SNY - Alpinum Investment Management AG Q1 2024 Investment Letter

2023-12-28 10:00:00 ET

Summary

- Alpinum Investment Management is a Swiss asset manager whose key areas of expertise include. traditional and alternative credit investments, direct lending and hedge funds.

- The economy faces a slowdown with rising capital costs, yet resilient consumers and government support avert an imminent recession. Markets expect a "soft landing" economic cooling. Market sentiment pivoted favourably as the perception of inflation underwent a positive shift.

- Anticipated 2024 Fed rate cuts, a departure from the prior hawkish stance led to a decline in US Treasury yields to 3.9%, signalling an expected 150 basis point reduction. Mild inflation data reinforces the belief that the ECB has finished its hiking cycle, increasing the probability of maintaining a restrained policy stance.

- The onshore CSI 300 fell by 14.0% in 2023, reflecting weak domestic demand and persistent deflationary pressures in China. The potential imposition of peace in Ukraine and the dynamics of the US election year could trigger significant positive market reactions.

Market pivot on inflation perception

In 2023, global financial markets witnessed a significant surge in equities, with the S&P 500 ( SP500 , SPX ) seeing a year-to-date increase of 22.4%, surpassing global bonds. Market sentiment pivoted favourably as the perception of inflation underwent a positive shift, mirroring the 2020 response to the Covid situation. The remedy this time is the alleviation of transient inflationary pressures and an economic slowdown, contributing to market stability. The normalisation process will lead to inflation rates, real interest rates and budgets that are historically more typical, resulting in valuations aligning closer to historical norms.

Chart 1: Equity markets anticipate low, but positive growth

Source: Alpinum Investment Management

The fourth quarter brought exceptional gains, especially in fixed income, driven by evolving expectations favouring substantial Fed rate cuts in 2024. This shift is reflected in the decline of US treasury yields, to 3.9%, anticipating 150 basis points of rate cuts in 2024. While positive Q3 earnings surprises in the S&P 500 are acknowledged, concerns persist about deteriorating global economic conditions, particularly in developed economies. There is a risk of underestimating negative growth momentum amid geopolitical uncertainties. Market vulnerability is emphasised, with concerns about the global economic outlook, including slowing growth, rising headwinds in consumer spending and elevated valuations.

United States

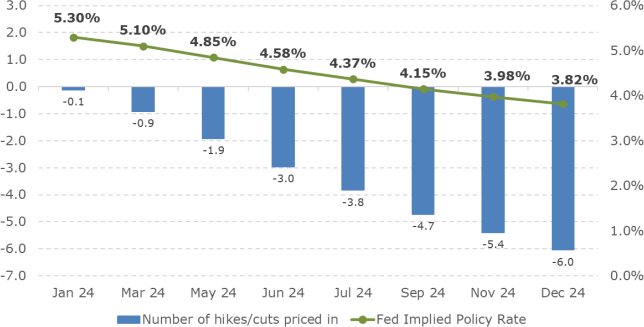

The November US Consumer Price Index ('CPI') revealed a tempered trajectory, with year-on-year declines in headline and core inflation to 3.1% and 4.0%, respectively. Driven by lower energy and gasoline prices, optimism grew for achieving 2% inflation by year-end in 2024. Investor expectations of a decisive interest rate hike by the Federal Reserve in December waned, followed by revised expectations for policy rates, indicating an anticipated 150-basis-points reduction in 2024. Despite indications of peak policy rates, the November FOMC minutes affirmed the Fed's commitment to sustained elevated rates.

Chart 2: Fed implied policy rates

Source: Alpinum Investment Managemen

{kind=link}

In Q3, the US GDP exhibited robust expansion, surpassing expectations by accelerating from 2.1% q/q to 5.2% q/q annually. The economy demonstrated resilience, fuelled by increased consumption and positive contributions from private inventory investment, government spending, and residential fixed investment. Despite signs of a cooling economy, including modest upticks in jobless claims and rising credit card delinquencies, optimism for a soft landing persisted, supported by ongoing economic momentum and tight labour markets. The S&P 500 Index rose 22.4% year-to-date, and core government bonds rebounded, with the 10-year US government bond yield falling below 4.2% despite Moody's negative outlook on US sovereign debt. In the housing sector, US home prices peaked in September, with a 0.7% monthly increase, slightly lower than August's 0.8% rise. Annually, house-price appreciation accelerated from 2.6% to 4.0%. However, new home sales contracted by 5.6% in October, below the expectations of a 5.1% decline, with a revision of September's increase from 12.3% to 8.6%. Escalating 30year mortgage rates, reaching a 23-year high by October's end, contributed to subdued housing demand.

Europe

Eurozone economic indicators provided a mixed picture in recent releases. CPI data from Germany and Spain showed moderation in price pressures, with both monthly and annual measures falling below expectations. The European Commission's indicators for economic, industrial, and services confidence exceeded expectations in October, providing a positive sentiment despite slight deteriorations in economic and industrial confidence. Germany's Q3 economic contraction of 0.1% q/q, although better than expected, underscores the overall weakness of the Euro area's largest economy. Soft inflation prints support the expectation that the ECB has concluded its hiking cycle, with the likelihood of maintaining a restrictive policy stance. However, credit indicators caution of the potential impact of tighter policy on the economy, and European equities are expected to face headwinds in the coming months. Eurozone retail sales continued to decline in September, while flash PMI estimates for November showed slightly less pessimism, with the composite PMI climbing to 47.1.

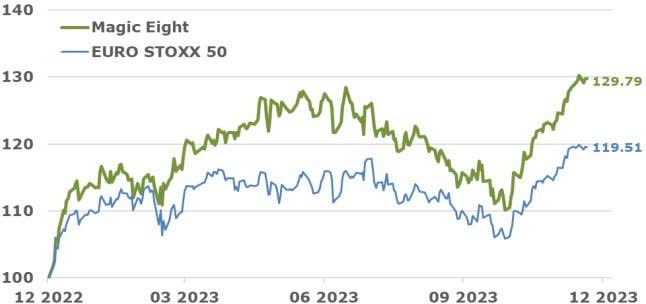

Chart 3: “Magic Eight” of the EURO STOXX 50

Source: Alpinum Investment Management

{kind=link}

Europe has its "Magic Eight" (the counterpart to the "Magnificent Seven" in the USA), large-cap stocks contributing significantly to EURO STOXX 50 ( SX5E ) gains: Air Liquide ( AIQUF ), ASML , L’Oréal, LVMHF , Sanofi ( SNY ), SAP , Schneider Electric ( SBGSF ), and Siemens ( SIEGY ). With a 21.8% share of the EURO STOXX 50 market capitalisation, they have been responsible for 50% of the price gains since 2015 and contributed 6.5% to the current 19.5% in 2023. However, their downside is being deemed expensive, trading at 21.2 times forward earnings compared to EURO STOXX 50's 12.6 times. Finally, in the UK, the economy avoided a contraction in Q3 due to strong trade performance, despite declines in consumer spending, business investment and government spending. The outlook for UK Gilts remains influenced by inflation and interest rate expectations, with signs of economic activity bottoming.

China and emerging markets ('EM')

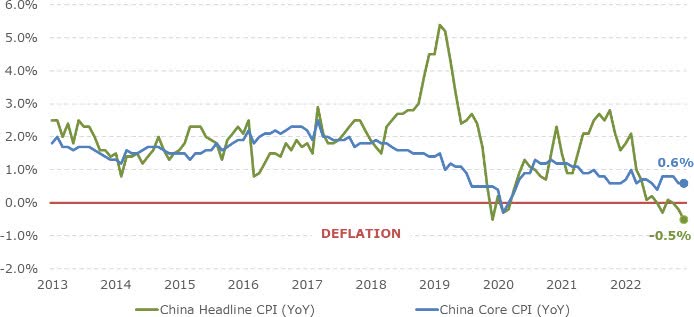

China's central bank, the People's Bank of China (PBOC), adhered to market expectations by intensifying liquidity injection while maintaining a 2.5% interest rate on 1.45 trillion yuan of one-year medium-term lending facility ('MLF') loans. With 850 billion yuan of MLF loans expiring, the operation resulted in a net 600-billion-yuan injection into the banking system. In the third quarter, China exceeded economic growth forecasts due to robust retail sales and government stimulus, offsetting the impact of the property crisis. However, October's trade data revealed a mixed outlook, with an unexpected import pickup contrasting with sluggish global demand for Chinese goods. China's CPI and PPI for October indicated deflationary pressures, supporting a targeted stimulus approach over expansive measures.

Chart 4: Core and headline inflation in China (YoY)

Source: Alpinum Investment Management

{kind=link}

House prices continued their decline, particularly in lower-tier cities, marking the fifth consecutive month of contraction. The Chinese government is taking decisive steps to address the property crisis, urging banks to address a USD 446 billion funding gap. Money and credit data for October depicted weakness, with total social financing below expectations and a decline in bank loans. Money supply indicators reveal slowing growth: M0 and M1 money growth dropped to 10.2% y/y (from 10.7%) and 1.9% y/y (from 2.1%), respectively, falling below the anticipated 2.5% y/y. The diminishing ratio between M1 and M2 money supply signals weakening private sector confidence. The recent weakening of the US dollar has alleviated pressure on the renminbi. The onshore CSI 300 dropped 14.0% since the beginning of the year, reflecting the subdued domestic demand and persistent deflationary pressures in China's economy.

Investment conclusions

The economy faces a slowdown due to increased capital costs, but resilient consumers and a supportive government mindset prevent an imminent severe recession. Markets anticipate a controlled economic cooling, embracing a "soft landing”. The "new normal" includes slightly higher structural inflation, elevated fiscal spending and ongoing regulatory support for troubled banks. High government debt and geopolitical factors contribute to sustained inflationary pressures, prompting global shifts like "re- or near-shoring". Potentially, the imposition of peace in Ukraine and the dynamics of the US election year might become events with significant potential, eliciting positive market reactions overall.

Chart 5: Yields in context with downside risk

Source: Alpinum Investment Management

Bonds: In light of rising default rates and the recent tightening in credit spreads, “credit” as an asset class is valued fairly, but selective bottom-up opportunities are still plentiful. We maintain a positive bias on duration exposure, considering it a valuable portfolio diversifier in the current economic cycle. We emphasise shorter maturities to mitigate risks associated with a potential steepening yield curve as the year progresses. We are positive on fixed income in general, both for IG and HY. However, our highest conviction is still on European loans, short-term HY bonds as well as CLOs.

Equities: Limited upside for US equities due to high (US-) multiples and vulnerable profit margins. Our preference within equities is non-US markets, maintaining a diversified strategy. Generally, we maintain our positive bias and our neutral positioning in equities and have an overweight position in credit exposure.

DisclaimerThis is an advertising document. This document does not constitute an offer to anyone, or a solicitation by anyone, to make any investments in securities. Such an offer will only be made by means of a personal, confidential memorandum. This document is for the intended recipient only and may not be transmitted or distributed to third parties. Past performance is not a guide to future performance and may not be repeated. You should remember that the value of investments can go down as well as up and is not guaranteed. The actual performance realized by any given investor depends on, among other things, currency fluctuations, the investment strategy invested into and the classes of interests subscribed for the period during which such interests are held. Emerging markets refer to the markets in countries that possess one or more characteristics such as certain degrees of political instability, relative unpredictability in financial markets and economic growth patterns, a financial market that is still at the development stage, or a weak economy. Respective investments may carry enhanced risks and should only be considered by sophisticated investors. Nothing contained in this document constitutes financial, legal, tax, investment or other advice, nor should any investment or any other decisions be made solely based on this document. Although all information and opinions expressed in this document were obtained from sources believed to be reliable and in good faith, no representation or warranty, express or implied, is made as to its accuracy or completeness and no liability is accepted for any direct or indirect damages resulting from or arising out of the use of this information. All information, as well as any prices indicated, is subject to change without notice. Any information on asset classes, asset allocations and investment instruments is only indicative. Before entering into any transaction, investors should consider the suitability of the transaction to their own individual circumstances and objectives. We strongly suggest that you consult your independent advisors in relation to any legal, tax, accounting and regulatory issues before making any investments. This publication may contain information obtained from third parties, including but not limited to rating agencies such as Standard & Poor’s, Moody’s and Fitch. Reproduction and distribution of third-party content in any form is prohibited except with the prior written permission of the related third party. Alpinum Investment Management AG and the third-party providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and will not be responsible for any errors or omissions (negligent or otherwise), or for the results obtained from the use of such content. Third-party data is owned by the applicable third parties and provided for your internal use only. Such data may not be reproduced or re-disseminated and may not be used to create any financial instruments or products, or any indices. Such data is provided without any warranties of any kind. If you have any enquiries concerning the document, please contact your Alpinum Investment Management AG contact for further information. The document is not directed to any person in any jurisdiction which is prohibited by law to access such information. All information is subject to copyright with all rights reserved. Any communication with Alpinum Investment Management AG may be recorded. Alpinum Investment Management AG is incorporated in Switzerland and is FINMA licensed and regulated. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Alpinum Investment Management AG Q1 2024 Investment Letter