AFMJF - Alphamin: Strong Q2 Results But Tin Prices Are Dropping Like A Rock

Summary

- The company’s Bisie complex finished Q2 2022 with a record production of 3,180 tonnes of tin and AISC fell below $15,000 per tonne.

- However, global tin prices have declined by over 50% since early March and it seems there is no end in sight.

- I think that low tin prices could push Alphamin to suspend the development of the Mpama South deposit.

- Alphamin looks cheap at these share price levels, but opening a position could be dangerous as tin prices are recording their sharpest decline in history.

Introduction

Alphamin Resources Corp. ( AFMJF ) is a DR Congo-focused tin miner which I've covered several times on SA. In June, I changed my stance from bearish to neutral due to rumors about the company putting itself for sale, as well as robust drill results coming from the Mpama South project. The Bisie complex finished Q2 2022 with record production and its EBITDA stood at $67 million. However, this represents a significant decline compared to the previous quarter due to lower tin prices as fears of a global recession mount. Tin prices have been in a freefall since March, and I think this is raising questions about the viability of this project from a financial point of view. In addition, there have been no updates on the sale of Alphamin and it's starting to look unlikely that a deal will take place. Overall, I think the company is starting to look cheap, but opening a position seems dangerous as tin prices are recording their strongest decrease in history. Let's review.

Overview of the recent developments

In case you haven't read my previous article about Alphamin, here's a brief description of the business. The company owns an 84.14% stake in Bisie, which is the highest-grade tin complex in the world as ore processed from the Mpama North deposit processed in Q2 2022 had an average grade of 3.65%. The mine has an annual output of about 12,000 tonnes of tin, which means that it accounts for some 4% of global production.

Alphamin Resources

Turning our attention to the production and financial performance of Alphamin, Bisie finished Q2 2022 with an output of 3,180 tonnes of tin and improved processing plant performance helped drive down all-in sustaining ((AISC)) costs to below $15,000 per tonne. The mine is on the path to meeting the 2022 production guidance of 12,000 tonnes and production in Q3 is expected to stand at around 3,000 tonnes. However, EBITDA slumped by 32% as the average tin sale price decreased by 19% for Q2 2022. Alphamin's net cash position improved by just $8.3 million to $138.1 million as the company made a $43.5 million corporate tax payment to the DR Congo government in April 2022.

Alphamin Resources

On August 2, Alphamin released an updated reserve and resource estimate for the Mpama North deposit which showed that reserves decline by just 12,000 tonnes despite 2.5 years of commercial production since the last estimate. However, we aren't comparing apples to apples here as the cut-off grade was decreased from 1.6% to 1%. The cut-off grade for the resource estimate was kept at 0.5% and there we can see a concerning decrease of 43,300 tonnes in the measured and indicated category.

Alphamin Resources Alphamin Resources

The reserve cut-off grade for the reserves was reduced due to improved run of mine output, optimized mine planning, out-performance versus dilution assumptions, improvements in the process plant recoveries, and higher tin prices. The mine life remains 11 years, but I have doubts Bisie can get there without the discovery of more ore. You see, the new cut-off grade calculation was performed based on tin prices of $32,000 per tonne, and I find this value concerning as this level is very high and tin prices are trading at just $21,060 per tonne as of the time of writing.

Trading Economics

The price of the metal reached a historic high of above $48,000 per tonne in March 2022 due to a tight market, but it has been dropping rapidly since then. The main reasons behind this decline include worsening global recession fears, tighter monetary policy across the world as well as never-ending COVID-19 lockdowns in China. Solder accounts for about half of global tin demand and I think that a prolonged global recession could lead to a long period of depressed prices, similar to what we had during the early 1980s.

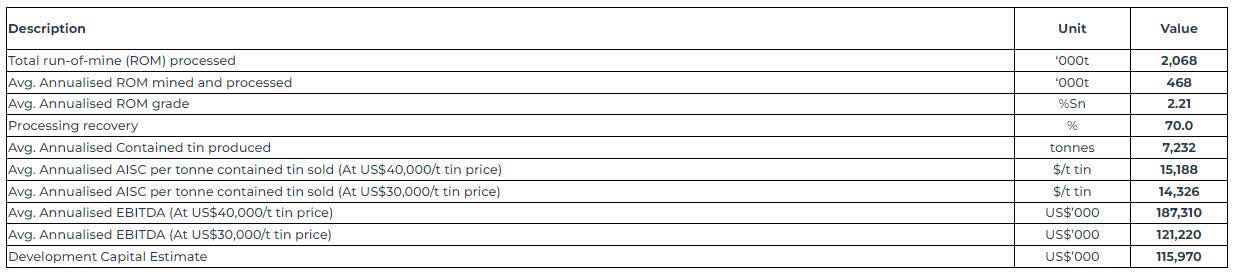

Unless tin prices stop dropping in the near future, I think that Alphamin could suspend the development of the Mpama South deposit. In March 2022, the company announced the results of a preliminary economic assessment ((PEA)) for this project which showed that AISC would stand at $14,326 per tonne at prices of $30,000 per tonne. However, the development of this deposit could lead to liquidity issues even at $15,000 per tonne as cash outflow during the first two years is expected to be $161 million due to the relatively high CAPEX and a 20-month construction period. This amount is higher than Alphamin's net cash as of the end of June 2022.

{kind=link}

Alphamin Resources

Turning our attention to the valuation, Alphamin has an enterprise value of $510 million as of the time of writing which I think is low for a company that holds over 80% of one of the best tin projects in the world. Bisie is a low-cost mine thanks to its high grade and it generated EBITDA of $165.1 million in H1 2022 alone. However, the prices of commodities are notoriously volatile, and tin is no exception. If they don't stop falling soon, Bisie could become unprofitable. Also, I think that Alphamin's share price has been under pressure from diminishing expectations that the company could be sold. In April 2022, media sources reported that the company was looking for a buyer for its business and that this was expected to attract interest from Chinese companies and private equity funds. Alphamin hasn't confirmed these rumors and there have been no updates on this story for over four months now.

Investor takeaway

Alphamin's Bisie mine posted record production for Q2 2022 thanks to improved operational performance but its market valuation has been falling rapidly over the past few months due to an unprecedented crash in tin prices. The USA is already in a recession, and it seems the EU will follow suit. In addition, China is still pressing forward with COVID-19 lockdowns, and I think tin prices could decline below $15,000 per tonne in the near future.

I think it's likely that Alphamin will delay the development of Mpama South in order to conserve cash and I don't like that the cut-off grade for the reserves at Mpama North is based on tin prices of $32,000 considering we've seen these levels only for brief periods in 2011 and 2022.

In my view, Alphamin looks undervalued at these share price levels but I think that it could be best for risk-averse investors to avoid this stock. The valuation of the company could remain under pressure over the remainder of 2022 as there is no relief in sight for the global tin market.

For further details see:

Alphamin: Strong Q2 Results But Tin Prices Are Dropping Like A Rock