ALTG - Alta Equipment: Debt And Control Concerns Mitigate The Gains From Acquisitions

2024-01-12 06:33:10 ET

Summary

- Alta Equipment takes the acquisition route to drive growth and has seen success in expanding into new territories and markets.

- Supplying equipment for infrastructure and residential & nonresidential construction markets have seen high demand in growth.

- Pricing concerns, ineffective internal controls, and a leveraged balance sheet are potential risks for the company, but its stock is reasonably valued compared to peers.

ALTG Has A Trade-Off

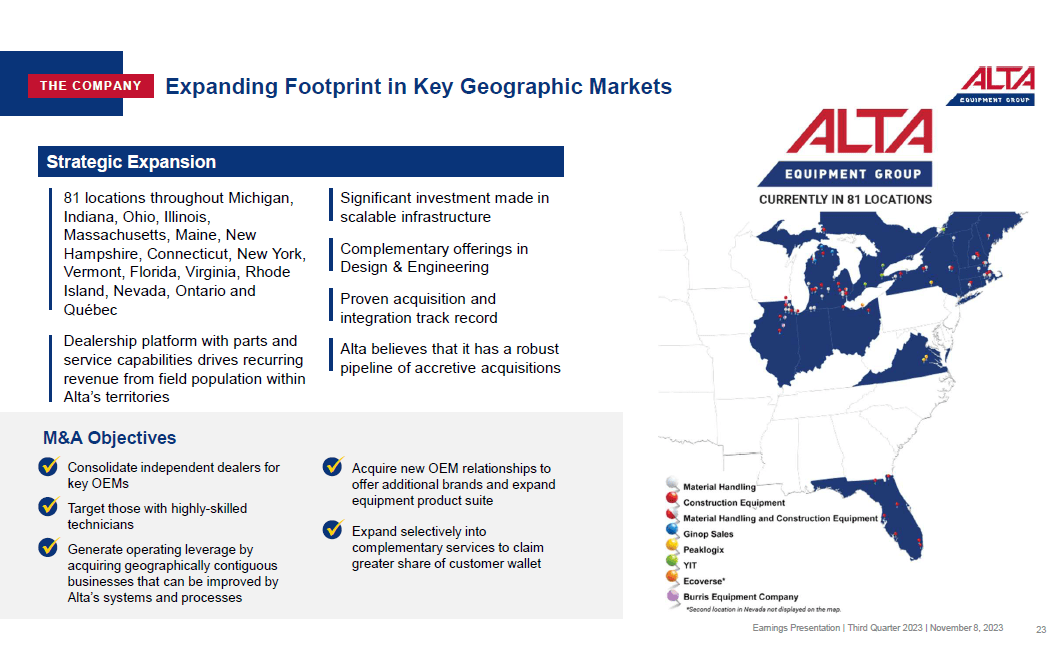

Alta Equipment Group (ALTG) is a dealer in the US and Canada that sells and provides equipment parts and support services. Its equipment portfolio includes lift trucks, heavy and compact earthmoving equipment, environmental processing equipment, and other material handling and construction. Currently, it operates through ~80 full-service locations across 14 states. It also has 800 field service vehicles.

The company recently entered Pennsylvania to gain market share in the residential & nonresidential construction markets. Following geographical diversification, its forklift and material handling equipment backlog soared. The company has been using acquisitions to pivot growth over the years. In late 2023, it acquired two companies that also gave it entrance to the Canadian market. The M&A strategy also bolstered its cash flows and deleveraged the balance sheet.

However, I think, pricing will remain a concern in the near term, particularly in the construction and material handling business. One notable risk in its management relates to its ineffective internal control, which can raise corporate governance issues. The company's balance sheet is also leveraged. Nonetheless, a 28% drop in share price over the past six months keeps the stock within a reasonably valued range compared to its peers. So, I assign a "hold" rating to it.

Identifying Key Drivers

Alta Equipment's Q3 2023 Earnings Presentation

{kind=link}

At the close of 2023-end, ALTG looks to expand into new territories, including scrap and demolition markets, power generation, large-scale mining operations, and turf and maintenance. As the supply chain improves, a better demand environment persists, leading to a higher demand for material-handling equipment.

Recently, the company entered Central and Western Pennsylvania through the dealer CASE Power & Equipment of Pennsylvania. Going forward, it plans to expand its central Pennsylvania operations in 2024. Here, it will look to serve the infrastructure and residential & nonresidential construction contractors by providing compact and subcompact equipment. It will also provide associated services like captive financing, planned maintenance solutions, and telematics and parts support.

Acquisition Strategy

Alta Equipment's Q3 2023 Presentation

{kind=link}

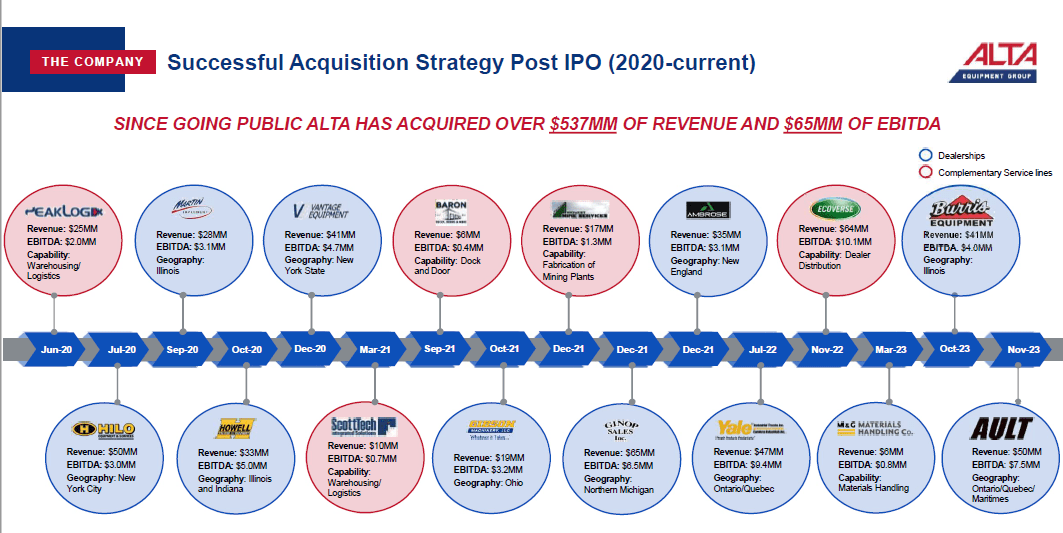

In November, ALTG acquired Ault Industries, which marked the company's first investment in the Construction Equipment segment in Canada. The acquisition provided exclusivity with an existing installed base and the potential to grow through infrastructure investment. In October, it acquired Burris Equipment Company, which supplies compact construction and turf equipment in Chicago. The company estimates that the compact segment of the construction equipment market has outgrown many other segments.

{kind=link}

Acquisition is a key part of ALTG's growth. Its M&A policy encompasses consolidating independent dealers, generating operating leverage by spreading into contiguous geographies, offering additional brands and product suites, and expanding through complementary services. Since its IPO in 2020, it has acquired around 16 companies and dealers, resulting in $537 million of additional revenue and $65 million of EBITDA.

Its revolving credit-based capital structure and positive cash flows provide opportunities for M&A-centric growth. On top of that, positive cash flows help reduce leverage its profile and boost liquidity for further investments.

Industry Outlook

{kind=link}

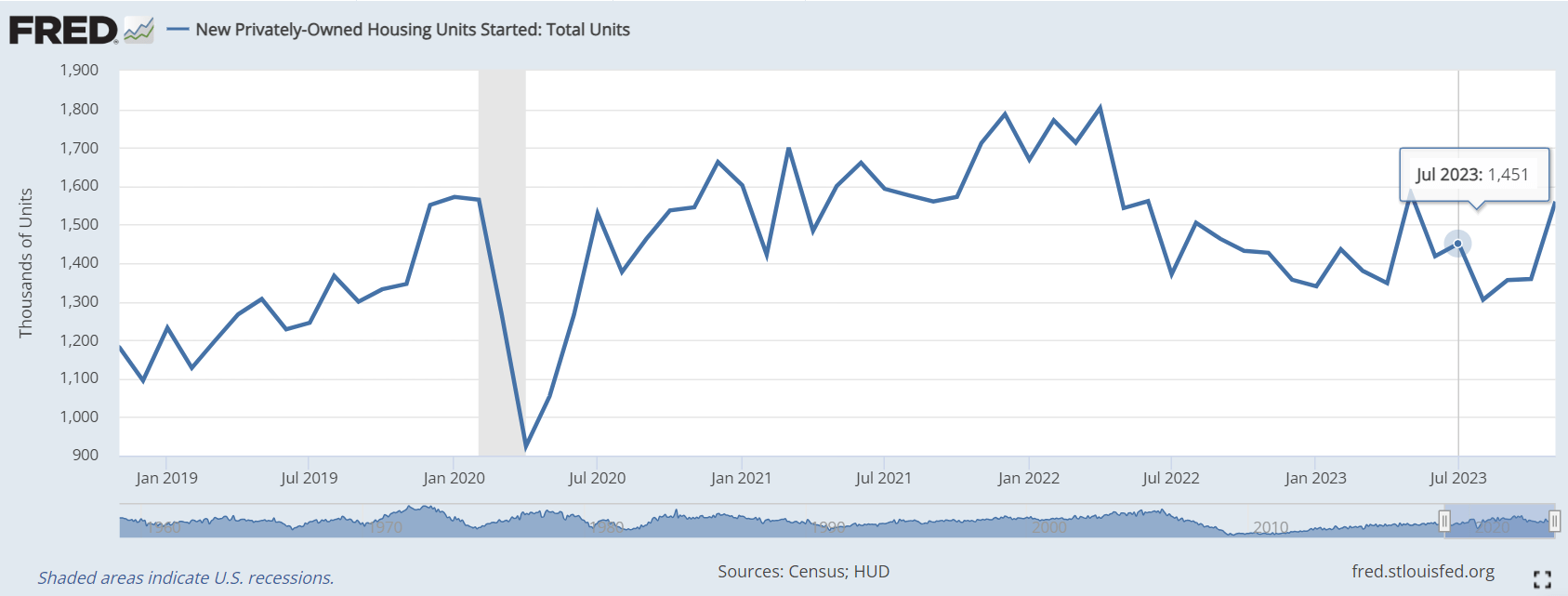

Let us check out the construction market in the US to get a sense of the end market growth. New "privately-owned housing units started" units increased by 15% year-to-date until November 2023 after remaining relatively unchanged in the past few months, indicating a recovery.

In December, the ISM Services PMI fell to 50.6 compared to 52.7 in November. Sloppy new order growth, low employment, and inventory contraction led to the fall. So, the economic indicators are quite mixed at the end of 2023.

The Backlog Push

ALTG goes into 2024 with a robust backlog of forklift customers and material-handling equipment. This will provide strong visibility on equipment sales in Material Handling. As the company diversified geographically, its backlog soared in the commercial side, aggregates, and mining. In the Construction segment, the macroeconomic factors can change in 2024, leading to better operating performance.

However, the company will continue to see headwinds and moderation in specific segments, e.g., the Construction and Material Handling portfolio product segments and retail used equipment. Pricing in these markets has decreased recently and may continue to be a downtrend in 2024. Utilization, too, has remained low, although rental rates were 6% higher in Q3 2023.

The Q3 Drivers

{kind=link}

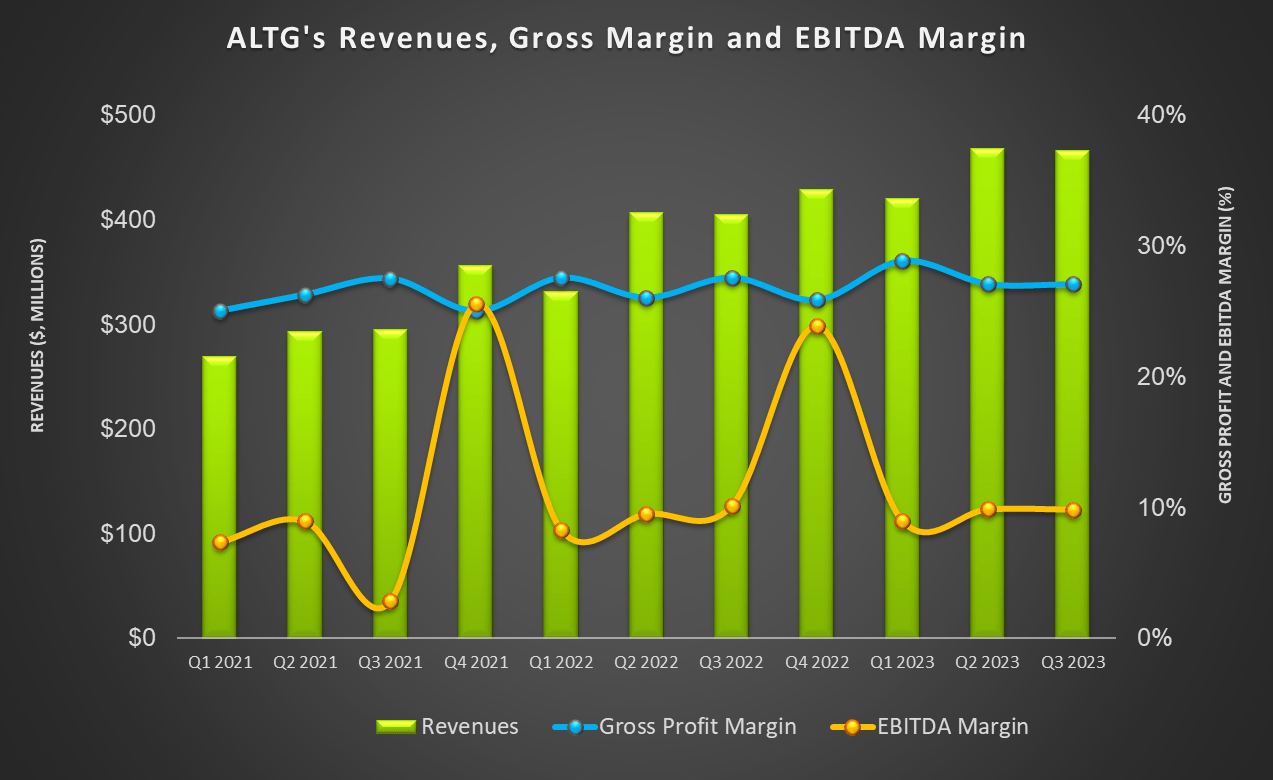

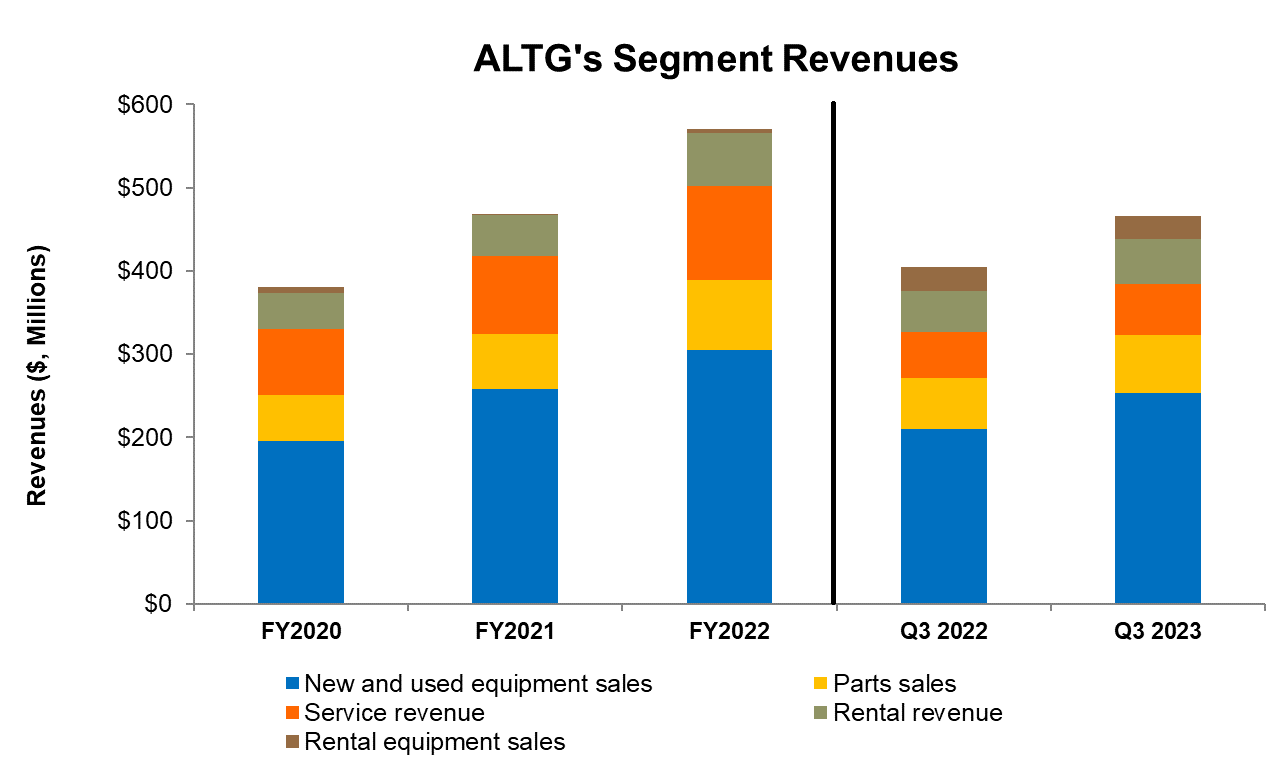

Although the macroeconomic environment remained weak, ALTG's Construction segment was resilient due to its market diversity. The construction market in Florida was strong in Q3 as the company expanded its reach beyond road, commercial, or housing projects. ALTG's New and Used Equipment Sales, which accounted for 54% of the Q3 revenues, increased by 21% in Q3 2023 compared to a year ago. The segment's gross profit margin remained steady over the past few years.

Higher equipment sales and growth in high-margin parts and services can increase product support revenues and gross margins in the coming quarters. In Parts sales and Service segments, revenues increased by 12% year-over-year in Q3 2023. However, gross margins were contracted during this period in Part sales, Rental revenue, and Rental equipment sales.

Cash Flows And Debt Level

In 9M 2023, ALTG's cash flow from operations (or CFO) turned negative from a healthy CFO to a year ago. During the first half of 2023, the company aggressively replenished inventory, which put pressure on working capital and led to a redeployment of floor plan lines. However, the situation appeared to ease in Q3 and should continue to improve in Q4 as supply chain issues are resolved. Free cash flow (or FCF) turned more into negative territory in 9M 2023 compared to a year ago.

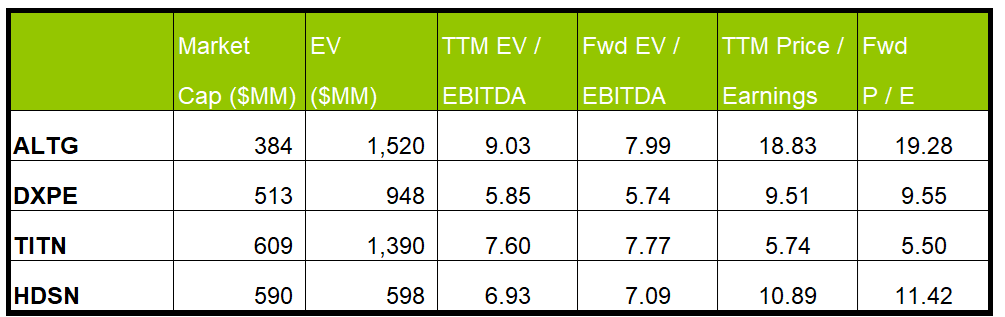

ALTG has a higher debt-to-equity ratio (6.7x) than some competitors (DXPE, TITN, HDSN). Its liquidity (totaled $206 million as of September 30, 2023. Negative cash flows and high leverage can aggravate investors' concerns and render investment in the stock risky.

Relative Valuation

Author Created and Seeking Alpha

{kind=link}

ALTG's forward EV/EBITDA multiple contraction versus the current EV/EBITDA is steeply higher than its peers, which typically reflects in a higher EV/EBITDA multiple than peers. Its EV/EBITDA multiple (9x) is higher than its peers' (DXPE, TITN, and HDSN) average of 6.8x. So, the stock is reasonably valued versus its peers. It is also trading at par with its past five-year average.

If it trades at the past average in the medium term, it can climb 32% from the current level. However, its value drivers do not appear to reflect such positive potential. If it trades at the industry average, it has 60% downside over the next year. I believe the stock can decline marginally in the short term but can pull through moderate (10%-15%) returns in the medium term.

Wall Street Rating

{kind=link}

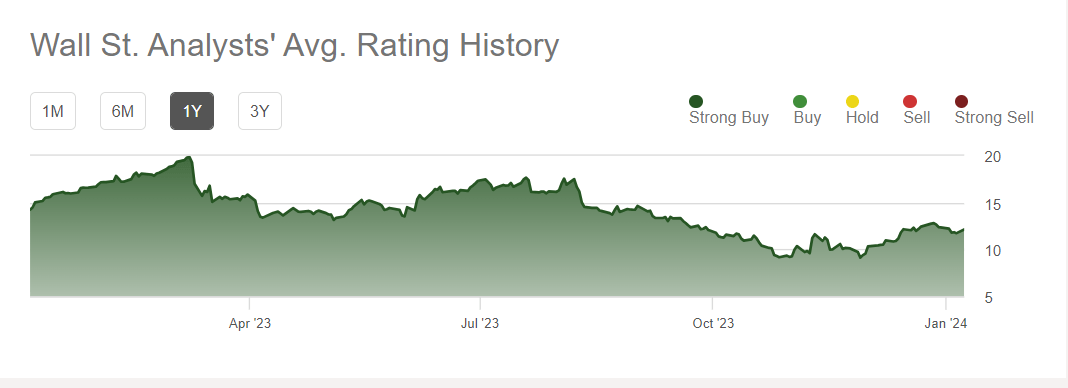

Four sell-side analysts have rated ALTG a "buy" (including "Strong buy.") None of the analysts rated it a "hold" or a "sell." The consensus target price is $22.3, suggesting an 84% upside at the current price. Given the risk factors and the operational challenges, I think the Wall Street analysts are overestimating returns.

Risk Factors

I see a few critical risks, including one relating to the company's business environment and the other relating to its internal affairs. ALTG operates in a highly competitive and fragmented industry. Its competitors vary from national to multi-regional operators, especially small and independent businesses. So, it is difficult for the company to pass input cost increases to its customers. The price stickiness can adversely affect its operating margin. We saw similar events in the recent supply-chain constraint period in the past couple of years. This caused the company's inventory level to swell, increasing the cost structure.

Similarly, ALTG sources 43% of its products and equipment from four major manufacturers (Hyster-Yale, Kubota, JCB, and Volvo). So, a relationship degradation with any of them could hurt its business.

The other issue was concerning ineffective internal control due to improper information technology general controls since 2021. The issues related to reviewing and authorizing pricing, discounts, sales agreements, and rental contracts. As of September 30, the material weakness remained. In my view, the inability to reconcile these issues for such a long period raises questions over its management's ability.

What's The Take On ALTG?

{kind=link}

ALTG, which supplies heavy equipment and material handling equipment, has started focusing on new markets, including power generation equipment, mining, and demolition. It looks to foray into Pennsylvania as it serves contractors with compact and subcompact equipment. One of its critical growth strategies is M&A, which helped it grow remarkably in new technologies and expanded its brand and product suites. With additional cash flows arising from the acquisition, it reduced leverage over the years. The company has a robust backlog of forklift customers and material-handling equipment.

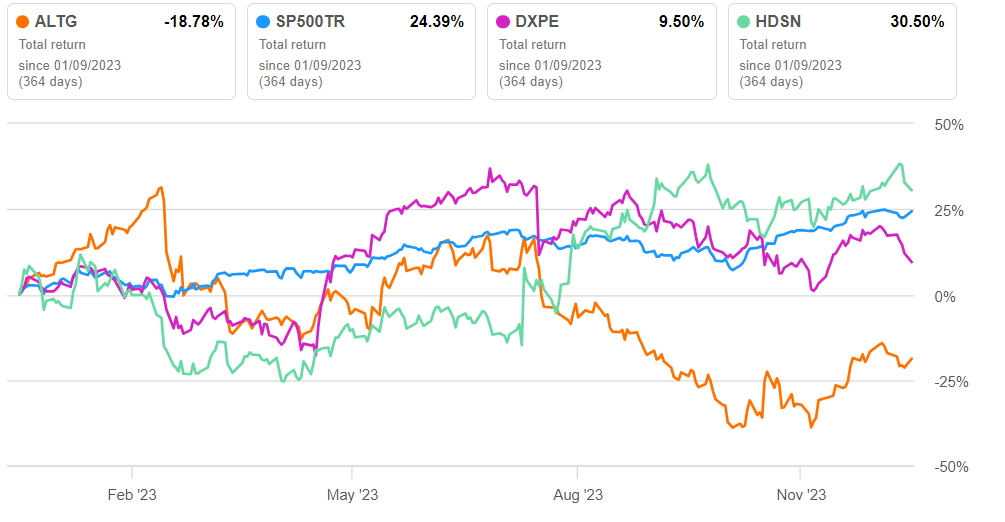

However, the economic indicators are not sufficiently encouraging. After going through a rough phase, the construction industry appears to be recovering in recent times. Adverse supply chain issues caused cash flows to shrink 9M in 2023. It can disrupt the company's deleverage efforts, which can be concerning given its high leverage. The deficiency in its internal control also raises questions over its corporate governance. So, the stock underperformed the SPDR S&P 500 ETF ( SPY ) in the past year. Given its relative valuation multiples, I think the stock deserves a "hold" call.

For further details see:

Alta Equipment: Debt And Control Concerns Mitigate The Gains From Acquisitions