ALSN - Allison Transmission: More Gains On The Cards

Summary

- Company beats EPS estimates with ease in Q3.

- Guidance gets raised on strong demand.

- We may look to get long here on a convincing swing low.

Intro

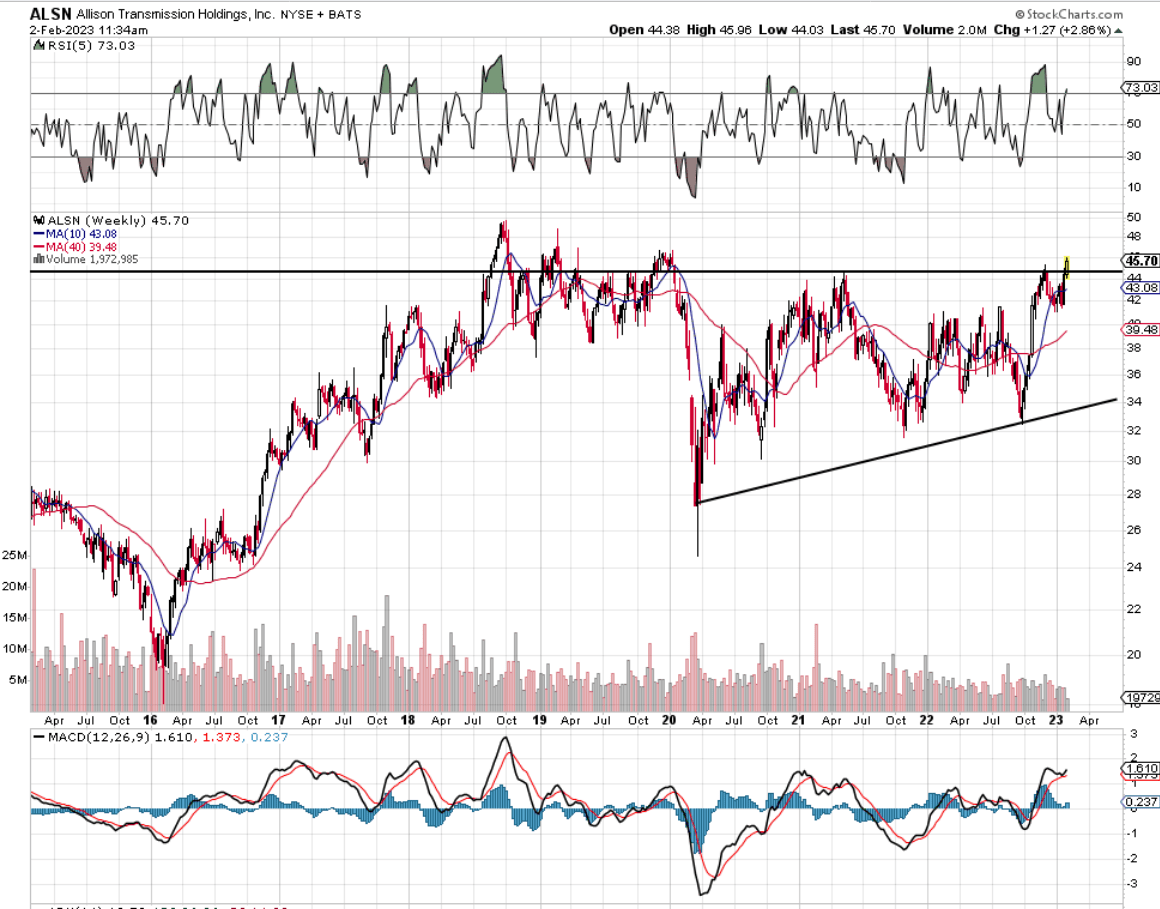

If we pull up an Allison Transmission Holdings, Inc. ( ALSN ) intermediate chart, we can see that shares are potentially undergoing a 3+ year-long ascending triangle which indicates accumulation. These patterns irrespective of where they show up on technical charts are invariably bullish. What interests us from a technical standpoint is the height of the triangle which comes in at almost $16 a share. Triangle heights give forecasting implications and recent news definitely lends to Allison's bull case remaining intact.

{kind=link}

Multiple Partnerships

In fact, if we revisit Allison's third-quarter earnings numbers, we see that the company reported strong beats on both the top (Sales of $710 million) and bottom line (GAAP earnings of $1.45 per share). Shares gapped up on the news but news since then leads us to believe that earnings will continue to grow meaningfully going forward. Firstly in early December, we had the announcement of the Abrams battle tank deal which was followed swiftly by the machinery upgrade by Morgan Stanley (MS). Then in the following month (January 2023), we received news of the Nikola (NKLA) partnership (Which will double down on the development of electric vehicles) as well as news on the Indian army using Allison's propulsion systems in its combat vehicles.

Q3 earnings

Furthermore, in the present environment where higher costs and supply chain headwinds continue to hurt manufacturing companies from a profitability standpoint, Allison on the contrary continues to go from strength to strength. In fact, in the recent third quarter, gross profit hit $328 million on sales of $710 million as mentioned resulting in a gross margin percentage of 46.2%. The important trend to note here is that Q3 gross margin remained in line with the trailing 12-month metric (46.9%) but yet sales grew by 25%. Therefore, when the income statement is showing robust top-line growth and margins are being maintained, this usually means significant bottom-line growth will result and this is what we got in Q3. In fact, net income increased by 47% to hit $138 million in the quarter and this number would have actually been higher were it not for an unrealized reported loss on marketable securities as well as increased spending.

When quarterly profits are generating positive cash flow, management then needs to efficiently allocate capital to ensure the company can continue its growth path if not accelerate it over time. Many times (especially in the initial innings of sustained investment), it can be difficult to surmise whether invested capital will result in solid gains for the company. Concerning Allison, the lion's share of its spending over the past four quarters has actually been in its own stock ($407 million from a free-cash-flow purse of $475 million) whereas only $189 million has been routed towards investment purposes.

The advantages here are two-fold. For one, heavily buying back company stock produces a guaranteed return on investment concerning earnings per share growth. To this point, the number of shares outstanding fell by approximately 11 million (10%+) over the past four quarters alone and continues to fall (The current Number is 92.49 million). Secondly, Allison continues to demonstrate that it does not need to spend big in order to maintain strong growth rates. Recent price increases have not adversely affected customer demand which is encouraging.

Valuation

The one area where investors may believe Allison is overextended is its balance sheet. Although shareholder equity ($762 million) continues to grow, the book multiple presents come in at 5.59. There are two points we would make concerning Allison's balance sheet. The first is that the earliest maturity of Allison's debt is in 2026. Therefore the $2.5 billion debt load is not impacting the income statement at present in an overly negative way (Trailing interest coverage ratio of 6.63). Secondly, that stagnant $2.5+ billion debt load will continue to lose its potency as company sales continue to rise. The CFO raised guidance on the Q3 earnings call due to resilient demand in many areas such as Global on and off Highway and service material, etc. Suffice it to say, by the time those maturities present themselves, Allison should be a totally different outfit in terms of net worth and the market is beginning to price this in.

Conclusion

Allison Transmission Holdings has all the hallmarks of being able to rise from its current share price. Sales growth combined with margin preservation continues to grow the bottom line. Let's see what Q4 numbers bring. We look forward to continued coverage.

For further details see:

Allison Transmission: More Gains On The Cards