ALIZY - Allianz: Solid 2023 Start

2023-05-16 08:23:43 ET

Summary

- Economic reinvestment yield is now at 4.0% thanks to changes in the interest rate environment.

- The P/C division benefitted from a better-combined ratio.

- Solid balance sheet and a new buyback plan. Our buy rating is then confirmed.

Allianz ( OTCPK:ALIZF , OTCPK:ALIZY ) has always been a Mare Evidence Lab's buy target opportunity, and as already mentioned in our ' Long-Term Opportunity ' follow-up note, 2022 was a challenging year. Despite that, the German insurance company managed to resolve the U.S. government investigations concerning Structured Alpha and be back on track to generate profits - this was also emphasized in our Fiscal Year 2022 and Q4 update titled ' Significant Headwinds Resolved '.

{kind=link}

Mare Evidence Lab's previous analysis

Our buy case recap was supported by 1) a solid track record with a history dating back to 1890, 2) the company's " attractive and predictable dividend ", and 3) the PIMCO Division upside coupled with higher reinvestment yield.

Related to the higher interest rates environment, we should mention a change of paradigm in the last 10 years . In detail, in a world with negative interests, insurance companies have always gotten better at managing costs to sustain more operating profit. In the past, insurer players were outperforming thanks to investment activities (reinvestment yield) and not the core operating activities. This is why one of our key metrics to check was the combined ratio ((CR)) quarterly evolution. This metric divides the incurred losses and expenses by the earned premium. A CR lower than 100% means a company that is profitable. Currently, here at the Lab, we are long in the insurance sector due to a double profit generation 1) higher reinvestment yield and 2) better CR evolution.

The other tangible growth driver is the Allianz Asia Pacific operation. The Asian operation is expected to significantly growth over the course of the next decade. The group was targeting 5% of the total operating profit; however, management expected to increase this number to €1 billion in 2024 and by €2 billion in 2030.

Region growth drivers are well understood and the German player is already ahead of distribution capabilities versus its competitors. Allianz is now focused on building its distribution capability thanks to its multi-channel strategy. In addition, there is a plan to grow its local agency presence. In APAC, Allianz has passed from a 70/30% split in bancassurance vs agency to closer to a 50/50% split. In China, the company also has a JV in P&C and fully owns its life and asset management entities . Allianz is currently present in 8 provinces but is expanding the agency distribution in order to maximize the bancassurance opportunities it has.

Q1 update

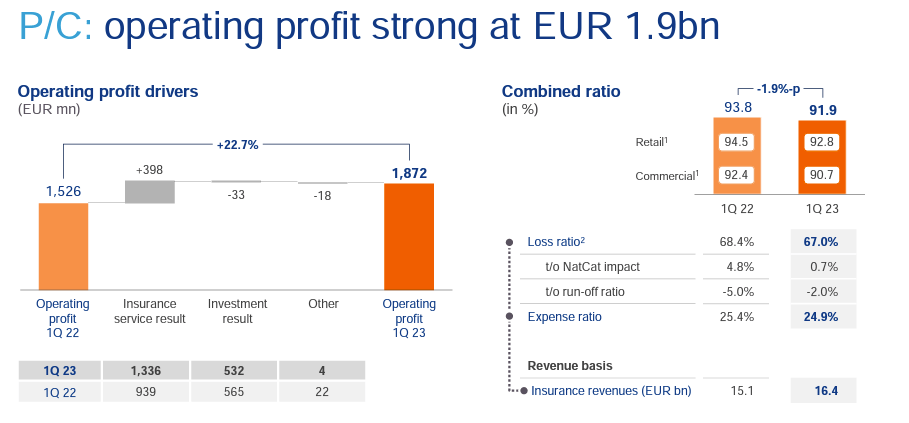

Before commenting on our metrics, it is important to report that Allianz reported total volumes up by 3.9% to €46.0 billion. This was well supported by P&C and L/H divisions thanks to solid pricing power, while the Asset Management segment performance was offset by lower AuM-driven turnover.

The CR signed a remarkable plus 1.9% to 91.9% (it was at 93.8% in Q1 2022). The loss ratio benefited from lower natural catastrophes claims and the expense ratio was better by 0.5% to 24.9% (Fig 1). The economic reinvestment yield reached 4.0% (Fig 2) and fully benefit from the yield environment changes. Duration for assets declines and during the Q&A call, we understood that the latest debt securities investment was at almost 4.6% yield from the 3.2% recorded in 2022. Therefore, we are not surprised to report that Allianz reported an outstanding performance in Q1 2023. In numbers, the core operating profit accelerated by almost 25% to €3.7 billion and the shareholders’ net income reached €2.2 billion.

CFO confirmed our investment key takeaways, in detail, he explained how Allianz (once again) " benefited from its diversified business mix and delivered a particularly strong performance in the Property-Casualty segment, driven by a robust pricing, continued underwriting discipline and focus on further productivity gains".

{kind=link}

Allianz combined ratio evolution

Source: Allianz Q1 results presentation - Fig 1

Allianz reinv. yield evolution

Fig 2

Conclusion and Valuation

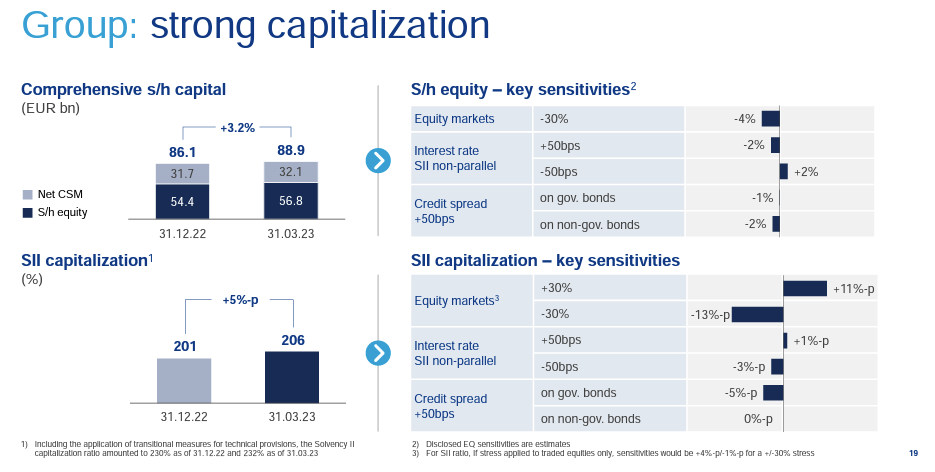

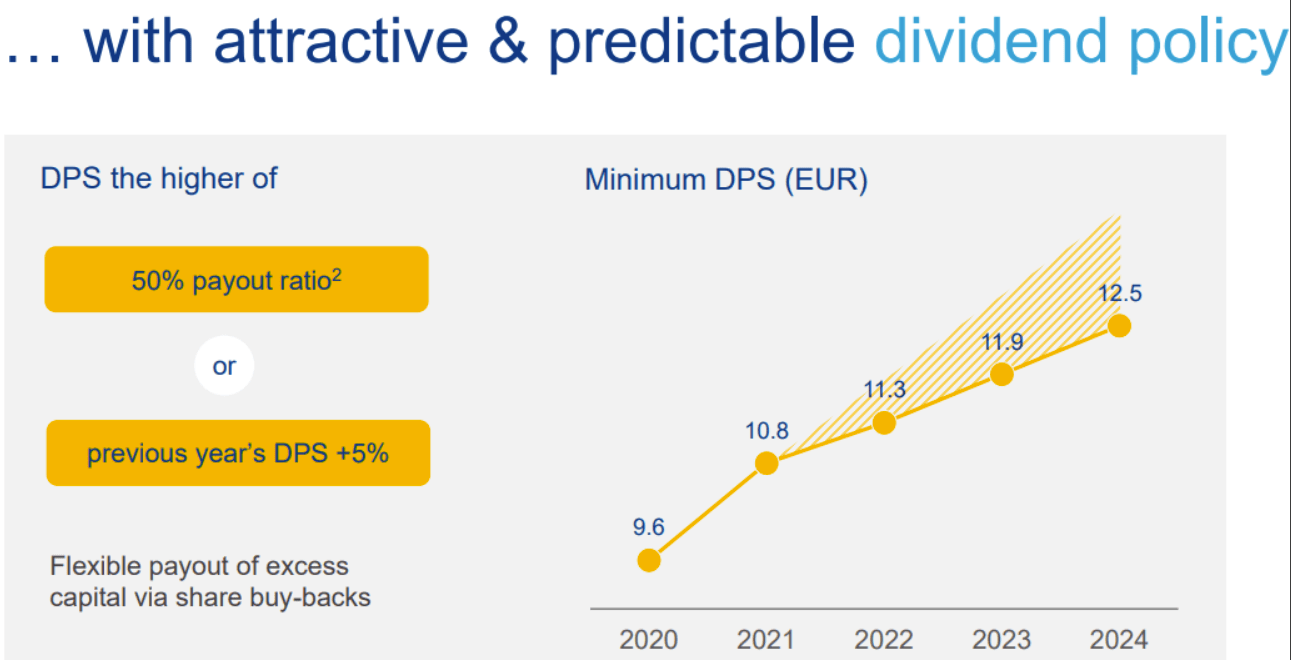

Important to report is the positive evolution of Allianz's Solvency II capitalization ratio. In detail, the company recorded a 206% versus 201% achieved at 2022 end (Fig 3). Last year, the German insurer was impacted by the Structured Alpha Funds one-off, and at the EPS level, it reached €1.02 per share, while in Q1 2023, the company achieved an EPS of €5.43. With a €2.2 billion net profit, the company is set for a higher DPS for 2024 which will be a minimum of 50% payout ratio or the previous year's DPS plus 5% (Fig 4). If we are using a 5-year average at a Price Earning of 10x, we confirm Allianz's buy rating at €220 per share ($23.4 in ADR). Last time, our buy target was more skewed on a neutral valuation; however, after this solid Q1, we are currently more confident. Important to note is the new share repurchase program up to €1.5 billion. This will support Allianz's stock price appreciation.

{kind=link}

Allianz SRII update

Fig 3

{kind=link}

Allianz DPS construction

Fig 4

For further details see:

Allianz: Solid 2023 Start