ALSN - Allison Transmission: Plenty Of Room To Increase The Dividend

2023-10-19 15:35:43 ET

Summary

- Allison Transmission is a dividend growth stock with potential for future dividend hikes.

- The company has a wide customer and product range, allowing it to thrive in different market conditions and reduce cyclicality.

- Despite challenges in the past year, the company's profits have been growing due to improved margins and cost management.

- It has a compellingly cheap valuation and its low payout ratio will make it possible for the company to keep growing its dividends for years to come.

Allison Transmission ( ALSN ) produces, distributes and sells transmissions and other vehicle propulsion solutions for medium-duty and heavy-duty trucks ranging from school buses to armored military vehicles. This company is shaping up to be a pretty decent dividend growth stock and I believe that it has plenty of room to hike its dividends in the near future as well as the long term which could make it a buy for dividend growth investors.

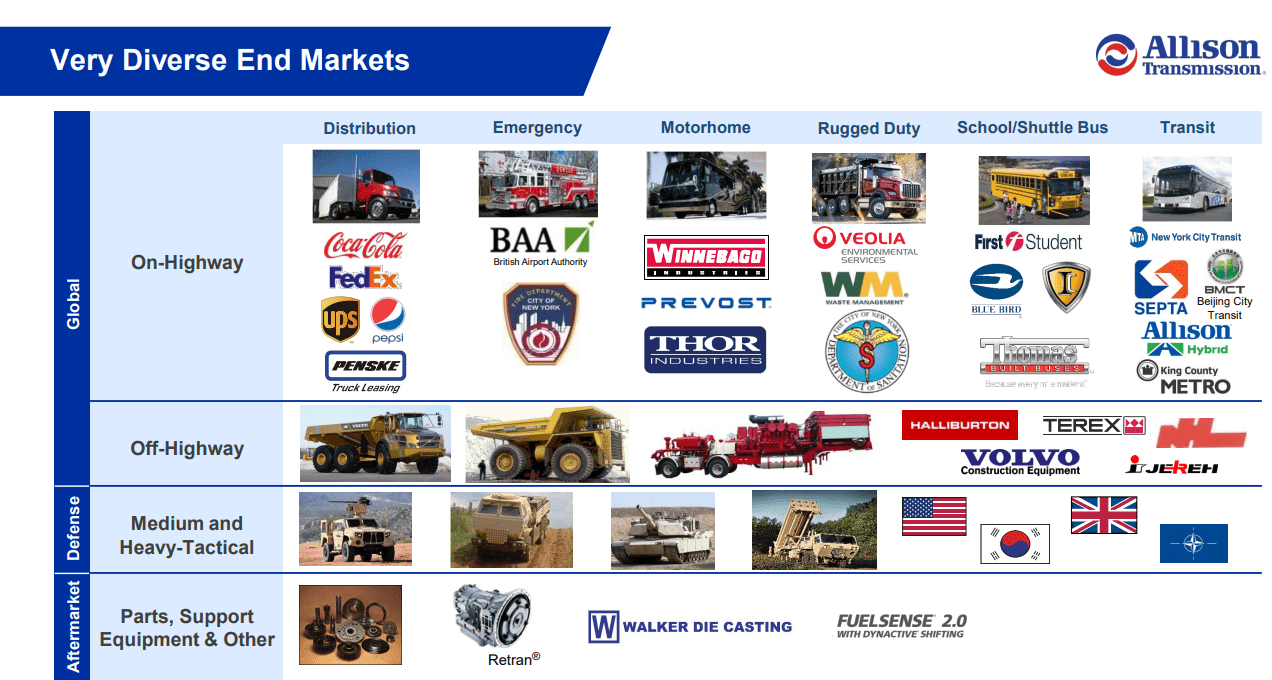

The company's customer and product range is very wide including school buses, fire trucks, RVs, construction machinery, agriculture machinery, city buses, semi-trucks and a variety of armored military vehicles such as tanks and infantry carriers. This type of diversification allows the company to survive and possibly thrive in all different market conditions and market cycles as the company's customers include cyclical and non-cyclical customers not to mention not all cyclical customers have the same cyclicality. The company is a global market leader in most segments that it operates in.

{kind=link}

Last year has been rather tough on the company as it had to deal with rising input costs, higher labor costs, supply chain issues and production disruptions but the company seems to be doing much better this year as most of those issues have been either resolved or their effects have been minimized.

In the long run, since the company's business is rather stable, its revenue growth has been somewhat slow and steady and mostly predictable but its profits (measured by EPS) have been growing at a much higher rate due to improving margins, better cost management, better product mix, more favorable contracts and being able to pass costs to customers.

Apart from those factors, another thing that absolutely helped the company grow its EPS was its stock buyback policy. In the last decade, the company's diluted share count shrank from 180 million to 90 million which is a pretty significant drop (50% to be exact). This means that each dollar the company generates in profits today is worth about $2 it generated a decade ago. Having fewer diluted shares outstanding has more than one advantage. Not only it allows the company to generate higher income but it also means there will be less shares to pay dividends on which will allow the company to grow its per-share dividends.

Which is exactly what's been happening. In the last decade, the company boosted its dividend payments by 92%. The company didn't exactly hike its dividends every single year and there has been periods where the dividend stayed flat but the general direction has been upwards, especially since 2019. There are two types of dividend growth companies. Those that grow their dividends every single year no matter what and those that grow their dividends over time even though they might skip hiking their dividends from time to time and this company falls into the second category. This doesn't make it less of a dividend grower though. I would much rather a company skip a few years of dividend hikes and hike it by 90% in a decade than a company that grows its dividends every single year but only hikes it by 40-50% at the end of the decade (of course that doesn't mean everyone should prefer it that way since preferences will vary by person depending on their investment profile and investment goals).

Having said that, this company currently has a low dividend yield even after growing its dividends significantly. The stock currently yields only 1.5% which doesn't make it a great stock for those who want to generate a high dividend yield. This stock is more for people who want to grow their dividends over time. Also, the reason the stock yields so little is because its share price had a pretty large rally from $35 to $60 earlier this year. This massive rally made a lot of investors happy but it reduced the dividend yield from 2.5% to 1.5%.

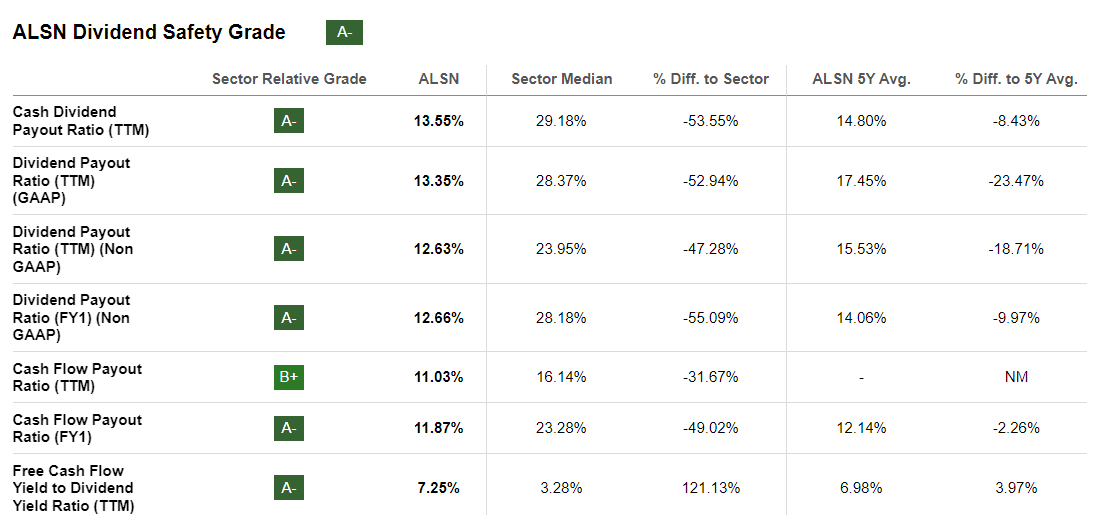

The company still has plenty of room to grow its dividends though. Currently the company's dividend safety grade at Seeking Alpha is A-. This is because of its low payout ratio and strong profitability which not only easily covers the current dividend but also allows for plenty of room for future dividend growth even if the company's growth slows down significantly. Currently the company's payout ratio is as low as 13% which is less than half of the sector median of nearly 30%. It's not low just this year either. The company's 5-year payout ratio average is 14.8% which is significantly below sector average. This means that the company is paying only 15 cents for each $1 it generates in net income. The company could easily double or triple its dividends from here without having to grow its earnings and possibly grow even more if its earnings keep growing. Also, the more shares the company buys back, the more room it will have for dividend hikes. Allison's cash flow payout ratio of 11% is even lower than its net income payout ratio.

{kind=link}

The company is very conservative and careful with its money and its very strategic about returning cash to investors in the form of dividends and stock buybacks.

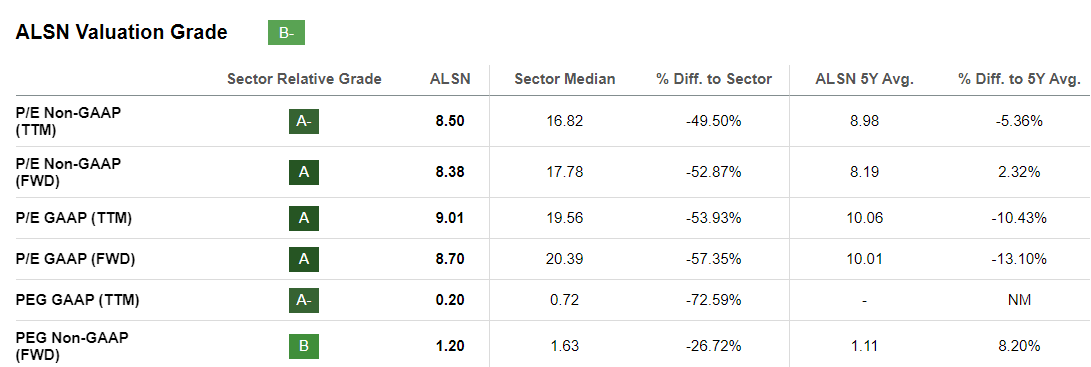

Despite having a pretty sizeable rally from $35 to $60 and almost doubling earlier this year, the company still enjoys a compelling valuation while it's trading at only 8 times its net income. The company's PEG ratio is 1.20. This is a metric you want below 2.0 because it shows you how richly valued a company is in comparison to its growth rate. Anything below 1 would be too cheap to ignore and anything between 1 and 2 would be compelling valuation. Valuation-wise manufacturing tends to be one of the cheaper sectors because this industry is highly cyclical and very capital intensive but this company trades at a 50% discount against its sector average which makes it even cheaper.

{kind=link}

The biggest risk in front of this company is rising labor costs. We've already seen labor disputes in big car companies like GM ( GM ) and Ford ( F ) who will have to raise its compensation and benefits significantly in order to keep their operations going. Manufacturing is a highly unionized industry and this company could also see rising labor costs in the future which could eat into its healthy profits and reduce the company's margins.

All in all, this is a good stock for dividend growth investors with its past dividend growth as well as potential future dividend growth and enjoys a cheap valuation even though its current dividend yield is not all that attractive at 1.5%.

For further details see:

Allison Transmission: Plenty Of Room To Increase The Dividend