, which is unsurprising as the stock is down 8.58% year-to-date:

{kind=link}

Overall, we appear to have a reasonably decent opportunity to start building a position here. It is certainly possible that the stock will decline further, especially if inflation remains high and the Federal Reserve is forced to raise rates further from today's levels, but that is not something that will be a huge concern to a very long-term investor. My advice would be to dollar cost average if you are interested in building a position.

Conclusion

In conclusion, Alliant Energy offers a great deal of stability for any investor, which is especially valuable considering the overall economic weakness that the economy may encounter over the coming months. Alliant Energy's cash flows have proven to be resistant to both recessions and inflation and it seems almost certain that this will continue to be the case due to the fact that this company provides a product that most people will consider to be a necessity. The company's balance sheet is strong relative to its peers, and its relative valuation is also not too bad. The biggest concern here is that the company's dividend coverage is tight, but it still seems unlikely that it will end up cutting it in the near future.

For further details see:

Alliant Energy: A Solid Utility Play To Ride Out The Coming Economic Uncertainty