AOMFF - Alstom: Plenty To Like At This Valuation Apart From Positive RoR

2023-08-14 22:25:00 ET

Summary

- Investing is becoming more challenging with rising interest rates and the need for higher returns.

- Alstom, a market leader in transportation, has strong fundamentals and potential for growth.

- The company's valuation is attractive, with the potential for significant upside even at a discounted price. I continue to see an upside for Alstom here, my target is €36.

Dear readers/followers,

Investing is getting trickier. We're in a situation where interest rates are not only rising, they're very likely to remain high for a longer time. By that, I mean above 4-5% for a minimum of 2-4 years. This influences what we should invest in. Logic dictates that if we can get 5% risk-free, then we shouldn't be investing in companies that have single-digit realistic upsides annually. Yet this is still what some people insist on doing. You have to shift your modality here, and realize what you're missing out on, or what could happen if you invest "incorrectly."

That's why my minimum requirement for putting serious capital to work is a conservative 15% annualized RoR on the upside. That needs to be 100% realistic, and it needs to be either growth, yield or preferably a combination of both.

Alstom ( AOMFF ) at one point had such an upside to give us.

In this article I will show you whether the company still has this, and if it does, why that is the case.

Let's get going.

Alstom - The fundamentals remain superb.

I last covered Alstom about 2 months back ( Source ). The company has given me double-digit RoR in a very short time, allowing me to outperform the market with my investment. This is always welcome, because that is after all what I go for. I'm never bugged when investment takes a bit more time to realize the upside - though I will look at these to see if something has changed.

When it comes to Alstom though, I really believe that there could be more to be had here.

I've been covering the company for over a year at this point, and I always want to reiterate when it's about a company like this, that this is a business you want to own.

It's a market leader. Market leaders at cheap or acceptable prices are never a "bad" idea unless something fundamental seems likely to change. I believe this is one of those global transport companies you really want to end up owning at some point. The reason is that the fields of transportation, signaling, and locomotives aren't going anywhere, and this company is a market leader here.

While I realize in full that American investors may look at this and go "Really, trains?" - yes, anywhere except North America and the USA specifically, train logistics are not only solid, they are the future.

They are by far the most effective (both in cost and other ways) ways of transporting goods, where it's possible to use them. That's what we've seen in Europe, and also in Asia. Africa is also developing its train network, and South America as well.

That makes Alstom, being a market leader in key segments, one of the best players here. It's a player in the midst of a turnaround, yes , but that turnaround is now nearing its end.

And I also don't want to give the impression that Alstom isn't in NA - it is. Just take a look at this 4-day-old piece of news, that Alstom is to supply 60 single-level coach cars to the Connecticut Department of Transportation for its statewide rail system. ( Source )

The company isn't just intermodal - it does this sort of business too, and that's an order worth €300M. A drop in the bucket for Alstom, but enough drops coming down, and it's raining - same with dividends.

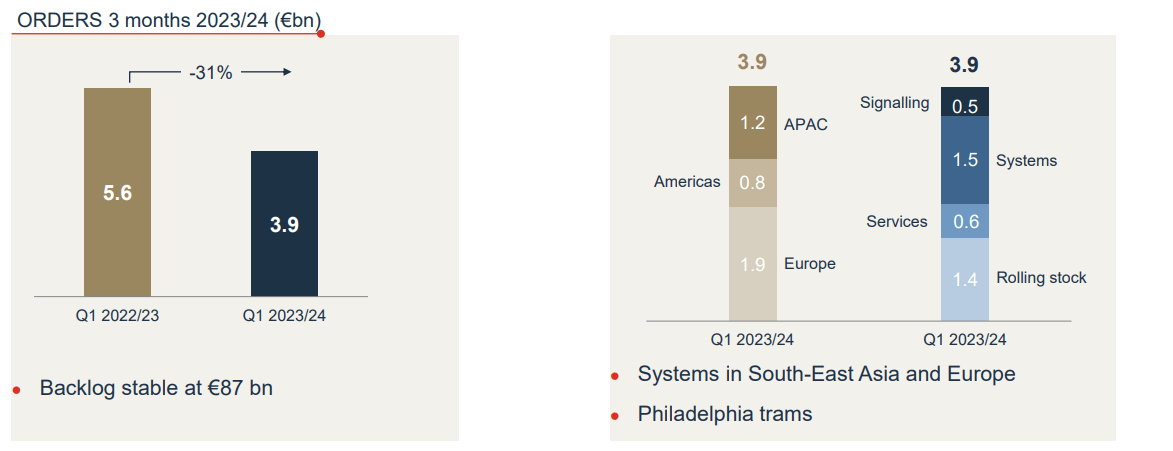

The last set of financials we have to sink our teeth into is less than 3 weeks old at the time of writing this article. While 3-month order trends are in decline, this is only part of an order normalization. In effect, this confirms the company's rolling 3-year pipeline, at order values of €220B , with a current backlog of over €85B.

{kind=link}

Main orders for the quarter include the Septa Urban Light Rail, with orders from the US, a Turnkey NSCR system order in the Philippines, and a metro system with the CLUJ Metro cars in Romania. These orders mean, valued at almost €4B alone, mean that the company can confirm a book-to-bill of over 1x for the quarter.

The company is preparing for the demand to increase. On a segment basis, we have growth in almost every segment - Rolling Stock up 5%, Services up 5%, signaling up 13%, and Systems down 16%. Systems though is by far the smallest segment, being less than 15% the size of Rolling stock as a segment.

The company's financial trajectory remains solid - and this is what I'm looking at. I'm waiting for this company to see significantly positive FCF, with an adjusted EBIT of above 5%. The company is set to deliver that for the full fiscal which it started now, while targeting an adjusted pre-tax margin in the double digits by 2025-2026, and an FCF conversion of above 80% in the same timeframe.

The issue, as I've said earlier, is that Alstom does not share segment-specific margins. We don't really know what segments are performing and which aren't, which makes it hard to really model the company on any sort of realistic level. This is also part of the reason why analysts have such a dismal accuracy when it comes to where this company is going. With a negative miss ratio of almost 60%, forecasts just don't tend to work for the company, and as long as the company doesn't give us these details, I, along with other analysts, need to severely discount the company in order to avoid exuberance in expectations - though far fewer analysts do this than they currently should.

The company is cyclical. No amount of service segments will take this away from Alstom.

However, if you look at anything else , the company is really doing well. Customer satisfaction for the products is high, and the fact it controls its own global supply chain with a multitude of suppliers - over 22,200 of them - means the company is once again less exposed.

Like other companies in the same situation, Alstom's main issue is reported and also confirmed to be project stabilization. We're still maybe 8-12 months away from Alstom being done with the legacy RSC orders, at which point the overall project margins will not only normalize but grow.

It all goes against my usual stance when it comes to investing. Patience. I don't invest my capital lightly - all my investment decisions are based on hours and usually over a week of research. That's why I, for instance, don't invest much in BDCs yet. I haven't done the work on them yet, and I want to understand what I invest in.

For Alstom, I understand the high level very well - and I see the trends we're moving to. From massive standardization not only across major product lines but in every SKU when it comes to parts and products.

Alstom IR (Alstom IR)

The net result of this is more customer satisfaction as product defects go down, safety issues go down, manufacturing throughput goes is improved, as well as on-time deliveries. I've worked as a manager in enough manufacturing units to know that while non-standardized or custom orders sometimes are necessary, 95 times out of 100, it's better to either stick to standard or skip the order - though this is my personal experience.

However, the trends for Alstom here are clear. These improvements, together with the turnaround, together with RCS legacy contract dropoffs, will likely result in a company cyclical upswing.

It's my conviction that this will result in more Alstom RoR, and that's why I'm neither selling nor stopping my buying here.

I'm buying more Alstom.

Alstom's valuation - remains very attractive here

You may recall that I set Alstom at €36/PT in my last article. I am not changing this price target here.

That high, you may ask - to which I would say "Yes, that high".

The company has not begun to see its reversal potential. If we really see a growth in earnings the like that's being forecasted - and I believe it to be likely given the underlying trends the company is reporting and where we are in terms of macro, then we still have 15%+ annualized here, even at discounts.

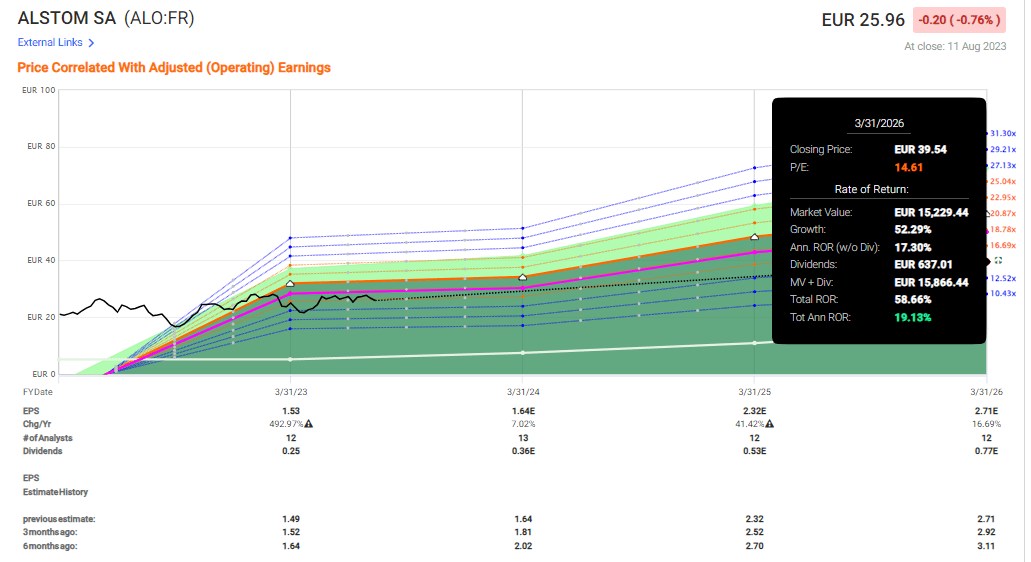

So, you tell me you don't want to offer Alstom its historical premium of over 17-19x P/E - that is too high for a company that is this cyclical. That's fine.

How about a 14.6x P/E instead?

{kind=link}

Because even at sub-15x P/E - and by the way, you could go to 12.5x and still get 12% annualized - as well as a sub-1% dividend yield, which is probably my biggest problem with Alstom at this time, you're still having market-beating upside potential.

At 15x P/E, we're massively discounting Alstom. A full reversal to 17-19x P/E would imply upwards of 35-38% annualized, or triple-digit RoR, despite substantial valuation improvements since my first article.

This, dear readers, is why I continue to be positive about Alstom. Why I believe that you should invest in the native ALO ticker if you have the means and like this company, and share my view on its upside. It really makes for what I believe to be an excellent future investment.

Alstom's analyst targets are somewhat lower than my own. That's fine., The company has 17 analysts, but 14 of those are at "BUY" or equivalent positive stance, with a target range starting at €22.5 and going up to €38, with an average of €32. I continue to see analysts as underestimating this company's potential in a big way. Why do I say this?

Because less than a year ago, there were analysts that literally argued the company was worth €15/share. Now they're up more than 40% in those valuation estimates. They were factually wrong. I continue to believe they are wrong, and I say €36/share is the least we should expect from this company.

I've been through the company's financials and reporting - what does exist - several times. I do not find any scenarios that I consider likely long-term where a downside seems likely over the long term. Not with these trends.

That's why I believe in Alstom's outperformance here.

Thesis

- Based on long-term positive business fundamentals from a combined rolling stock/service/turnkey business and added to by urbanization in the emerging markets, the future trends for Alstom are likely to be positive. Pushes for green services and marketing are likely to enhance this even further.

- The company's focus on improving portfolio margins and moving to higher-margin segments such as signals/services is likely to benefit the company in the long term.

- I view the company as a "Buy" with a PT of €36/share.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ):

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company fulfills every single one of my requirements and therefore warrants a "Buy". I still maintain that despite the recent surge, the company is actually cheap for what it offers.

For further details see:

Alstom: Plenty To Like At This Valuation, Apart From Positive RoR