ALNY - Alnylam: Unlimited Promise Or Unlimited Losses?

2023-08-08 07:30:00 ET

Summary

- Alnylam's shares have seen significant growth, up over 140% since September 2019.

- The company has secured approvals for five RNAi drugs and aims to become a top-tier biotech company by 2025.

- The success of its RNAi therapeutics and potential future approvals in new indications, e.g. Alzheimer's, are key factors for Alnylam's valuation and stock performance.

- Big Pharma partners buying into the technology include Roche and Sanofi. The next wholly owned opportunity is in ATTR-cardiomyopathy and could help push revenues >$2bn.

- For me, Alnylam is valued at a premium, and I would not rush out to buy shares - but I would certainly consider buying the next dip - which is usually not far away in the drug development field.

Investment Overview

Investors who have been holding Alnylam ( ALNY ) shares since before 2020 will likely be well pleased with their purchase. In September 2019, the RNA-interference specialist's shares traded at ~$77, and today they trade at a value of $186 - up >140%.

In August 2022, shortly after Alnylam had secured US approval for its fifth commercial product - AMVUTTRA, indicated for the treatment of polyneuropathy of hATTR amyloidosis in adults, the company's share price reached an all time of ~$235, and a few months later, after the drug had been also been approved in the EU, UK, and Brazil, shares regained a similar high.

During the period of the pandemic, when vaccines were developed that used messenger RNA to instruct cells to manufacture copies of the COVID spike protein to train the immune system to seek out and destroy them, it was mRNA that took centre stage, with the likes of BioNTech ( BNTX ) and Moderna ( MRNA ) earning close to $20bn per annum from these vaccines.

MRNA therapeutics looked like the future, but progress has stalled as BioNTech, Moderna, Pfizer ( PFE ) and other companies have struggled to translate their COVID vaccine success to other indications. Meanwhile, the field of RNAi therapeutics, the technology that preceded lab manufactured / synthetic mRNA, which works by blocking naturally occurring MRNA to prevent unwanted, damaging proteins being made, has been making tangible progress.

It has to be said that Alnylam has been chiefly responsible for the progress, having secured all 5 approvals for RNAi drugs to date, although Ionis Pharmaceuticals ( IONS ) has secured 4 drug approvals using its antisense oligonucleotide mechanism of action ("MoA"), which also suppresses gene expression, albeit using a single-stranded oligonucleotide as opposed to double stranded RNA.

Andrew Fire and Craig Mello were awarded the Nobel Prize in 2006 for their discovery of RNA-interference, but it took more than a decade for the approach to succeed and win a first full approval - Alnylam's ONPATTRO, indicated for TTR-type familial amyloid polyneuropathy.

Alnylam's fortunes have ebbed and flowed since its listing in 2005, but today, the company and its management is looking forward with confidence and has a plan to become a "top-tier" biotech company by 2025. According to the company's 2022 10K statement ( annual report ):

In early 2021, we launched our Alnylam P5x25 strategy, which focuses on our planned transition to a top-tier biotech company, as measured by market capitalization, by the end of 2025. With Alnylam P5x25, we aim to deliver transformative rare and prevalent disease medicines for patients around the world through sustainable innovation, while delivering exceptional financial performance. Specifically, we intend to end 2025 with the following profile:

Patients: Over 0.5 million on our RNAi therapeutics globally

Products: Six or more marketed products in rare and prevalent diseases

Pipeline: Over 20 clinical programs, with 10 or more in late stages and four or more INDs per year

Performance: ?40% revenue CAGR (compound annual growth rate) through YE 2025

Profitability: Achieve sustainable non-GAAP (generally accepted accounting principles) profitability within the period

Alnylam's market cap is currently $23bn, and last year, the company broke the $1bn revenues per annum barrier - in 2019, revenues generated were "just" $220m. As impressive at that growth is, the historical price to sales ratio implied of ~23x is very high for an established commercial Pharma company - the average amongst the 15 largest commercial stage Pharmas by market cap is ~7x - plus Alnylam is a heavily loss making company. Since 2018, Alnylam has recorded annual net losses of $(762m), $(886m), $(858m), $(853m), and $(1,131m).

As such, when evaluating the investment case for Alnylam, and whether to buy shares in the company, it arguably comes down to potential, versus potential losses.

As exciting as Alnylam's technology is, it has traditionally been limited in its scope by off-target toxicity i.e. the silencing of unintended targets with potentially damaging consequences. With each new drug approval, however, Alnylam increases its total addressable market ("TAM").

In order to join the Pharma elite, however, Alnylam needs to find a way to stem its losses, because all of the major Pharma companies are very profitable. The top 10 largest Pharma's by market cap had an average net profit margin, in 2022, of ~25%, and an average price to earnings ratio of ~22x, which is lower than Alnylam's price to sales ratio!

With more and more companies recognizing the potential of RNAi technology, and Alnylam's focus now shifting from experimental drug development, to achieving non-GAAP profitability by 2025, the next 2 years' promise to be pivotal for the company, and its valuation.

In this post I will take a closer look at the current portfolio and pipeline, to try to gauge whether Alnylam can meet its goals, and what implication that may have for the company's share price. Let's start by taking a look at performance across 2023 so far.

Alnylam - Q2'23 / H1'23 Performance Review

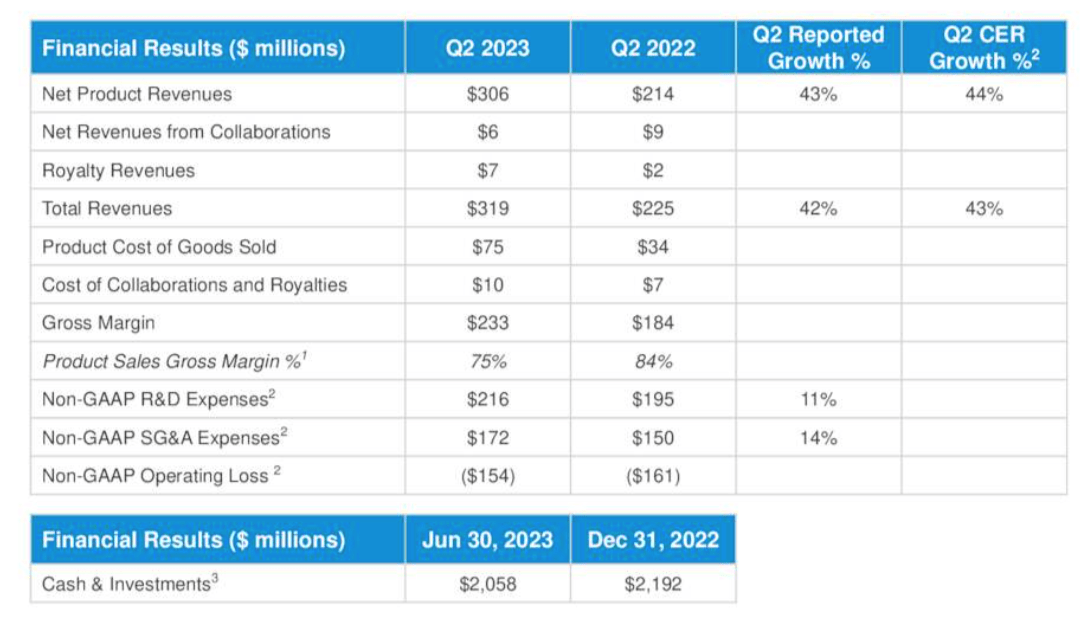

Reviewing Alnylam's Q2 2023 financial summary, a couple of positives jump out immediately.

{kind=link}

The first is the increase in net product revenues of 43% year-on-year, the second is a slight narrowing of the operating loss, from $(161m) in Q2 2022, to $(154m) last quarter, and the third is the solid cash position of >$2bn - similar to the cash position last year, although it should be noted the company issued $900m of 1% convertible notes due 2027 last September.

Alnylam product revenues as of H123 (Alnylam Q2 2023 10Q submission)

Revenues by product for Q2 2023 and H1 2023 are displayed above. The first thing to note is that ONPATTRO revenues are being cannibalized as patients are being switched to AMVUTTRA, which has a more convenient subcutaneous, and less frequent dosing regime. In H1 2023 ONPATTRO revenues fell 33% year-on-year, and in Q2 2023, by 40% year-on-year.

The more pronounced decline in the second quarter seems to suggest that ONPATTRO's peak selling days in this indication are behind it, but AMVUTTRA, which outperformed ONPATTRO in its pivotal clinical study, with patients achieving an average 2.2 point score improvement on a modified neuropathy impairment score after nine months, versus a 1.4 point improvement recorded by ONPATTRO (patients taking placebo in the ONPATTRO study recorded a 17 point worsening), ought to easily offset those lost revenues. According to Alnylam, 67% of patients have already made the switch from ONPATTRO to AMVUTTRA.

As we can see, within Alnylam's rare disease division, GIVLAARI, indicated for Acute Hepatic Porphyria, and Oxlumo, indicated for Primary Hyperoxaluria Type 1, both grew sales substantially across H1 2023, by 32% and 64% respectively. With that said, these being ultra-rare diseases, the peak revenue opportunity in each indication may not amount to much more than the low triple-digit millions, even while the list prices for both drugs are not far off $500k.

Leqvio, indicated for hypercholesterolemia, was developed in partnership with Swiss Pharma giant Novartis ( NVS ), with Alnylam earning a ~20% royalty share of revenues, which amounted to $22m in H1 2023, whilst the company also earned $12m from a collaboration with Regeneron in respect of a candidate targeting non-alcoholic steatohepatitis - a double-digit billion market opportunity.

Looking Ahead - Pipeline & Partnerships

Based on the above, it seems clear that AMVUTTRA is an extremely important drug for Alnylam. The traditional problem faced by RNAi drug developers has been one of delivery - how to get the double stranded RNA to the target cell without its being destroyed by the immune system. Previously, most progress has been made targeting the liver, which helps to explain why Alnylam's drugs target rare liver diseases.

AMVUTTRA is considered to have "blockbuster" potential, meaning it can target >$1bn revenues per annum, but much of that figure depends on whether the drug can now go on and secure an approval in ATTR cardiomyopathy, a form of ATTR that affects the heart.

While the ATTR polyneuropathy market is comprised of ~50k patients, the ATTR cardiomyopathy market could be four times as large, analysts believe, although the competition is fierce, with Pfizer's Vynqadel long established in this market, earning ~$2.5bn of revenues last year, and BridgeBio ( BBIO ) celebrating positive Phase 3 data for its candidate Acormaidis in the same indication a couple of weeks ago.

Both patisiran / ONPATTRO and vutrisiran / AMVUTTRO are being evaluated by Alnylam in late stage studies in ATTR with cardiomyopathy ("CM"), with patisiran having already achieved positive results from its APOLLO-B study. Alnylam's Chief Medical Officer Pushkal Garg told analysts on the Q2 2023 earnings call :

The sNDA for patisiran is under FDA review based on the positive results of the APOLLO-B study, and as we recently announced, the application will be discussed at the Cardiovascular and Renal Drugs Advisory Committee on September 13th.

The Prescription Drug User Fee Act ("PDUFA") date will arrive October 8th, when the FDA will make its final ruling on whether to approve the drug, which met the primary endpoint of the APOLLO-B study in September last year.

Presumably, however, if vutrisiran's HELIOS-B study in ATTR-CM is successful (results are due in early 2024) the drug would cannibalise patisiran sales as it did in the polyneuropathy indication. The easiest way to look at it is that Alnylam has the potential, analysts believe, to drive ~$1.8bn of revenues across both indications, and both drugs, by ~2026.

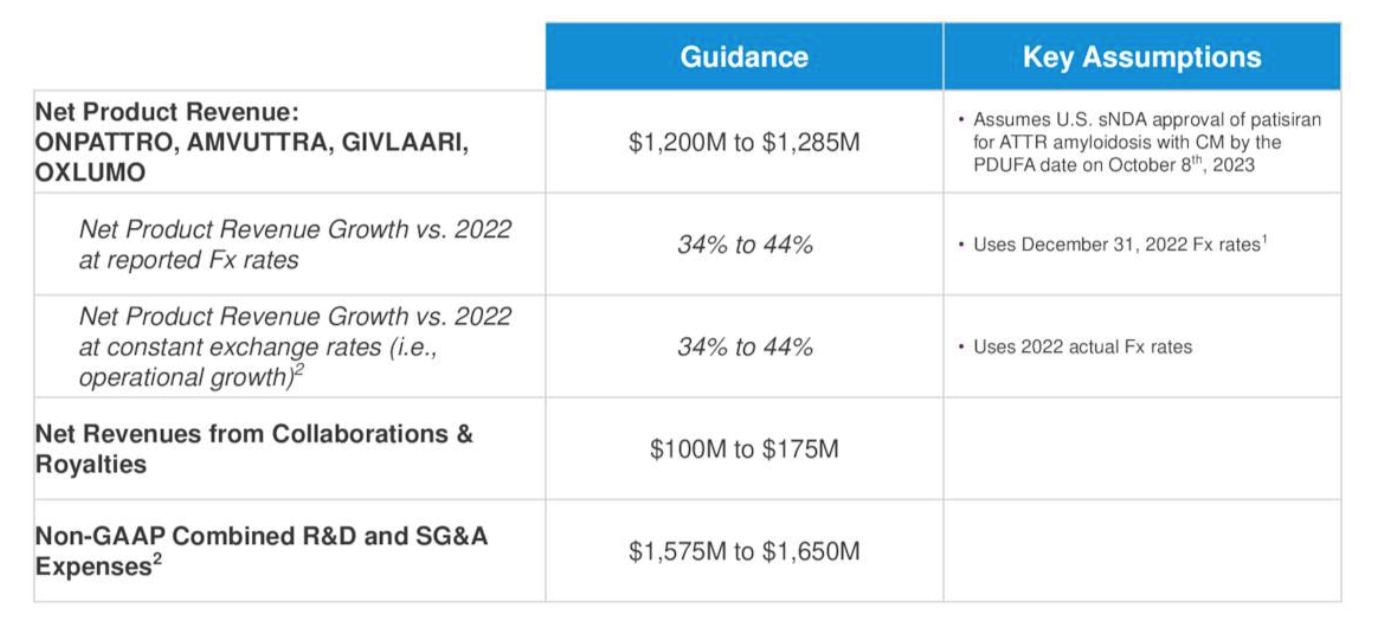

Alnylam updated its FY23 guidance last quarter as follows:

{kind=link}

As we can see, R&D and SG&A expenses are expected to be $1.58bn - $1.65bn, meaning net losses could come in substantially lower than in 2022, although Alnylam's >$2bn of long term debt means there will likely be >$100m of interest expense to pay, plus any other expenses. Nevertheless, it feels like a step in the right direction.

If the company wants to meet its 40% annual growth target in 2025, by my estimation, it will need to generate ~$2.4bn of revenues in that year. That figure looks a long way off today, but secure an approval for patisiran in 2023, and for Vutrisiran in 2024 in ATTR-CM, and with the additional rare disease revenues the figure may just be achievable.

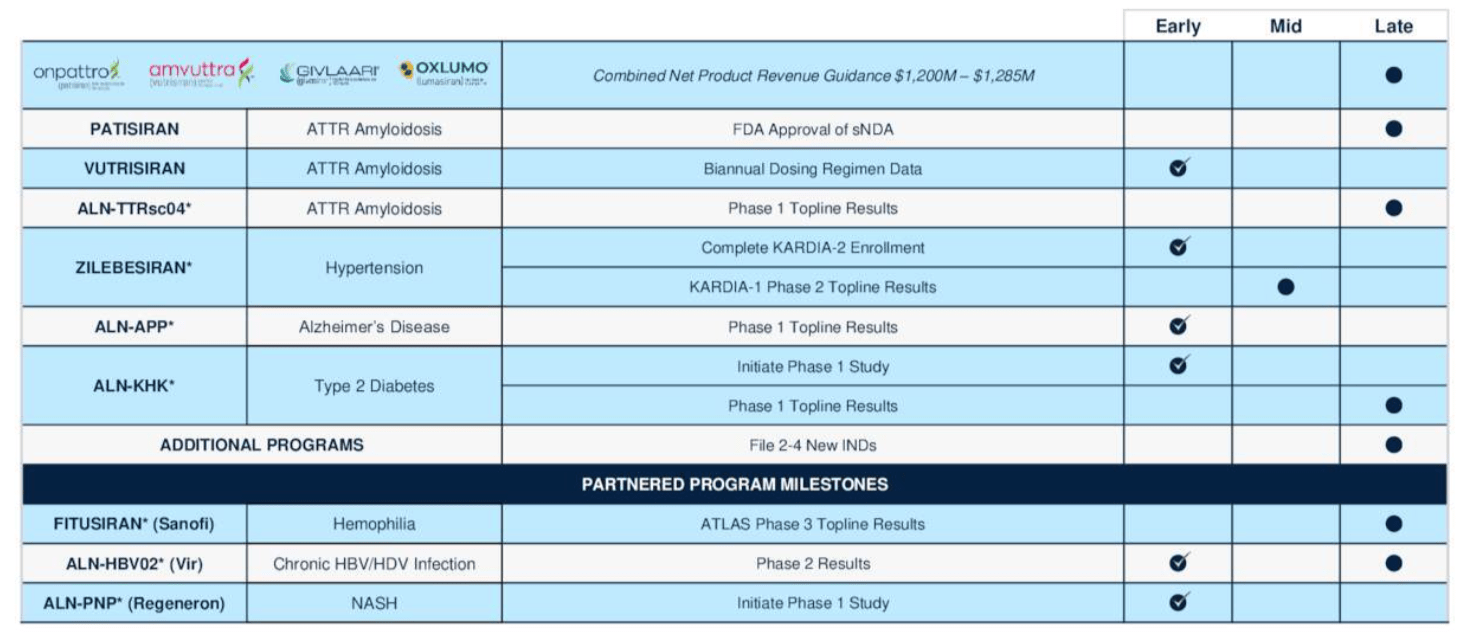

Meanwhile, there are more opportunities in play as we can see below.

{kind=link}

None of the above opportunities are likely to add much to the top line before 2025, but long-term there are some exciting possibilities here.

A couple of weeks ago, Swiss Pharma giant Roche (RHHBY) paid just over $300m for the rights to develop and commercialise zilebesiran, used to treat high blood pressure.

The drug targets cardio-metabolic disease, like Leqvio, which Novartis paid $9.7bn to acquire from Alnylam's partner the Medicines Company a couple of year ago. Specifically, it targets hypertension, and the total value of the deal to Alnylam could be $2.8bn if all commercial and regulatory milestones are met. It is early days, with the drug only in Phase 2 studies, but the soon to be revealed KARDIA-1 data ought to be intriguing.

Another early stage opportunity with enormous potential is ALN-APP, which targets Alzheimer's Disease. Earlier this month, Alnylam released positive data from its Phase 1 study, showing that:

Patients treated with a single dose of 75mg ALN-APP experienced a rapid and sustained reduction in cerebrospinal fluid of both soluble APP? (sAPP?) and soluble APP? (sAPP?), biomarkers of target engagement, with maximum reductions of 84% and 90%, respectively. Mean reductions in sAPP? of greater than 55% and sAPP? greater than 65% were sustained at 6 months after a single dose.

ALN-APP is injected directly into cerebrospinal fluid ("CSF") and like the approved AD drug Leqembi, and likely soon-to-be-approved donanemab, developed by Eli Lilly ( LLY ), it targets amyloid beta, the "sticky" protein found in patients with AD.

Unlike Leqembi / Donanemab, however, which remove deposits of amyloid, ALN-APP is designed to prevent its appearance in the first place . It is very early days, but if successful, this drug would represent a historic breakthrough in a very hard to treat patient population numbering nearly 6m in the US alone.

Concluding Thoughts - Based On Performance, Pipeline & Opportunity, Is Alnylam Stock Worth >$180 Per Share

Alnylam's progress in recent years has certainly been exciting, with the development and approval of its 2 rare disease drugs, and most excitingly, the approval of AMVUTTRO. The tantalising prospect of approvals for Patisiran and Vutrisiran in ATTR-CM raises the prospect of management meeting its 40% CAGR goal, and driving annual revenues towards the $2.5bn per annum mark by 2025.

Longer term, the ability to treat conditions outside of the liver is attracting the might of global Pharmas like Roche, and French Pharma Sanofi ( SNY ), with whom Alnylam is developing Fitusiran, a candidate I have not mentioned until now but which could, if approved - and Phase 3 studies are underway - achieve blockbuster sales, with Alnylam set to receive 15-30% royalties on net sales. Meanwhile, ALN-APP is a distant, but extremely exciting prospect.

Even with all of these positives in play, however, I would still come back to Alnylam's valuation relative to some industry metrics. For example, the very high price to sales ratio of >18x based on 2023 forward revenues projections of ~$1.25bn, the lack of profitability - net losses could easily exceed $500m this year, which may be an improvement on 2023, but is a troubling figure nonetheless - and what looks like a substantial gap between the exciting near-term approval prospect for 2 drugs in ATTR-CM, and the next approval shot, which looks a long way off for any wholly owned Alnylam asset.

As such, although I am a fan of Alnylam, it's science and technology, it's partnerships, cash position, products and pipeline, I would not be rushing out to buy shares after the latest Q2 2023 earnings. Setbacks have historically checked Alnylam's share price quite significantly, and in the drug development arena, setbacks are fairly common, even for the very best and most established drug developers - the flipside of an industry that handsomely rewards success with exceptionally strong profit margin, cashflow generation, and patent protection.

Alnylam stock fell to a low of $125 per share in May last year - personally, I would be very tempted to purchase stock in a range of $125 - $150, based on the opportunities in play, and the fact that RNA-i appears to be overcoming some of its drug delivery issues and partnering with Big Pharmas.

The prospect of an M&A deal involving Alnylam is an enticing one - I could see any deal valuing the company even higher than the $43bn Pfizer looks set to pay for Seagen ( SGEN ), the antibody drug conjugate developer that is similar to Alnylam in terms of revenue generation and pipeline opportunities, albeit in oncology.

In short, I would definitely consider buying the next dip in the valuation of Alnylam, but unless you are a deal hungry Big Pharma, paying >$180 per share feels a little steep.

For further details see:

Alnylam: Unlimited Promise Or Unlimited Losses?