ALSN - Allison Transmission: TINA (Still) Doesn't Live Here Though She's Closer

2024-01-02 14:00:28 ET

Summary

- Since I last wrote about Allison Transmission, shares have returned a loss of about 1.2% compared to a gain of 10.4% for the S&P 500.

- The dividend yield of 1.6% for Allison Transmission seems low compared to the 3.9% risk-free investment in Treasury Notes.

- The financial results for 2023 have been excellent, with revenue, operating income, and net income all showing significant increases.

Happy New Year. I hope everybody enjoyed their holidays as much as possible given everything. I’m glad to be back. Anyway, it’s been about 2 ½ months since I suggested that investors would be wise to buy 10-Treasury Notes instead of shares in Allison Transmission ( ALSN ). Since then, the shares have returned a loss of about 1.2% against a gain of 10.4% for the S&P 500. I should also point out that since the yield on the 10-Year Note has dropped about 1.2% since I wrote this article, the 10-Year Note has gained about 8%. Yes, stock investors, bonds can rise in price. Equally shocking: water is wet. Anyway, the company reported financial results just after I posted the article, so I thought I’d review those to see if it now makes sense to buy these shares, given that they’re about $1 cheaper than they were when I last reviewed the name. More importantly, since rates are lower, the delta between the risk-free rate and the dividend yield has obviously shrunk. That’s relevant to newer investors here.

My writing has been described as “a slog”, “a bit much”, “a bit extra”, and “too much to take.” I hear the people and I offer an alternative to needing to read through an entire one of my screeds. I offer a “thesis statement” to those people who want to understand my thinking, but who want to avoid the terrible jokes and proper spelling. You’re welcome. I’m of the view that the world of investing is innately relativistic, so we’re always looking for the best risk-adjusted returns, not simply “returns.” Given that it’s possible to earn 3.9% in a risk free investment at the moment , the paltry 1.6% dividend yield seems a bit slight, given the risks involved. In my view, investors acquire this stock as an income generator, tied to hopes of continued dividend growth. The issue for me is that in order to match the cash flows earned from the Treasury Note, the dividend would need to grow at a CAGR of about 10.8% over the next decade. That is significantly higher than the 6.8% rate at which the dividend grew since 2014. I think the relative merits of the stock and the Treasury Note have shrunk since last October, given the fall in Treasury yields, but I still think Treasuries offer a better risk adjusted return from here. I’ll check back on this name after they publish full year results, because if the yield on the Treasury Note continues to fall, TINA may move back in.

Financial Snapshot

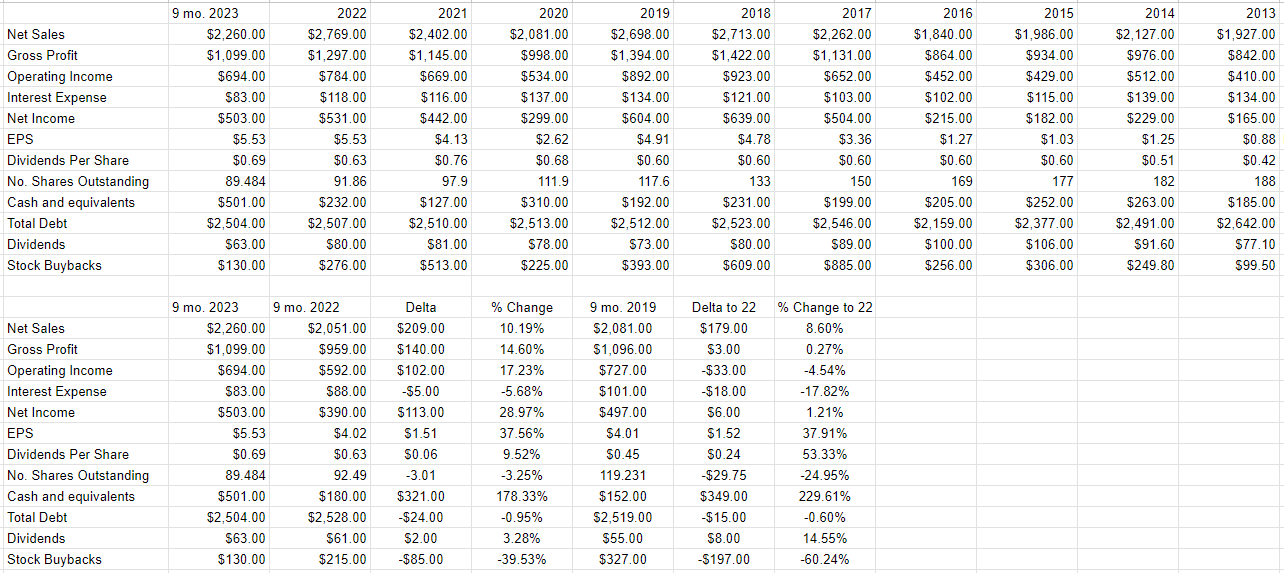

The financial results for 2023 have so far been excellent in my view. For instance, relative to the same period in 2022, revenue, operating income, and net income are up by 10.2%, 17.2%, and 29% respectively. Profits were up nicely in spite of significant upticks in cost of sales (up 6.3%), and SG&A expenses (up 14.72%). It could be said that Allison has returned to pre-pandemic levels, given that net income is up a whopping 1.2% compared to the same period in 2019. Management has rewarded shareholders handsomely, with a 9.5% uptick in dividends over the past year, and an increase of over 53% when compared to 2019. At the same time, the company has improved the balance sheet very nicely, with cash and equivalents up by $321 million, and long term debt down by $24 million. In my view, the ~$80 million the company spends on dividends is reasonably well covered here.

Allison Transmission Financials (Allison Transmission investor relations)

{kind=link}

The Stock

The world of investing is innately relativistic. We have limited capital, so when we buy investment “A”, we are, by definition, eschewing any number of investment “Bs.” Our goal is to maximize our return while minimizing our risk. So, we’re not seeking “great returns”, we’re seeking “great risk adjusted returns.” When I measure the relative risk of an investment, I do a few things, two of which I write about here. First, I compare the dividend to the risk free rate. After all, if an investor can earn greater cash flows, while taking on lower risk in a Treasury Note, why would they bother with the stock? Second, I look at the current valuation, and compare it to the history of the stock. I want to see a stock trading at a discount to both the overall market and the stock’s own history. I’ll start today by comparing Allison Transmission to the risk free rate.

Equalizing The Dividend and the 10-Year Treasury Note

When we last visited Allison Transmission, I concluded that in order to match the cash flows then available to purchasers of the risk free Treasury Note, the dividend would need to grow at a CAGR of about 24%, which was way beyond the historical norm here. Given that rates have come down since then, I completed this calculation again, and I present the results below for your enjoyment and edification. The yield is still pitifully low here, about 238 basis points below the risk free rate , so there’d need to be some growth just to break even. It turns out that for people considering these two options today, the dividend would need to grow at a CAGR of about 10.8% for the cash flows received from the stock to match the cash flows earned on the risk free Treasury Note. Given that the dividend has grown at a CAGR of about 6.7% over the past decade, this may be a bit of a stretch. In my view, the valuation would need to be very compelling at this point for me to consider the stock relative to the Treasury Note.

Dividend v. Treasury Note (Author calculations)

Valuation

As I wrote above, I want to review the valuation here. After all, even if a stock is troubled in some ways, it might be a sound investment if, to quote a very famous game show host “the price is right.” So, let’s review the price compared to the past. Apart from that period where sales and earnings slipped between 2020 and 2022, various multiples have been remarkably stable here, floating around 8-8.5 times earnings, and . So, absent a catalyst, I can’t imagine a huge uptick in price from current levels.

Source: YCharts

Source: YCharts

Given my view that there won’t be much of an uptick in multiples paid by the market, I’m left with the view that this is a company someone will buy for the dividend, and the growth thereof. So, it’s a cash cow. Given that it’s possible to earn much more cash, at much less risk, I see no value in buying these shares at the moment. Now, the spread between the yield and the risk free rate is significantly lower than it was previously, but it’s still high in my view. Thus, if you were considering buying these shares, I would hold off and buy the Treasury Note instead.

For further details see:

Allison Transmission: TINA (Still) Doesn't Live Here, Though She's Closer