LNT - Alliant Energy: Time To Consider Buying This Blue-Chip Dividend Stock

2023-11-03 16:31:26 ET

Summary

- Utilities can be part of a portfolio geared toward reliable dividend growth.

- Thanks to its capital growth spending plans, Alliant Energy is a utility with a healthy growth outlook.

- The company's investment-grade credit rating can help to fund the electric and gas utility's growth ambitions.

- Per Dividend Kings' fair value and my inputs into the dividend discount model, Alliant Energy is trading at a double-digit discount to fair value.

- The stock could deliver market-beating annual total returns in the next 10 years in my view.

Though they're not exciting, regulated utilities are some of the most consistent performers in the investment universe for dividend growth. That's because regulated utilities operate in an oligopoly-like business. Unless it has billions of dollars in capital and utility industry veterans, a startup in somebody's garage isn't going to compete with well-established utilities.

As a dividend growth-oriented investor, this is why I own nine utility stocks in my portfolio. One of them that I especially like is Alliant Energy ( LNT ). For the first time since January , please allow me to elaborate further on why.

{kind=link}

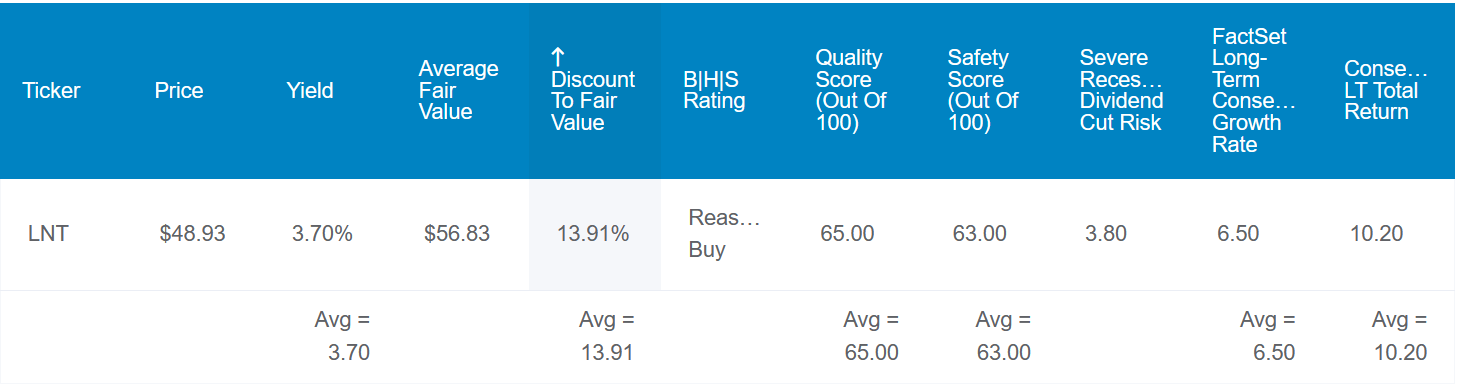

Alliant Energy's 3.7% dividend yield isn't going to stand out in this high interest rate environment. But with the EPS payout ratio clocking in at 62%, the electric and gas utility's payout ratio is well below the 75% that rating agencies like to see from utilities.

Alliant Energy's A- credit rating from S&P on a stable outlook makes it an excellent pick for capital preservation. This is because the implied probability of the company going bankrupt in the next 30 years based on its credit rating is just 2.5%. Put another way, in 39 out of 40 scenarios, Alliant Energy most likely won't close its doors by 2053.

The stock also looks to be trading at an appealing valuation. Averaging out historical yield, P/E ratio, and other valuation measures, the stock's $51 share price is trading 11% below its $57 fair value per Dividend Kings (as of November 2, 2023). Plugging in Alliant's $1.92 annualized dividend per share, a 10% discount rate, and a 6.5% annual dividend growth rate into the dividend discount model, I get a similar $55 fair value.

Considering these variables, here's what the stock could generate for total returns in the coming 10 years (assuming earnings increase as expected and the valuation multiple reaches fair value):

- 3.7% yield + 6.5% FactSet Research annual growth outlook + 1.2% annual valuation multiple upside = 11.4% annual total return potential or a 194% cumulative total return versus 10.2% annual total return prospects for the S&P 500 ( SP500 ) or a 164% cumulative total return

A Great Utility With A Viable Plan For Growth

Alliant Energy September 2023 Investor Presentation

{kind=link}

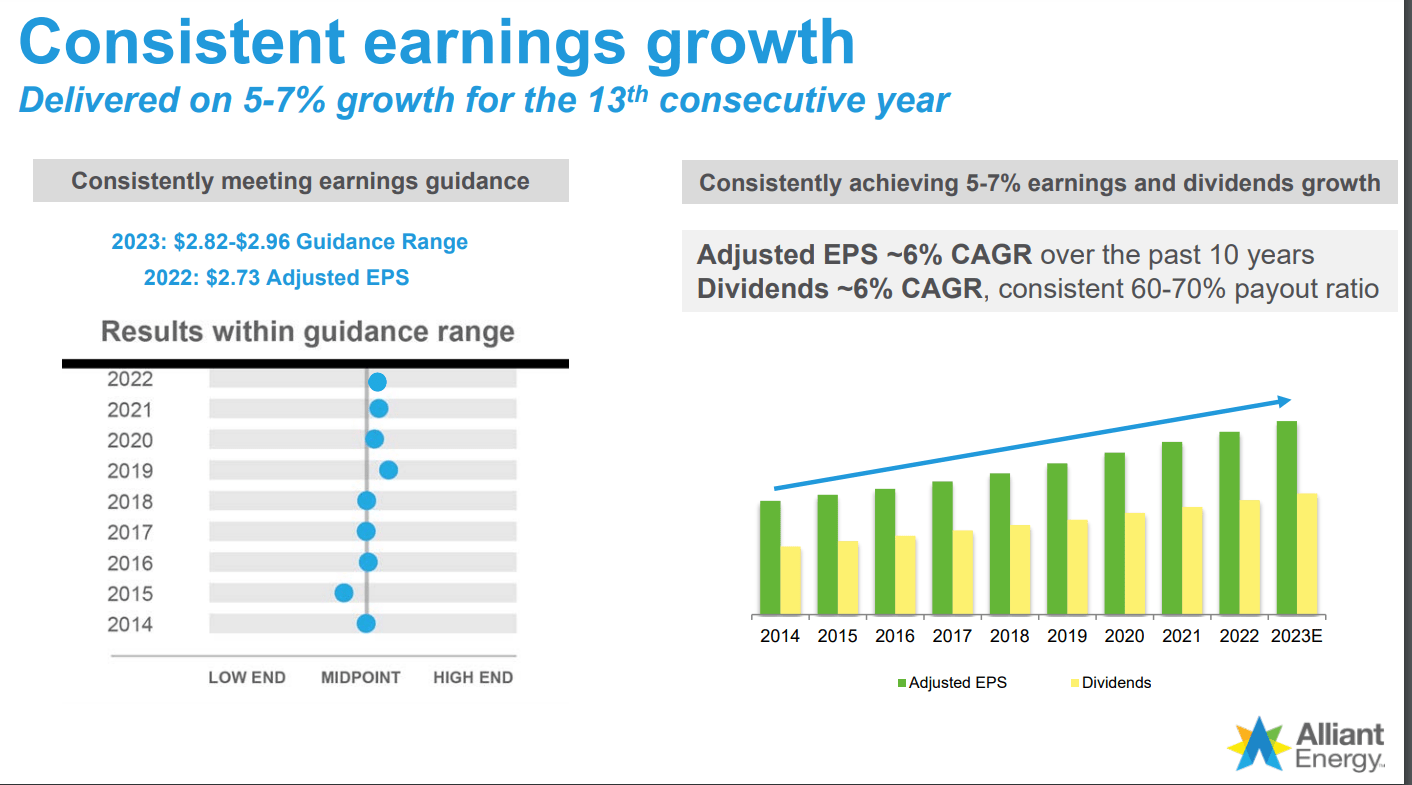

The biggest reason for investing in utilities overall is for reliability. Alliant Energy shines in this regard. The company is on track for its 13th straight year of producing 5% to 7% adjusted EPS growth for its shareholders. Alliant Energy's $2.89 midpoint adjusted diluted EPS guidance for 2023 would be 5.9% growth over 2022 - - firmly within its long-term targeted range.

The company's results through the first nine months of 2023 were good enough that management was confident enough to narrow guidance from $2.82 to $2.96 to $2.85 to $2.93 (for the same $2.89 midpoint). Also, Alliant Energy issued guidance for 2024. As a testament to its steadiness as a business, the company expects $3.06 in midpoint adjusted EPS. That's a 5.9% growth rate over 2023 as well (slide 3 of 9 of Alliant Energy's Q3 2023 Earnings Presentation ).

Alliant Energy September 2023 Investor Presentation

{kind=link}

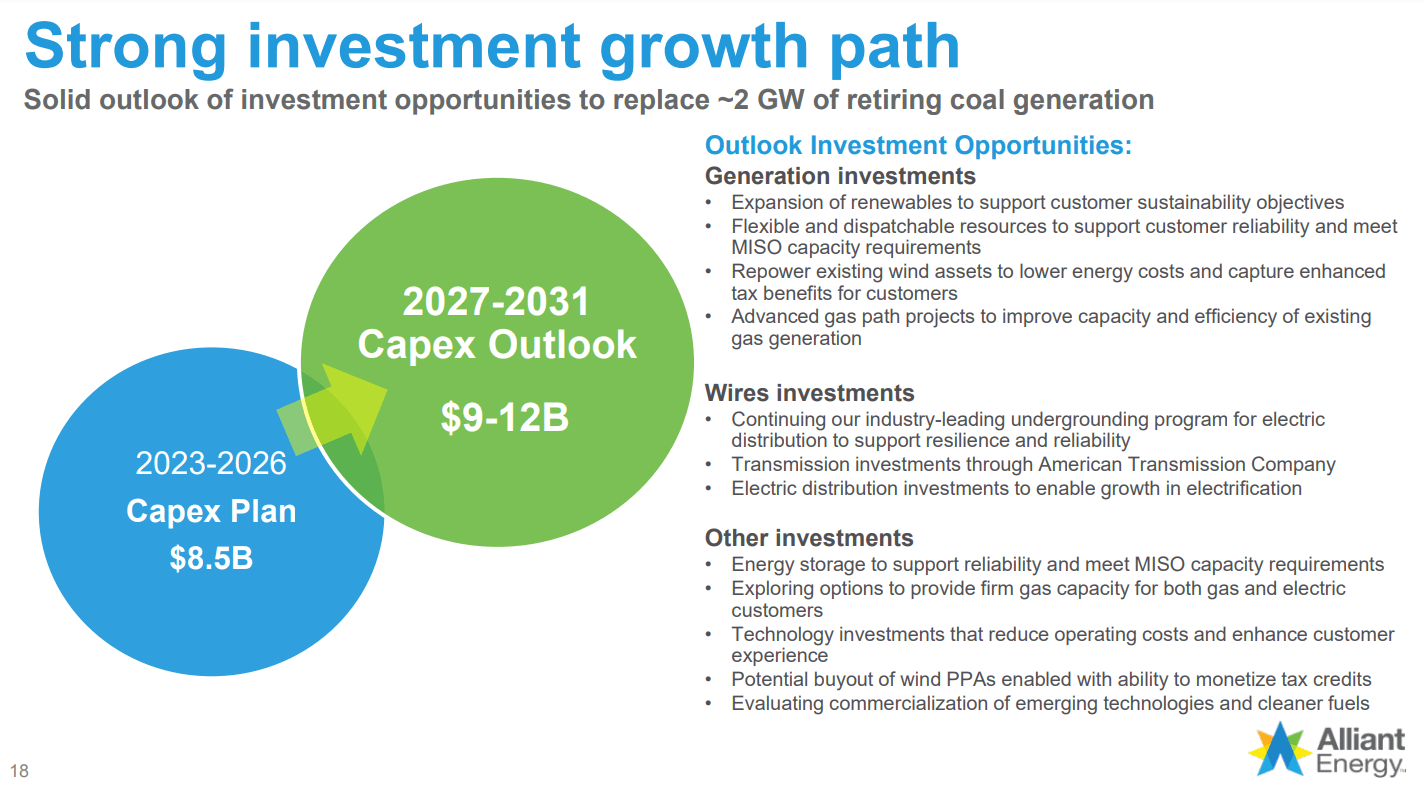

Moving forward, the company should have the ability to keep growing adjusted EPS at a mid to high-single-digit rate annually. This is because Alliant Energy plans on spending $8.5 billion on renewable generation and battery storage, electric distribution, and flexible, dispatchable generation between 2023 and 2026. This is why the company's rate base is expected to grow by about 8% annually during that time from $13.2 billion in 2023 to $17.9 billion in 2027 (per slide 4 of 9 of Alliant Energy's Q3 2023 Earnings Presentation).

Alliant Energy also upped its capital spending outlook for 2024 to 2027 by $600 million: The utility is poised to spend $9.1 billion during that time, which will both modernize its infrastructure and expand it to serve more customers.

Due to these reasons, the FactSet Research adjusted EPS annual growth consensus of 6.5% seems to be reasonable. But can Alliant Energy pull off its capital spending plan financially?

The answer appears to be yes. That is because aside from billions in retained earnings that can be used to fund its projects, the company can lean on its robust balance sheet to issue debt on favorable terms. In September, Alliant Energy issued $300 million in debt maturing in 2033 at a 5.7% rate. This is an especially attractive rate considering that the 10-year U.S. treasury currently yields 4.7% .

As the company's rate base grows, so too will its earnings. That is what makes the utility's moderately growing debt load manageable.

Dividend Growth Should Remain Healthy

Alliant Energy's dividend has grown for 20 consecutive years. Fortunately, this impressive dividend growth streak appears primed to continue.

Alliant Energy expects midpoint adjusted EPS of $3.06 in 2024. Against the $1.92 in dividends per share to be paid in 2023, that works out to a 62.7% payout ratio. That's well within the company's 60% to 70% payout ratio that it targets, which should leave room for dividend growth slightly ahead of earnings growth.

Risks To Consider

Thanks to its proven track record as a utility and low cost of capital, Alliant Energy enjoys a 10/13 quality rating from Dividend Kings. That makes it an above-average quality business. Yet, the company does face risks that investors need to know before buying.

A risk in the near term is that interest rates look like they will need to remain high for the foreseeable future. Since utility stock performance is correlated with risk-free rates, Alliant Energy could continue to underperform over the next year or two. The company also has $909 million in debt maturities for 2024 (per page 78 of 135 of Alliant Energy's 10-K ), which will probably be refinanced at higher rates. This could result in higher interest expenses, which would eat into the company's earnings.

Another risk to Alliant Energy is that as a regulated utility, regulatory authorities may not approve rate cases that the company files. This could also weigh on growth prospects in the future.

Summary: The Long Term Risk/Reward Is Compelling

{kind=link}

Alliant Energy is an all-around good utility. Investors who want a predictable dividend payer with decent growth potential should consider the utility for their portfolios.

Now is an especially attractive time to do so, with shares of Alliant Energy trading at an 11% discount to fair value. While not a huge margin of safety, I believe it's adequate for one of the better utilities out there. That is why I'm comfortable reiterating my buy rating for Alliant Energy here at $51 a share.

For further details see:

Alliant Energy: Time To Consider Buying This Blue-Chip Dividend Stock