ALIZY - Allianz: A Healthy Level Of Caution Is Advised

2023-04-27 08:31:16 ET

Summary

- Allianz reported solid results for fiscal 2022 and is also rather optimistic for fiscal 2023.

- And while financial institutions are still reporting healthy results in the first quarter, I would be very cautious right now.

- The stock could be undervalued, but I see very limited upside potential at this point and would not invest in financial institutions at this point.

In my last article published at the end of October 2022, I was bullish about Allianz ( OTCPK:ALIZF ) and although I saw the risk of lower share prices in the months and quarters to come that did not happen (at least not until now). Instead, Allianz gained almost 30% and clearly outperformed the S&P 500 ( SPY ).

And not only due to the higher stock price, we should take another look at Allianz. Considering recent developments - especially collapsing financial institutions in the United States and Switzerland - we must ask once again if Allianz is a good investment. The stock declined in the week the SBV collapse happened but performed well in the following weeks (compared to other banks) and we can therefore conclude that investors don't seem to be worried about Allianz. I, on the other hand, see the stock market on the brink and the banking crisis is just the next domino falling.

Annual Results

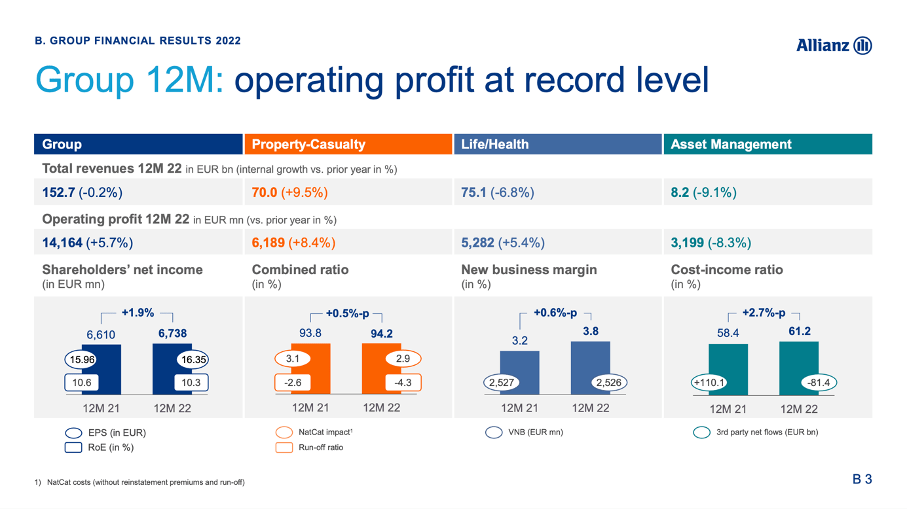

When talking about Allianz we can start by looking at the income statement and results for fiscal 2022, which can be seen as solid. Total revenue increased 2.8% year-over-year from €148.5 billion in fiscal 2021 to €152.7 billion in fiscal 2022. Operating profit increased 5.7% year-over-year from €13,400 million in fiscal 2021 to €14,164 million in fiscal 2022. Diluted earnings per share also increased slightly from €15.83 in fiscal 2021 to €16.26 in fiscal 2022 - 2.7% YoY growth.

Return on equity declined slightly from 10.6% in fiscal 2021 to 10.3% in fiscal 2022 and Solvency II capitalization ratio declined from 209% in the previous year to 201% in fiscal 2022.

And for fiscal 2023, Allianz is expecting operating profit to be similar to fiscal 2022 (around €14.2 billion). However, Allianz has a target range of €1 billion higher or €1 billion lower, which would result in either 7% decline or 7% increase.

{kind=link}

When looking at the three different segments, only Property-Casualty could report growing revenue (increasing 9.5% YoY to €70 billion) with the other two segments reporting declining revenue. Sales for the Life/Health segment declined 6.8% to €75.1 billion and revenue for Asset Management declined 9.1% YoY to €8.2 billion. And while Asset Management also had to report a declining operating profit (8.3% decline to €3,199 million), operating profit for Life/Health increased 5.4% YoY to €5,282 million and operating profit for Property-Casualty increased 8.4% YoY to €6,189 million.

Balance Sheet

Aside from the income statement, we should also take a look at the balance sheet. And in the last twelve months, the balance sheet got worse - we are comparing the balance sheet on December 31, 2022, to one year earlier and total equity for Allianz declined from €84,222 million one year earlier to only €55,242 million. Total assets also declined from €1,139 billion at the end of 2021 to €1,022 billion at the end of 2022.

And while the turmoil was especially in the banking sector (and mostly affecting regional banks in the United States), we should also be cautious regarding Allianz. Aside from its insurance business, Allianz was also generating about 23% of its operating income from its asset management business. And of course, Allianz is not facing the risk of a bank run (which brought Silicon Valley Bank to its knees), but investors can also pull out investments.

{kind=link}

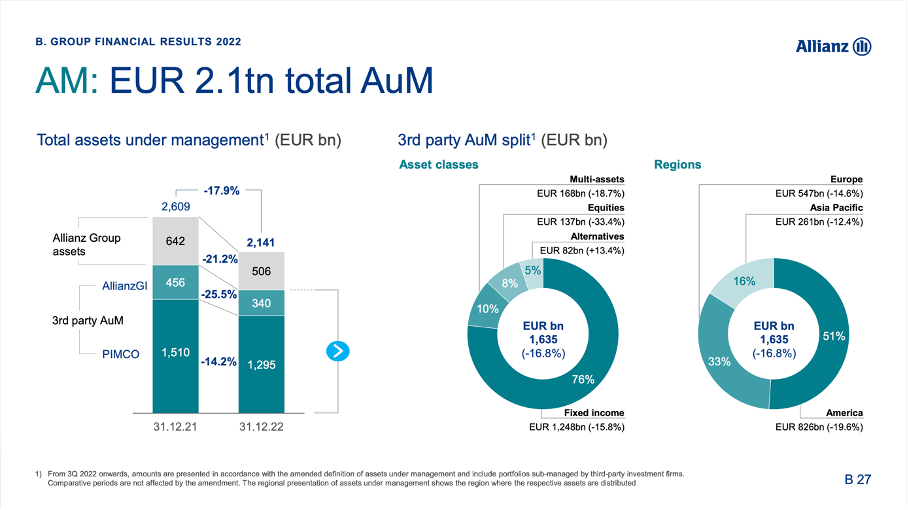

When looking at investments under management, we see a decline of 17.9% year-over-year from €2,609 billion in AUM to only €2,141 billion right now. And third-party assets under management declined from €1,966 billion in fiscal 2021 to €1,635 million in fiscal 2022. The biggest part of this decline is stemming from lower prices for most assets, but Allianz also had to report €81 billion in third part net outflows.

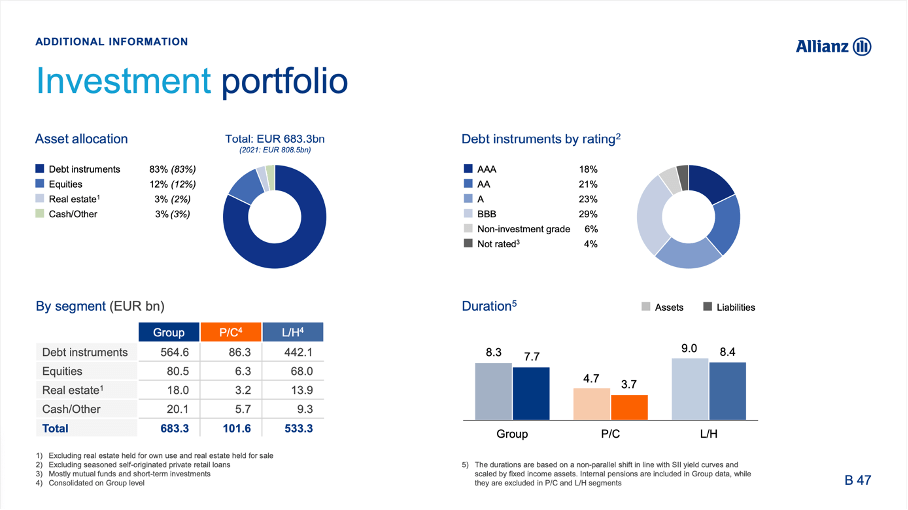

The investment portfolio also declined from €808.5 billion at the end of fiscal 2021 to €683.3 billion at the end of fiscal 2022. The biggest part is still debt instrument (accounting for 83% of assets) with about two third being A-rated (either AAA, AA or A).

{kind=link}

Overall, a declining investment portfolio or lower assets under management are not alarming and it doesn't also imply huge problems for Allianz right away. And while we must not fear solvency or liquidity problems, outflows and lower assets under management will have a negative effect on the profitability of Allianz.

Recession

And when looking at the performance of Allianz in the past decades, the results were fluctuating quite heavily. But despite these fluctuations one pattern is quite obvious: Allianz was always performing well and reported great results in the years before a bear market and recession but during recessions the results were often terrible. In 2002 and 2008, Allianz even had to report a loss.

Allianz is certainly a great and solid business, but it is not recession resilient. In the chart above, I marked the years before the economy entered a recession (in dark blue) and we can clearly see that results declined in every one of the last four recessions. And while the results in 1992 and 2020 were still acceptable, the results during the Great Financial Crisis and the years following the Dotcom bubble were horrible.

And right now, it seems again as if the world economy is on the eve of a global recession and although Allianz did not see the impressive growth rates leading up to the year 2000 and again to 2007, we should be cautious as 2022 might be similar and 2023 and/or 2024 could see much lower earnings per share. In my last article I already explained why a recession has a negative impact on Allianz:

And when the bear market is getting worse (and in my opinion, it will get worse over the next few quarters), assets are probably withdrawn for different reasons (i.e., panic, liquidity) and declining asset prices will also lead to shrinking total AuM for Allianz.

And when talking about a potential recession, bear market and a potential banking crisis we should also not ignore that the results in the first quarter so far are looking quite good for financials. According to FactSet , financials are one of the best performing sectors and the financial institutions that reported so far, increased revenue by 10.5% year-over-year and earnings 5.4% year-over-year. Talking about a banking crisis in light of these results might seem a bit absurd. I would also like to mention Howard Mark's latest memo " Lessons from Silicon Valley Bank " in which he argued that the SVB collapse might rather be an outlier and he is seeing the risk for a second Great Financial Crisis rather low. And who am I to disagree with Howard Marks - nevertheless, I would not be so optimistic. While I might be a little more pessimistic about the outlook for the banking sectors, Howard Marks seems to have a similar opinion about the direction of the economy and the markets and is expecting rough times ahead .

Growth

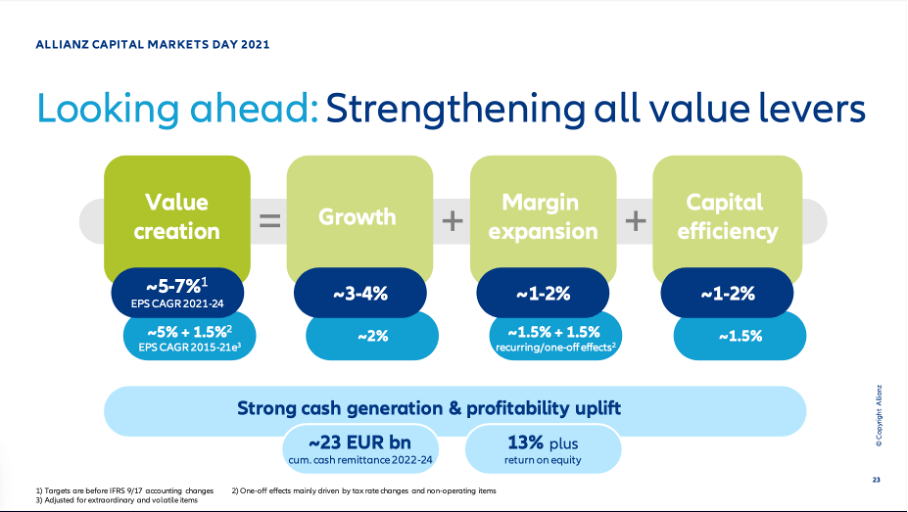

And while we should be rather cautious, management was rather optimistic during its 2021 Capital Markets Day. The bottom line growth target was 5% to 7% growth, which was mostly stemming from organic growth, but also from margin expansion as well as capital efficiency.

Allianz Capital Market Day 2021 Presentation

{kind=link}

During the earnings call , CFO Giulio Terzariol was also optimistic that Allianz will beat its own outlook for fiscal 2023 - as it has in most years in the past:

And as you know, we have a track record to beat the outlook. It happened all the time, except in 2020 when we had COVID. So I believe history has a tendency to repeat itself. So I will say that most likely we're going to be better than this number.

Analysts are also optimistic for 2023 and are expecting much higher earnings per share (close to $24 earnings per share). I however would be rather skeptical - especially for fiscal 2023 as well as fiscal 2024. For the years after the potential recession, I think these growth rates are realistic.

And while I am rather pessimistic for the coming quarters (and maybe next two or three years), I also expect that Allianz will be able to grow in the mid-single digits over the long run. As I said above, the results of Allianz were fluctuating quite heavily over time and when calculating long-term growth rates, it depends quite a lot on which year one is taking as starting point. When taking 2007 for example as starting point, we must state that Allianz saw earnings decline slightly over the last 15 year - but this is not an accurate description of Allianz as 2007 was rather an extreme outlier.

| Growth |

| Since 2017 |

| Since 2012 |

| Since 2005 |

| Since 2004 |

| Since 1997 |

| Since 1992 |

| Since 1987 |

| EPS CAGR |

| 1.42% |

| 3.65% |

| 2.23% |

| 5.72% |

| 5.86% |

| 9.48% |

| 8.74% |

But I think growth rates in the mid-single digits are realistic for Allianz in the long run.

Dividend

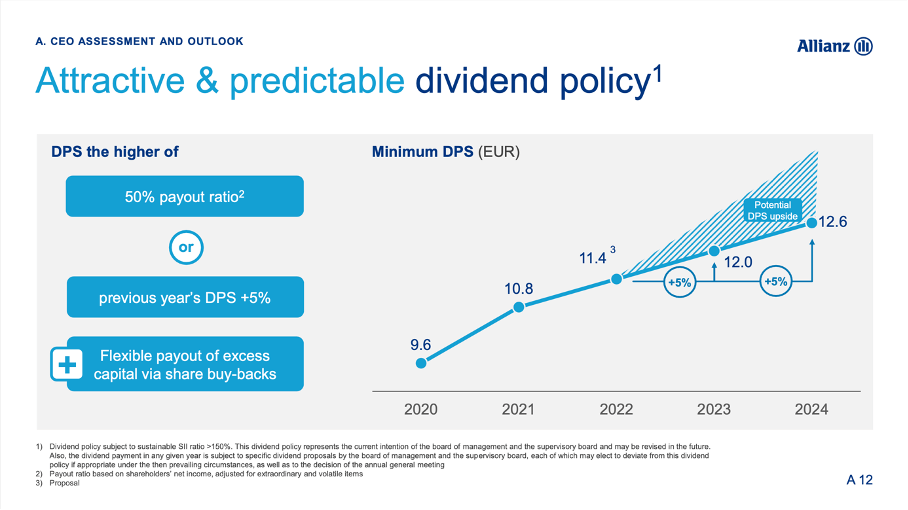

Allianz also proposed a dividend of €11.40 per share and compared to €10.80 in the previous year this is reflecting a 5.6% YoY increase. Management is also predicting dividend growth in the years to come, and Allianz will increase its dividend at least 5% annually resulting in an expected dividend of at least €12.00 in fiscal 2023 and €12.60 in fiscal 2024.

{kind=link}

Right now, Allianz has a dividend yield of 5.1% and although the dividend yield was already higher for Allianz in the past, this is still a very attractive dividend yield. A problem, however, is the rather high payout ratio. The current dividend is resulting in a payout ratio of 70% when using the fiscal 2022 earnings and as Allianz is targeting a payout ratio of 50% the current dividend is clearly above the target range.

{kind=link}

And since 2008, Allianz increased the dividend from €3.50 to a proposed dividend of €11.40 in fiscal 2022 - this is resulting in a CAGR of 10.34%. By the way, Allianz goes ex-dividend on May 5, 2023, and investors can still profit from the dividend.

Intrinsic Value Calculation

When trying to calculate an intrinsic value for Allianz or determine a price target, we can start by looking at the price-earnings ratio. Using the earnings per share for fiscal 2022 (which were €16.26), Allianz is trading for a P/E ratio of 13.7 right now. While this is not a high valuation multiple in absolute terms, it is a rather high valuation multiple for financial corporations (and many major banks are trading for much lower valuation multiples right now).

Nevertheless, I would not call Allianz overvalued and when calculating an intrinsic value by using a discount cash flow calculation we will reach the same conclusion. As always, I will calculate with 10% discount rate as well as 403.3 million outstanding shares. Let's make the following assumptions: For fiscal 2023, we assume €0 net income (although I don't think this is realistic, it is just a way to reflect a recession in the calculation - it could also happen in 2024). For the following year we assume half of the net income of fiscal 2022 and for 2025 we assume a full recovery (same net income as in fiscal 2022). In the years after 2025 we assume Allianz will continue its path of low-to-mid-single digit growth and different growth rates lead to different intrinsic values.

| 2% growth |

| 3% growth |

| 4% growth |

| 5% growth |

| Intrinsic Value |

| €191.34 |

| €217.63 |

| €252.67 |

| €301.73 |

So, depending on what growth rates we see as realistic in the years to come, Allianz might be slightly overvalued, or it could even be undervalued.

Conclusion

I would be cautious about Allianz for several reasons. The stock does not appear expensive, but Allianz is facing a similar problem as many banks and when looking at the last recessions, we must expect the stock to decline quite steep in case of a recession or bear market. Additionally, Allianz is at a major resistance level, and I think Allianz will have troubles to break above this resistance level in the current market environment.

And we should always keep in mind that the first quarter of fiscal 2023 is not reflected in any results. Allianz will provide information for the first quarter on May 12, 2023, and it remains to be seen if any negative effects are already visible (probably not as most financial institutions reported solid results so far).

For further details see:

Allianz: A Healthy Level Of Caution Is Advised