DFE - Alpinum Investment Management AG Q4 2023 Investment Letter

2023-10-12 05:10:00 ET

Summary

- Alpinum Investment Management is a Swiss asset manager whose key areas of expertise include. traditional and alternative credit investments, direct lending and hedge funds.

- The economic outlook is soft, but not disastrous. US economy demonstrates strong resilience, highlighted by robust labour market conditions, and documented by a solid 2.4% annualized real GDP growth rate in Q2. There are no signs for a severe US recession.

- During the quarter, the Federal Reserve raised the key interest rate range by 25 basis points, reaching a 22-year high of 5.25% to 5.50%.

- Europe grapples with an economic downturn driven by higher interest rates, lower consumption, and fiscal restraint. A significant decline in business activity has arrived, whereas Germany has already entered recessionary territory.

- China's economy faces deflationary pressures, with negative CPI and PPI, weak retail sales growth, and a struggling real estate sector.

“Muddling through” is a benign outcome

Central banks' unwavering commitment to curbing inflation and mitigating economic deceleration remains a central concern. The era of escalating interest rates appears to be drawing to a close, giving rise to expectations of a protracted period marked by elevated interest rates. Thus far, the economic repercussions of this heightened interest rate environment have proven to be manageable, albeit with certain sectors and companies facing challenging adjustments. The global economy continues to exhibit remarkable resilience, with no discernible indications of an impending US recession on the horizon. In the second quarter, the US GDP surpassed initial expectations, underlining the persistence of disinflationary pressures and the robustness of the labour market.

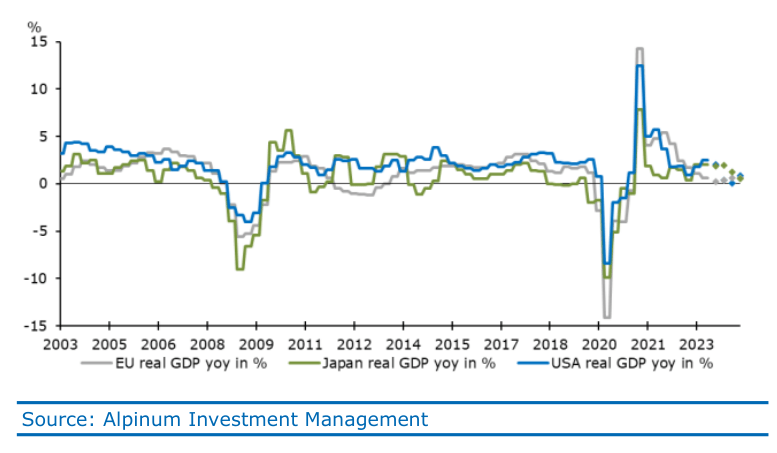

Chart 1: Potential stagflation but no ((deep)) recession

{kind=link}

In the United States and Europe, the prevailing economic climate can be described as a state of 'muddling through', characterized by subdued yet positive real growth in the United States, estimated to range between 1-3%, while Europe experiences meagre growth prospects. This landscape is underpinned by the anticipation of vigorous government expenditure, modestly favourable corporate investments, and the resurgence of inflationary forces. At present, the most prominent risks to this outlook encompass the precarious condition of the Chinese property market, coupled with the looming spectre of long-term US Treasury rates inching closer to the 5% threshold.

United States

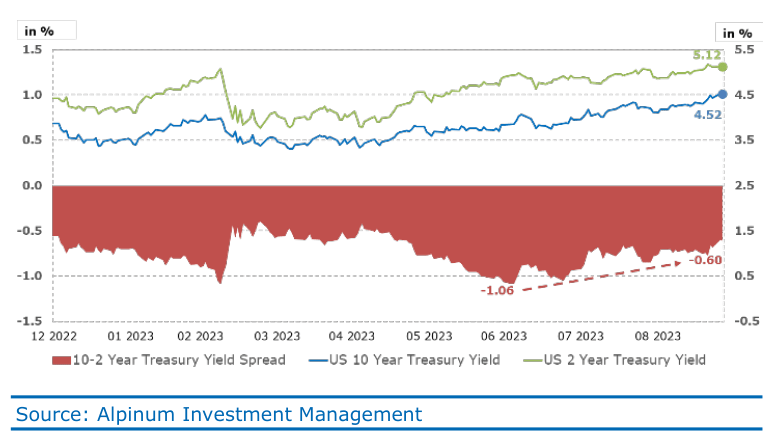

Fitch Ratings' recent credit rating downgrade of the United States from AAA to AA+ underscored the nation's deteriorating fiscal conditions, mounting public debt, and declining governance standards. Amidst these challenges, the US economy exhibited notable resilience during the quarter. In August, the labour market demonstrated its strength as nonfarm payrolls expanded by 187,000, despite a slight uptick in the unemployment rate to 3.8%. However, the trajectory of inflation remained equivocal. While the Consumer Price Index ((CPI)) for August fell short of expectations, elevated shelter inflation persisted. Concurrently, the Producer Price Index ((PPI)) recorded an ascent, primarily driven by price increases in services. Inflation expectations for the coming year reached a level (3.5%) not witnessed in over two years. In the meantime, the yield on 10-year government bonds propelled to over 4.5%.

Chart 2: Less inverted US Treasury yield curve

{kind=link}

In a surprise turn, second-quarter GDP figures exceeded forecasts, with an annualized real GDP growth rate of 2.4%. This notable performance was boosted by robust consumption and substantial business fixed investments, partly offset by a modest decline in net exports. In addition, oil prices surged to their highest levels since November 2022 due to unexpected developments within the OPEC+ alliance. West Texas Intermediate ((WTI)) crude oil traded above USD 90 per barrel. In July, the Federal Reserve ((Fed)) raised the key interest rate range by 25 basis points, reaching a 22-year high of 5.25% to 5.50%. This move had been well-telegraphed by various Fed officials. In September, the Fed decided to keep interest rates unchanged. Federal Reserve Chairman Jerome Powell reiterated the central bank's willingness to enact further rate hikes, contingent upon incoming economic data, especially the timing of additional increases. Market indicators suggest the likelihood of one final rate hike of 25 basis points in 2023, followed by a potential series of rate cuts in the second half of 2024.

Europe

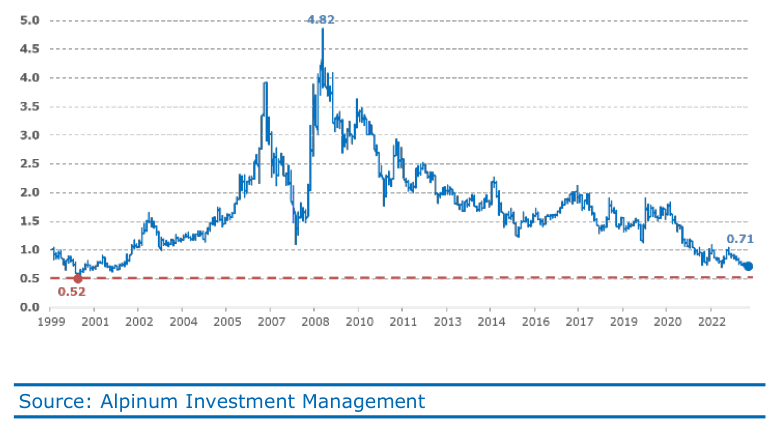

Europe faces a confluence of economic challenges marked by the potential for a recession, primarily driven by higher interest rates and a resurgence of fiscal restraint. In the past quarter, Europe experienced a significant decrease in business activity, as indicated by a purchasing managers' survey, reaching its lowest point in almost three years. This decline was particularly pronounced in Germany, the economic leader of the region, which saw its most substantial monthly drop in business activity in over three years, highlighting wider economic apprehensions. At the same time, the European Central Bank (ECB) has implemented its 10th consecutive rate hike by raising rates another 25 basis points, indicating the likely end of the tightening cycle and the confidence in achieving the target inflation level within the forecast horizon. Despite these challenges, European stocks present compelling valuations when compared to their US counterparts. Earnings projections have reached historic highs, and the forward price-to-earnings ratio of the STOXX 600 in comparison to the S&P 500 indicates that European stocks are substantially more appealing.

Chart 3: Valuations of European compared to US stocks

{kind=link}

On the flip side, the economic outlook in Europe continues to be uncertain. While Eurozone GDP experienced modest growth in the second quarter of 2023, labour markets remain tight. Inflation, although showing slight moderation, remains elevated, which sustains expectations of future rate hikes by the ECB. During the quarter, the MSCI Europe ex-UK index faced headwinds, particularly in the banking sector, due to Italy's announcement of a tax on banks' excess profits. European bond yields remained stable. Despite a BoE rate hike, the UK economy had a positive Q2 2023 (+0.2%), marked by robust wage growth. Expectations of more rate increases remained, leading to a rise in the 10-year Gilt yield while the FTSE All-Share underperformed global peers.

China and emerging markets ( EM )

China's economic landscape in recent months has been marked by several concerning trends. In the past quarter the Consumer Price Index ((CPI)) in China dipped into negative territory at -0.3% year-on-year, indicating deflationary pressures. Simultaneously, the Producer Price Index ((PPI)) recorded its eleventh consecutive month of deflation, reflecting a sustained period of falling prices in the manufacturing sector. Retail sales growth in China also disappointed, registering at just 2.5% year-on-year, significantly below expectations of 4.5% year-on-year. The real estate sector, in particular, bore the brunt of these challenges, experiencing an 8.5% drop in investment between January and July. Notably, property developers like Country Garden and Evergrande faced difficulties, underscoring the fragility of the real estate market in China.

Chart 4: MSCI China Index compared to the S&P 500 Index

{kind=link}

In August, the People's Bank of China (PBoC) responded to looming deflationary risks with two interest rate cuts, aiming to stimulate economic activity and combat deflation. Despite these efforts, the Renminbi continued its year-long depreciation against the USD, with a YTD decline of 5.6%. Simultaneously, the CSI 300 index, reflecting China's leading firms, hit its lowest point of the year. In stark contrast, Japan demonstrated impressive resilience during the same period. In Q2 2023, Japan’s economy expanded significantly by 4.8% quarter-on-quarter, primarily driven by strong contributions from net trade. An encouraging sign of recovery from deflation emerged as Japan's core CPI increased by 10 basis points, reaching 4.3% YoY in July. Japanese equities showcased this resilience by outperforming many global markets, with the Topix index surging by 3.6% in the third quarter. This performance underscores Japan's economic strength relative to its global counterparts and hints at a promising trajectory beyond deflationary concerns.

Investment conclusions

The economic growth outlook is soft, but not disastrous. Tightening measures slow growth, affecting regions differently, leading to a slowdown or stagflation in the United States, stagnant growth or stagflation in Europe, and stronger emerging markets from a weak basis. Monitoring the resilience of the US consumer is crucial. Inflation is gradually decreasing, with sticky core inflation leading to a slow adjustment. Monetary tightening is nearing its peak, but rate cuts are not expected in the near future. Real rates have risen significantly in the last three months, surpassing 2%, driven by decreasing inflation expectations. These higher long- and short-term real rates have become advantageous for fixed income investors in various credit market sectors. In particular, HY bonds and syndicated loans offer real yields that comfortably outperform equities, even with optimistic earnings growth assumptions.

Chart 5: Yields of syndicated loans at historic high, 10%

{kind=link}

Bonds: Monetary policies are in a tightening phase, approaching their peak and, with no expectations of a U-turn soon. Currently, markets are assuming a terminal policy rate close to 5.5%. We continue to favour European loans, IG, non-cyclical US and Scandinavian short-term HY bonds as well as structured credit.

Equities: Equity multiples remain challenged by rising interest rates and vulnerable/shrinking profit margins. Within equities, we continue to favour non-US markets, maintaining a mixed approach.

Our cautious stance with a neutral positioning has been the right action during these extremely uncertain times. We maintain a neutral position in equities and an overweight position in credit exposure.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Alpinum Investment Management AG Q4 2023 Investment Letter