PINE - Alpine Income Property: Talk About Best-In-Class

2023-10-03 10:06:29 ET

Summary

- Alpine Income Property Trust, Inc.'s straight-line lease agreements and fixed-rate debt obligations provide it with a significant advantage in a tough interest-rate environment.

- As a cash-heavy investment fund, Alpine possesses the opportunity to securing high-yielding acquisitions while commercial real estate valuations compress.

- Alpine's dividend profile is alluring. Moreover, an absolute valuation suggests the REIT is undervalued.

- Risks such as a devalued asset base and a high VaR number must be considered. However, we believe Alpine possesses more positives than negatives at this time.

Today's analysis examines Alpine Income Property Trust, Inc. ( PINE ) . As a real estate investment trust, or REIT, Alpine makes for an interesting analysis, given the recent volatility of that asset class. Although much of the REIT's prospects are systemic, Alpine possesses various idiosyncratic features that we believe could come into play in the final months of 2023.

Without further delay, let's move on to the analysis.

Portfolio Review

This section assumes an accounting-based vantage point. In other words, it looks at Alpine's operations and identifies how they might affect its prospective financial statements.

Leases

From an income perspective, the first thing to consider is that more than 94% of Alpine's leases are fixed and amortized on a straight line. What does this mean? It means that the bulk of Alpine's income is non-cyclical, especially if it is factored in that 63% of the REIT's tenants are investment-grade companies.

{kind=link}

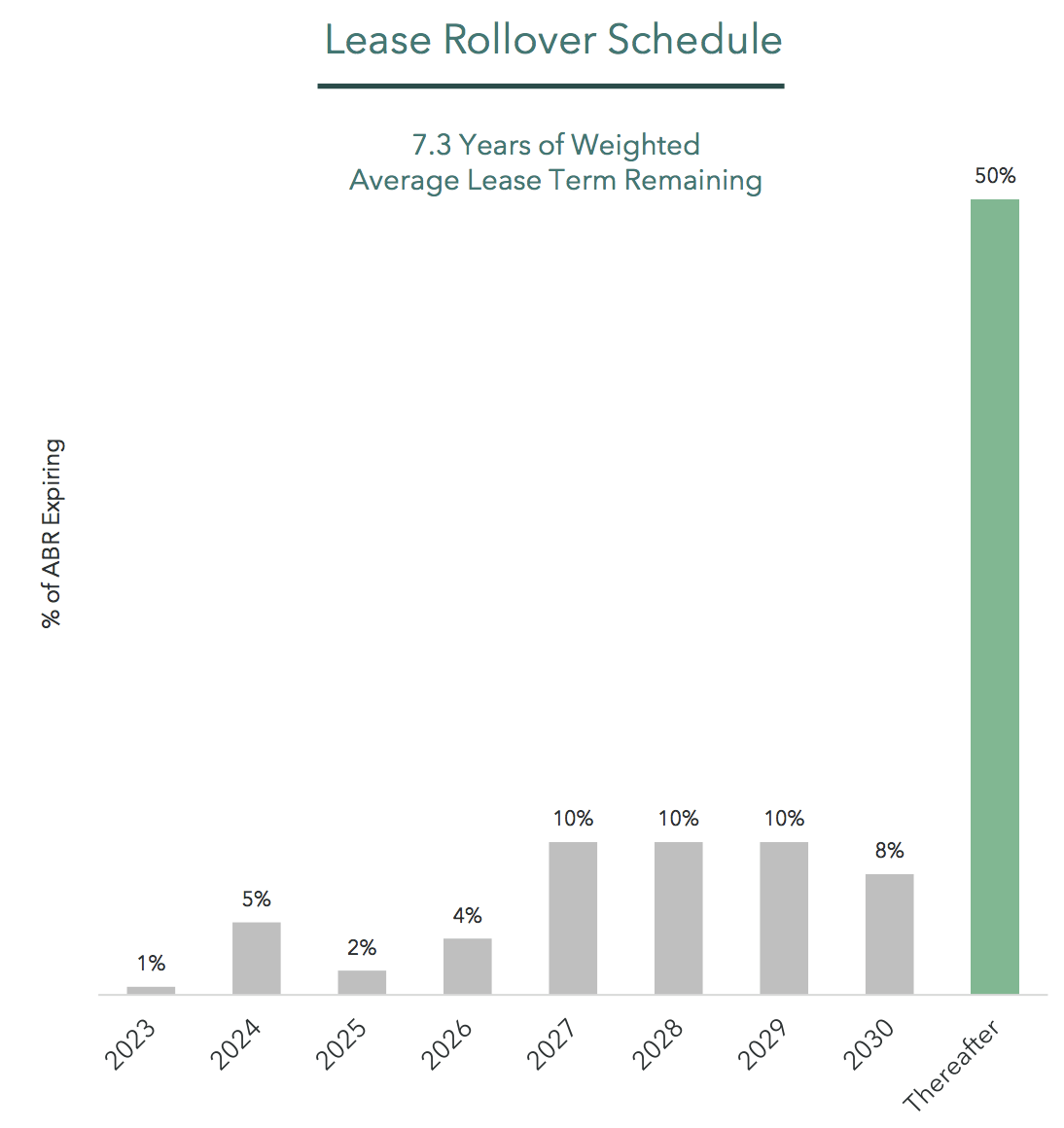

The remaining tenure of Alpine's average tenant (weighted for size) is 7.3 years. In our view, most of Alpine's long-term leases will be renewed, or prompt turnover will occur. As a premise, the REIT is running on 99.5% occupancy and hosts established businesses as tenants. Therefore, demand doesn't seem to be an issue.

{kind=link}

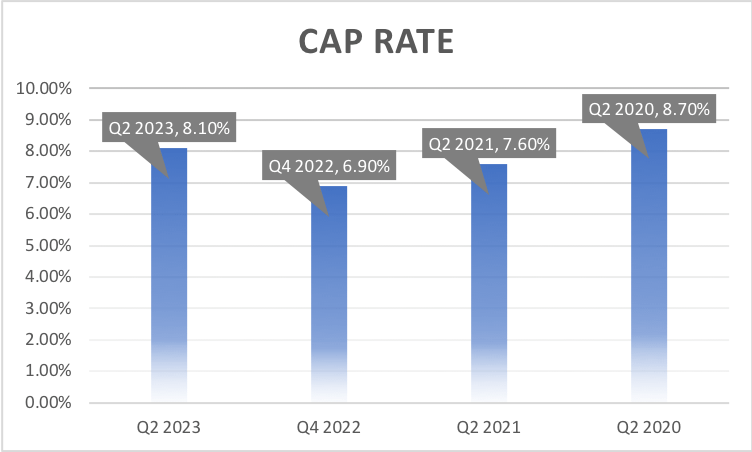

I dug up Alpine's recent cap rates to illustrate the sustainability of its tenant base – For further exposition, the average cap rate within the U.S. currently sits below 6% .

We believe Alpine's cap rates will increase in the next few quarters. A few reasons substantiate the claim, with the first being receding property valuations, which isn't a desirable way to increase your cap rate. However, positive factors such as sustainable rental escalation and undervalued acquisitions (discussed later) might come into play, raising Alpine's cap rate organically.

Author's Work, Data from Alpine

{kind=link}

Property Valuations

Despite its growing rents, Alpine faces valuation risks.

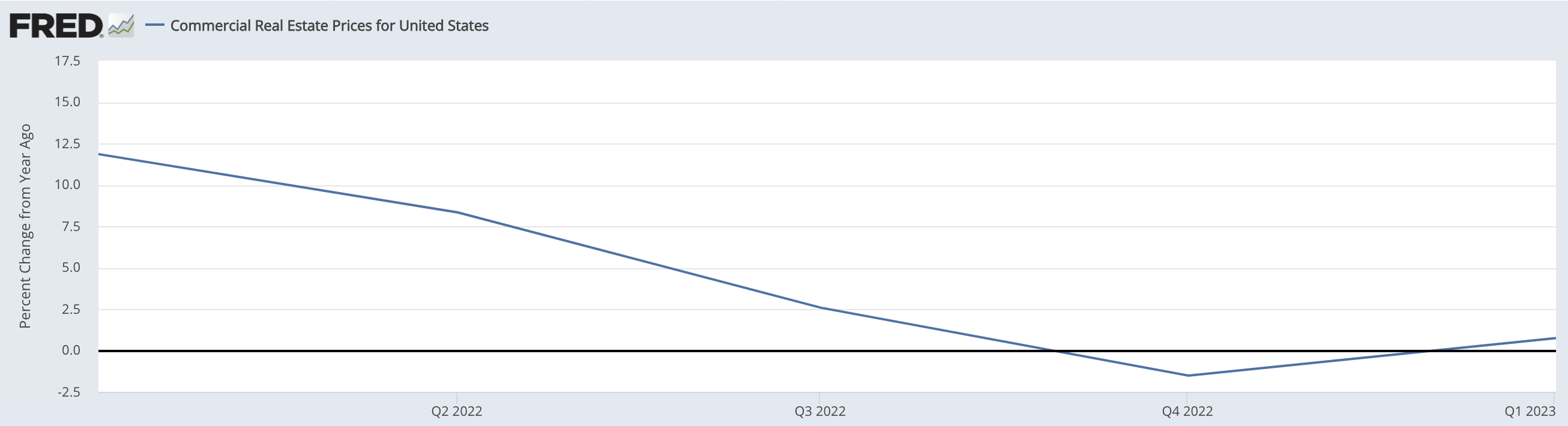

According to the REIT's 10-Q , it values its assets via a combination of market-based and real valuation metrics. Whether market-based or real value, we think Alpine's valuations will flatline in the coming quarters as factors such as lower repeat sales price growth and higher interest rates come into effect. Keep in mind that real estate and commercial real estate is a cyclical environment; as such, temporary dips are a frequent occurrence.

U.S. Commercial Real Estate Prices (St. Louis Fed)

{kind=link}

On the plus side, lower market valuations provide Alpine with a glorious opportunity to acquire undervalued assets. Capital is scarce at the moment, and liabilities are running high; therefore, many property owners are likely being forced to sell their units below their fair values. Thus, cash-rich REITs such as Alpine have golden opportunities.

To provide an example of my aforementioned claim, Alpine acquired nine retail properties in Q2, amounting to $60.5 million in transactional value. Further, the REIT secured a weighted-average going-in cap rate of 6.8% on the units, illustrating the high-yielding deals on offer in today's market.

In essence, Alpine's existing assets are taking a bit of a knock in the current economic environment. However, we anticipate its existing asset base to revert to mean in due course; moreover, we think Alpine has a rare opportunity to lock in high-yielding acquisitions as commercial property valuations are compressing.

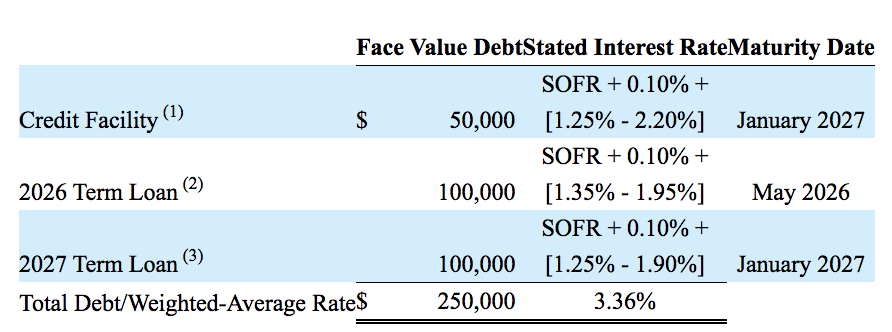

Favorable Debt Structure

Another alluring component of Alpine Income Property Trust is its capital structure. The REIT has no floating-interest exposure on its long-term debt, meaning the elevated interest rates currently experienced are unlikely to affect the vehicle.

{kind=link}

In our view, Alpine's 3.36% cost of debt and fixed-rate terms allow it to pass along significant value to its shareholders throughout the economic cycle.

Market-Based Variables

Valuation

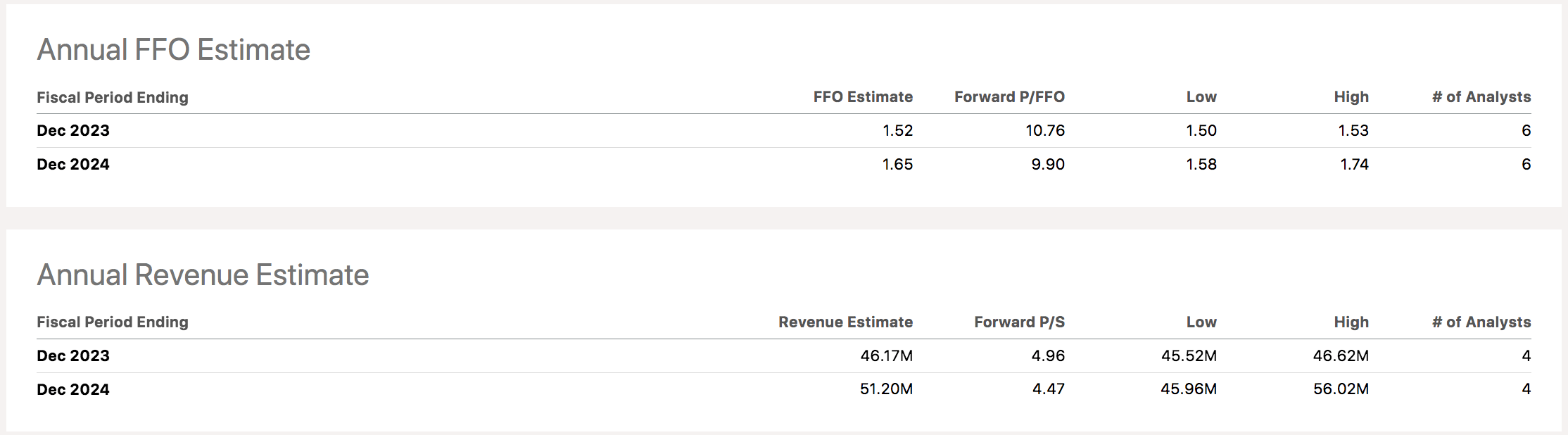

There's a reasonable amount of market-based data available on Alpine. Therefore, I decided to use the P/E Expansion formula (P/FFO in a REIT's case) to value Alpine Income Property Trust, and, based on the available data, Alpine has a fair price target of 18.51x by December 2024, which is approximately 14% higher than its current market price.

Formula = Sector Median P/FFO x FFO Estimate for Dec 2024

{kind=link}

Investors should ideally combine numerous valuation metrics before deciding whether an asset is undervalued or not. However, the method applied above holds reasonable strength as it is frequently applied across the investment industry.

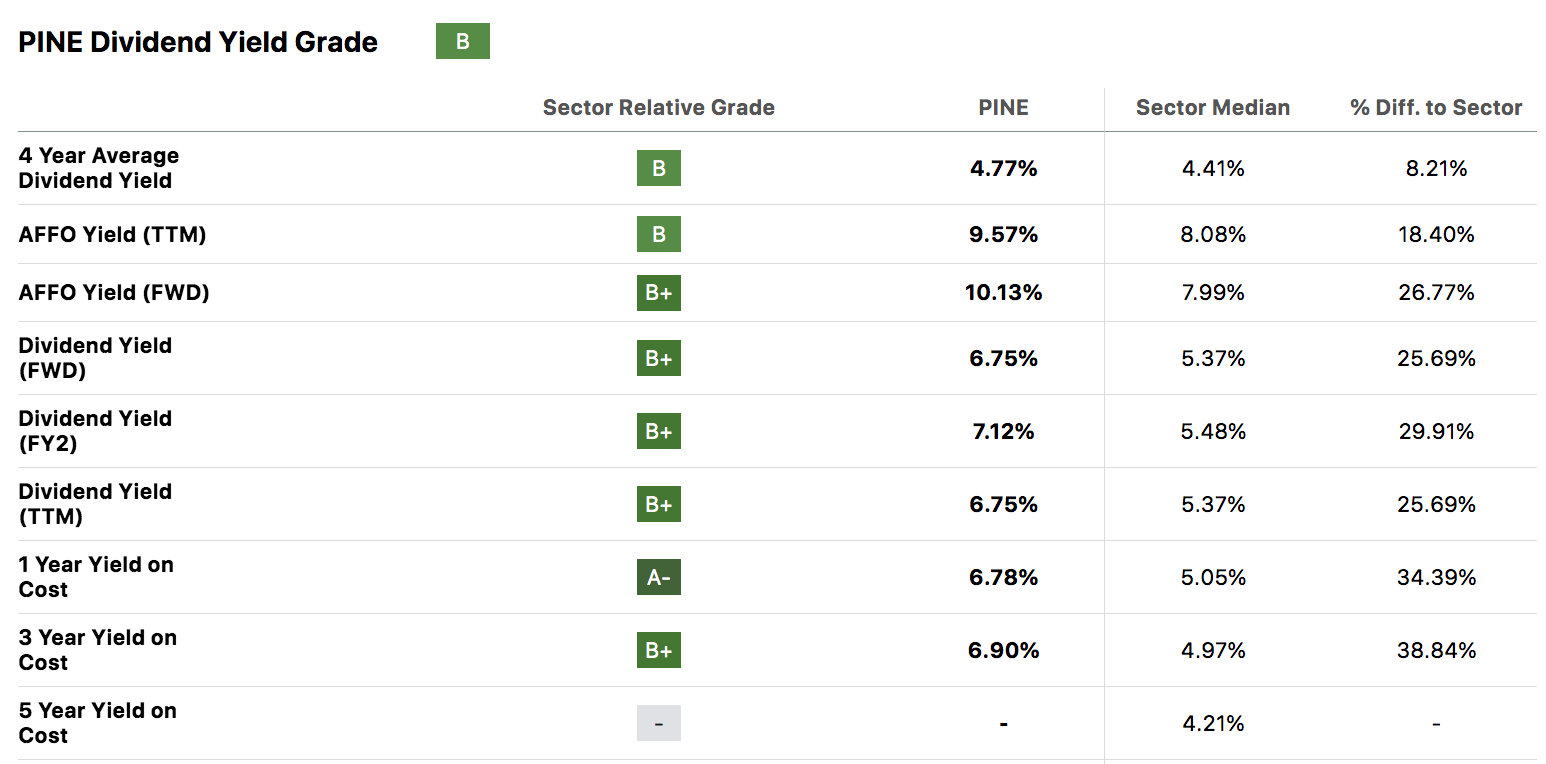

Dividends

Alpine presents a solid dividend profile. The REIT's 3-year average dividend yield-on-cost of 6.90% is owed to robust portfolio growth paired with an efficient capital structure. Although cyclicality risk cannot be overlooked, the signs are that Alpine will pay a sustainable dividend for now.

{kind=link}

Risks

Let's sum up a few of Alpine's risks.

As mentioned earlier in the article, valuation risk remains a concern to Alpine. Although the REIT might profit from new acquisitions, its existing asset base will likely experience prolonged headwinds, which might influence the REIT's market price.

Furthermore, a "higher for longer" interest rate environment might eventually pull Alpine's cost of capital upward. Sure, the REIT's existing fixed-rate debt is priced relatively cheaply; nevertheless, any new issuances will likely carry higher coupons and diminish shareholder value.

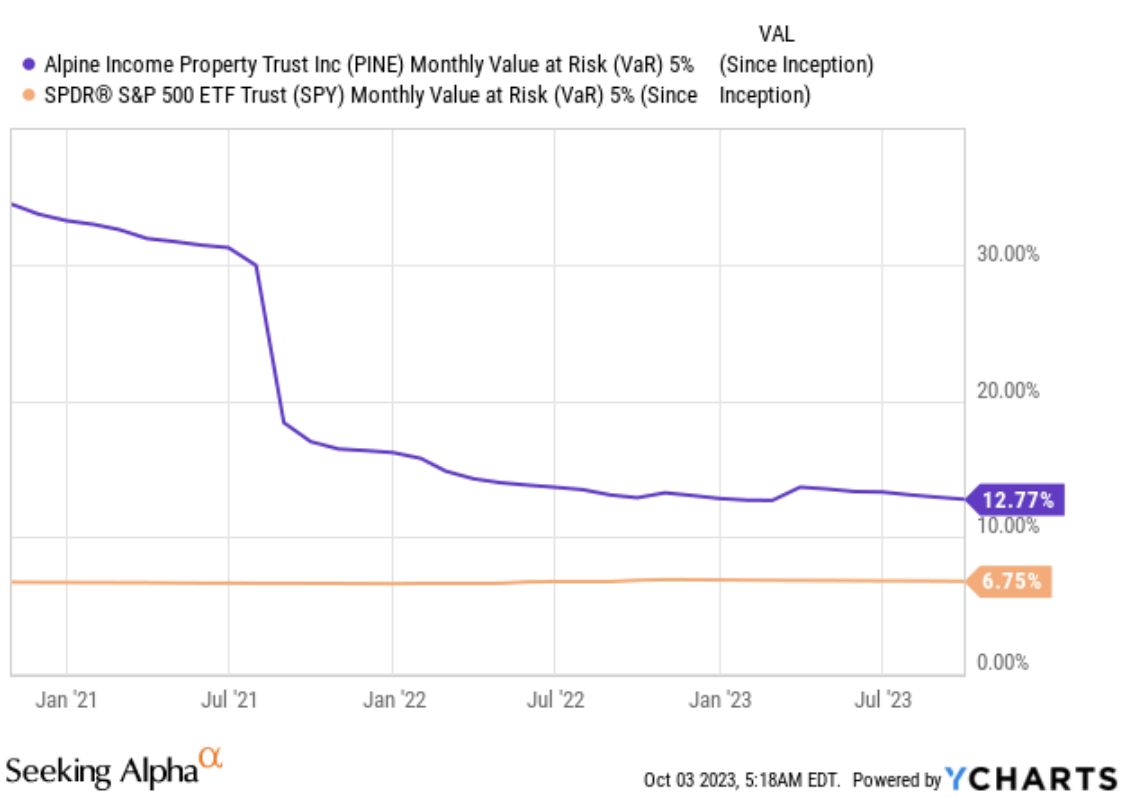

Lastly, as illustrated in the diagram below, Alpine has a high value-at-risk reading, suggesting that it may experience excess drawdowns in a bear market, which is certainly something investors should consider before committing to a final investment decision.

{kind=link}

Concluding Thoughts

Our analysis shows that Alpine Income Property Trust presents solid risk-return attribution.

Although some U.S. REITs are in a hint of trouble, Alpine's straight-line rent and fixed-rate debt provide it with a distinctive advantage. Moreover, an absolute valuation suggests the REIT is undervalued, with its alluring dividend profile providing an added bonus.

After netting out Alpine's positives and negatives, we decided on a strong buy rating.

For further details see:

Alpine Income Property: Talk About Best-In-Class