ALPP - Alpine 4: 2023 Is Shaping As A Tough Year (Rating Downgrade)

2023-07-06 05:22:44 ET

Summary

- Several of Alpine 4’s subsidiaries struggled in Q1 2023 and I think that revenues for the full year could fall below $100 million.

- I think that net loss for 2023 is likely to surpass $20 million and that there could be significant stock dilution soon.

- The short borrow fee rate is just above 10%, but I think that risk-averse investors should avoid ALPP stock.

Introduction

I’ve written four articles on SA about holding company Alpine 4 Holdings (ALPP), the latest of which was in August 2022 when I said that the fundamentals of the business looked poor as margins were deteriorating.

I think that this is a good time to revisit Alpine 4 as it recently released its financial results for the first quarter of 2023. In my view, the financial results were underwhelming as revenues were stagnant and most of the key subsidiaries were in the red. In my view, the net loss for 2023 could surpass $20 million and there could be significant stock dilution soon. I’m cutting my rating on the stock to a strong sell. Let’s review.

Overview of the Q1 2023 financial results

In case you're not familiar with Alpine 4 or my earlier coverage, here's a short description of the business. The company was established in 2014 and is a conglomerate focused on acquiring small businesses and integrating them with each other even if they operate in different industries. The strategy is centered around synergistic innovation and for example, Alpine 4’s drone subsidiary Vayu uses the solutions of its printed circuit board assembly services arm Quality Circuit Assembly ((QCA)) for its avionics and various other prototype needs.

Alpine 4 currently has 14 subsidiaries and the business is split into five segments - aerospace, defense services, technology, manufacturing, and construction services.

{kind=link}

Alpine 4 employs over 500 people and four of its subsidiaries account for about 80% of revenues – RCA, Alt Labs, QCA, and MSM. RCA is a business-to-business LED lighting and electronics products maker, Alt Labs is a nutraceuticals contract manufacturer, and MSM is a sheet metal contractor focused on the construction sector.

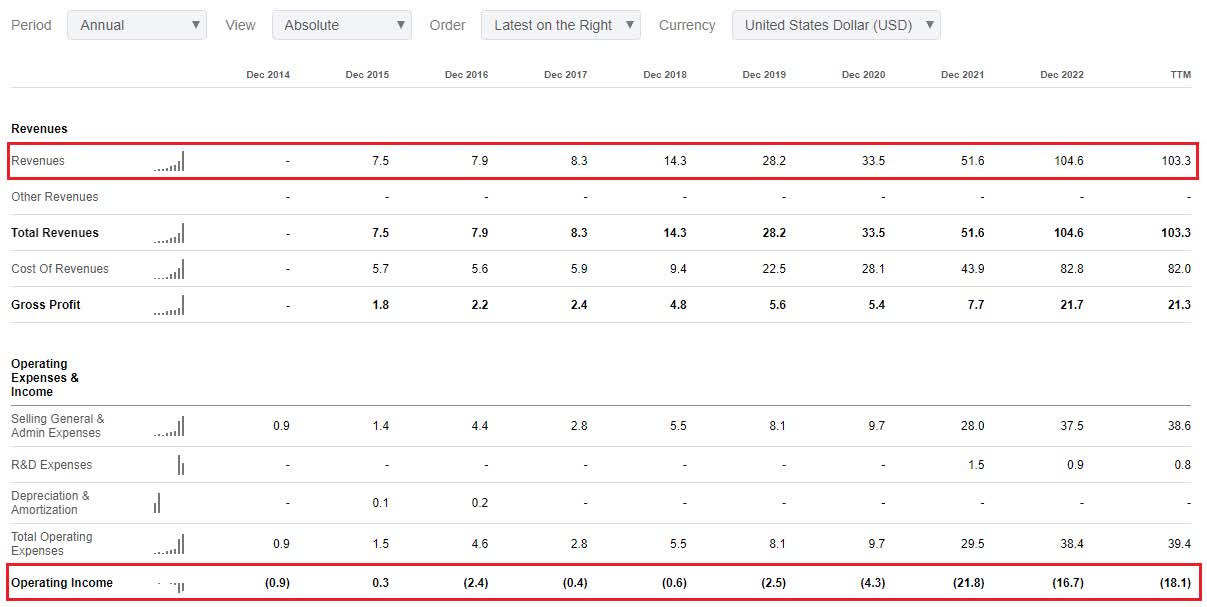

Turning our attention to the financial results, Alpine 4 had the goal of reaching annual revenues of over $100 million since 2017 (slide 6 here ) and this was finally achieved in 2022 when it booked sales of $104.6 million. The main reason the company finally managed to go over the $100 million mark was the purchase of RCA, which contributed revenues of $38.6 million in 2022. Yet, Alpine 4 remained in the red for the year as general and administrative expenses soared.

{kind=link}

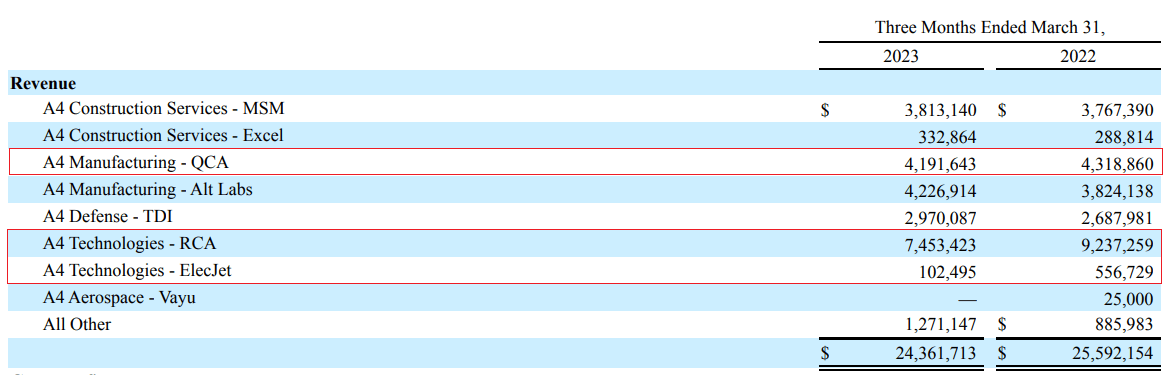

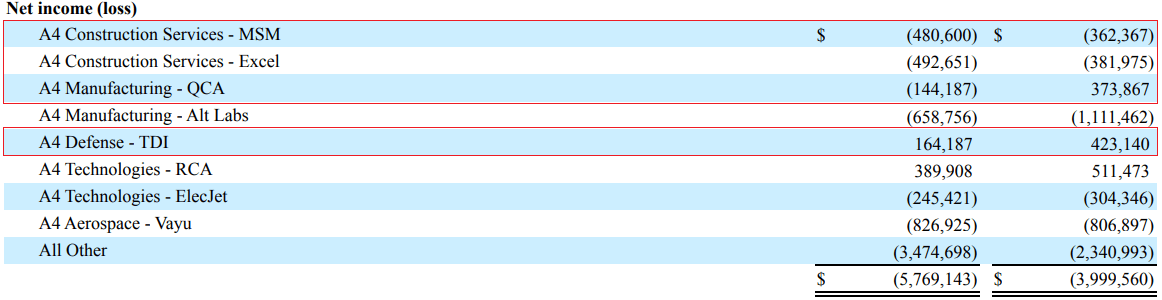

Looking at the Q1 2023 financial results, I think that annual revenues could go down below the $100 million mark this year as several of Alpine 4’s key subsidiaries seem to be struggling financially. During the quarter, RCA’s revenues went down by 19.3% to $7.5 million and QCA and battery research and development company ElecJet also posted significant sales declines. In my view, the lower sales of RCA and ElecJet are particularly concerning considering together they launched a new solid state battery line in August 2022. Overall, Alpine 4’s total sales decreased by 4.8% year on year to $24.4 million. In addition, several subsidiaries including MSM, Excel, QCA, and TDI suffered from margin contraction which boosted the net loss of Alpine 4 by 44.2% year on year to $5.8 million in Q1 2023.

{kind=link}

{kind=link}

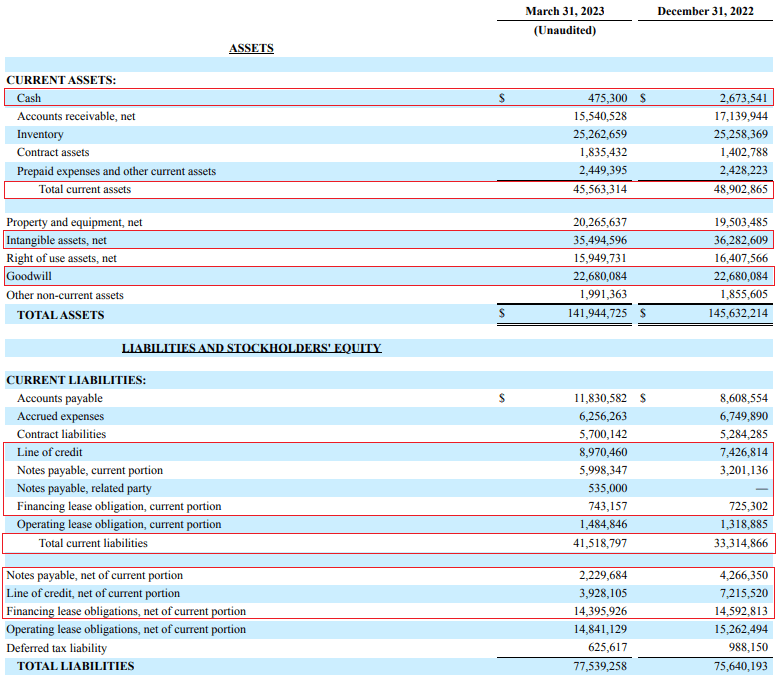

Turning our attention to the balance sheet, I think that the situation looks grim as net debt stood at $36.3 million at the end of March while cash declined to just $0.5 million. In addition, the tangible book value was only $6.2 million while working capital declined to just $4 million from $15.6 million a quarter earlier as short-term debts and accounts payable rose.

{kind=link}

Overall, I think this was an underwhelming quarter for the company as the revenues of several key subsidiaries decreased and it seems that synergies between them are lacking as margins contracted as well. I find the financial performance of RCA particularly concerning as its sales have been falling ever since Alpine 4 acquired it in 2021.

Looking at what to expect for the future, I think that continued weak performance by RCA is likely to be the key driver for Alpine 4’s revenues to decline below $100 million in 2023. In addition, quarterly general and administrative expenses surpassed $10 million in Q1 2023, and I think that net loss for the year is likely to surpass $20 million.

So, how do you play this? Well, I think it could be best for investors to avoid this stock as short selling seems dangerous. Data from Fintel shows that the short borrow fee rate is 10.09% as of the time of writing which isn’t that high. Yet, it takes over 33 days to cover, which means that there’s a significant short squeeze risk here. In addition, the lowest available strike price available for call options is $2.50.

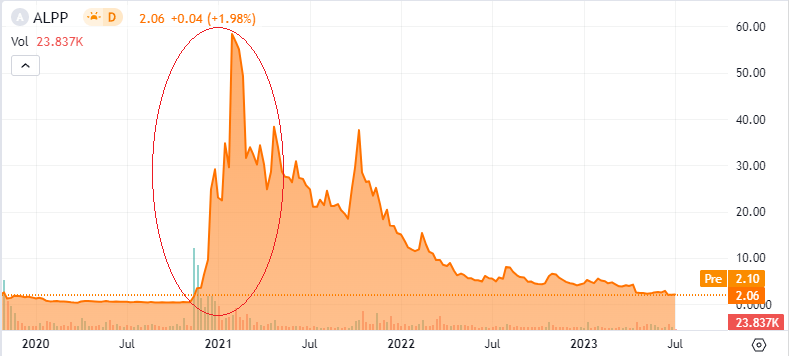

Looking at the upside risks, I think that there are two major ones. First, it's possible that I'm too pessimistic about Alpine 4's financial performance over the remainder of the year and that the company's revenues and margins improve over the coming months. This could provide a boost to the share price. Second, the share prices of microcaps can soar without any news or catalysts, which can lead to significant losses for short sellers. Alpine 4 itself is a good example of this, as its share price increased over 100 times between November 2020 and February 2021.

{kind=link}

This is a relatively thinly traded stock, with a daily trading volume rarely exceeding 50,000 shares.

Investor takeaway

In my view, Alpine 4 had an underwhelming start to 2023 as it continues to struggle to grow revenues organically. RCA's performance is particularly concerning as its revenues have been falling for several quarters and I think this is likely to be a key driver for total revenues declining below $100 million for the full year. In addition, synergies between Alpine’s subsidiaries are still lacking as margins continue deteriorating, and with general and administrative expenses surpassing $10 million in Q1 2023, I think that the net loss for the full year is likely to be above $20 million. Working capital and cash are decreasing, and I think that Alpine 4 could tap the equity market soon which would lead to significant stock dilution. That being said, I think that it could be best for risk-averse investors to avoid this stock as short selling seems dangerous. While the short borrow fee rate is just over 10%, it takes over 33 days to cover.

For further details see:

Alpine 4: 2023 Is Shaping As A Tough Year (Rating Downgrade)