AOMFF - Alstom: Compelling Narrative But Hold

2023-07-11 07:58:24 ET

Summary

- Alstom, a French multinational provider of rolling stock and related services, is recommended as a "Hold" due to limited upside and potential risks.

- The company's acquisition of Bombardier Transport has led to serious issues, negatively impacting its equity value, despite the strategic sense of the deal.

- The company received a credit downgrade from Moody's, and this could lead to further issues.

We present our note on Alstom (ALSMY) with a "Hold" rating. We explore major events including the Bombardier Transport acquisition and Moody's downgrade. We find the industry and Alstom's equity story attractive but we see little upside and plenty of risks, hence we recommend "Hold".

Alstom: Compelling ESG story but poor cash generation

Alstom is a capital goods company that is uniquely positioned in a growing fragmented market, supported by strong ESG tailwinds. In January 2021 it announced a transformational M&A deal which has since led to a range of serious issues, massively penalizing the equity value. As the company executes its plan to fix the botched acquisition the markets remain torn on the story. It is largely a consensual long on the sell-side with most analysts seeing considerable upside, while on the other hand, it is heavily shorted by hedge funds.

We will do a deep dive into the latest events, analyze differing viewpoints on key issues and drivers, and assess the potential implications for investors.

Alstom's Equity Story

Alstom is a French multinational provider of rolling stock and related services. The company operates worldwide in rail transport markets through the following segments: Rolling Stock, Services, Signalling, and Turnkey.

The rail global market is set to grow LSD-MSD CAGR% into 2025, underpinned by strong trends in urbanization, growth of travel, environmental concerns, and prioritization of rail by public authorities.

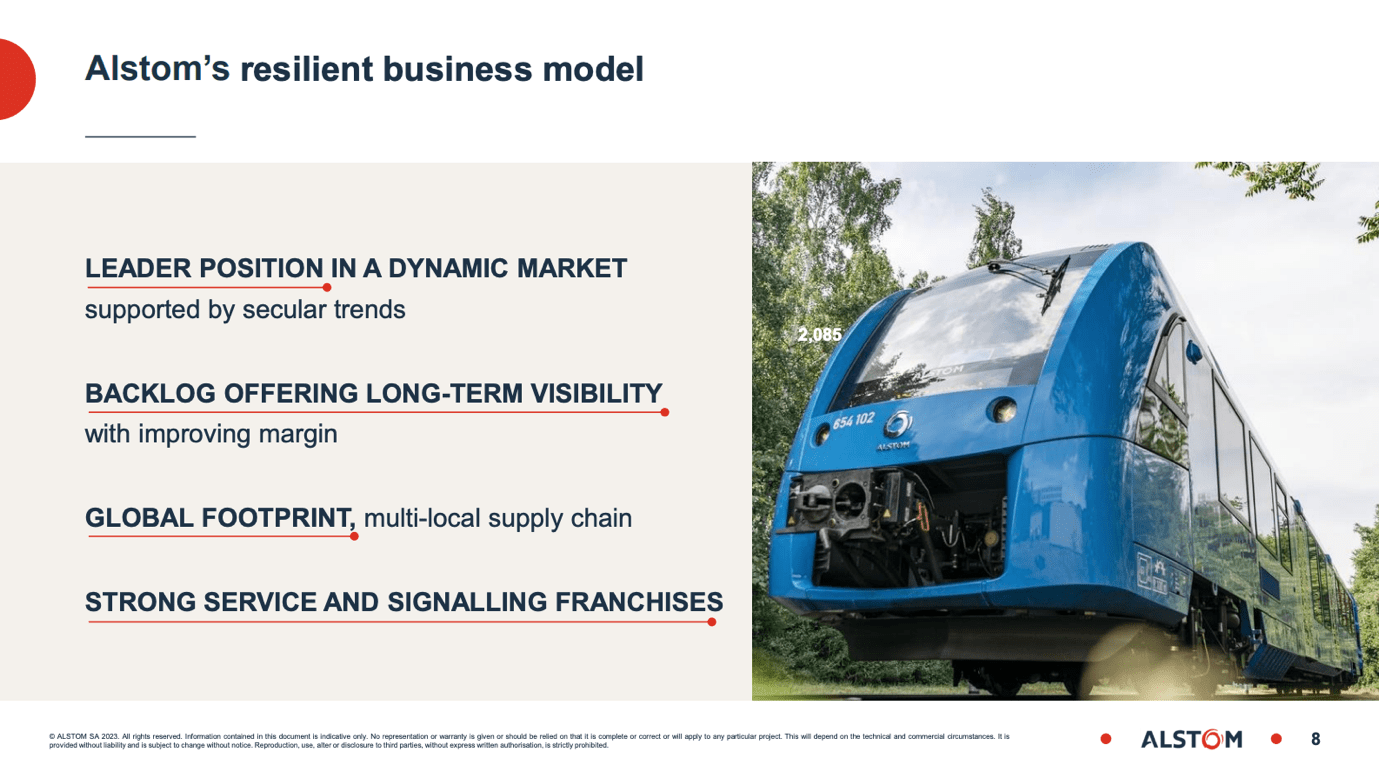

Alstom is a leader in Rolling Stock outside China. Rolling Stock is a large and steady market, with an estimated accessible market 2025-27 of €44 billion / year. The growth of the market is supported by France's rail plan , India's budget for rail 2023/24, US acceleration with Jobs & Infrastructure Act, and diesel replacement in Europe. Alstom has approximately 33% market share in Rolling Stock, or >20% more than its closest competitor. Major competitors include Siemens Mobility (SIEGY) (#2 player), Talgo (TLLGF), Hitachi ( HTHIY) , and Stadler Rail (SRAIF). The fragmentation of the market allows Alstom to consolidate by making smaller acquisitions.

The Rolling Stock product line acts as a key enabler to the Services and Systems businesses and the global installed base provides recurring maintenance revenue. Alstom has strong Services and Signalling franchises. It is #1 in the competitive Services market, with ca. €3.8 billion in sales (~€2bn more than number 2) with over 250 service sites, 1400 contracts, and €31 billion of backlog. This is a short-cycle business with contracts as long as 30 years and inflation indexation clauses. In the mid-term Alstom aims to have 35% of the Installed Base covered by Services contracts, a 10 points improvement vs. current levels. Alstom is the #2 player in the Signalling market (small difference with #1), with €2.4 billion in sales and €7.5 billion of backlog approximately 2/3rd of which originating from Alstom legacy and 1/3rd from Bombardier. The contracts are typically small in size and last less than 2 years, with few being above €100 million and lasting 3 years or longer. The Signalling market is growing at 4%+ CAGR while Alstom aims to grow its Signalling business by high single digits % CAGR.

{kind=link}

Alstom is now a global and unique player thanks to Bombardier Transport. It is benefiting from portfolio complementarity, geographic complementarity, and innovation catalysis. Moreover, synergies are on track, we will expand on that in the Bombardier acquisition section of our analysis.

The company has shown resilience in the face of high inflation with approximately 2/3rd of contracts being covered by cost inflation indexation clauses, and 70% of contracts with suppliers being price fixed or capped. Alstom has a backlog offering long-term visibility with improving margins. The backlog stands at >€87 billion, out of which €43 billion in Rolling Stock, €31 billion in Services, €7 billion in Signalling, and €6 billion in Systems.

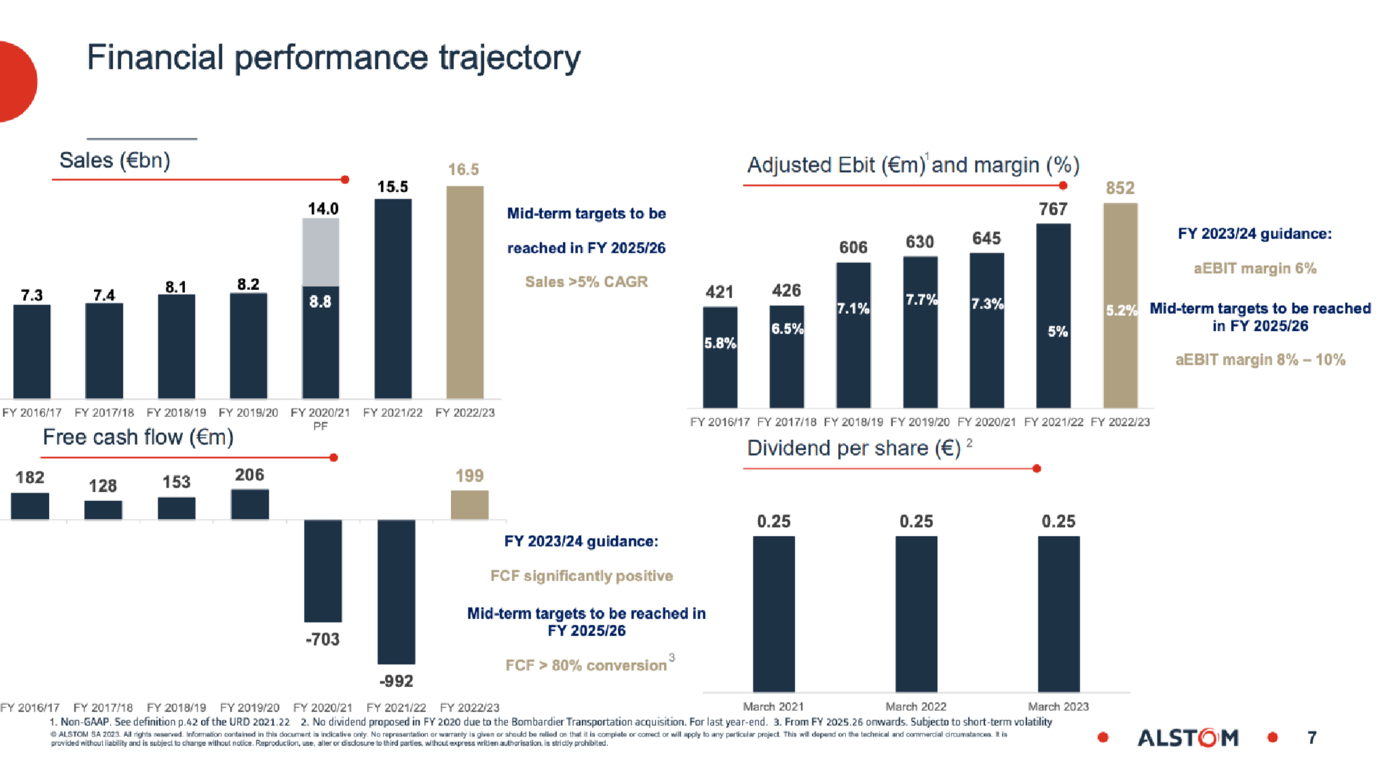

Alstom has set forward ambitious targets. By FY 2025/26 it aims to have a book-to-bill ratio above 1, a Sales CAGR higher than 5%, an EBIT margin between 8% and 10%, and an 80% conversion rate of Net income to Free Cash Flow.

Equity Story Presentation - Alstom's website

{kind=link}

Bombardier Transport Acquisition

Acquiring Bombardier Transport made sense strategically for Alstom but the period following the acquisition was very challenging. BT had issues that were widely known, and Alstom was aware of them. While Alstom knew of the complexity of the contracts, lack of expertise, and unsatisfactory coordination of operation, it turned out much worse, and Alstom had to set aside €630mn for contract provisions on top of the €450mn it had allocated when the acquisition closed.

The period after the announcement of the acquisition was particularly bad with BT widely underperforming - having issues with supplier payments and executing contracts very poorly with major defects such that the final product was not fit for the customers anymore~€6.7bn of contracts are expected to be 0 gross margin contracts, which effectively results in negative high single digits EBIT margins. €2.6bn of those have been executed until last FY, with another €2.6bn coming until the end of FY23, and the rest fading until 2024.

Over the last quarters, the provisions have stabilized, and Alstom has been working to amend the relationships with clients, reaching agreements on a majority of the projects that had been litigated. The roadmap for the integration of BT has been announced in July 2021, consisting of an initial stage of 2-3 years to stabilize the order book before benefiting from synergies within 4-5 years . So far Alstom has stuck by the announced timeline

~€100mn of synergies were achieved in FY'21-22, ramping up to €400mn in FY'23-24 and Alstom expects a run-rate target of €475-500mn of synergies from FY'25-26 onwards. The synergies will be achieved through procurement synergies, management overlaps, footprint production efficiency, best use of products through massification, and an alignment of BT's financing conditions with Alstom's.

We would like to note that there is an arbitration going on regarding the acquisition and we are monitoring the situation.

FY 22/23 Results

Alstom reported mixed FY results with sales and EBIT being in line with company complied consensus and FCF missing by ca. 4%. Medium-term EBIT and FCF targets were pushed by 1 year to FY25/26 due to macroeconomic conditions and Moody's downgraded Alstom ratings to the last investment grade level: Baa3.

Risks and the short thesis on Alstom

Short sellers believe there is an increasing threat from CRRC - China's leading rolling stock manufacturer - aiming to increase its market share. CRRC is effectively monopolistic and has been bidding on projects at ~30% lower than other players. It acquired Vossloh Locomotives, which potentially may indicate its interest in Europe, and has successfully bid for projects in the US. However, this threat has not materialized despite many years of discussions around this.

Moreover, some argue problems at Bombardier Transport will not be fixed as quickly and a multi-year underperformance is coming that is very hard to turn around as issues do not only relate to isolated contracts but to more structural problems such as culture, internal processes, etc. So far Alstom has executed its integration plan accordingly and this should be a key driver of its share price performance.

In addition, given the poor to inexistent free cash flow generation, the ability to reduce leverage organically is limited, and potentially receiving another credit downgrade (becoming junk), could cause liquidity issues if customers reduced the advance payments. Hence Alstom may need to raise €2+ billion in equity to restore confidence and lower the risk of another credit downgrade. The company has firmly committed to maintaining investment grade.

Valuation and conclusions

At first sight, there is much to like about Alstom, including strong underlying growth trends, ESG tailwinds, an industry-leading position, improving margins, and favorable sell-side ratings. However free cash flow generation remains limited, and investor scares about a potential equity raise and a further credit downgrade are, in our opinion, valid concerns. Below we value Alstom using an EV/EBIT methodology common for capital goods companies and a FCF Yield% approach given the focus of the financial markets on this particular metric for Alstom.

We project 5% sales growth until FY2026 and a linear margin progression up to 8% adjusted EBIT margin, as per the guidance. We are in line with consensus on sales growth and a couple of basis points higher on the EBIT margin. We have projected ca. €1.5 billion of adjusted EBIT in FY2026. We value Alstom at 12x EBIT'26e at €18.4 billion. We discount this EV to the present at a cost of capital of 8% (3% risk-free rate, beta of 1, and 5% Equity Risk Premium), and we get an EV of €14.6 billion. We subtract €2.7 billion of net debt and other EV adjustments and arrive at an equity value of €11.9 billion, and a share price of €31 or ca. $34. This implies a 23% upside. Alternatively, we value Alstom at a 5% FCF yield in 2026 (derived from 8% cost of capital and 3% terminal growth rate), arriving at an EV of €15.6 billion in 2026. We discount that to the present and get an enterprise value of €12.4 billion, and an equity value of €9.7 billion, which is equal to the current share price.

{kind=link}

A blended valuation implies a share price of €28.2, or $31, i.e. only 12% upside. We rate Alstom as a "Hold". We will closely monitor the integration of Bombardier, execution of zero-margin contracts, margin progression, credit outlook, and free cash flow generation. If the company faces these challenges deftly, the equity will surely become more attractive, and we will revisit the name.

For further details see:

Alstom: Compelling Narrative But Hold