CM:CC - Allocating To Banks Preferreds In A Difficult Market

2023-04-20 07:30:00 ET

Summary

- It has been a rollercoaster ride for the Banks sector over the past month and a half.

- In this article, we take a look at some of the key metrics investors ought to be familiar with which explain a lot of the price action so far.

- We also highlight our stance in the sector as well as our recent trades.

This article was first released to Systematic Income subscribers and free trials on Apr. 12.

It has been a rollercoaster ride for Banks and sector preferreds. In this article we take a look at some of the key metrics investors ought to be familiar with which explain a lot of the price action so far. We also take a look at our stance and our recent trades.

Navigating The Sector

Investors trying to make sense of the price action in the Banks sector and guide future allocations have to consider at least three major things.

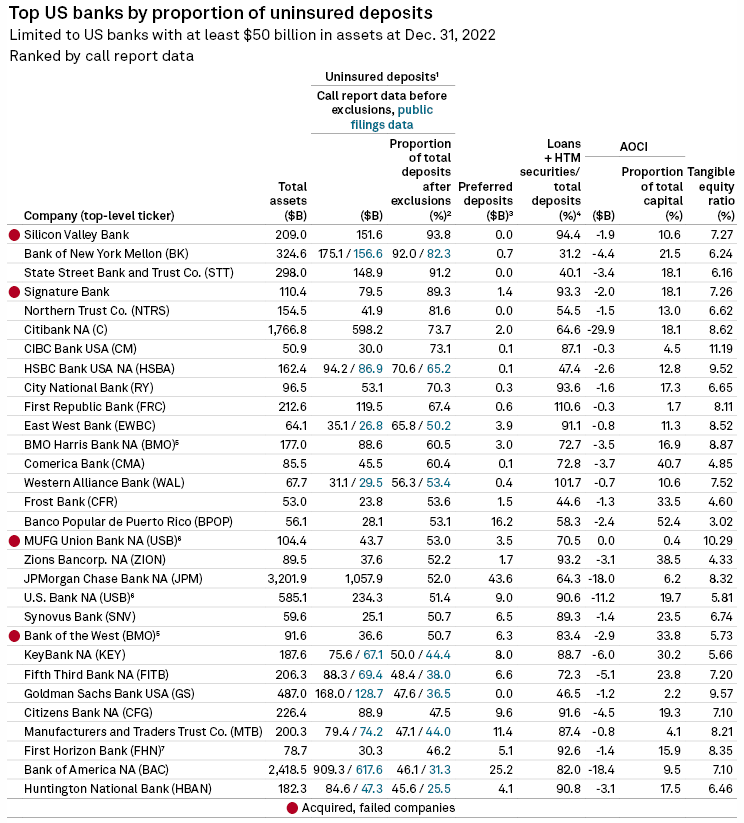

First is the very familiar uninsured deposit metric. It was this scary figure for SVB at around 94% which was key to its demise, particularly since the BTFP did not exist before it failed (i.e. SVB was forced to monetize losses on its bond portfolio in order to generate cash and pay out depositors - something banks no longer have to do).

The chart below shows what this looks like for the largest US banks. Banks that have struggled like PacWest (not in the table below as its $41bn of total assets is below the $50bn cutoff) and Western Alliance are at 52% and 56% - on the higher side in the sector where the average is in the 30s. [[FRC]] looks terrible on this front with a very high level of uninsured deposits at around twice the average. It also looks very bad on the liquidity metric i.e. the sum of loans + hold-to-maturity or HTM securities relative to deposits.

{kind=link}

A sidenote here is that we should make a distinction between custody banks like [[BK]] and [[STT]] (numbers 2 and 3 in the table) and "normal" banks. The business of custody banks is to hold securities and cash of corporates and institutional investors for safekeeping. These banks are much less involved in the bread-and-butter lending business which is why their ratio of Loan + HTM securities to deposits is well below that of other banks. In other words, we shouldn't worry as much about these banks' high level of uninsured deposits.

The other key metric is the level of unrealized losses on bank securities and loans. Much of the discussion here reasonably revolves around Treasuries, Agencies and Munis on bank balance sheets (which many banks bought as a result of large deposit inflows, themselves a result of the large fiscal support during COVID). These inflows unfortunately happened in a period of low rates which meant that the bonds were bought at high prices / low yields which drove losses once rates started to rise in 2022.

The other part of the unrealized loss puzzle, however, is the more prosaic loans that the banks themselves made. This part is important because it explains why FRC in particular is in trouble. Once we include it, we see that FRC equity is below zero (it's easy to find FRC in the chart below as it's the only one with negative equity after adjusting for loan losses) - worse than it was for SIVB when it went bust and well below the other banks.

JPMAM

A key issue here is that a bank can't borrow against its loans so it remains hostage to depositor flight. Deposit flight appears to have stabilized however the gap between deposit rates (as well as CDs) and money market yields remains.

The third key factor for banks is the exposure to commercial real estate which is the sector that has started to worry the market, in particular, the office sub-sector which is already in distress. Office appraisal values have fallen by a quarter in just the past year, office rent growth has been well below other property types, office leasing activity is near pandemic lows and sales of office buildings are down by two-thirds from 2022. Regional banks are the largest lenders to both CRE as well as the office sub-sector which is what's creating some concerns. Some of the outliers here are [[CFR]], [[BKU]], [[VLY]] and some others. FRC looks fine on this metric but that's not very relevant in light of its equity position.

JPMAM

Dividend Suspension Thoughts

Whenever we talk about bank preferreds we need to highlight the risk of dividend suspension. Many investors avoid bank preferreds because bank preferreds tend to be issued as non-cumulative stocks, meaning in case of dividend suspension, the issuer does not have to pay back the skipped dividends.

Our view has been consistently that banks are not going to suspend dividends just because they feel like it because doing so will signal that something is wrong with their liquidity and, possibly solvency, position, something that will accelerate their demise.

If anything, the recent preferred dividend suspension by First Republic Bank does provide some support to our claim that banks won't just suspend dividends because they feel like it but only do so in a very dire situation.

The fact that FRC has been under the gun since the start of March (and arguably earlier when it was the second biggest borrower from the San Francisco Federal Home Loan Bank) echoes that it is only banks that are in dire straits that will consider suspending preferreds dividends.

The second element of the thesis is that a bank that has suspended its preferred dividend is unlikely to continue to function in a business-as-usual way. This has played out so far when Silvergate suspended its preferred dividend at the end of January and announced an intent to wind down in early March.

We also saw this in 2009 when Citi and [[MS]] stopped paying dividends. However, this happened shortly before the $245bn TARP-funded preferred investment in the banks by the Treasury, in effect, a bailout of the sector. This recapitalization (and later the bank stress tests) restored some confidence in the sector and allowed banks to reinstate dividends. In other words, banks came out of the other end looking quite different than when they suspended dividends. What's also important is that the gap between dividend suspension and a resolution (either a failure or dividend reinstatement) was not indefinite (though, annoyingly, it wasn't very short either).

Overall, our view remains that banks won't suspend dividends without an exceptional reason but if they do, the dividends are very unlikely to be suspended for an extended time (though clearly one resolution here could be bank failure and a full writedown of the preferreds).

Stance And Takeaways

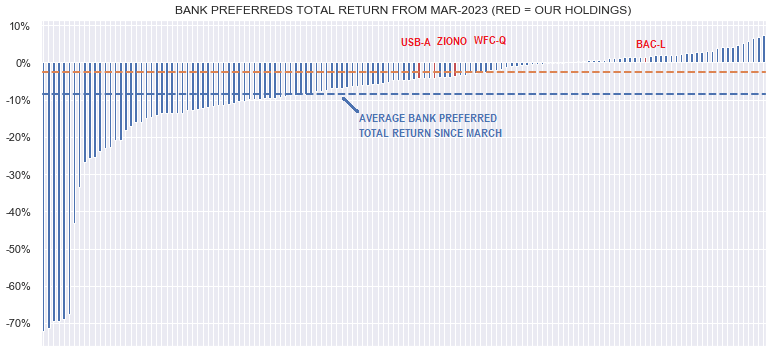

Going into the March sell-off our holdings in the Bank preferreds sector were primarily in the larger banks with three falling in the top 7 banks and the remaining Zion Bank being by far the smallest of the bunch (roughly 40th largest bank in the US).

Our allocations were also primarily tilted toward floating-rate preferreds with USB.PA and ZIONO being floating-rate, WFC.PQ switching to a floating-rate coupon in September, unless redeemed and BAC-L being a non-callable fixed-rate stock.

As the chart below shows all four of the positions (red bars) outperformed the sector since the start of the current crisis in early March.

{kind=link}

In our view this is owed to their larger footprint as well as floating-rate profile. Their larger footprint, particularly of USB, WFC and BAC, allowed these banks to, arguably, benefit from the recent fallout, as depositors viewed these banks as more stable.

And the floating-rate footprint meant that these stocks typically offered higher yields than their fixed-rate counterparts. For example, USB.PA trades at an 8.02% yield vs. a 5.7% average for the other USB preferreds while ZIONO trades at a 9.8% yield vs. a 7% yield for ZIONP. In an efficient market this wouldn't happen, however, retail preferreds can be somewhat inefficient as investors can find it difficult to gauge the actual yields on offer in the sector.

Most investors allocate by looking at stripped yields however these yields understate actual yields of floating-rate preferreds due to the lagged nature of how short-term rates flow through coupon accruals in a rising short-term rate environment. For instance, USB.PA stripped yield is 7.55% vs. its actual yield of 8.02% and ZIONO stripped yield is 6.55% vs. actual yield of 9.81%. By actual yield we simply refer to today's Libor as the base rate rather than the Libor that is being accrued since today's Libor is more representative of the ongoing level of yield for the stocks (in a way, averaging current and next coupon accruals).

With about 6 weeks after the start of this ongoing crisis, we slightly modified our position by doing two things: we slightly reduced our allocation to Bank preferreds and we rotated from the ZIONO holding to a First Horizons Bank Series D preferred (FHN.PD).

The overall reduction in the Bank preferreds allocation has to do with two factors. One is that, despite the sell-off since March, the sector looks somewhat rich to the broader preferreds market. The chart below shows that the gap between the Banks sector credit spread (blue line) and the broader sector credit spread (red line) remains fairly wide and wider of the level through 2021 and most of 2022.

Systematic Income Preferreds Tool

The second reason for a slight reduction in exposure to the Banks sector is to lower the holding of individual corporate preferreds, in favor of much more diversified securities such as funds or CEF preferreds.

The rotation from ZIONO to FHN.PD is largely due to the stronger metrics of First Horizon Bank such as the much better equity capital position, slightly better deposit metrics and roughly similar CRE metrics.

There are five preferreds in the FHN suite which look like the following in terms of forward yields (i.e. stripped yields based on forward short-term rates). FHN.PD should enjoy a big bump in yield relative to the other series on its first call date in a year's time which should also support its price. FHN.PD has a stripped yield of 7.3% as of this writing.

Systematic Income Preferreds Tool

And although FHN.PD has a lower yield than ZIONO, it's a matter of time before it moves out to a higher one. If the stock is redeemed, it will be a 20% tailwind and a great result.

Systematic Income Preferreds Tool

For further details see:

Allocating To Banks Preferreds In A Difficult Market