TMUS - Alphyn Capital Management Q2 2023 Letter To Investors

2023-07-06 11:00:00 ET

Summary

- Alphyn Capital Management LLC (“ACML”) is a registered investment advisor in New York. We help clients invest in high quality public companies to both preserve and grow their wealth over the long term.

- Compliance advisors recommend withholding performance reporting until next quarter to avoid using private market figures or speculative estimates for the preceding two quarters.

- The portfolio has been rebalanced to align with long-term objectives, with a new position initiated in Cogent Communications and additional purchases in Amazon, Ashtead, Brookfield Corp, and IAC.

- Positions in Exor, Fairfax, and Prosus were trimmed, while the Alvotech position was entirely closed.

Performance

Typically, I start these letters with an overview of our performance metrics. However, WANdisco ( WANSF ) shares remain suspended. Per the company’s regulatory announcements, it has raised $30m in a private placement at £0.50 a share. While a substantial drop from its last recorded value, it has the funds to continue operating as a going concern and runway to effect its transition plans under new and experienced management. As of this writing, we expect shares to resume trading by the end of July. I am crediting clients’ fees for this position. My compliance advisors recommended I withhold performance reporting until next quarter to avoid using private market figures or speculative estimates for the preceding two quarters. Your patience is deeply appreciated. Clients can, of course, see detailed balances in your brokers' statements.

Portfolio management and rebalancing

Investing in the public markets entails embracing uncertainty and relinquishing a certain level of control. Central to my approach is the belief that owning stocks means owning a real business rather than just pieces of paper or numbers on a screen. However, an inherent distinction exists between owning a private company and a public one. Owners typically wield direct agency over business decisions in a privately owned business and can significantly influence outcomes. In contrast, public company investors must take an entirely passive approach. They can only control buy and sell decisions, choosing how much to allocate to a specific investment at the prevailing market rate. While public investment has the potential to be rewarding over time, it requires taking a view on the quality and prospects of a company based on limited public information while depending on the management team’s execution and various other factors over which investors have no direct control.

Building on lessons shared in last quarter’s letter, I have dedicated time to carefully underwriting each investment in our portfolio – the goal is to strike a balance, avoiding excessive dependence on any single position yet ensuring sufficient allocation so that successful investments can meaningfully contribute to overall returns. The result of this exercise was to rebalance the portfolio to better align with our long-term objectives of sensible long-term compounding of our capital. The remainder of this letter will focus on the trades executed along with their high-level rationale.

Portfolio – top and bottom performers [1]

| Top Performers |

| Contribution |

| Bottom Performers |

| Contribution |

| Fairfax Financial Holdings Ltd. ( FRFHF ) |

| +ve |

| SPX put options |

| -ve |

| Wayfair Inc. ( W ) |

| +ve |

| Prosus NV ( PROSY ) |

| -ve |

| Amazon Inc. ( AMZN ) |

| +ve |

| Alvotech SA ( ALVO ) |

| -ve |

| Exor NV ( EXXRF ) |

| +ve |

| VanEck Gold Miners ETF ( GDX ) |

| -ve |

| CarMax Inc. ( KMX ) |

| +ve |

| Wayfair covered calls |

| -ve |

| As calculated in the Master Account brokerage statement. |

Portfolio changes

I initiated a new position in Cogent Communications ( CCOI ) and purchased a few more SPX put options. I trimmed Exor, Fairfax, and Prosus and added to Amazon, Ashtead ( ASHTF ), Brookfield Corp ( BN ), and [[IAC]]. The Alvotech position was entirely closed, as were a series of covered call trades on Wayfair.

Cogent Communications – new position

I initiated a position in Cogent Communications, led by Dave Schaeffer, a remarkable founder-operator with technical acumen, astute business sense, and a long-term ownership mindset. Schaeffer has shown a propensity for making transformative bets while effectively managing risk and allocating capital shrewdly.

In 1999, Schaeffer secured $500 million to build an affordable, all-fiber internet network. The telecom market’s collapse in 2000 allowed Cogent to buy 13 companies, built at an initial cost of $14 billion, for just $60 million. Over the last few decades, Cogent has grown into a $3 billion company, producing $600m in revenue and nearly 40% EBITDA margins. Revenues have increased by 10% annually, and margins have expanded by 200bps annually. As a result, Cogent produces significant cash flow, which it has used to return over $1bn to shareholders; it has repurchased 22% of shares outstanding and increased dividends for the last 41 sequential quarters, with a current dividend yield of ~5.75%.

Cogent is a strong business in its current state. However, my interest was piqued by the exceptional potential behind Cogent’s recent acquisition of Sprint’s former wireline business, which it is purchasing from T-Mobile ( TMUS ) following the acquisition of Sprint. At its peak, the Sprint business generated an impressive $40 billion in revenue and $16 billion in EBITDA, employing around 70,000 individuals. The initial capital investment to build the network was approximately $20 billion. Unfortunately, due to neglect, the business has declined to about $440 million in revenue, with an EBITDA loss of around $300 million and a workforce of only 1,320 employees.

Cogent is buying the business for $1 and will receive ~$760m in payments from T-Mobile over the next 4.5 years to cover expenses while it integrates the company and restores it to profitability. Dave Schaeffer believes he can turn the $300m loss into a $90m profit. The acquisition opens potential new revenue streams that could see the company 3x revenue and 5x free cash flow over the next few years. The market is not crediting the company for the transformational potential of the deal, while the T-Mobile payments significantly de-risk the acquisition.

Business

Cogent provides internet access and data transport over fiber optic, IP data-only network, carrying over 22% of global internet traffic across 51 countries and 219 markets. Its customer base can be broadly divided into two categories:

- Corporate customers - small to medium-sized businesses located in Multi-Tenant Occupied Buildings (MTOBs) in North America contribute to ~56% of the company's revenues.

- The "netcentric" division, primarily large streaming, gaming, and access companies, account for ~44% of revenues but constitutes 96% of the traffic.

The core of Cogent’s Corporate service comprises its “on-net corporate” services, accounting for 35% of revenues; Cogent directly connects its corporate customers to its expansive network, including 61,000 miles of inner-city fiber and an additional 17,000 miles of metropolitan fiber.

Cogent connects roughly 1,820 skyscrapers directly to its network, totaling nearly 1 billion square feet. They install equipment in the basements of these buildings, extending infrastructure upwards to establish direct connections with the building’s business tenants. On average, these buildings are 550,000 square feet and 41 stories high, housing around 51 businesses, of which typically 7 are Cogent customers.

Cogent also offers “off-net corporate” services, contributing 21% of revenues. These cater to secondary offices that are typically 19k sq ft in size with four tenants, locations where it isn’t economically feasible for Cogent to provide direct access. This service is exclusively available to existing on-net customers with secondary offices. Cogent provides “last mile connectivity” and has relationships with 90 different off-net providers, offering access to over 4 million buildings.

This division’s clientele primarily comprises law firms, financial services firms, advertising and marketing firms, healthcare providers, educational institutions, and other professional services businesses. These firms require high bandwidth (100 Mbps to 400 Gbps), and secure and reliable internet connectivity. Cogent prices its services in line with competitors but offers 3x the reliability and 30-60x the bandwidth.

The physical equipment installed in the buildings and the appealing quality-to-cost ratio give Cogent substantial competitive advantages, especially in the on-net corporate division.

Historically, the business has grown by 11% per year. There is room for continued growth within its existing businesses, which currently secure less than half (40%) of new proposals. Moreover, there are over 93,000 MTOB tenants worldwide, presenting a significant opportunity for expansion.

Approximately 44% of Cogent’s revenue, accounting for 97% of its traffic, is generated through the sale of bulk internet connectivity to roughly 1,415 carrier-neutral data centers (CNDCs). The company terms this “netcentric” division, serving major clients such as streaming services, gaming companies, and internet service providers (ISPs, ILECs, etc.). The company offers services at a 50% discount relative to its competitors, reinforcing its competitive standing within the market.

Cogent is one of only 24 Tier 1 networks worldwide, which means it can exchange traffic with other networks settlement-free, conferring a significant cost advantage.

Operating under the belief that internet connectivity is a commodity business, Dave Schaffer, Cogent’s founder, established the company with a focus on simplicity, allowing it to become a low-cost operator. The network runs on a single fiber pair, eliminating the need to manage legacy systems while positioning the company to benefit from the rapid advances in optical technology over the last 15 years. As fiber optic capacity increased and the cost to transport data fell, Cogent has reduced fees charged to customers on a per-routed bit-mile cost.

New transaction

Cogent is buying the business for a nominal $1, but importantly will receive $700m over the next 54 months, structured as a 100% margin supply agreement, $25m of restructuring/severance costs, and a $100m blanket indemnification from T-Mobile for any unforeseen liabilities. The supply agreement is front-loaded, with $350m due in the first 12 months, and $350m over 3.5 years, to fund operating losses while Cogent restructures and assimilates the business.

T-Mobile has been trying to shed the unit for years, and hiring a consultant revealed that shutting it down would cost over $1.5 billion. This agreement provides a politically acceptable way for T-Mobile to divest from a lossmaking business without resorting to job cuts, which could be a sensitive issue after its merger with Sprint.

The opportunity for Cogent is twofold. First, it plans to trim unprofitable revenue streams (from 28 products down to 4, the maniacal focus on simplicity again) while retaining long-standing enterprise customer relationships. It will migrate most of Sprint’s traffic onto its network, saving significant 3rd party carriage costs. Approximately 93% of Sprint’s services are delivered using third-party networks. Cogent, by contrast, will be able to have 75% of Sprint’s traffic on its network. As a result, Cogent expects it can take a declining, cash-burning business and generate $440m of stable revenue with a positive $90 million EBITDA.

The real value of this acquisition lies in its potential to provide optical wavelength services. Wavelengths offer dedicated point-to-point connections with customer-specific and dedicated spectrum frequencies. They cater to high-bandwidth users seeking enhanced security, privacy, and independent links that are not reliant on the internet. Think of Amazon AWS connecting data centers. Customers value redundancy and alternative routes to mitigate failures and outages. Potential customers include hyper scalers (Amazon, Google, etc.), Tier 2 internet service providers, and the top 100 corporations aiming to establish proprietary networks.

Sprint’s substantial assets include 19,000 intercity and 1,100 metropolitan fiber miles and 1.6 million square feet of data center space. Notably, many of these fibers run along railroad rights of way, providing unique routing advantages for wavelength clients. Combining these assets with Cogent’s metro network and its extensive network of 800 carrier-neutral data centers (compared to Sprint’s 24), Cogent can offer twice as many routes as its competitors.

The cost of replicating such infrastructure would have amounted to billions of dollars for T-Mobile, with the resulting profits being relatively insignificant. This acquisition taps into a $2 billion total addressable market, growing 7% per year, which two slow-moving incumbents currently underserve. Cogent’s competitive advantages include the ability to eventually provide service in 17 days versus 3+ months for competitors, a focused sales force, and a negative cost basis on the network. This advantageous position enables Cogent to price aggressively and set its sights on capturing a quarter of the market within seven years.

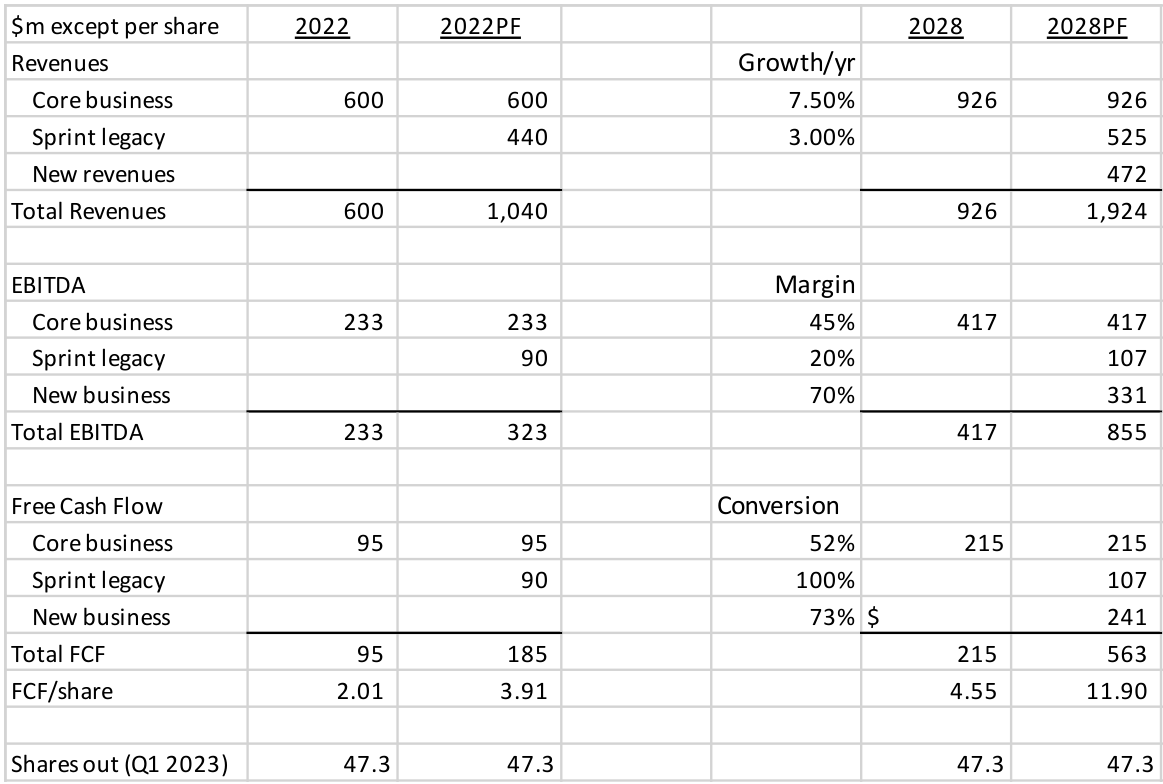

The table below provides a comparison of Cogent’s results for 2022 with the pro forma numbers for the “legacy Sprint” deal. It includes an additional $440 million of revenue, assuming full integration on day one without any payout from T-Mobile. Additionally, estimates for 2028 are provided for Cogent alone and the combined business, considering the maturation of all new revenue streams.

{kind=link}

The potential for substantial free cash flow ((FCF)) accretion is evident, and not reflected in the current $65 share price.

Risks/mitigants

The thesis may take a year or so to start working. The shift towards remote work has impacted growth at the corporate division. Historically this segment grew at an annual rate of 11%; with Covid, it shrunk by 9% and is now effectively at zero growth. The decline in this segment might take time to normalize, but Cogent believes it will eventually return to its growth trajectory. In the interim, the market could negatively perceive the company if it takes longer than expected to normalize, and synergies from the Sprint deal have yet to kick in.

There are always execution risks with any large M&A deal. However, in this case, the payment from T-Mobile grants Cogent the necessary time to navigate the integration process.

There are no guarantees that the wavelength business will take off. My research indicates a significant pent-up demand, considering the continuous growth of data and the need for route diversity. Moreover, as proof of concept, the company has already begun limited-scale cross-selling activities.

Sprint’s fiber infrastructure is over 20 years old. Cogent argues that these fibers are buried deeper than modern fibers with reinforced sheaths. Combined with routing along railway lines, are offer superior quality and are less prone to cuts and damage over time.

The company has experienced increased salesforce churn since the onset of the pandemic, with the work environment presenting challenges. Ensuring alignment within the salesforce and effectively promoting the new services will be critical to the future success of the acquisition.

Lastly, Schaeffer maintains tight control over the business and is involved in all aspects, from strategy to deal negotiations. While this concentration of power has been beneficial thus far, it presents a key man risk.

Special thanks to my friends Aaron Chan of Recurve Capital and Howie Xia of BeaconLight Capital for their insights about this opportunity.

SPX put options – new position

I bought some out-of-the-money put options on the S&P 500 index, slated for expiration in September. Paralleling the profitable options I liquidated in the preceding quarter, their primary function is safeguarding against significant tail-risk events, not shielding against minor retracements. These options have decreased value due to a substantial contraction in the market’s implied volatility, but their term extends until mid-September.

Exor and Fairfax - trim

In the spirit of prudent portfolio rebalancing, I pared down our positions in both companies as these holdings had grown into double-digit allocations. I firmly believe that Exor and Fairfax remain robust firms and maintain a bullish outlook on their prospects. However, there are a few smaller positions I wanted to allocate to and needed to free up capital.

Prosus - trim

For similar reasons, I trimmed our position in Prosus. Towards the end of July, the company updated the market on its half-year results. Management continued their efforts to narrow the discount to Tencent, successfully contracting it by approximately 17%. Thus far, they’ve strategically repurchased shares in Naspers ( NPSNY ) and Prosus amounting to $10.5 billion. Additionally, they fulfilled their pledge to untangle the company’s complicated structure with a plan to eliminate cross-holdings, making it much simpler to ascertain each company’s economic value. As we know, the market appreciates straightforward narratives. Prosus will henceforth be a Naspers subsidiary, with Naspers owning 43% and the free float, or public shareholders, owning 57%. Notably, a significant part of the CEO and CFO’s compensation is directly tied to narrowing the discount. The adage attributed to Charlie Munger, “Show me the incentive, and I will show you the outcome,” could not be more apt here.

Operationally, despite a solid 36% YoY growth in their core commerce business, management acknowledges there’s more work ahead to hit the 2025 profitability goals. However, their continued discipline bolsters my confidence in our investment in Prosus.

Amazon - add

In my 2002 Q4 letter, I outlined quantitative reasoning for why I believe the company’s financials mask its true earnings power. More qualitatively, Amazon continues to make strategic strides that enhance its appeal as an investment. Firstly, Amazon’s willingness to streamline costs and shutter underperforming initiatives demonstrates prudent financial management. The company’s overhaul of its fulfillment network, transitioning from a national to a regional model, will improve efficiency and delivery speed, resulting in lower costs and increased customer satisfaction, both critical drivers of revenue growth. Second, Amazon’s unparalleled scale, leading e-commerce platform position, and technology investments attract advertisers eager to engage with its vast customer base and provide consumers with highly targeted ads. This strategy has propelled Amazon’s advertising business to surpass broader market trends. Finally, Amazon remains a long-term growth entity. With retail, 80% of shopping is still offline, and Amazon has been steadily expanding its business sales (currently at $35 billion) and international presence. With AWS, despite near-term conservative enterprise spending, 90% of global IT spending remains on-premise. With other bets, Amazon has ambitious forays into diverse sectors such as grocery, healthcare, and satellite internet connectivity,

Ashtead - add

I increased our position in Ashtead, having grown more confident in its business model recently. A key thesis point is that Ashtead benefits from economies of scale, providing attractive economics vs. the rest of the industry. Ashtead and United Rentals, leaders in the market, boast robust EBITDA margins of 45% and 47%, surpassing number 3 Herc’s 24%. Similarly, their 52% and 57% dollar utilization rates outshine Herc’s 45%.

Notwithstanding the past impact of macro trends on the rental industry, these leaders maintain that their scale affords pricing discipline and less reliance on residential construction, thanks to their successful expansion into specialty lines (outlined in my 2022-Q3 letter). The upcoming $2 trillion government-backed construction boom, characterized by large, multi-year, cycle-independent projects, could counterbalance potential recession effects. With each year seeing the initiation of $300bn worth of projects and assuming rental revenues constitute about 1% of total construction costs, Ashtead, due to its scale, could capture a sizable 30%. This could translate into yearly incremental revenues surpassing $900m, offsetting any recession-driven revenue decline.

Brookfield Corporation - add

During a recent Forbes conference, Bruce Flatt was asked what he perceives to be most underrated in the current environment. His response, "long-term compounding of wealth... not for the next two months, six months, two years, it's for the next 20 years," aptly encapsulates Brookfield's investment philosophy. They embody the principles of value investing and long-term strategy, boasting an impressive track record over three decades. With their increasing fee-paying assets under management, which provide attractive recurring income, the ability to reinvest in their balance sheet at attractive rates of return, exposure and competitive advantages with high ticket global real assets, expansion into areas such as insurance (for more float to reinvest) I believe the company can continue to compound for the foreseeable future. Brookfield acquired an 80% stake in American Equity in June for $3.4 billion. This move aligns with its value-creation strategy. On completion, Brookfield will manage an additional $50 billion of assets, yielding $119 million in net fees. Over time, transitioning 40% of these assets to its private funds, where it can apply higher rates, will increase net fees to $151 million, marking a 27% rise.

Given the market's concerns about commercial real estate, we acquired additional shares at an attractive price. In the mid-30s per share, Brookfield is trading at less than the company's fundamental value, even if one were to assign zero value to its entire real estate portfolio, highly improbable given its array of premium assets that have proven more resilient than average commercial properties.

IAC - add

IAC’s cyclical share price patterns—rising before spin-offs and stagnating afterward—provide opportunities for patient investors. I believe the current undervaluation and subsidiary progress a profitable window. IAC’s $4.5bn market cap, lower than the combined value of its investments in MGM ($2.8bn), Angi ($1.1bn), and cash ($1bn), implies undervaluation of its private ventures—Dotdash Meredith, Care.com, Vivian Health, and Turo—businesses valued at $4.6bn two years ago. CEO Joey Levin has reoriented Angi towards fundamentals, focusing on manageable, easy-to-bid projects that enhance customers’ and service providers’ experiences. Moreover, IAC’s increased investment in Turo, a car rental service exhibiting promising growth, presents future optionality.

Alvotech - sell

I exited our Alvotech stake after it failed an FDA re-inspection in April, which along with an intensifying competitive biosimilar market, undermined my confidence in the company. This surprise news hurt the share price, which was once at 1440. We sold at around $11/share, realizing an 8% profit. (The price has since fallen to about $7/share).

Wayfair covered calls - close

Wayfair has endured a tough couple of years, resulting in the stock being out of favor with investors, presenting the opportunity to earn premiums from covered call options. I profitably exited calls sold in Q1 and re-initiated a position following the earnings announcement. The market seemed unmoved by Wayfair’s claim of market share gains, given headline revenue declines of 7.3% for the quarter. However, a business update in June, in which the company disclosed rising order volumes, precipitated a stock price rally, forcing me to close out the calls. Longer term, Wayfair’s scaled presence in online furniture, comprehensive product offering, and prior investments in supply chain infrastructure is well-positioned to capitalize on the industry’s increasing shift to online. Assuming management maintains its recent focus on cost control, Wayfair is on track to return to profitability and reach its target margin of 30%.

Samer Hakoura

Footnotes[1] There is no assurance that any of the securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable. See “Disclaimers” at the end for more details. |

DisclaimerAlphyn Capital Management, LLC is a state registered investment adviser. The description herein of the approach of Alphyn Capital Management, LLC and the targeted characteristics of its strategies and investments is based on current expectations and should not be considered definitive or a guarantee that the approaches, strategies, and investment portfolio will, in fact, possess these characteristics. Past performance of specific investment advice should not be relied upon without knowledge of certain circumstances of market events, nature and timing of the investments and relevant constraints of the investment. Alphyn Capital Management, LLC has presented information in a fair and balanced manner. Alphyn Capital Management, LLC is not giving tax, legal or accounting advice, consult a professional tax or legal representative if needed. Reference or comparison to an index does not imply that the portfolio will be constructed in the same way as the index or achieve returns, volatility, or other results similar to the index. Unlike indices, the model portfolio will be actively managed and may include substantially fewer and different securities than those comprising each index. Results for the model portfolio as compared to the performance of the Standard & Poor’s 500 Index (the “S&P 500”) for informational purposes only. The S&P 500 is an unmanaged market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent US equity performance. The investment program does not mirror this index and the volatility may be materially different from the volatility of the S&P 500. Performance results of the master portfolio are presented for information purposes only and reflect the impact that material economic and market factors had on the manager’s decision-making process. No representation is being made that any investor or portfolio will or is likely to achieve profits or losses similar to those shown. Results are net of all standard fees calculated at the highest rate charged, expenses and estimated incentive allocation. Model portfolio returns are inclusive of the reinvestment of dividends and other earnings, including income from new issues. The return is based on annual returns since inception and does not give effect to high water marks, if any. Returns may vary for investors who are restricted from participating in new issues. Hypothetical performance results are unaudited and do not reflect actual results of any accounts managed by Alphyn Capital Management, LLC. Hypothetical performance results are for illustrative purposes only and are not necessarily indicative of performance that would have been actually achieved if an investment utilized the strategy during the relevant periods, nor are these simulations necessarily indicative of future performance of the strategy. Inherent limitations of hypothetical performance may include: 1) hypothetical results are generally prepared with the benefit of hindsight; 2) hypothetical results do not represent the impact that material economic and market factors might have on an investment adviser's decision-making process if the adviser were actually managing client money; 3) there are numerous factors related to the markets in general, many of which cannot be fully accounted for in the preparation of hypothetical performance results and all of which may adversely affect actual investment results. There is no assurance that any of the securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed do not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein. The graphs, charts and other visual aids are provided for informational purposes only. None of these graphs, charts or visual aids can and of themselves be used to make investment decisions. No representation is made that these will assist any person in making investment decisions and no graph, chart or other visual aid can capture all factors and variables required in making such decisions. This report is for informational purposes only and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy or investment product. Our research for this report is based on current public information that we consider reliable, but we do not represent that the research or the report is accurate or complete, and it should not be relied on as such. Our views and opinions expressed in this report are current as of the date of this report and are subject to change. Any reproduction or other distribution of this material in whole or in part without the prior written consent of Alphyn Capital Management, LLC is prohibited. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Alphyn Capital Management Q2 2023 Letter To Investors