LNT - Alliant Energy: Buy This Blue-Chip Stock For Growing Passive Income And Strong Returns

Summary

- Alliant Energy's non-GAAP EPS payout ratio will edge slightly higher from 61.3% in 2022 to 62.6% in 2023.

- The company's revenue surged 14.8% higher in the nine months ended 2022 while non-GAAP EPS edged 2.6% higher during that time.

- Based on my inputs into the dividend discount model and discounted cash flows model, Alliant Energy is trading at a 3% discount to fair value.

- Alliant Energy's 3.1% dividend yield, 6%-7% annual earnings growth prospects, and 0.3% annual valuation multiple potential should deliver annual total returns of around 10% to shareholders in the years ahead.

When done properly and given enough time, dividend growth investing is a strategy that can help ordinary investors to reach financial independence. For clarity, I mean financial independence as the point at which an investor's annual dividend income (and other passive income) surpasses their annual expenses.

One dividend growth stock in my portfolio that I believe all dividend growth investors should consider buying is Alliant Energy ( LNT ). For the first time since my article last April , let's go over the company's fundamentals and valuation to understand why I rate it a buy for dividend growth investors.

Sleep Well At Night With A Safe Dividend

Once Alliant Energy announces its next dividend hike in approximately two weeks, the company will have raised its payout for 20 consecutive years. This firmly establishes the company as a Dividend Contender and positions the electric utility to become a Dividend Aristocrat toward the end of this decade.

Alliant Energy's 3.09% dividend yield is basically in line with the regulated electric utilities industry average of 3.11% . Since the stock doesn't stand out as a yield trap, this alone suggests that the dividend is probably at minimal risk of being cut.

Alliant Energy is forecasting midpoint non-GAAP EPS of $2.795 for 2022 ( $2.76 to $2.83 ). Compared to the $1.71 in dividends per share that the company paid for the year, this equates to a 61.3% payout ratio. Putting this into perspective, that's well within Alliant Energy's 60% to 70% target payout ratio (according to slide 5 of 36 of Alliant Energ y November 2022 Investor Presentation).

And the company issued midpoint non-GAAP EPS guidance of $2.89 for 2023 ($2.82 to $2.96). Stacked against the $1.81 in dividends per share that will likely be paid in 2023, this would work out to a still manageable 62.6% non-GAAP EPS payout ratio.

Alliant Energy's payout ratio has modest room for future growth and earnings will grow around 6% annually . This is why I believe a 6.75% annual dividend growth rate is doable over the long haul.

Alliant Energy Is A Steady Grower

{kind=link}

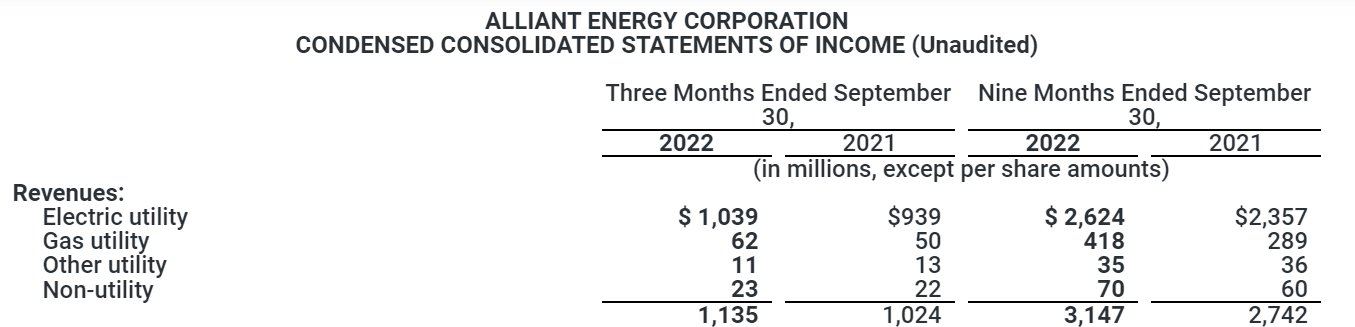

Through at least the first three quarters of the year, Alliant Energy has had a solid year. The company's total revenue increased 14.8% through Sept. 30 over the year-ago period to $3.1 billion.

Alliant Energy's spike in year-to-date revenue was driven by double-digit growth in both its electric and gas segments. As demand for electricity and its customer base grew, the company's year-to-date electric sales of megawatt-hours edged up 3.3% to 24,511. Paired with higher electricity rates , this is how the segment delivered respectable revenue growth. Alliant Energy's utility gas sold rose 12.2% year over year to 120,525 dekatherms. Along with higher gas rates, this led to mid-double-digit revenue growth in the gas segment.

Alliant Energy's year-to-date non-GAAP EPS inched 2.6% higher to $2.34. Non-GAAP EPS growth lagged behind revenue growth because of sharp increases in the electric production fuel and purchased power expense category and cost of gas sold expense category.

The $2.795 in midpoint non-GAAP EPS that Alliant Energy is anticipating for 2022 is equivalent to a 6.3% growth rate over 2021's base of $2.63 (except the link above, all details in this subheading per Alliant Energy Q3 2022 earnings press release and Alliant Energy Q4 2021 earnings press release ).

Risks To Consider:

Alliant Energy is a thriving utility. With that being said, the company has its share of risks.

In its efforts to counter the inflationary environment, the Federal Reserve is consistently raising interest rates. Analysts believe that the fed funds rate will top out around 5% in 2023. Alliant Energy plans to allocate $8.5 billion toward capital spending over the next four years (sourced from slide 17 of 36 of Alliant Energy November 2022 Investor Presentation). But if the company isn't able to get the green light from regulators to pass the increased interest expenses to customers, it could be harmed in the near term.

The other risk to Alliant Energy is that the Federal Reserve could end up plunging the economy into a recession if it mismanages monetary policy. This would hurt the company's industrial and commercial customers if it were to occur.

A Wonderful Utility At A Fair Valuation

When dealing with slower-growing businesses like Alliant Energy, it's especially important to not meaningfully overpay for ownership stakes. That's why I'll be using two valuation models to estimate a fair value for shares of Alliant Energy.

Investopedia

The first valuation model that I will utilize to appraise Alliant Energy's shares is the dividend discount model or DDM, which consists of three inputs.

The first input for the DDM is the expected dividend per share, which is another term for the annualized dividend per share. This amount will soon be $1.81, so I will use that for this input.

The next input into the DDM is the cost of capital equity, which refers to the annual total return rate that an investor requires from their investments. My personal preference is for 10% annual total returns.

The final input for the DDM is the long-term DGR or annual dividend growth rate. As I referenced in the dividend section above, I believe that a 6.75% annual dividend growth rate is achievable.

Plugging these inputs into the DDM, I get a fair value of $55.69 a share. This implies that shares of Alliant Energy are trading at a 0.6% discount to fair value and offer a 0.6% upside from the current price of $55.35 a share (as of January 6, 2023).

{kind=link}

The second valuation model that I will employ to approximate the fair value of Alliant Energy's shares is the discounted cash flows model or DCF model. This also is made up of three inputs.

The first input into the DCF model is earnings over the last four quarters. In the case of Alliant Energy, this amount is $2.69.

The second input for the DDM is growth assumptions. I will assume a 6% annual non-GAAP EPS growth rate through the next five years and use 5% thereafter.

The third input into the DCF model is the discount rate. I'll again use 10% for this input.

Using these inputs for the DCF model, I come out to a fair value output of $58.99 a share. This means that shares of Alliant Energy are priced at a 6.2% discount to fair value and can provide 6.6% capital appreciation from the current share price.

When I average out these two fair values, I compute a fair value of $57.34 a share. This suggests that Alliant Energy's shares are trading at a 3.5% discount to fair value and offer a 3.6% upside from the current share price.

Summary: A Proven Dividend Growth Stock With Decent Total Return Potential

Raising a dividend for two consecutive decades requires world-class quality. And this is exactly what Alliant Energy can provide its shareholders. The company's dividend is well-covered and its earnings are consistently growing.

The cherry on top is that Alliant Energy's shares are trading at a roughly 3% discount to fair value. The company's trifecta of its yield, growth potential, and small valuation upside could lead to double-digit annual total returns over the next five- to 10 years. This makes Alliant Energy an interesting pick for dividend growth investors without skimping on total returns.

For further details see:

Alliant Energy: Buy This Blue-Chip Stock For Growing Passive Income And Strong Returns