ALSMY - Alstom: Keeping Pace With The S&P 500 And More

2023-06-21 05:19:45 ET

Summary

- Alstom, a French industrial/infrastructure company, is considered a strong long-term investment despite some issues.

- The company is capable of handling mega-projects in the rail segment and is a key player in transportation and infrastructure.

- Alstom has outperformed the index since the last article, further confirming the positive outlook on the company.

Dear readers/subscribers,

I started writing on Alstom ( ALSMY ) over a year ago. The company is an attractive industrial/infrastructure business out of France, and next to companies like Siemens ( SIEGY ), one of the most relevant transportation and infrastructure businesses on earth. It's one of the few companies that can handle infrastructure mega-projects in the rail segment, and despite some issues that have been relatively clear for a few years, I still consider Alstom likely to outperform over the longer term.

Whenever an investment beats the index, it's worth noting. Alstom has beaten the index since my last article , which continues to confirm my positive thesis on the company.

In this article, I'll update you on Alstom and what I expect for the business going forward in the next few quarters. There's no doubt to me that we're in for a rocky period in infrastructure and construction overall - there are plenty of talks of layoffs here in Europe, and I expect things to remain volatile for at least 2-3 years.

This both means that we need to have a respectable investment timeframe when we go in here, but also means we can expect significant returns once things turn around - which I believe they will.

Alstom - Plenty to like, despite challenges

After over a year of covering Alstom, going through their financials, and projecting their data with better and better estimates, I can confidently say I'm getting better at seeing where things might go here. I believe this is one of those global transport companies you really want to end up owning at some point. The reason is that the fields of transportation, signaling, and locomotives aren't going anywhere, and this company is a market leader here.

Market leaders, provided they don't screw around or come with massive risks, are usually good investments. Even in turnaround cases, there's a lot to like here.

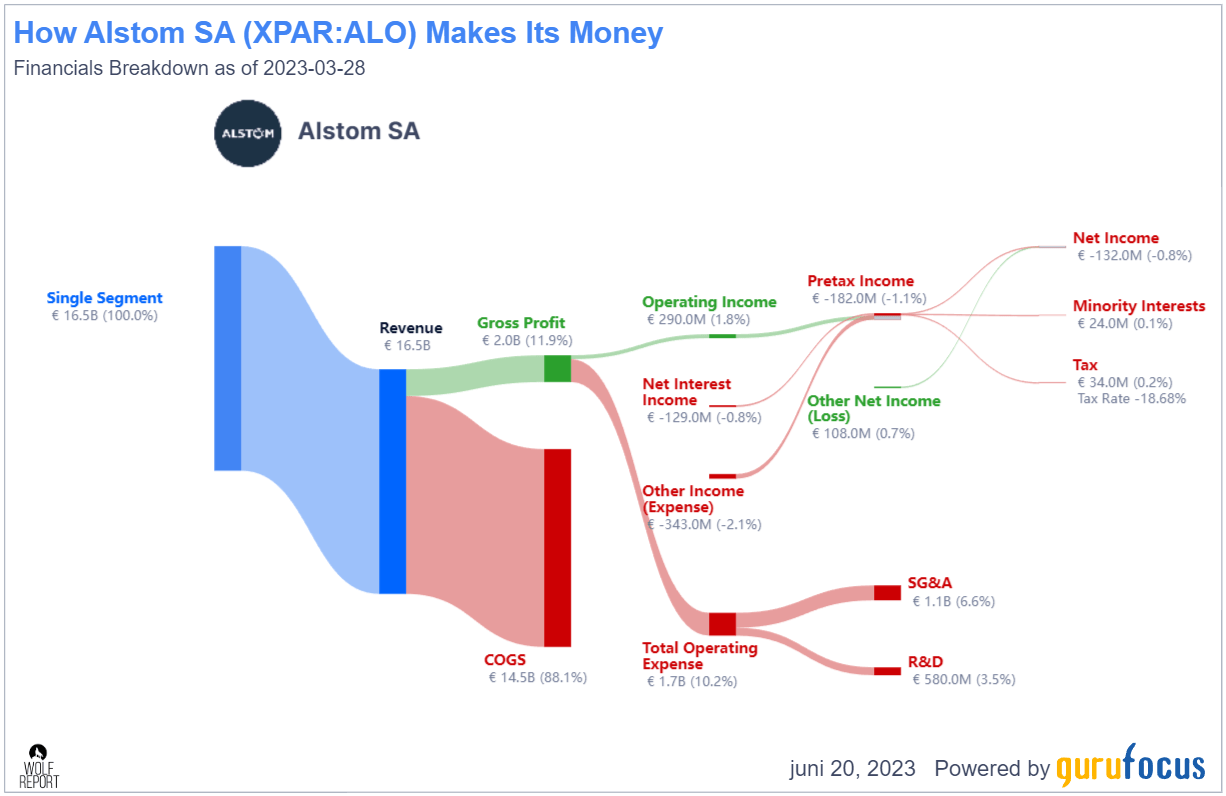

While Alstom isn't currently any sort of margin leader in the field, it's nonetheless a profitable business that manages to go from top-line to bottom-line and usually comes out with a decent net income. Not lately - the company is still working through legacy contracts with very poor margins. This has impacted COGS, which is currently at 88.1% for the 2022 revenues - well above where it should be for any company, I don't care what sector they're in.

{kind=link}

But as I see things, these impacts are temporary. The company is in a turnaround, and once they do a turnaround, the company will see good profitability once again.

Alstom IR (Alstom IR)

The company doesn't have the best past since 2000, but let's focus instead on what we can expect going forward. The French native ALO ticker is the one you want to invest in if you can.

The company has a sub-1% yield, and its valuation is being vastly underestimated due to history, rather than forward estimates. Why?

Because on a forward basis, the company is expected to grow by double digits per year. 21% per year by FactSet to be exact - 18-20% by me, for the period until the 2026 fiscal.

The company is far from the easiest business to analyze. Why? Because the company doesn't provide us with segment data. That means we have to guesstimate based on knowledge of the sector which, while extensive, is going to be imperfect. So going into Alstom, realize the higher degree of volatility you're going to end up with.

The company reports things going well.

{kind=link}

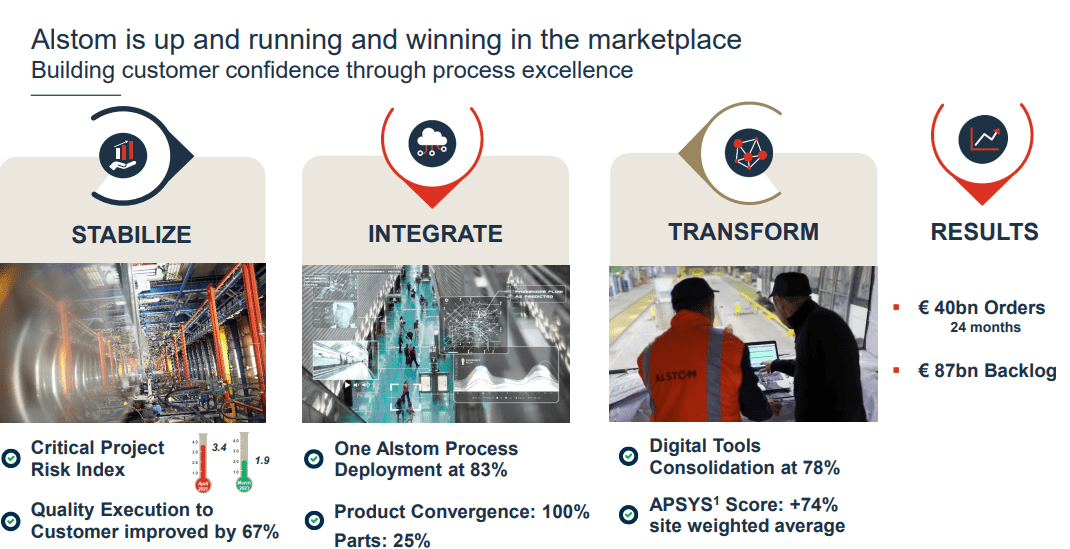

There is extensive proof, to me, that the company is "winning". Its order flow and the interest in services speak for themselves, as does the process of getting the old out of the way. The integration of processes is on its way, and we're already seeing results.

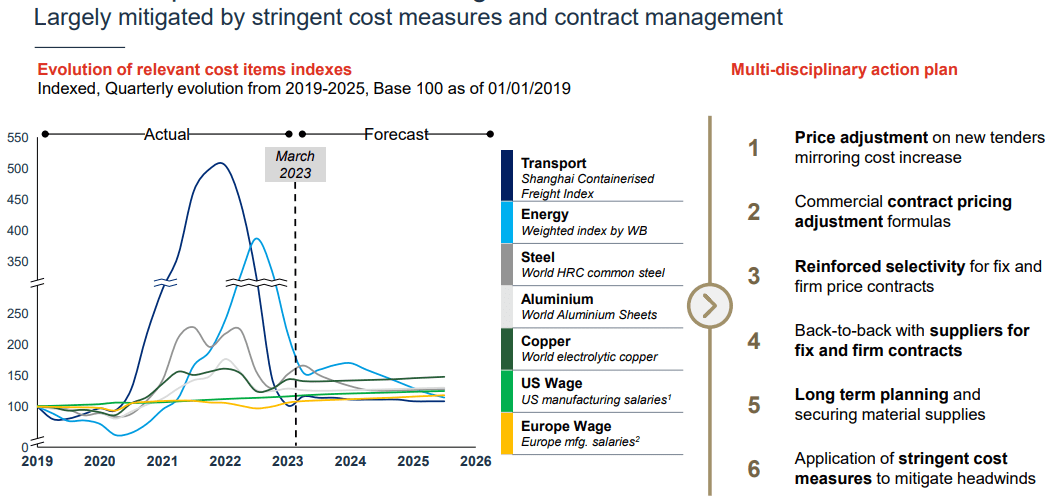

And in terms of impacts from inflation on material and wage costs, Alstom is actually managing them better than most companies.

{kind=link}

Customer satisfaction for the products is high, and the fact it controls its own global supply chain with a multitude of suppliers - over 22,200 of them - means the company is once again less exposed.

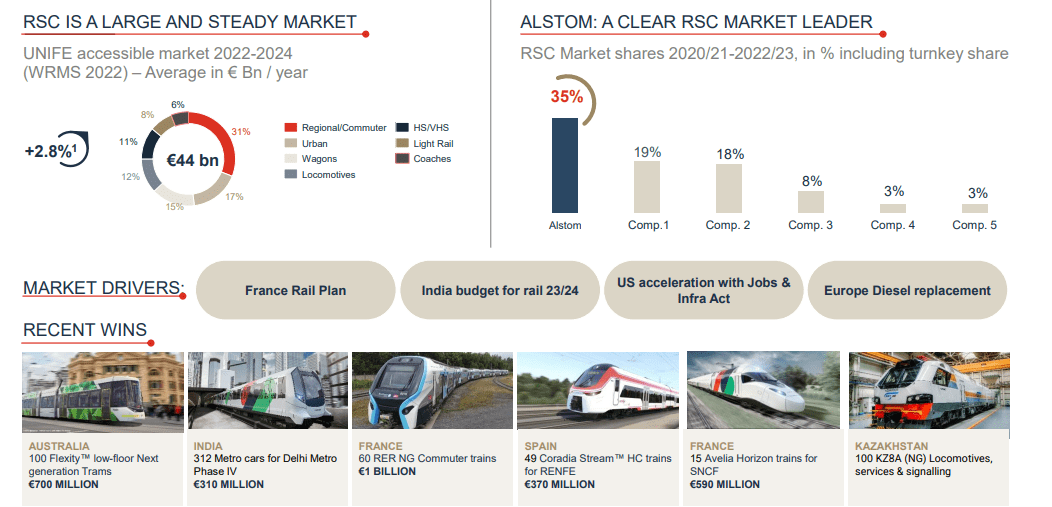

To say the company has reached its goal is going way too far. They haven't - not yet. But to say the company is up and running, and on "track", that's accurate. There are enough improvements for me in Alstom to increase my conviction in my bullishness on the company, especially with Alstom's market position in key areas like Rolling Stock & Components.

{kind=link}

This is a global and diverse market. Alstom's past makes the company appealing for most geographies to work with, and it scores contracts across the world, with representation across all continents. It even manufactures its products on every single continent on the planet to some degree.

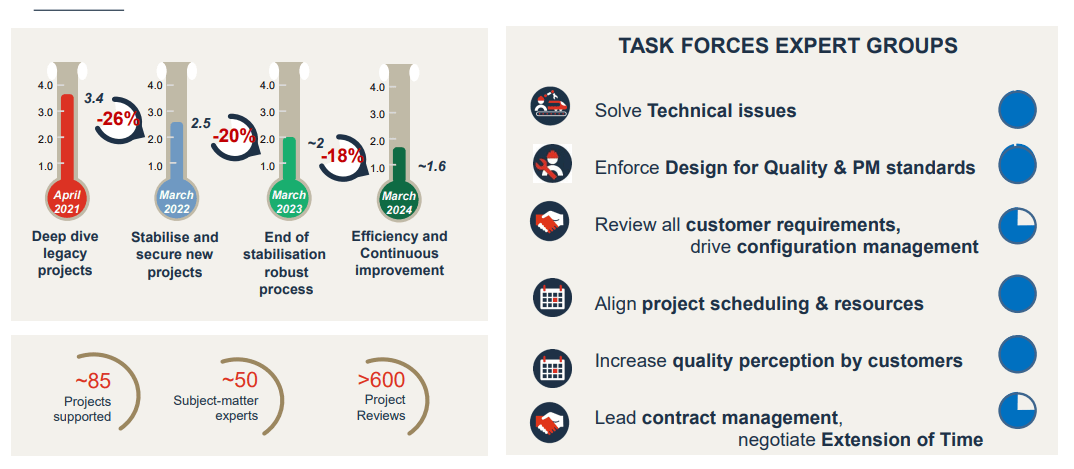

The main issue with Alstom continues to be project stabilization, and this is mostly rolling stock/components, or the RSC segment. The company expects to be mostly done with this by this time next year - and we're already "in the green", so to speak.

{kind=link}

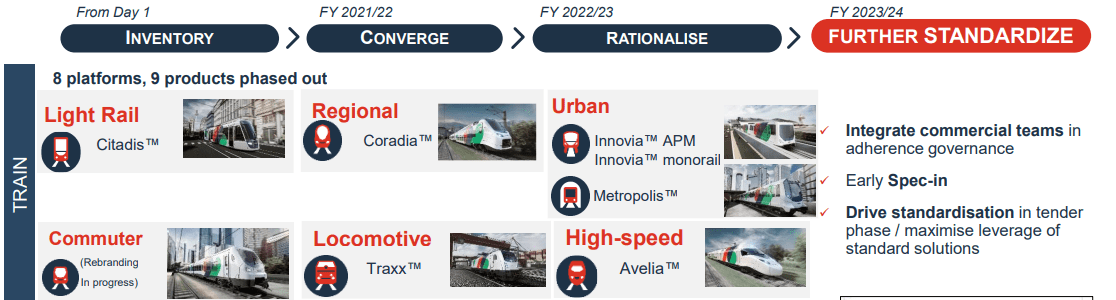

In fact, the company's task forces are already now switching towards new, non-legacy contracts. We'll be seeing impressive trends, I believe, in the next few years, and this is only the beginning. The company has market leadership thanks to its platforms no matter what the customer need is. It doesn't matter if its Light Rail, Regional, Urban, Commuter, Locomotives, or High-speed - the company can fill any need with its current portfolio, and they do so well.

{kind=link}

Standardization has been the name of the game for a few years now, and the company is well on its way, with 35 active products and 20 reference solutions in one segment, which is a reduction of over 47% in converters, and -42% in Bogies references in another.

This in turn reduces product defects, demerits, and safety issues, while increasing deliveries on time, throughput in manufacturing, and on-time reviews. The company has started walking - and it's about to start running.

{kind=link}

In 2023-2024, I consider it extremely likely that this start-up of synergies and positives will translate into an acceleration of the journey, with more profitable contracts, getting the best footprint and scale in terms of manufacturing (massification and specialization). This also, obviously, means significant R&D expenses to increase both quality and safety - but this is of course a given here.

The services segment is also delivering good growth - with Alstom being a market leader in terms of size, is by far the largest in sales by almost a billion euros to competitors. The contracts we're seeing now are also far more favorable than legacy and historical ones because customers are increasingly bundling tenders with both rolling stock and associated service contracts - and Alstom wants 35% of the company's base under active service contracts.

Overall, Alstom remains a fundamentally attractive business hounded by the fact that it's still getting its house in order. While initially there might have been some doubts about the timing of this, I now have a high conviction that in 2024-2025 we'll see double-digit EPS improvements and margin improvements as legacy drops off and we can focus more and more on better contracts and trends. The company's scale also makes them a first choice, being able to better compete globally, and every single market the company is in is seeing positive overall trends.

Let's look at company valuation.

Alstom - The valuation remains compelling

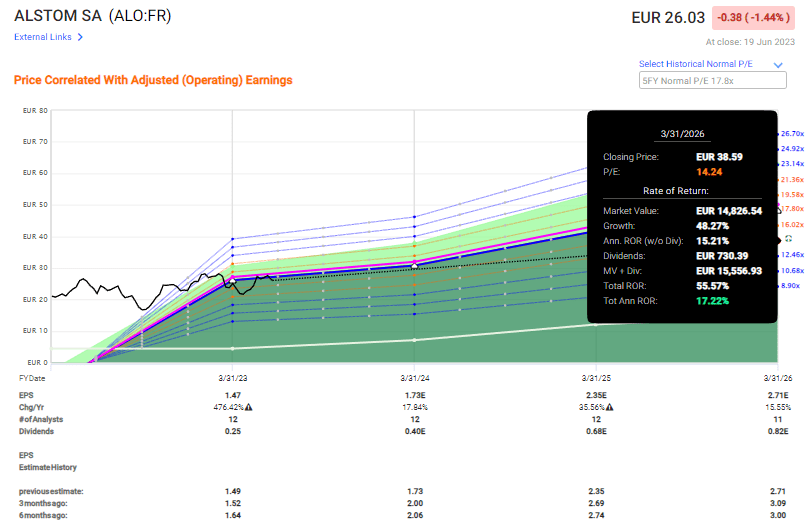

I've written about this company a few times now. Alstom remains an investment I consider to be attractive. I've successfully sold cash-secured puts, as well as bought common shares of the company. The company currently trades at a 2023 average weighted P/E of around 16.5x, which for a company that's estimated to grow 21% every year is on the low side.

As I said, I consider this growth to be realistic. But if you want, you could forecast Alstom at a 15-16x P/E, heck even 14.2x, and based on current growth estimates, you'd still handily beat the market here.

Alstom forecast (F.A.S.T graphs)

{kind=link}

I am far from the only positive analyst of this name. Alstom remains well-covered in Europe, and 18 analysts follow the company, with 14 of them at "BUY" or "Outperform" ratings. The current price of €26/share is only indicative in the short-term of what this company is capable of doing. My PT for the company is €36/share as of my last article, and I see absolutely no reason to change this as of this particular article.

€36/share doesn't even represent a 14x 2026E P/E. The company might well be worth as much as €50/share or more once these things normalize, which opens the potential for a triple-digit RoR, especially if you're able to invest early on in the company with a price lower than the current one.

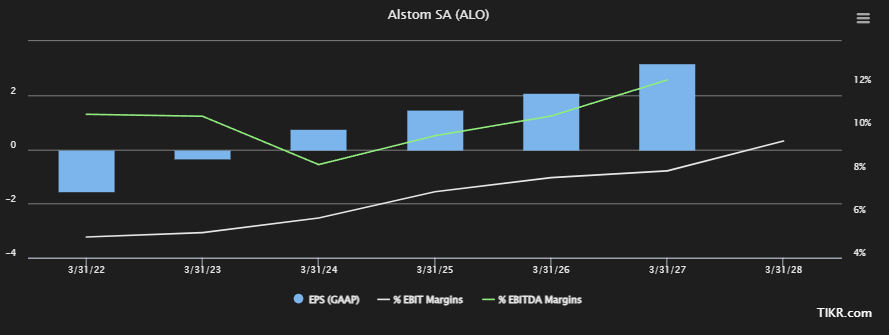

Improvements are expected across the board. EBITDA margins, EBIT margins, EPS - it's all there.

Alstom Expectations (Tikr.com)

{kind=link}

Even if the specifics of this increase might turn out differently, I believe the direction of the overall company is correct here - and that makes it a "BUY" for me. I expect considerable continued margin pressure until after 2022 relating to Bombardier Transport, but not after 2023 , after which I model for a margin increase, and when other analysts are doing the same for this business.

As I said in my last article - I could nitpick here and go down slightly to account for the somewhat longer ramp-up - but now we're in June, and I don't believe in nitpicking or cent-changing in my price targets. So I'm sticking with my general price target here.

Thesis

- Based on long-term positive business fundamentals from a combined rolling stock/service/turnkey business and added to by urbanization in the emerging markets, the future trends for Alstom are likely to be positive. Pushes for green services and marketing are likely to enhance this even further.

- The company's focus on improving portfolio margins and moving to higher-margin segments such as signals/services is likely to benefit the company in the long term.

- I view the company as a "Buy" with a PT of €36/share.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ):

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills every single one of my requirements and therefore warrants a "Buy". I still maintain that despite the recent surge, the company is actually cheap for what it offers.

For further details see:

Alstom: Keeping Pace With The S&P 500 And More