ATEC - Alphatec: Price Reversal Diverges From Economic Levers That Are Well In Situ (Rating Upgrade)

2023-08-10 13:10:13 ET

Summary

- Alphatec Holdings' Q2 numbers were strong, posting another double-digit upside at the top line.

- The company's surgical segment, particularly the LTP procedure, shows promise for growth and profitability in my view.

- Sentiment towards Alphatec's stock is mixed, with bullish positioning in the short-term but potential downside in the long term.

- Net-net, revise to buy, eyeing 36% initial return objective.

Investment briefing

The equity stock of Alphatec Holdings, Inc. ( ATEC ) has caught a 20% bid since my January publication. The stock rallied 12 months from July FY'22—'23 and then sold off quickly. This isn't uncommon in smaller names, whereby distribution occurs at the 12-month mark within an upside leg given those long of the stock are no longer constrained by ST capital gains tax when taking profits. The company's Q2 numbers don't appear to be helpful here either, pushing through a deeper operating loss on ~40% YoY growth in revenues. Yet, on closer inspection, there was no deviation from the company's long-term growth route, hence, there's a chance the selloff is over-extended in my view.

Net-net, I revise my ATEC rating to buy given the profile outlined here. On asset factors and sales growth, the company has a propensity to rate to $20/share in my view. Revise to buy.

Figure 1. ATEC price evolution with selloff at 12-months post rally origination, also with Q2 numbers last week.

{kind=link}

Critical facts to investment thesis

The investment debate is summarized into fundamental, sentimental and valuation factors in my opinion. I'll run through each here, outlining the relevant points for each way. Specifically, on asset factors and sales data, ATEC appears as a qualified growth company. A more detailed appraisal is warranted to discern the investment value going forward.

1. Fundamental drivers

ATEC's most recent numbers in Q2 FY'22 were strong and aligned with its trajectory to date. Revenues were up 39% YoY to $117mm on $1.5mm in adj. EBITDA and a net loss of $0.43.

Critically, the primary revenue driver is its surgical segment, where it books sales on delivery of its spinal implant products. These include pedicle screws, interbody units, plates, along with tissue-based biologics. It also books income from the sale of the medical imaging equipment used in the planning of surgery and post-op review. Procedure-wise, its main revenue drivers are the prone transpsoas ("PTP") procedure, anterior lumbar interbody fusion ("ALIF"), and lateral transpsoas ("LTP") procedures.

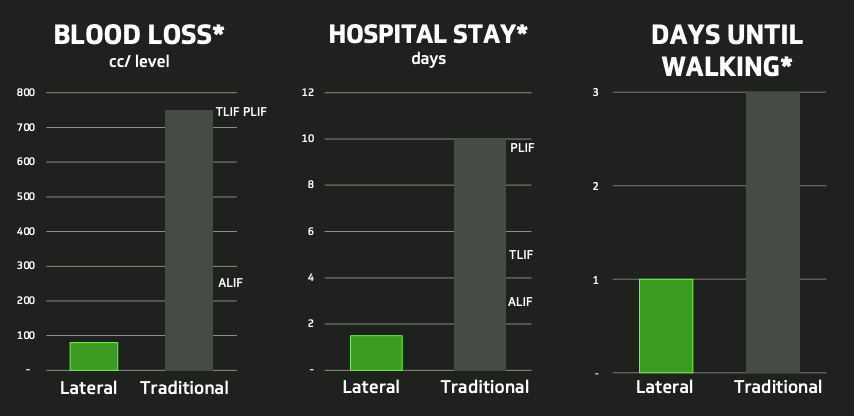

The LTP offering has promise in my view. From my many discussions with orthopaedic surgeons and hospital executives over the years, what I dub as patient economics are factored heavily into all decision-making on surgery preference. First, the efficacy and safety of the procedure are paramount. Patient outcomes are top priority, for obvious reasons. But adjacent to that, length of procedure (to increase surgeries/day), length of recovery, blood loss/infections, and, time before discharge are all factored highly.

That is, shorter surgery time, shorter recovery, less bloods/infections, and quicker discharge. These all mean the surgeon can complete more surgeries in a set time period, ultimately driving higher income for surgeon and hospital. The LTP procedure looks to offer this kind of profile, which talks to the patient economics I mentioned. Figure 2 is taken from its Q2 investor presentation, and highlights the potential benefits compared to conventional spinal surgery techniques. This is due to the access point being through the psoas muscle (also known as the hip flexor, and located in front of the spinal column). You're avoiding a large incision through the anterior or posterior tissues of the abdomen this way—much less invasive.

Figure 2.

Data: Author, ATEC Q2 investor presentation

{kind=link}

It is for good measure that the LTP has surgeon attractiveness too. The key economic levers for ATEC—for all its portfolio—are converting new surgeons, growing the number of surgeries from its existing base, and adding new products/procedures to expand its markets. This has the potential to create an attractive economic flywheel in my view. Why?

One, ATEC's top-line growth qualifies it as a legitimate growth company in my view. Just taking the Q2 numbers from FY'19—'23, quarterly revenues are up $79.3mm from surgeries, and up $8.5mm from imaging (note: imaging recorded from 2021 on its introduction). Net-net, it did $102mm of business from surgeries last quarter, up ~40% YoY. Further, procedural volumes were up 32% YoY, with average revenue per case up 7% as well.

Figure 3.

Data: Author, ATEC 10-Q's

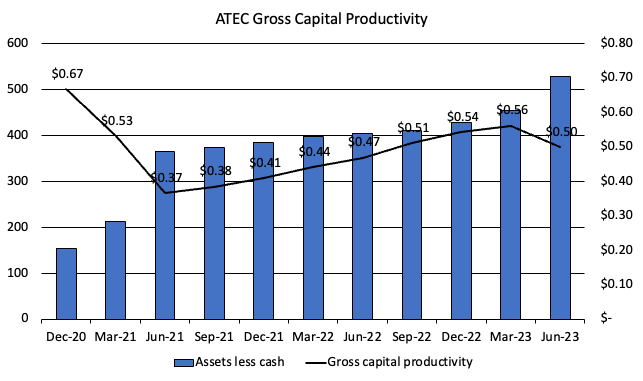

Two, with the growth in operating assets (total assets less cash + marketable securities) delivered from its business returns so far, it has circled back ~$0.15 per $1 in assets back in gross over Q2 FY'21. It now sees ~$0.50 in gross capital productivity on each $1 of capital tied up into its asset base [Figure 4].

It has grown operating assets by $364.4mm across this time, and produced an additional $33.1mm in quarterly gross profit ($102.7mm in TTM figures). This equates to a 9% incremental gain in gross capital productivity, or 28% on a TTM basis (102.7/364.4 = 0.28). As such, we have a scenario, where as the business expands—from an asset growth perspective—the gross profit it produces on this is matching the speed of growth. If gross profitability scaled by ATEC's assets was lagging, I would be a little more concerned.

Figure 4.

Data: Author, ATEC SEC Filings

{kind=link}

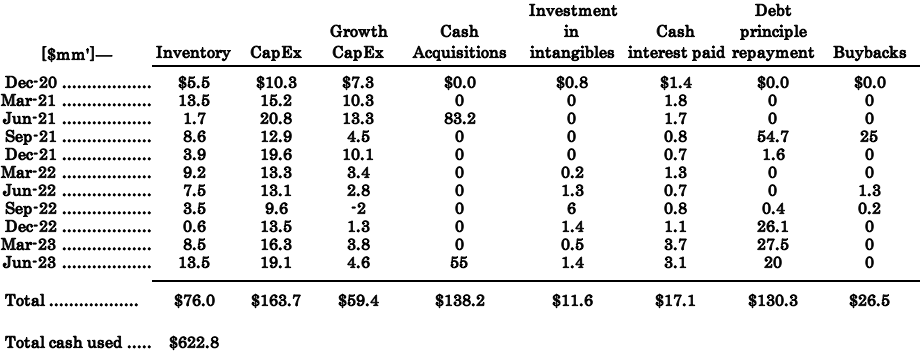

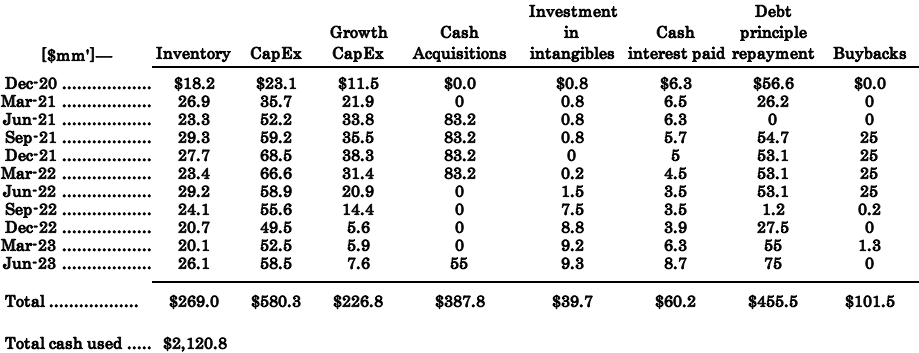

Three, the firm has been deploying cash towards growth initiatives on a sequential basis. The quarterly and TTM cash allocations are outlined in Figure 5 and Figure 6, respectively. Taking the quarterly numbers, you'll note it's deployed an additional $623mm in total towards maintenance and growth capital budgeting. In particular, the $76mm inventory matched by $59mm in growth CapEx are notable. It's also completed 2x cash acquisitions in this time, the most recent being REMI Robotic Navigation System in April. It raised $60mm in external capital to finance the transaction. From my analysis earlier, the $623mm ($476mm stripping out debt + interest servicing) has added ~$79.4mm in Q2 revenue growth (2019—'23) or $276.1mm on TTM values from 2020—Q2 FY'23.

Figure 5. Uses of cash, quarterly

Data: Author, ATEC SEC Filings

{kind=link}

Figure 6. Uses of cash, TTM format

Data: Author, ATEC SEC Filings

{kind=link}

2. Sentimental factors

Sentiment in ATEC's equity stock is balanced in my view. We see this in a few ways.

First, options-generated data shows us that investors are positioned bullish until the end of August and also September. Strike depth on the calls ladder extends down to $20, with heavy open interest at this level on the chain. Activity on the puts ledger isn't balanced, indicating the bullish positioning of money at risk.

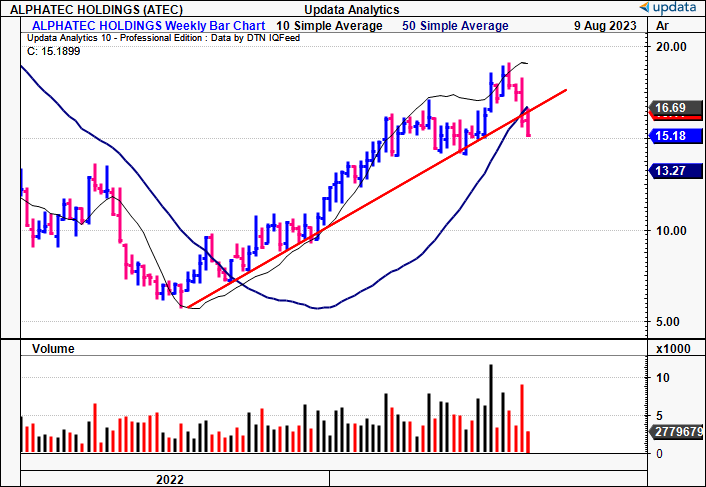

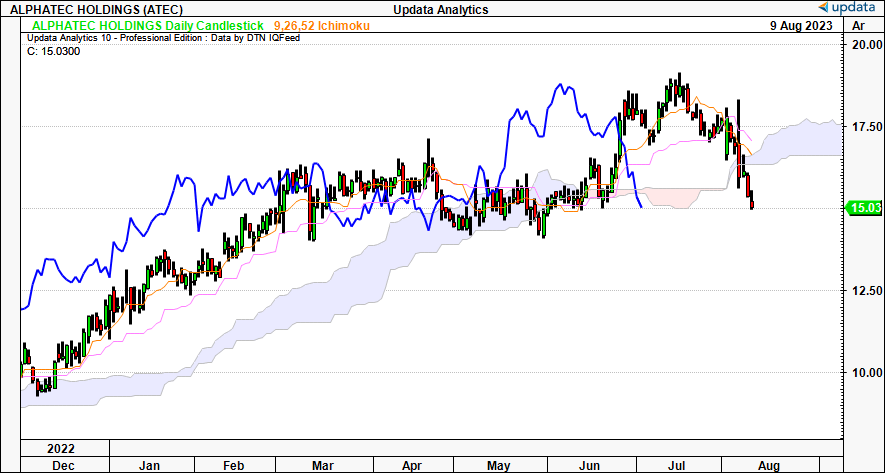

Second, short-term momentum has begun to run out of steam. The stock trades below its 10, 50 and 100DMA', indicating it is priced 'below average' on each of these time frames. Further, on the daily cloud chart below, that shows the prevailing trend, the price line and lagging line have cracked the base of the cloud and are now into bearish territory in my view. This implies further downside ahead.

Figure 7.

{kind=link}

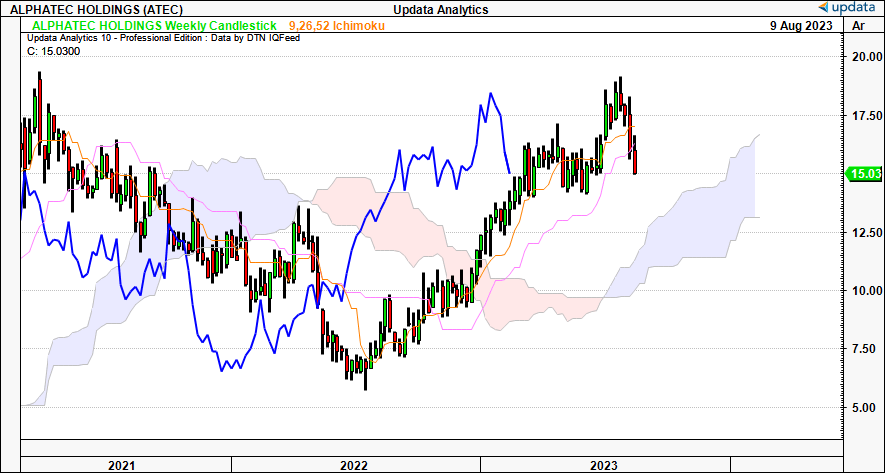

The weekly chart, that looks to the months ahead, tells a different story. It has room to move above the cloud still. However, I'd be looking to $15—$17 as support at the cloud's top towards yearend in order to remain on this trend. In the direction it's heading, we could be looking at congestion into this range first. Nevertheless, this suggests the stock is trading bullish on the long-term view.

Figure 8.

{kind=link}

Finally, Wall Street has updated its revenue estimates into FY'23—'25 a total of 8 times in the last 3 months, supporting a constructive outlook. Consensus now calls for 32% growth at the top line this year, clipping to 19% by FY'24. The overall trajectory is biased to the upside, but ATEC now has to outshine 20% projected sales growth next year in order to outpace these estimates, which are ultimately baked into the price as we speak. This should be considered heavily. The forward estimates are potentially attractive but have likely been priced in, one reason why the prospective re-pricing over the past 4 weeks.

3. Valuation factors

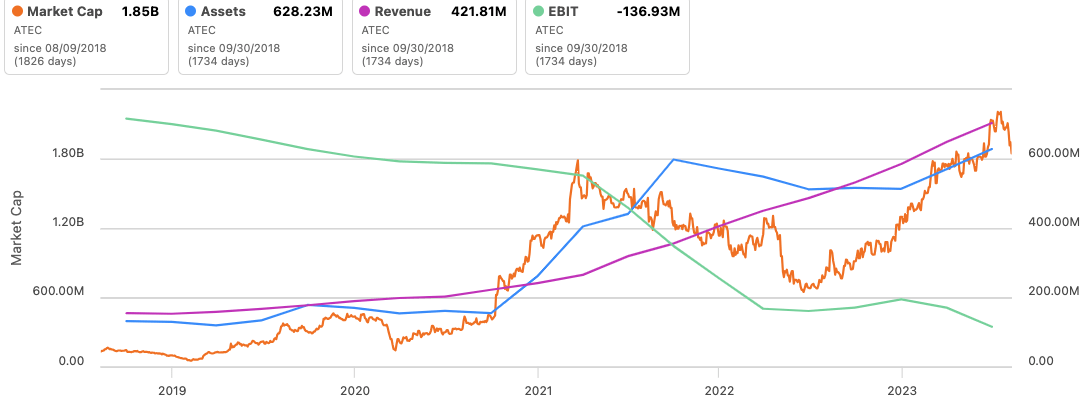

Investors are selling ATEC at 4x forward sales , asking you to pay $1.85Bn in market value on this. This is roughly in line with the sector, not suggesting any outsized expectations from the market. Both management and consensus expect $462mm in sales this year on adj. EBITDA of $2mm.

The market has been valuing ATEC on asset factors rather than earnings power [Figure 9]. Makes sense, given the sequential operating losses, and that ATEC's capital are what produces the business (IP in the surgery, devices to perform the surgery). It currently trades at 2.95x total assets at the current market cap of $1.85Bn as I write (1,850/62 = 2.95). Bringing this multiple forward to my FY'24 estimates of the company's gross productivity and asset growth to $823mm, I get to $2.45Bn in estimated market value, otherwise $20.4/share (est. asset base $823 x 2.95 = $2,450). This is ~36% upside potential and supports a buy rating in my view. To get there, ATEC must continue adopting new surgeons to drive procedural volumes, and get to $600m by FY'24. Based on this analysis, I believe it can get there. Adding confluence to this number, I've got upside targets to $22.50 on my point and figure studies below, which have been incredibly helpful in eyeing directional moves in ATEC in combination with the analyses provided [Figure 10].

Figure 9.

{kind=link}

Figure 10.

Data: Updata

In short

Net-net, I have revised my outlook on ATEC from hold to buy given the proven sales record and growth in its core offerings. The top line numbers speak for themselves, the underlying market is adopting its surgeries, and there is clinical data to support their uptake. Several other bullish signs point to a potential re-rating over the coming months into FY'23. I am looking to an initial price objective of $20, looking to rate higher from there with another period of strength in H2. Revise to buy.

Risks to investment thesis

Investors should recognize the following risks that could nullify the investment thesis:

- Healthcare companies have copped a battering in the last 3 months amid a number of macroeconomic and idiosyncratic drivers. Company results have missed estimates, along with a higher cost of capital reducing the deployment of cash towards achieving growth. If this continues, it could hurt the valuations of healthcare stocks.

- We shouldn't forget the broader macro picture here either given its impact on global equity markets at present. There's no saying what factors like inflation and rates will do in the near-term. Yet, their effects are pronounced. This could result in a re-rating in broad equities.

- The company's surgeon adoption needs to continue at a reasonable past to continue seeing profitable revenues from Q3 this year. If this doesn't occur, the market may look elsewhere for them.

Investors must observe these risks in full before proceeding any further.

For further details see:

Alphatec: Price Reversal Diverges From Economic Levers That Are Well In Situ (Rating Upgrade)